- The paper introduces financial relativity by modeling asset prices as geodesic projections of terminal payoffs onto evolving information subspaces.

- It employs an analogy with general relativity, where the curvature of probability space (induced by information constraints) explains risk premiums and volatility.

- The framework formalizes asset pricing via field equations, unifying risk-neutral and physical measures and offering testable predictions for market dynamics.

Introduction and Motivation

The paper "Financial Relativity: An Information-Geometric Interpretation of Asset Pricing" (2604.03961) provides a formal reinterpretation of asset pricing by leveraging information geometry and constructing an analogy with general relativity. The core critique is the asymmetry and ambiguity in the conventional framework: asset pricing is conducted under the risk-neutral measure Q, whereas economic interpretation is typically referenced to a "physical" measure P. The distinction between P and Q is theoretically convenient but conceptually problematic, especially in contexts of heterogeneous beliefs and incomplete information.

Rather than granting ontological priority to P or treating Q merely as a computational artifact, the paper posits both as probability "reference frames" determined by informational constraints. The key innovation is to model asset prices as projections of terminal payoffs onto information subspaces, with price dynamics analogized to geodesic motion in curved probability geometries—a framework the author terms "financial relativity". This resolves conceptual ambiguities and unifies several strands of pricing theory within an extensible geometric architecture.

Structural Analogy: From Physics to Asset Pricing

The core analogy runs as follows:

- Terminal payoff vectors correspond to objects in spacetime.

- The financial "spacetime" is defined by (time, terminal state space Ω, and filtration Ft).

- Probability measures define curvature: the flat prior P corresponds to flat spacetime; Q is the generally curved geometry shaped by structural informational constraints.

- Price is the orthogonal projection of terminal payoffs onto observable information subspaces—mirroring how events are projected in curved spacetime.

