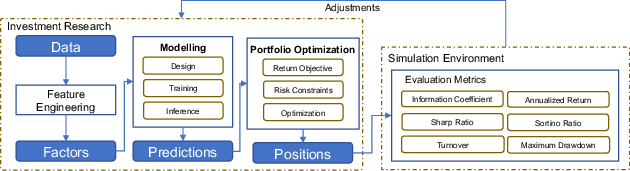

- The paper introduces a comprehensive benchmark platform that integrates data processing, modeling, and evaluation for quantitative finance.

- It leverages evolutionary algorithms, deep learning, and reinforcement learning to optimize factor mining, portfolio construction, and order execution.

- Empirical results show that ensemble and temporal models deliver superior predictive accuracy and robustness compared to hypergraph approaches.

QuantBench: Benchmarking AI Methods for Quantitative Investment

Overview

QuantBench aims to standardize AI methods for quantitative investment by providing a benchmark platform that aligns with industry practices. It facilitates integration of various AI algorithms, offering a complete pipeline from data processing to model evaluation, significantly streamlining the quantitative analysis workflow.

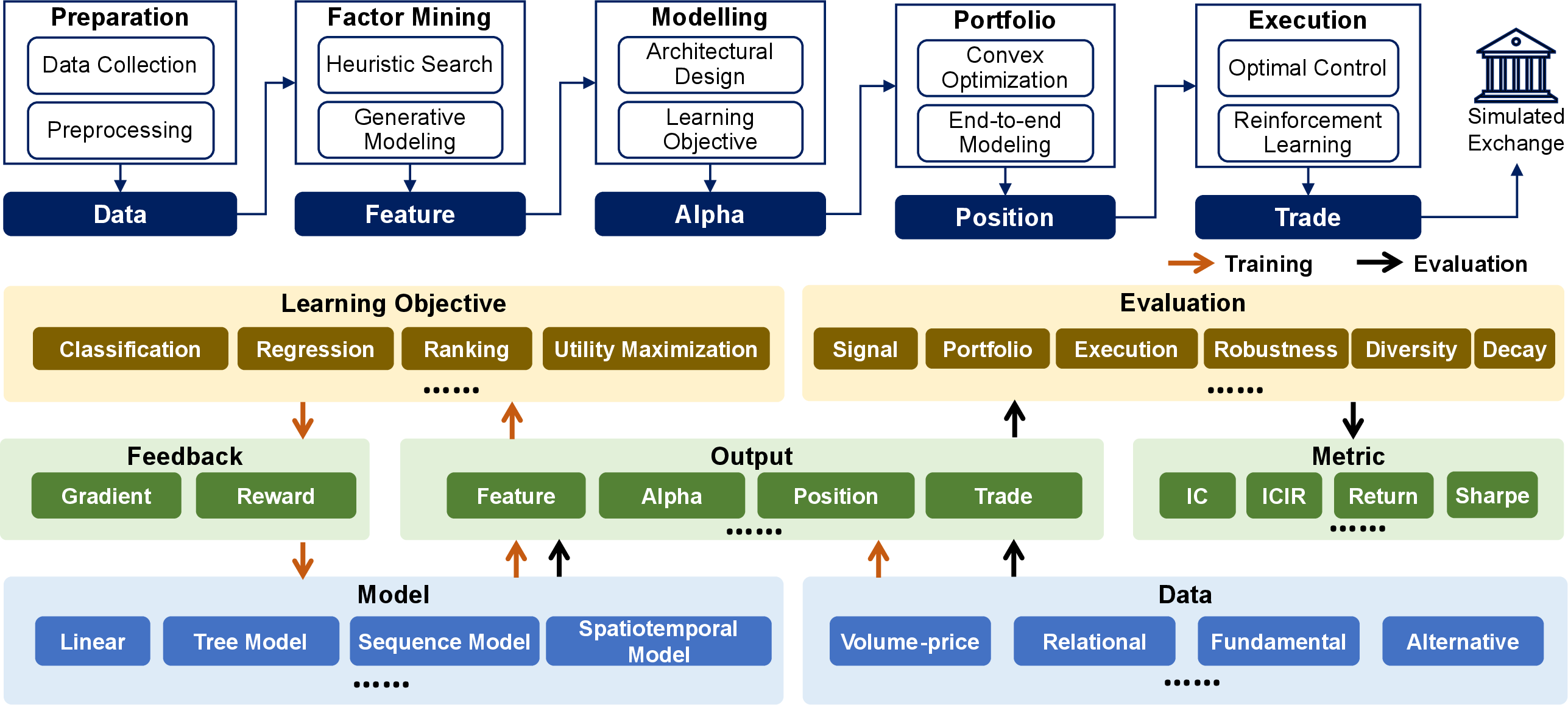

Figure 1: Overview of QuantBench. Upper: Quant research pipeline covered in QuantBench. Lower: The layered design of QuantBench.

