Malliavin calculus for signatures with applications to finance

Published 24 Apr 2026 in math.PR | (2604.22528v1)

Abstract: Malliavin calculus is a powerful and general framework for the analysis of square-integrable random variables, but it often suffers from a lack of tractability and explicit representations. To address this limitation, we focus on a subclass of random variables given by finite linear combinations of time-extended Brownian motion signatures. The class remains rich due to the universal approximation properties of signatures. Leveraging the algebraic structure of signatures, we first derive explicit formulas for the Malliavin derivative of signatures of continuous Itô processes. As a consequence, we obtain closed-form expressions for the Clark--Ocone representation, the Ornstein--Uhlenbeck semigroup and its generator, as well as the integration-by-parts formula within the class of Brownian signature variables. These results provide purely algebraic formulations of the classical operators of Malliavin calculus. As an application, we compute Greeks for general path-dependent options under signature volatility models, and numerically compare different choices of Malliavin weights.

The paper presents an explicit algebraic framework that transfers Malliavin calculus operations to a linear operator calculus on tensor algebra.

It leverages key signature properties like Chen’s identity and the shuffle product to derive closed-form expressions for Malliavin derivatives and associated weights.

The framework enables efficient computation of Greeks for path-dependent derivatives and robust sensitivity analysis in signature volatility models.

Malliavin Calculus for Path Signatures: Structure, Explicit Computations, and Financial Applications

Introduction and Motivation

This paper develops a comprehensive algebraic framework for Malliavin calculus applied to finite linear combinations of path signatures—specifically, signatures of continuous Itô processes, with emphasis on time-augmented Brownian motion. The motivation arises from the challenge that, although Malliavin calculus provides a powerful set of tools for extracting probabilistic and sensitivity information for Brownian functionals (such as Greeks in quantitative finance or density regularity in SDEs), explicit and numerically tractable representations for Malliavin derivatives and associated integration-by-parts weights are typically unavailable.

The authors exploit the universal approximation and algebraic structure of path signatures, transferring all Malliavin-calculus operations into a linear-operator calculus on the (extended) tensor algebra. This allows for the explicit computation of Malliavin derivatives, Clark–Ocone terms, Ornstein–Uhlenbeck operators, chaos expansions, and integration-by-parts weights. These operations are then specialized and illustrated for pricing and differentiating path-dependent derivatives in signature volatility models, with numerical benchmarks for practical implementation.

Algebraic Formulation of Signatures and Malliavin Operators

Path Signatures and Tensor Algebra

The signature X of a d-dimensional continuous path over [0,T] is defined as the infinite sequence of iterated Stratonovich integrals. The signature admits a clean algebraic structure by identification with the extended tensor algebra T, and features critical properties such as:

Chen’s identity: Concatenating intervals corresponds to the tensor product of signatures.

Shuffle product: Products of signature coefficients correspond to shuffle products in the algebra.

This formalism enables signatures to play a role akin to polynomial bases on path space, encoding universal approximation theorems and stochastic Taylor expansions for functionals of Brownian motion.

Malliavin Derivatives of Signatures

The central technical achievement is the derivation of explicit, closed-form expressions for Malliavin derivatives of the signatures of Itô processes. If X is a continuous Itô process driven by (Wt) and atk are regular adapted coefficients,

where As encodes the local vector fields. In the special case of time-augmented Brownian motion, repeated Malliavin differentiation produces formulae corresponding to “piercings" (letter insertions) in the signature at the differentiation times. This clarifies both algebraic and geometric aspects of Malliavin calculus for signatures.

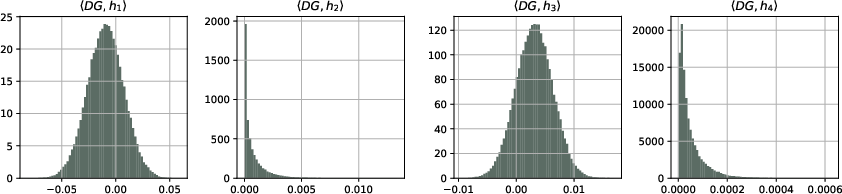

Figure 1: Empirical distribution of DGh for Malliavin weights associated to different functional choices d0.

Explicit Algebraic Evaluation of Classical Operators

Skorokhod Integral, Clark–Ocone Formula, and Chaos Expansion

The algebraic formalism allows the Skorokhod integral d1 of signature-based functionals to be expressed as an explicit combination of signature coefficients, via the “switching operator” d2, which permutes/augments words in the shuffle algebra. Similarly, the Clark–Ocone representation for any linear functional of the signature admits closed-form integrands in terms of signatures. The Wiener–Itô chaos expansion becomes explicit by combining the iterated application of Malliavin derivatives and expected signatures, with only finitely many non-vanishing terms when the linear functionals are truncated signatures.

Ornstein–Uhlenbeck Semigroup and Generator

The Ornstein–Uhlenbeck (OU) semigroup, key to the analysis of densities and regularity, is realized as an explicit operator on the tensor algebra, with its generator decomposed into combinations of switching and counting operators. Thus, the classical semigroup methods, usually formulated in terms of chaos projections, are tractable for signature-based functionals.

Explicit Malliavin Integration by Parts and Rational Weights

A significant outcome is that for d3 (a linear functional of a Brownian signature) and d4 a ratio of such functionals, one can produce the exact Malliavin weight and thus the sensitivity formula: d5

where d6 admits a tractable explicit formula involving rational functions of the signature. Notably, the denominator, previously a source of instability with classical choices, is now represented transparently within the algebraic calculus, aiding both symbolic and numerical work.

