CSTrader: A Testbed for Language-Grounded Trading in a Community-Driven Virtual Asset Market

Abstract: Niche asset markets, such as Counter-Strike 2 (CS2) weapon skins, are small, volatile, and heavily driven by community discussions and platform rules. These properties make them hard for traditional quantitative models, but provide an ideal testbed for studying how LLMs turn unstructured text into trading actions. We present CSTrader, a multi-agent framework for language-grounded trading in the CS2 skin market. The system first integrates heterogeneous signals from various sources, then uses specialized agents for technical analysis, liquidity, events, and (reversed) sentiment, and finally applies risk control, transaction friction, and portfolio management agents to produce buy, sell, or hold decisions under realistic trading frictions. We build a live-like evaluation environment with real CS2 data from a highly volatile period and evaluate several recent LLM backbones. Across models, CSTrader consistently outperforms both a falling market index (-15.62%) and simple single-prompt LLM baselines, achieving up to a 7.58% cumulative return with controlled risk. Ablation studies show that liquidity, reversed sentiment, and transaction friction agents are crucial for turning noisy language signals into stable profits, suggesting that niche, language-driven markets are a useful benchmark for future language-to-action research. Code is available at: https://github.com/IatomicreactorI/CSGOTrading?tab=readme-ov-file#quick-start

Paper Prompts

Sign up for free to create and run prompts on this paper using GPT-5.

Top Community Prompts

Explain it Like I'm 14

What this paper is about (in simple terms)

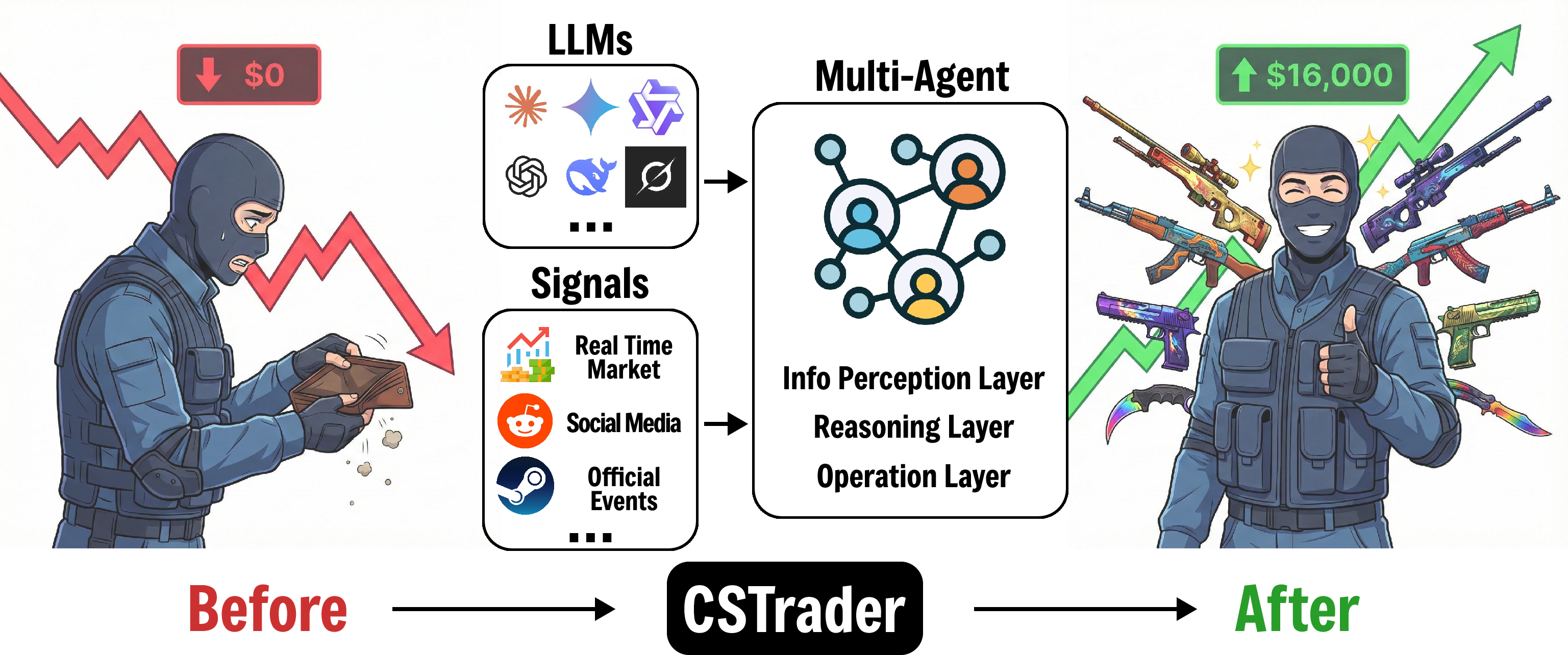

This paper builds and tests a smart “team of AI helpers” that tries to trade virtual game items from Counter-Strike 2 (CS2) for profit. These items are “skins” that change how a weapon looks. Their prices jump around a lot and are heavily influenced by player chatter on sites like Reddit and by game updates. The authors use this market as a playground to study how AI that reads language (LLMs, or LLMs) can turn unstructured text into real trading decisions.