The Quant Pipeline

QuantBench supports a comprehensive pipeline for quantitative research, enabling data preparation and trading simulations in the following phases:

- Factor Mining: Utilizes evolutionary algorithms and RL to discover predictive financial features.

- Modeling: Employs machine and deep learning models for forecasting market movements.

- Portfolio Optimization: Uses strategies from simple characteristic-sorted portfolios to deep learning models aiming at utility maximization.

- Order Execution: Involves optimal control and RL to minimize the impact of trades on the market.

Figure 2: Quant pipeline.

Design of QuantBench

The design leverages a layered approach integrating models, datasets, and evaluation metrics, enhancing reproducibility, and bridging academic and industry research gaps. The training and evaluation processes are distinctly streamlined through this structured design.

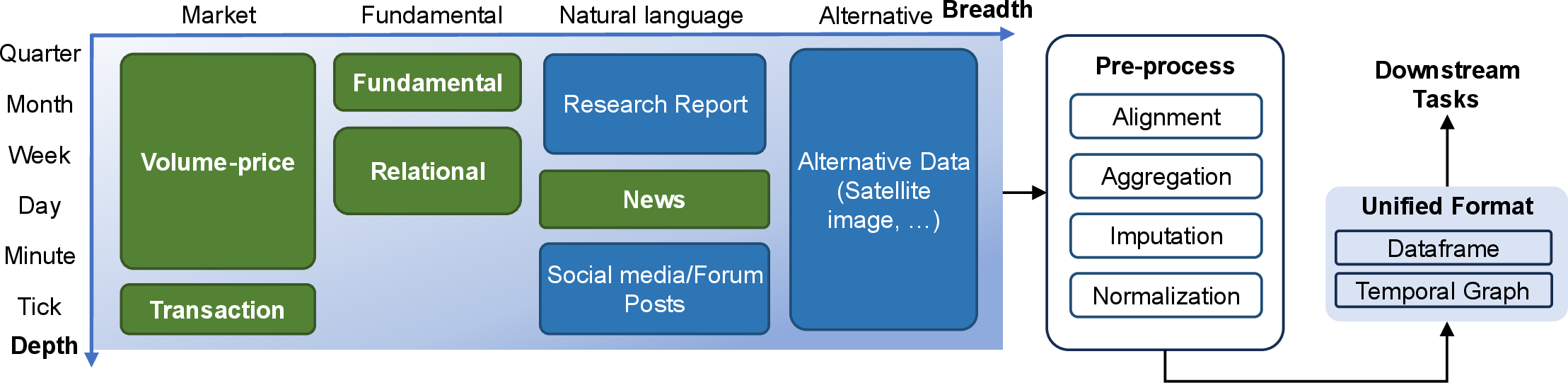

Figure 3: Data processing pipeline of QuantBench. Blocks with green background are already supported in QuantBench, and blocks with blue background are planned to be supported in the future.

Data

QuantBench incorporates a variety of data sources essential for quantitative finance:

Models

QuantBench includes a dynamic range of models categorized by architectural design:

