- The paper extends the universal approximation theorem to non-geometric rough paths by employing Itō-type signatures enhanced with time and quadratic variation.

- It introduces a quasi-shuffle framework and rigorous tensor algebra constructions to approximate continuous functionals for financial applications.

- Practical experiments demonstrate that the extended signatures improve calibration and pricing accuracy, validating their use in regression models.

Universal Approximation with Signatures of Non-Geometric Rough Paths

Introduction and Motivation

The theory of signatures for paths, originating in rough path theory, has established signatures as powerful feature maps for streamed data, extracting nonlinear and algebraic information from complex time series. Classical universal approximation theorems guarantee that linear functionals of a path's signature can approximate any continuous functional on suitable spaces of paths, underpinning many applications in machine learning and quantitative finance. However, these results rely on weakly geometric rough paths—those naturally arising when iterated integrals are defined via Stratonovich integration.

The present work extends the universal approximation theorem to signatures of rough paths that are not necessarily weakly geometric, particularly those built from Itō-type integration, which is canonical in financial mathematics due to martingale properties and modeling fidelity. The authors introduce path extensions by time and rough path bracket (or quadratic variation) and show that linear functionals of extended signatures approximate arbitrary continuous functionals uniformly on compact sets of rough path spaces.

Algebraic and Analytic Framework

The paper rigorously builds on the tensor algebra of the path's space, discussing truncated and extended tensor algebras, and group-like elements. It details the classical shuffle property for the signature of weakly geometric rough paths (Stratonovich-type), crucial for Stone-Weierstrass theorem applications, and introduces a quasi-shuffle property for signatures of non-weakly geometric rough paths (Itō-type), obtained by appropriately extending the path.

A key construction is the bracket extension: for a path X, the bracket [X]t=X0,t⊗X0,t−(X0,t(2)+(X0,t(2))⊤) captures quadratic variation or rough path bracket information. The path extended via time and bracket is shown to yield a signature with the required algebraic closure (quasi-shuffle property), enabling universal approximation.

Universal Approximation Theorem

The central result is the universal approximation property for linear functionals of the signature of rough paths extended by time and brackets (quadratic variation): for any compact subset of the space of rough paths, any continuous functional can be uniformly approximated (arbitrarily closely) on this subset by a linear functional of the extended signature. Stone-Weierstrass arguments are invoked, leveraging the quasi-shuffle algebraic structure.

This generalizes the classical result for weakly geometric rough paths, now allowing Itō signatures (non-group-like) and providing theoretical justification for using the Itō signature as a regression basis for path-dependent functionals, including those naturally appearing in finance.

Pathwise and Stochastic Integration

The paper introduces pathwise stochastic integration properties (γ-RIE), generalizing Föllmer’s framework, enabling signatures to be built by limits of Riemann sums and connecting Stratonovich, Itō, and backward Itō integration (via the parameter γ). For paths with finite p-variation, canonical rough path lifts are constructed, and their signatures defined and shown to satisfy universal approximation theorems.

In probabilistic settings, the theory is applied to continuous semimartingales. Signatures defined via stochastic Itō integration of continuous semimartingales, extended by quadratic variation, admit the universal approximation property for almost every path.

Numerical Experiments and Financial Applications

Numerical experiments are carried out in the context of model calibration and option pricing in mathematical finance, illustrating the practical implications of extending the path by time and quadratic variation for signature regression models.