They create a system called CSTrader, which reads:

- numbers (prices and volumes),

- people’s posts (community discussions),

- and official news (game updates),

and then decides whether to buy, sell, or hold items—while respecting real-life rules like marketplace fees and trade locks.

The big questions the paper asks

- Can we build a realistic, fair “testbed” (practice environment) where AI traders that read text and numbers can be compared?

- What kind of AI setup works best in a small, volatile, community-driven market like CS2 skins?

- Which pieces of information (price trends, social chatter, events, liquidity, fees) actually help make better trades?

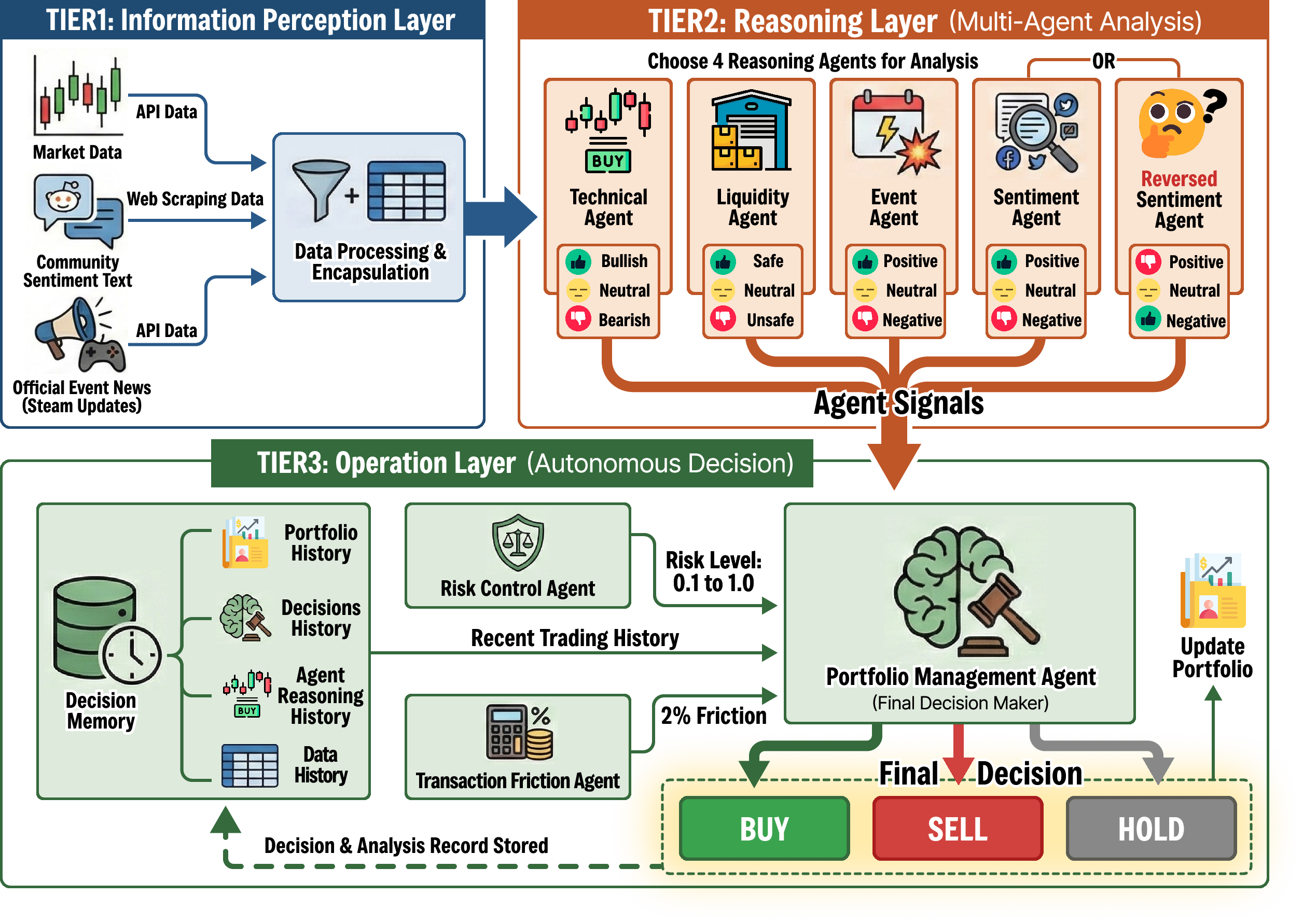

How the system works (explained like a team sport)

Think of CSTrader as a coached team with three layers. Each layer has specialists with clear jobs.