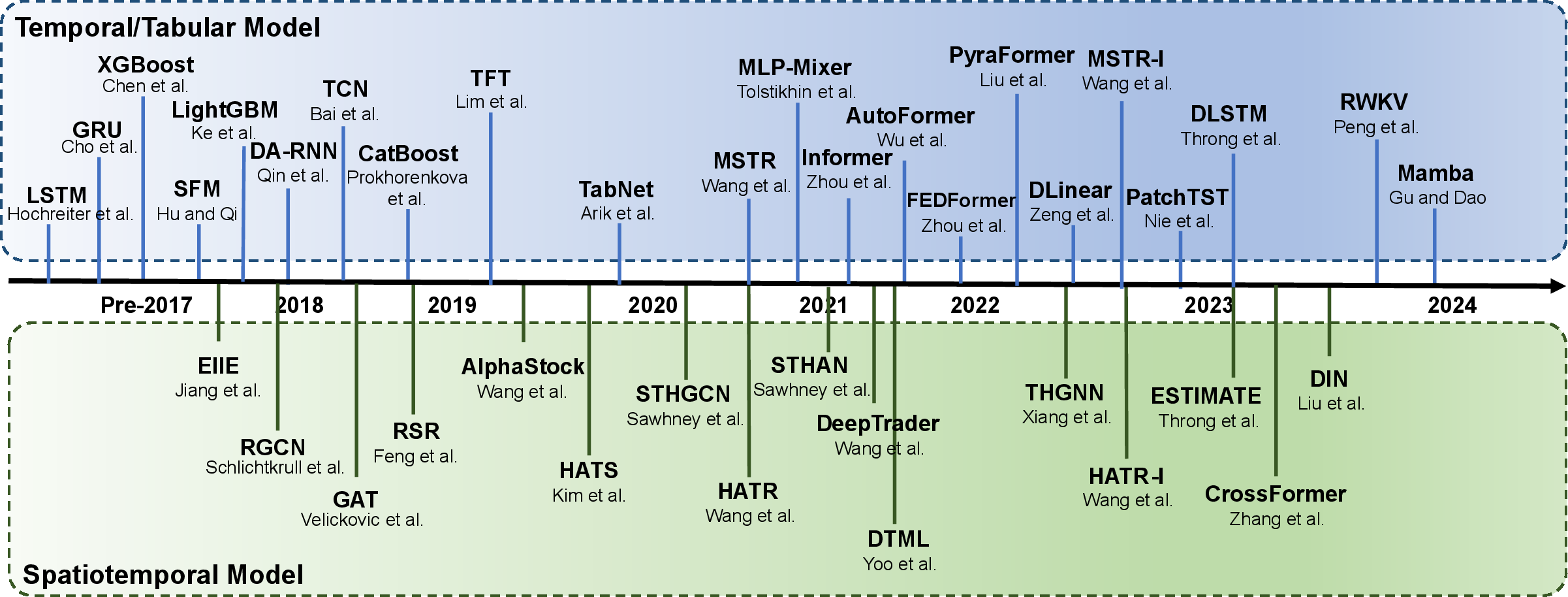

- Temporal Models: Incorporate LSTM, XGBoost, and Transformer-based models like FEDformer.

- Spatial Models: Use graph-based architectures including GAT and RGCN for exploring stock relations.

The platform supports diverse training objectives such as classification and regression, with emphasis on utility maximization for portfolio management.

Evaluation

QuantBench provides task-specific metrics like IC for signal quality and Sharpe ratio for portfolio evaluation. Task-agnostic metrics such as robustness, correlation, and alpha decay are also incorporated to address financial data intricacies.

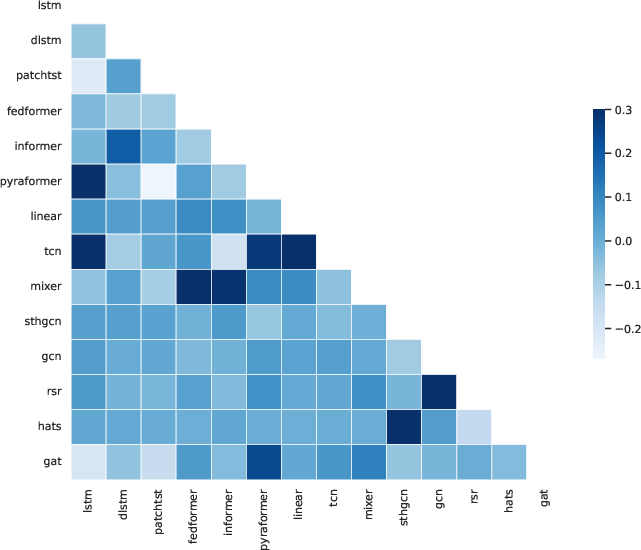

Figure 5: Correlation matrix of temporal and spatial models on CSI300.

Empirical Study

QuantBench's empirical studies illustrate key findings in model performance, influencing future research directions:

Conclusion

QuantBench constitutes a comprehensive, scalable evaluation framework for AI-driven quantitative investment strategies. Future developments may focus on expanding data sources and integrating more innovative modeling techniques, improving engagement between academia and industry.