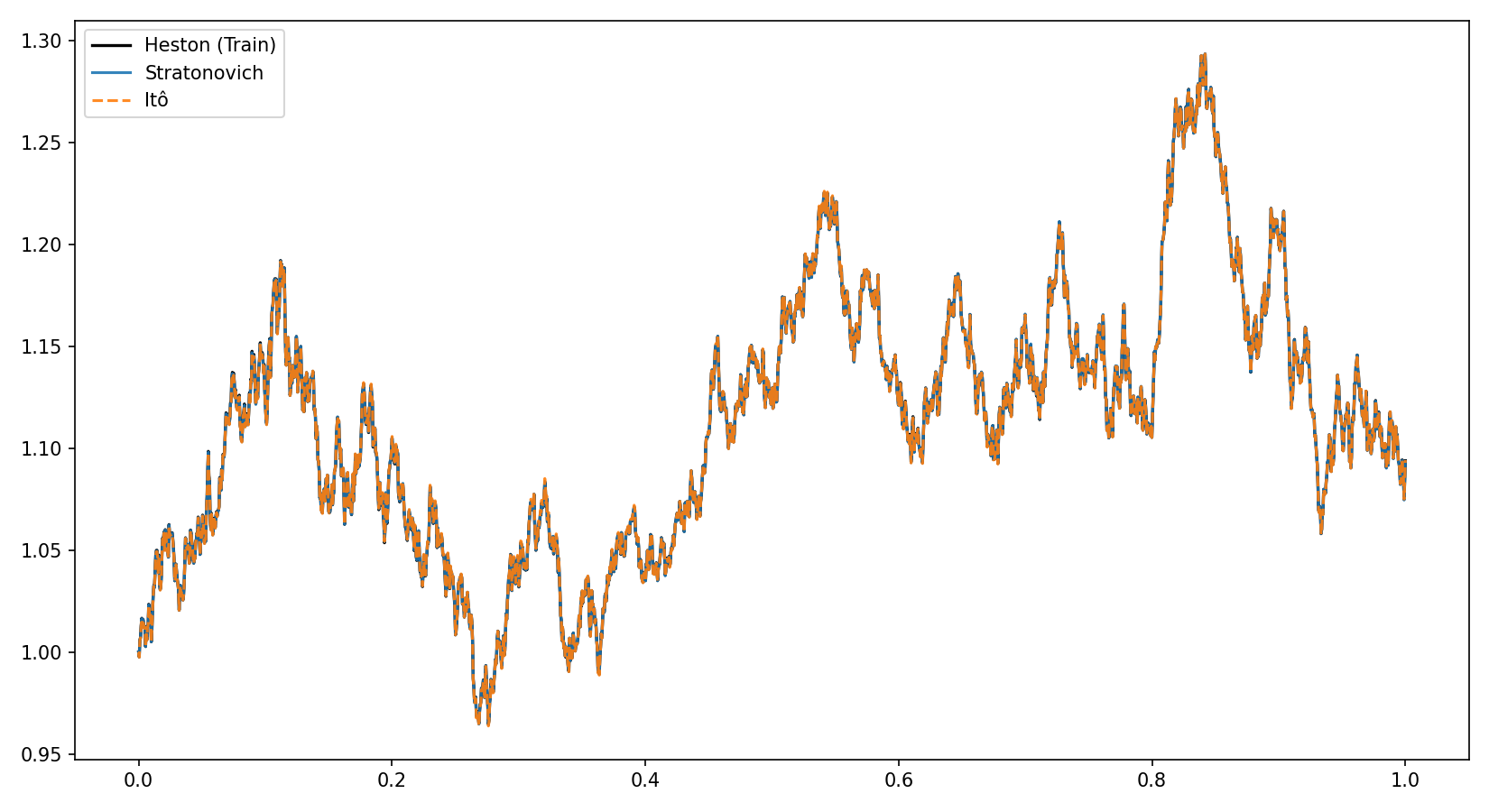

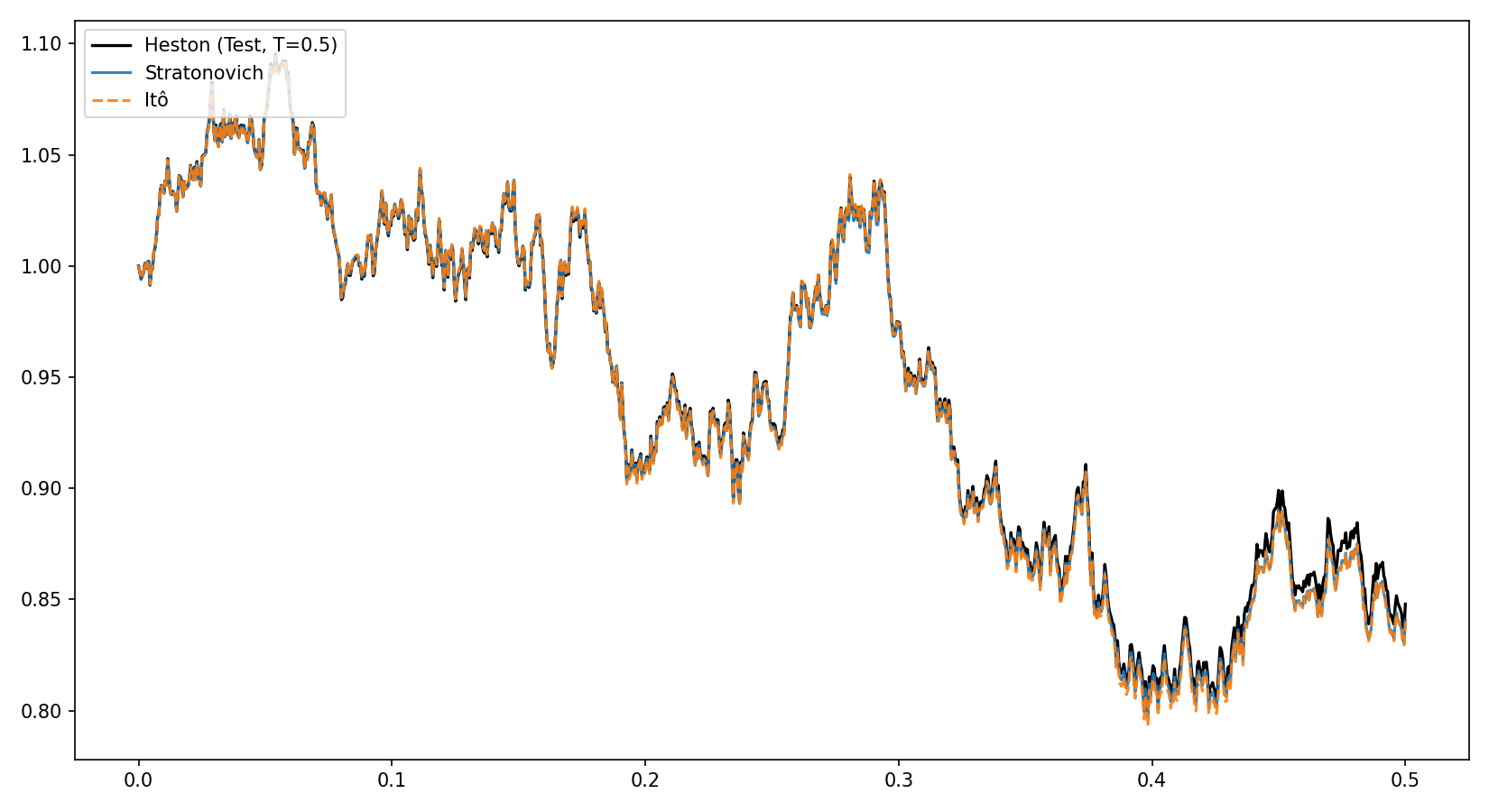

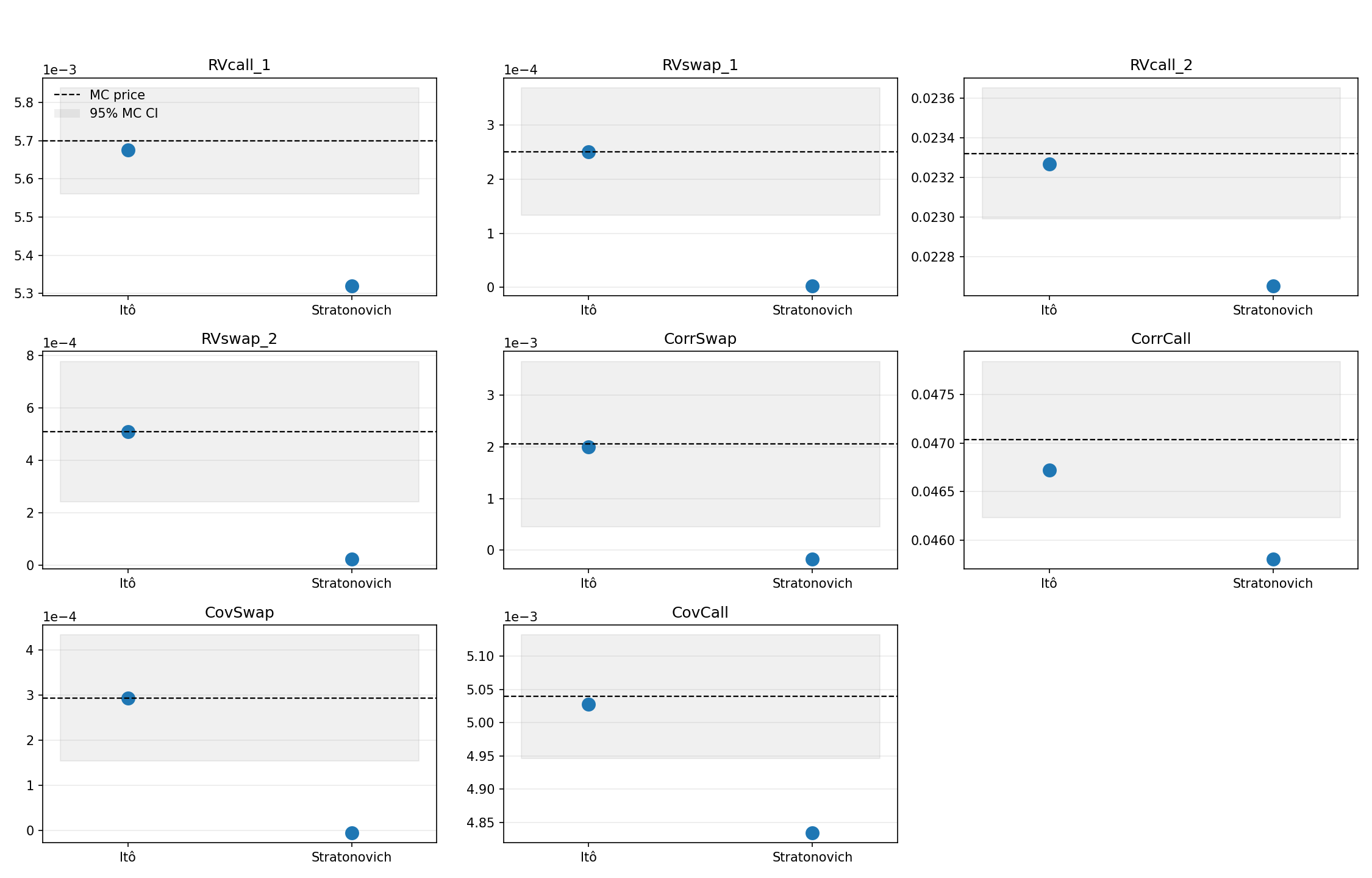