- Information Perception Layer: The “scouts”

- Collects and cleans three types of input:

- Market prices (daily open/high/low/close and trading volume—think “price history and how busy the market is”)

- Community posts (Reddit discussions that reflect what people feel and think)

- Official events (Steam/CS2 updates that can change supply or demand)

- Reasoning Layer: The “analysts”

- Five specialist AI agents read the inputs and give simple signals like “Bullish” (positive), “Bearish” (negative), or “Neutral,” with short explanations:

- Technical Agent: Looks at price patterns and momentum (like watching trends on a graph) to guess near‑future moves.

- Sentiment Agent: Reads Reddit to sense the mood—are people hyped or worried?

- Reversed Sentiment Agent: Does the opposite of the crowd on purpose when hype looks extreme (a “contrarian” who avoids bubbles and panic).

- Liquidity Agent: Checks how easy it is to buy and sell without getting stuck. Liquidity means “how many buyers and sellers are there?” Poor liquidity can trap you in an item you can’t resell.

- Event Agent: Watches official updates to see if news will change supply/demand soon.

- Operation Layer: The “coaches and captains”

- Turns the analysts’ signals into actual trades while controlling risk and costs:

- Risk Control Agent: Limits how big each position should be so the portfolio doesn’t take reckless risks.

- Transaction Friction Agent: Accounts for marketplace costs (like a ~2% fee) and blocks tiny trades that would lose money after fees. “Friction” just means fees and other real-life obstacles.

- Portfolio Management Agent: Makes the final buy/sell/hold call, considering cash, recent decisions, and safety checks.

Analogy: The scouts gather info, analysts give opinions, and the coaches make careful, cost-aware plays.

What the researchers did to test it

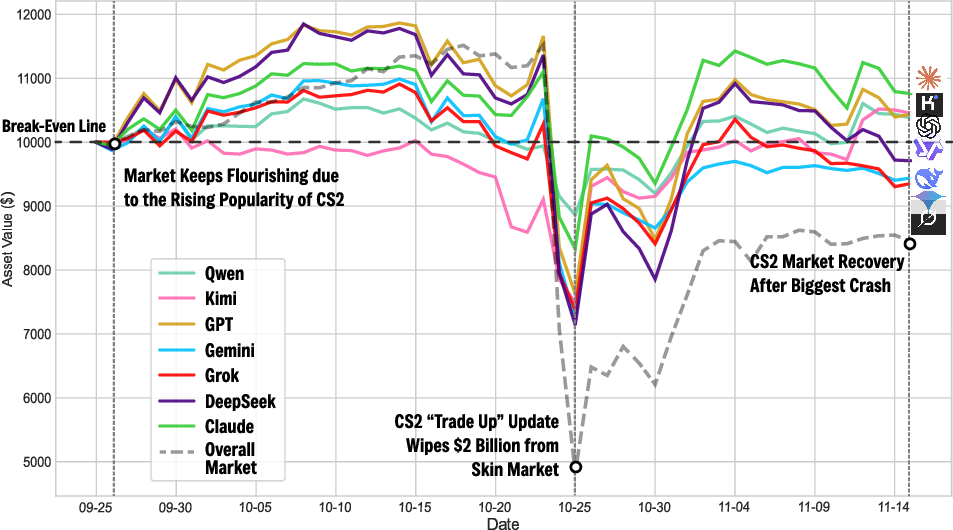

They ran CSTrader on real CS2 market data during a wild period (from late September to mid‑November) when the overall market dropped by about 15.6%. They compared:

- CSTrader using different base LLMs (the “brains” behind the agents),

- simple single‑prompt LLM baselines (just asking an AI directly what to do),

- and the overall market index (a “just hold everything” baseline).