Application to Path-Dependent Option Greeks in Signature Volatility Models

Signature Volatility Model Formulation

The signature volatility model generalizes stochastic volatility by setting the instantaneous volatility as a linear functional of the time-extended Brownian signature, d7. Such models are dense in a variety of classical, non-Markovian, and rough volatility models.

Greeks Computation and Numerical Benchmarks

For generic path-dependent payoffs (including Asians and power functionals), the price and all common Greeks can be obtained via differentiation under the expectation by leveraging the algebraic structure. Malliavin weights for Monte Carlo estimation are provided in explicit algebraic form. The paper performs a systematic comparison of different Malliavin weights for European and path-dependent derivatives, highlighting differences in numerical stability (depending on the structure of the denominator and choice of d8) and required signature truncation orders.

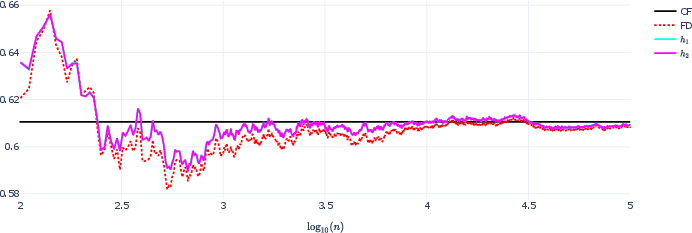

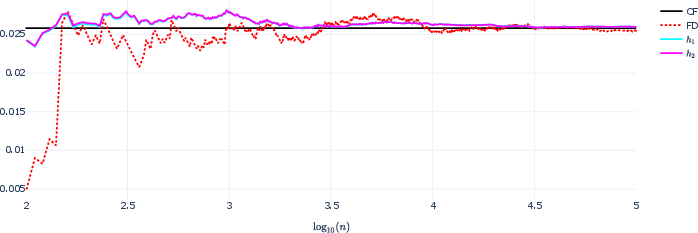

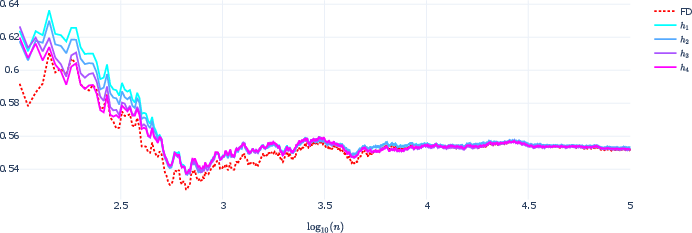

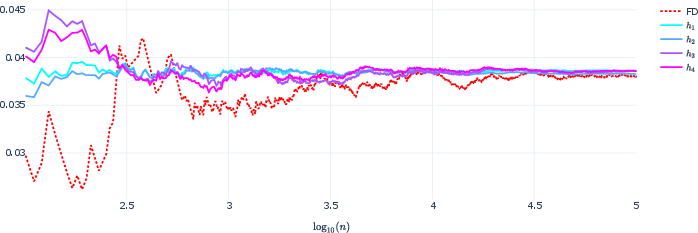

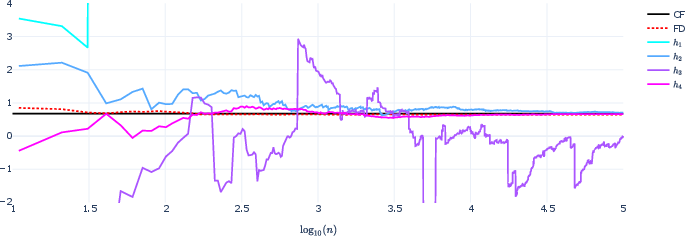

Figure 4: “Convergence” diagram for vanilla ATM options in the stochastic volatility model, illustrating MC estimator performance as a function of sample size and weight selection.

The results indicate that, for non-smooth payoffs, the Malliavin-based estimators (especially when carefully matched with the problem structure) converge more efficiently and stably than pathwise-derivative or finite-difference estimators. The algebraic calculus enables the avoidance of intractable discretization or differentiation of pathwise functionals.

Implications, Limitations, and Outlook

These explicit computations facilitate the use of signatures for unbiased, efficient Monte Carlo Greeks in exotic/rough volatility models, as well as rigorous sensitivity analysis for complex functionals of Brownian paths. The algebraic closure of function classes under Malliavin operators also opens avenues for regularity analysis of densities in rough-path dynamics and for the principled statistical inference of functionals approximated by linear signature maps.

From a numerical and practical perspective, algebraic transparency enables symbolic or even automatic implementation of all Malliavin operations, making robust risk management and calibration feasible for a much broader range of models.

While the expressiveness of signatures is tied to the truncation level and the complexity of the resulting algebraic expressions, the explicitness gained in this framework is unmatched by alternative methods such as functional Itô calculus, especially for highly path-dependent or non-weakly path-dependent derivatives.

Conclusion

The paper develops an operator-algebraic calculus for Malliavin differentiation and integration-by-parts formulae for path signatures, making explicit all classical stochastic analysis operations in this universal function class. Special attention to tractable formulae for Greeks under signature volatility models demonstrates the framework's value for both theoretical and computational aspects of stochastic analysis and mathematical finance (2604.22528).