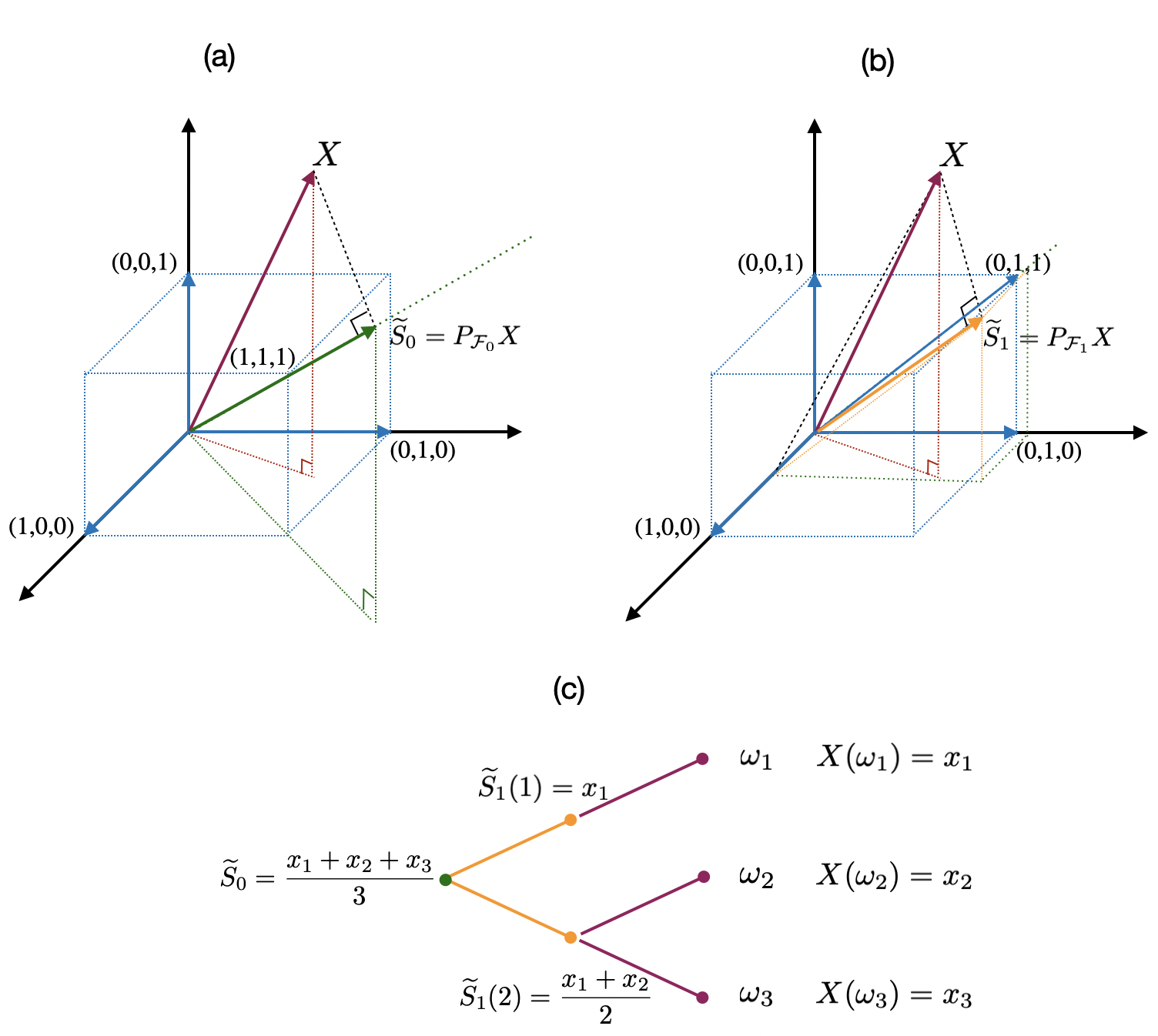

For a finite probability space, prices at each P0 are computed as conditional expectations:

P1

These satisfy the geometric property of being orthogonal projections in the Hilbert space P2, linking pricing relations to geometric structure and reference frames.

Figure 1: Schematic illustration of the discounted price process as projection of terminal payoff vectors onto successively refined information subspaces.

This geometric interpretation underlies a "financial equivalence principle": observed risk premia can be reinterpreted as geometric artifacts due to observing geodesic price motion in a non-natural (i.e., "wrong") reference frame, rather than as compensation for risk per se. The observed drift in returns (risk premium) under P3 arises as an apparent acceleration due to curvature, precisely as in relativity.

The paper's major theoretical contribution is the formalization of probability geometry formation via financial field equations paralleling the Einstein field equations:

- Terminal structural information (constraints, institutional/frictional structure, etc.) induces a geometric potential P4.

- This potential curves the probability geometry:

P5

- The analogy to general relativity is explicit with a prototype field equation:

P6

where P7 is a geometric operator (e.g., Laplacian) acting on the potential, and P8 encodes structural informational sources.

- Maximum entropy is used as a selection principle in incomplete markets to determine which P9 in the set of equivalent martingale measures should be selected.

This structure supports both closed-system (fixed structure) and open-system (dynamically evolving constraints) settings.

Discrete and Continuous Models: Projections, Posterior Geometry, and Price Geodesics

Discrete Model

A worked example in a finite branching structure demonstrates:

- How structural sources curve geometry and induce non-uniform probability weights.

- How price at each time is the projection of the terminal payoff onto the information filtration, partitioning states into observable equivalence classes (price reveals which branch, not the underlying state).

- The information conservation law: total terminal uncertainty decomposes into information revealed by the price process and residual unrevealed uncertainty.

Continuous Model

The continuous-time version models the market as sequentially receiving noisy signals (structural updates):

P0

- Posterior geometry P1 is dynamically updated via a stochastic differential equation akin to a (nonlinear) filtering equation:

P2

- Here, price is again a projection: P3 with P4 the posterior mean.

- Crucially, price volatility is induced endogenously by posterior variance,

P5

so volatility spikes when information is most uncertain (e.g., around events), aligning with empirical patterns in event-driven assets.

A fundamental result is that the manifestation of information in prices is determined by probability geometry and the filtration: price processes are compressed representations, revealing equivalence classes within the terminal partition. Mutual information and conditional entropy supply quantitative tools to measure informational efficiency, connecting directly to generalized tests for market efficiency and the measurement of informational content in prices.

Figure 1: Illustration showing how, as information partitions become finer through the information filtration, the projection of the payoff vector (price) refines its state distinguishing power.

Implications and Empirical Directions

The implications of this framework are substantial:

- Unified Explanation: Event-driven volatility, risk premia, price jumps, and drift are reframed as consequences of geometric structure and reference frame, rather than exogenously specified preferences or risk aversion alone.

- Testable Predictions: Volatility must comove with posterior variance; price drift can arise from reference frame effects; event-induced volatility is the endogenous result of geometry reconfiguration.

- Efficiency Measurement: Empirical work can leverage option-implied distributions, market forecasts, and high-frequency data to reconstruct the evolution of implied geometry, and to empirically test the link between price motion and posterior geometry dynamics.

- Extension Potential: The operator-field formalism supports extensions to jump processes, regime shifts, heterogeneous priors, and interacting field dynamics, bridging to information-theoretic and statistical foundations.

Conclusion

The financial relativity framework provides a rigorous geometric foundation for asset pricing that subsumes the risk-neutral measure as an endogenous product of structural constraints and information, not as an ad hoc transformation of natural probabilities. Price processes are characterized by their geometric projection properties, and volatility and drift are artifacts of reference frames and the curvature of probability space. This unifies and clarifies the organizational structure of asset pricing theory and offers powerful avenues for extension, empirical investigation, and theoretical refinement. The proposal to organize asset pricing around information geometry, projection, and reference frame invariance opens a pathway toward greater internal coherence and deeper structural understanding of observed asset market phenomena.

References

- Lin Li, "Financial Relativity: An Information-Geometric Interpretation of Asset Pricing" (2604.03961)