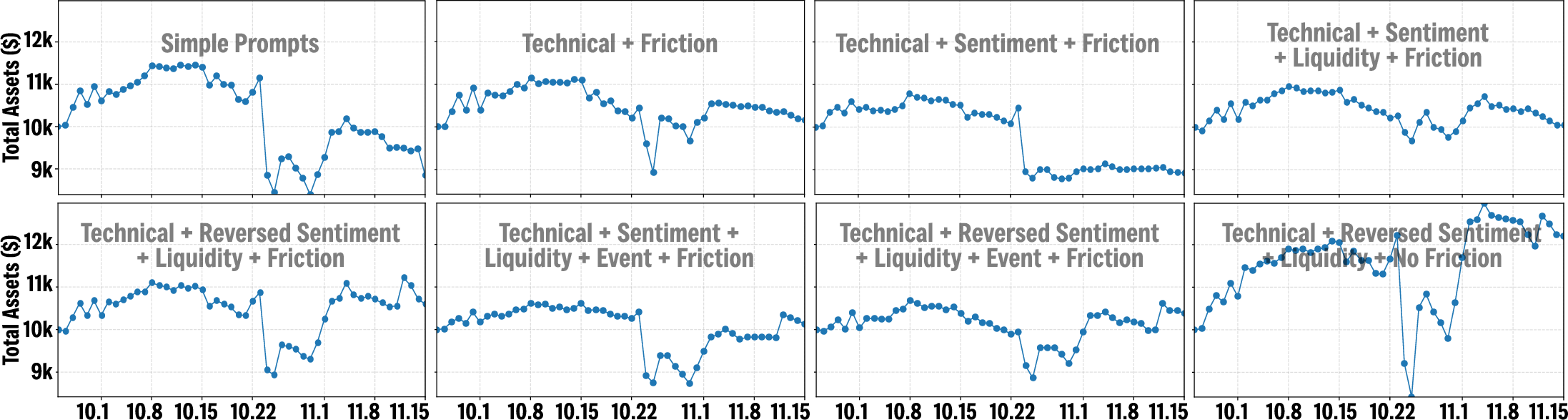

They also did “ablation” tests—turning some agents on/off to see which ones matter most.

Main findings and why they’re important

- The multi-agent system beat the market during a crash:

- While the overall CS2 market fell ~15.6%, CSTrader versions using strong LLMs made positive returns (up to about +7.6%) and recovered faster after a big update-related crash.

- This shows that combining price data with community chatter and platform rules—plus careful risk and cost control—can create advantages even in tough markets.

- Some agents are especially valuable:

- Liquidity Agent: Helped avoid getting stuck in items that are hard to sell—crucial in thin, niche markets.

- Reversed Sentiment Agent: Often did better than plain Sentiment. In a hype-driven market, doing the opposite of the crowd at extremes helped avoid bubbles and catch bargains.

- Transaction Friction Agent: Modeling fees turned “paper profits” into more realistic results and discouraged money-losing “churn” (too many small trades).

- Event Agent wasn’t a big boost:

- Official news often got priced in quickly, so it added limited extra edge on top of the other signals.

- The base LLM matters:

- Stronger reasoning models tended to earn more, while more cautious ones had lower risk and volatility. Weaker models struggled to pick good items consistently.

Why this matters: It shows that in small, language-driven markets, success isn’t just about reading news—it’s about integrating sentiment, liquidity, and costs, and sometimes going against the crowd.

What this could mean for the future

- A useful testbed: CS2 skins (and similar markets like NFTs or collectibles) can be great practice fields for building AIs that turn text into real decisions under real-world rules.

- Better AI decision-making: Breaking the problem into specialized agents (trends, mood, liquidity, costs, risk) made the system more robust and easier to understand.

- Beyond games: The same ideas—reading community chatter, respecting platform rules, and controlling risk—could help in other small or alternative markets.

Simple takeaway: In places where talk moves prices, an AI team that reads the room, watches the rules, and keeps risk in check can make smarter moves than a one-size-fits-all approach.

Short note on limits and next steps

- This study looked at one market (CS2) over a relatively short, volatile window. Real trading also involves things like order books and execution delays that weren’t fully modeled.

- The agents relied on carefully designed prompts and a handful of LLMs; stronger non-AI baselines weren’t deeply tested.

- Next steps include trying longer periods and other markets, adding more realistic trading mechanics, and mixing in classic “quant” models or learning-based decision layers.

In other words: good early results, but more testing in different conditions is needed before assuming it works everywhere.

Knowledge Gaps

Knowledge gaps, limitations, and open questions

Below is a single, concrete list of unresolved issues that future work could address:

- Generalization across time and markets: Does CSTrader’s performance persist across longer horizons, different market regimes (bull, bear, sideways), and other language-driven assets (e.g., NFTs, collectibles) beyond the short CS2 window studied?

- Survivorship and universe selection bias: What are the exact liquidity filters and inclusion/exclusion criteria for skins, and how do results change under dynamic universes that add/remove newly released or delisted items?

- Microstructure realism: How do order-book shape, partial fills, slippage, execution latency, and queue position affect realized PnL in illiquid skins, and how should these be simulated in the environment?

- Trade-lock and fee modeling: To what extent do realistic trade-lock periods and accurate fee schedules (which may be substantially higher than the 2% used) alter turnover, profitability, and optimal holding times?

- Self-impact and market footprint: How does the agent’s own trading (especially in thin markets) move prices, and what position-sizing and execution tactics minimize detectable footprint and adverse selection?

- Mark-to-market under illiquidity: How sensitive are reported returns to the choice of marking prices (last trade, mid, volume-weighted), stale quotes, and gaps in trading days?

- Alternative and stronger baselines: How does CSTrader compare against tuned classical strategies (momentum, mean-reversion, cross-sectional factors), reinforcement-learning agents, and practitioner heuristics on the same data and frictions?

- Statistical significance and robustness: Are observed outperformance metrics statistically significant when evaluated with multiple seeds, bootstrapped confidence intervals, rolling windows, and repeated out-of-sample periods?

- Anti-leakage guarantees: Exactly how are social posts timestamped, time-zoned, and aligned to avoid look-ahead; can a formal audit trail or a replayable event log demonstrate no future information seepage?

- Broader information coverage: How much signal is lost by restricting to Reddit; does adding Discord, Steam forums, X/Twitter, and non-English sources improve recall and robustness?

- Adversarial and spam robustness: How vulnerable are the sentiment and event pipelines to coordinated hype, bot campaigns, or misinformation, and what filtering or provenance checks mitigate this?

- Event-to-asset mapping: How are Steam updates causally linked to specific skins; can a principled taxonomy, lag structure, and causal tests (e.g., event studies with controls) clarify when event signals add value?

- Contrarian vs. pro-cyclical sentiment: Under which regimes does reversed sentiment outperform standard sentiment; can regime-switching or thresholded contrarian rules be learned adaptively rather than fixed?

- Agent arbitration: Can the aggregation of technical/liquidity/sentiment/event signals be learned (e.g., via meta-learner, Bayesian model averaging) instead of prompt-engineered weights, and does this improve stability?

- Hyperparameter and prompt sensitivity: How sensitive are outcomes to agent prompts, memory length, thresholds, and temperature; can automated prompt/parameter search or fine-tuning yield consistent gains?

- Learning-based decision layers: Do fine-tuned LLMs, retrieval-augmented models, or offline RL/IL policies outperform purely prompt-based agents under the same frictions?

- Interpretability and fidelity: Do agent rationales faithfully reflect the evidence they use; can we quantify explanation consistency, error modes, and their correlation with trading performance?

- Hallucination and fact-checking: How often do agents fabricate events or misread posts, and can retrieval-grounding, tool use, and veracity checks reduce decision errors?

- Risk measurement tailored to illiquids: Beyond Sharpe/MDD/volatility, how do time-to-liquidate, CVaR, drawdown duration, and liquidation cost metrics alter perceived risk and portfolio choices?

- Stress testing: How does the system behave under extreme but plausible scenarios (e.g., sudden ban, fee hikes, liquidity freeze), and what policy safeguards limit tail losses?

- Execution constraints specific to venues: How do Steam wallet non-withdrawal constraints, bans, and cross-venue (third-party market) frictions affect real deployability and cross-market arbitrage opportunities?

- Use of item micro-attributes: Can incorporating float values, pattern indices, and rarity more directly into signals improve selection and timing, especially for premium pattern-dependent items?

- Frequency and granularity: Would higher-frequency data (intraday) or finer-grained social/event parsing materially change signal latency and profitability, and what are the computational trade-offs?

- Cost and latency of LLM inference: What is the dollar and time cost per decision across backbones and agent stacks, and how does model compression or distillation affect net performance after costs?

- Non-stationarity and model drift: How stable are decisions across LLM versions, API updates, and randomness; can ensembling, temperature control, or calibration reduce variance across runs?

- Benchmark standardization: Can the community get a public, replayable benchmark with synchronized market/social streams, hidden test periods, and a standardized evaluation harness to ensure reproducibility?

- Memory mechanism design: What is the optimal decision-memory length and content; does longer memory improve regime awareness or induce inertia that hurts responsiveness?

- Portfolio sizing methods: How do alternative position-sizing rules (e.g., Kelly fraction, risk parity, convex risk budgets) compare to the current heuristic ratio in risk-adjusted returns?

- Cross-market transfer: Do agents trained/tuned in CS2 transfer to other virtual economies without re-prompting, and which components (liquidity, sentiment, events) generalize best?

- Human-in-the-loop oversight: What workflows allow human experts to audit, veto, or guide agent actions in real time, and how does this affect performance and safety in live settings?

- Ethical and compliance considerations: How to prevent the system from amplifying or exploiting manipulative narratives, and how to ensure compliance with platform terms and local regulations during deployment?

Practical Applications

Immediate Applications

Below are concrete, deployable use cases that leverage the paper’s framework, agents, and findings, mapped to sectors and accompanied by practical tool ideas and feasibility notes.

- Liquidity-aware trading copilot for virtual assets

- Sectors: Finance, Gaming Marketplaces, Retail Traders

- Tools/Products: “LLM Liquidity Guard” that scores items’ sellability; trade-size throttling; automatic “time-to-exit” estimates; contrarian buy/sell hints using the Reversed Sentiment Agent.

- Assumptions/Dependencies: Reliable access to price and volume feeds (Steam API or aggregators), Reddit API or alternative social data, platform ToS compliance, configurable fee/trade-lock parameters.

- Friction-aware backtesting and execution filter

- Sectors: Finance, Software

- Tools/Products: A transaction-cost module (fees, trade locks) that wraps existing bots; pre-trade checks to block submargin trades; fewer, higher-conviction orders as suggested by the paper’s Transaction Friction Agent.

- Assumptions/Dependencies: Accurate fee schedules and lock-period metadata; minimal slippage estimates even if order-book data is unavailable.

- Event/sentiment dashboards for niche markets

- Sectors: Data Providers, Analytics, Gaming

- Tools/Products: “Language-grounded Event Monitor” to summarize patch/update implications; dual Sentiment and Reversed Sentiment panels; alpha attribution view that ties PnL to agent signals.

- Assumptions/Dependencies: Timely ingestion and de-duplication of patch notes and official announcements; rate-limit-aware social scraping.

- Platform-side liquidity health and UX cues

- Sectors: Marketplaces/Platforms (e.g., Steam-like), Product Management

- Tools/Products: Item pages that show “estimated time-to-sell,” “liquidity risk,” and “expected net after fees”; nudges discouraging liquidity traps; portfolio-level risk bars based on CSTrader’s Risk Control Agent.

- Assumptions/Dependencies: Access to internal marketplace statistics; A/B testing infrastructure; alignment with user trust and policy.

- Compliance and market integrity triage for hype cycles

- Sectors: Trust & Safety, Compliance

- Tools/Products: Reversed Sentiment-derived alerts for pump-like activity; clustering of coordinated posting patterns; explainable flags with agent rationales.

- Assumptions/Dependencies: Historical labeled incidents for tuning thresholds; cross-post identity resolution; governance for false positives.

- Research benchmark for language-to-action systems

- Sectors: Academia, R&D Labs

- Tools/Products: The paper’s open-source testbed as a standard evaluation harness; leaderboards; reproducible ablations for Liquidity/Event/Sentiment agents.

- Assumptions/Dependencies: Versioned datasets; frozen evaluation windows; community-maintained baselines.

- Teaching sandbox for computational finance and NLP

- Sectors: Education

- Tools/Products: Course labs on fee-aware trading, sentiment inversion, agent explainability; capstone projects porting CSTrader to NFTs/collectibles.

- Assumptions/Dependencies: Curated historical data bundles; simplified APIs; institutional access to LLMs.

- Portfolio summary and “explain-my-trade” assistant

- Sectors: Retail Tools, Fintech

- Tools/Products: A client-facing assistant that explains recent trades using agent rationales; what changed (technical vs. sentiment vs. liquidity); recommended action vs. friction-adjusted expectancy.

- Assumptions/Dependencies: Secure portfolio read/write permissions; guardrails against over-reliance; disclosures for non-advisory use.

- Niche-asset indices and factor products

- Sectors: Data Providers, Asset Management (Alt Assets)

- Tools/Products: Liquidity-filtered indices; contrarian sentiment factors; “event-exposed” baskets for patch-sensitive items.

- Assumptions/Dependencies: Stable item taxonomy; survivorship-bias handling; rebalancing rules accounting for trade locks.

- Vendor-neutral agent observability and audit

- Sectors: Software/MLOps, Risk

- Tools/Products: An “agent observability” layer that logs prompts, rationales, and final actions; drift monitors for sentiment vs. price reality; alpha/beta decomposition by agent.

- Assumptions/Dependencies: Centralized logging; privacy controls; cost management for LLM telemetry.

Long-Term Applications

These opportunities extend the framework to broader markets or require additional R&D, richer data, or regulatory alignment.

- Extension to regulated small-cap equities and emerging markets

- Sectors: Finance

- Tools/Products: Microstructure-aware multi-agent traders that integrate order books, slippage models, and venue fees; human-in-the-loop override based on risk budgets.

- Assumptions/Dependencies: Licensed market data; compliance approvals; robust best-execution policies; latency-sensitive infrastructure.

- Regulatory sandbox for rule design and consumer protection

- Sectors: Policy/Regulation

- Tools/Products: Simulators to test fee changes, lockups, disclosure rules, or anti-manipulation policies; stress tests for social-media-driven volatility.

- Assumptions/Dependencies: Data-sharing agreements with platforms; privacy-preserving analytics; explainability to support supervisory review.

- Cross-platform market-making for virtual economies

- Sectors: Market Infrastructure, Gaming

- Tools/Products: Autonomous agents that set spreads using liquidity risk and sentiment; inventory hedging across correlated items (e.g., skins, stickers, cases).

- Assumptions/Dependencies: Programmatic market access; clear legal status of automated liquidity provision; capital controls.

- Systemic manipulation and contagion analytics

- Sectors: Compliance, Risk Management

- Tools/Products: Early-warning systems for coordinated hype and cross-asset contagion; “sentiment velocity” thresholds that trigger dynamic circuit breakers.

- Assumptions/Dependencies: Cross-platform social/firehose access; robust entity resolution; governance and escalation runbooks.

- Generalized language-to-action decision layer for digital markets

- Sectors: E-commerce, Ads, Carbon/Energy Credit Markets

- Tools/Products: Friction-aware multi-agent controller for pricing/bidding that accounts for fees, latency, and liquidity constraints; contrarian signals to avoid herd bidding.

- Assumptions/Dependencies: Domain-specific constraints and KPIs; safety policies for automated actions; offline-to-online validation.

- Hybrid learned agents and offline RL on top of LLM reasoning

- Sectors: AI/ML Research, Quant

- Tools/Products: Fine-tuned policy heads, decision transformers, or offline RL that consume agent rationales as state; auto-curriculum tuned via the testbed.

- Assumptions/Dependencies: High-quality logged trajectories; careful reward design to avoid fee-ignorant overtrading; compute budgets.

- Publisher-side economy design and patch planning

- Sectors: Game Development, Product Strategy

- Tools/Products: Forecasting tools to simulate patch/update effects on supply, demand, and volatility; policy optimizers for fee schedules that maximize long-term engagement, not short-term churn.

- Assumptions/Dependencies: Access to internal telemetry; causal evaluation of prior updates; multi-objective optimization.

- Human-AI trader collaboration suites

- Sectors: Professional Trading, Fintech

- Tools/Products: Co-pilots that surface disagreements between agents (e.g., Technical vs. Reversed Sentiment), show scenario analyses, and trace expected net returns after frictions.

- Assumptions/Dependencies: Rich UX for explanations; decision logs for audit; integration with OMS/EMS.

- Standardized benchmark suite for realistic language-grounded decision-making

- Sectors: Academia, Standards Bodies, Open-Source Community

- Tools/Products: Multi-domain benchmarks (virtual items, NFTs, carbon credits) with enforced frictions, public leaderboards, and interpretability scores.

- Assumptions/Dependencies: Community governance; dataset licensing; neutral hosting and evaluation protocols.

- Ethical guardrails and certification for LLM traders

- Sectors: Policy, Industry Consortia

- Tools/Products: Certification criteria for friction-aware, manipulation-averse agents; red-team playbooks; transparency reporting (rationales, failure cases).

- Assumptions/Dependencies: Consensus on standards; third-party auditors; incident disclosure frameworks.

Glossary

- Ablation study: An experimental method that removes or alters components of a system to assess each part’s contribution to performance. "Ablation studies show that liquidity, reversed sentiment, and transaction friction agents are crucial for turning noisy language signals into stable profits"

- Alpha (): A measure of excess return earned by a strategy compared to a market benchmark after accounting for risk. "and alpha () capturing excess return over the market."

- Annualized Volatility (AV): The yearly scaled standard deviation of periodic returns, used to quantify how much returns fluctuate. "Annualized Volatility (AV)~\cite{cochrane1991volatility}: The standard deviation of daily returns, showing price fluctuations;"

- Backtesting: Evaluating a trading strategy using historical data to estimate how it would have performed. "Backtesting methods often lack realism."

- Beta (): A measure of a portfolio’s sensitivity to movements in the overall market; values above 1 imply higher volatility than the market. "beta () relative to the overall market index"

- Bollinger bands: A technical indicator that places bands around a moving average at a set number of standard deviations to gauge relative price levels. "Bollinger-band style mean reversion"

- Contrarian: A trading approach that goes against prevailing market sentiment or trends. "applies a contrarian lens to the standard sentiment output"

- Cumulative Return (CR): The total percentage change in portfolio value over a period. "Cumulative Return (CR)~\cite{hull2012cr}: The total percentage change in the portfolio value;"

- Decision memory: A short-term record of recent actions used to inform current decisions and maintain consistency. "a short decision memory of recent trades"

- Drop pools: The defined sets or probabilities that govern which items can be dropped in-game, affecting supply. "changes to drop pools, item supply, and game visibility."

- Elo: A relative rating metric originally for skill ranking, here used to compare model capability. "For each provider, we list the model name, release date, knowledge cut-off, Elo rating, and whether the model is open source."

- Execution latency: The delay between issuing a trade and its actual execution, which can affect realized prices. "without explicitly modeling order-book dynamics, slippage, or execution latency beyond a simple 2\% transaction fee."

- Exponential moving averages: Trend indicators that weight recent prices more heavily to smooth time series and track direction. "it combines exponential moving averages"

- Float value: A continuous parameter in representing the wear level of a CS2 skin, with lower values indicating less wear. "each skin instance has a continuous float value in the range "

- Herd effects: Collective behavior where many participants follow the same sentiment or action, potentially causing bubbles or crashes. "To capture herd effects, the Reversed Sentiment Agent applies a contrarian lens"

- Knowledge Cut-off: The latest point in time up to which a model’s training data is known, beyond which it may lack information. "For each provider, we list the model name, release date, knowledge cut-off, Elo rating, and whether the model is open source."

- Liquidity: The ease of buying or selling an asset without causing large price changes. "These assets often have low liquidity, which means prices can change quickly with small trades"

- Liquidity trap: A situation where an asset is listed at high prices but has insufficient demand, making it hard to sell. "It flags ``liquidity traps''---items with high listed prices but little real demand---"

- Market capitalization: The total market value of tradable items in an ecosystem. "the notional market capitalization of tradable CS2 skins is on the order of 4--5 billion USD."

- Market frictions: Real-world costs and constraints (fees, locks) that impede idealized trading. "under the same market frictions and data streams"

- Market index: A composite measure tracking the average price movement of a set of assets, used as a benchmark. "We use the overall market index~\cite{csqaq_market_index} as our primary baseline"

- Market microstructure: The mechanisms and rules underlying trade execution and price formation in a market. "exhibit distinct microstructure and information channels"

- Maximum Drawdown (MDD): The largest peak-to-trough percentage decline in portfolio value over a period. "Maximum Drawdown (MDD)~\cite{ang2006downside}: The largest peak-to-trough decline in the portfolio value."

- Mean reversion: The tendency for prices to move back toward a long-term average after deviations. "Bollinger-band style mean reversion"

- Momentum: The persistence of price trends, where rising (or falling) prices tend to continue for some time. "momentum"

- OHLCV: A time-series format recording Open, High, Low, Close prices and Volume for each period. "daily OHLCV(Open, High, Low, Close, Volume) records"

- Order-book dynamics: The behavior of buy and sell orders at various price levels that determine trade execution and liquidity. "without explicitly modeling order-book dynamics, slippage, or execution latency"

- Pattern index: A random identifier determining a skin’s specific texture overlay, influencing rarity and price. "each skin instance has a continuous float value and pattern index"

- Position ratio: The targeted proportion of portfolio capital allocated to a specific asset. "optimal position ratio"

- Reversed sentiment: A contrarian interpretation of crowd sentiment, treating extreme optimism as bearish and vice versa. "Reversed Sentiment Agent"

- Risk-free rate: The return of an investment with theoretically zero risk, used to adjust performance metrics. "calculated using a 2\% risk-free rate"

- RSI: Relative Strength Index, a momentum oscillator measuring the speed and magnitude of recent price changes. "RSI-type momentum"

- Sharpe Ratio (SR): A risk-adjusted performance metric equal to excess return divided by volatility. "Sharpe Ratio (SR)~\cite{sharpe1994sharpe}: The risk-adjusted return, calculated using a 2\% risk-free rate;"

- Slippage: The difference between the expected trade price and the price at which the trade is actually executed. "without explicitly modeling order-book dynamics, slippage, or execution latency"

- Support/resistance levels: Price zones where buying (support) or selling (resistance) pressure tends to halt or reverse moves. "support/resistance levels"

- Trade lock: A platform-imposed period during which items cannot be traded after certain actions. "such as high fees or ``trade lock'' periods"

- Transaction fee: A platform charge taken from each trade that reduces net proceeds. "without explicitly modeling order-book dynamics, slippage, or execution latency beyond a simple 2\% transaction fee."

- Transaction friction: The cumulative effect of costs like fees that make frequent trading less profitable. "transaction friction agents are crucial"

- Volatility regimes: Distinct periods characterized by different levels of price variability. "volatility regimes"

- Wear level: A categorical representation (e.g., FN, MW, FT, WW, BS) of a skin’s visual wear that affects value. "Wear level and float value."

Collections

Sign up for free to add this paper to one or more collections.