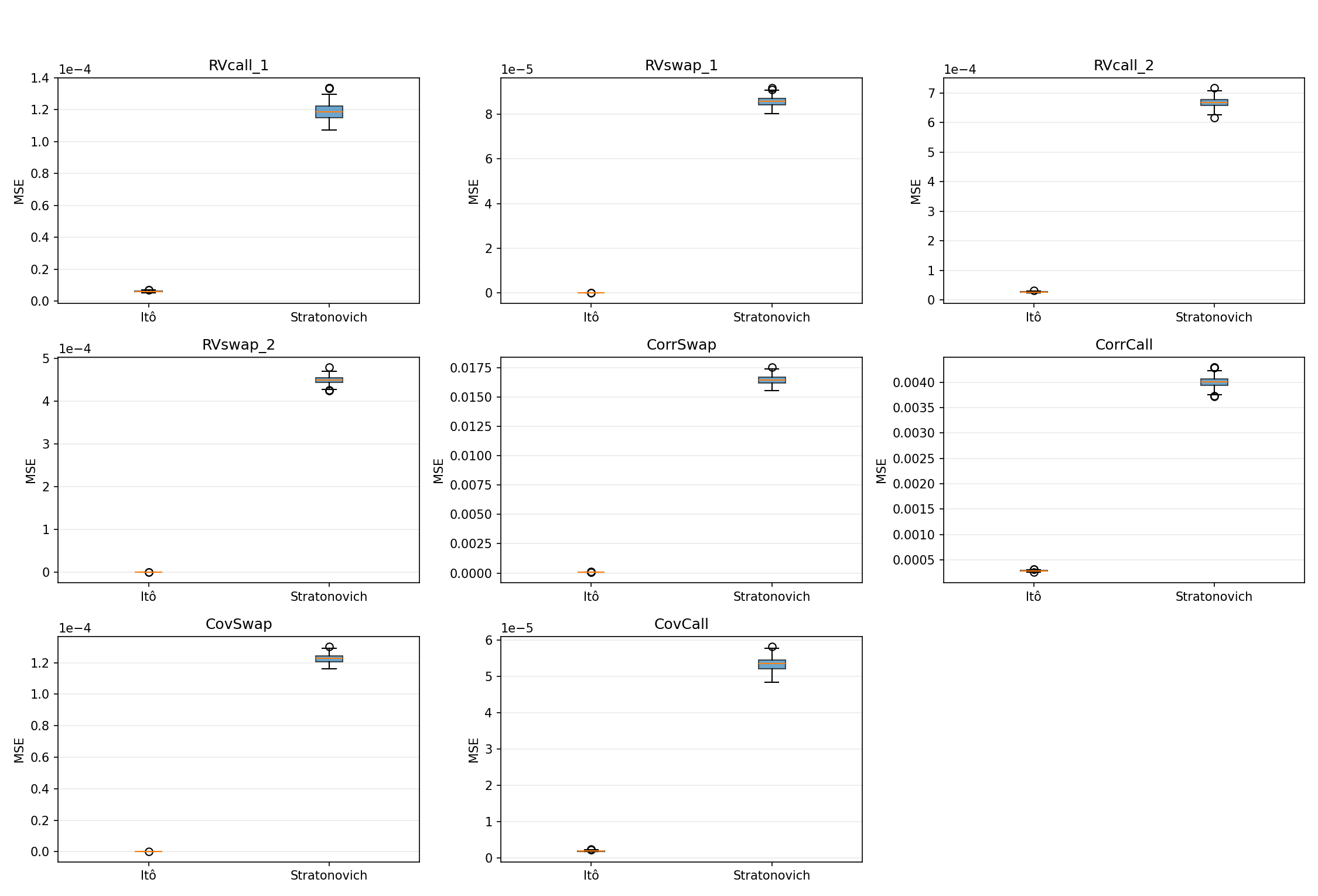

When the underlying dynamic is Brownian (whose quadratic variation coincides with time), both Stratonovich and Itō signatures perform comparably in regression and pricing tasks, with negligible differences:

Figure 1: In-sample calibration of signature models for Heston dynamics, showing near-identical fit for Stratonovich and Itō signatures.

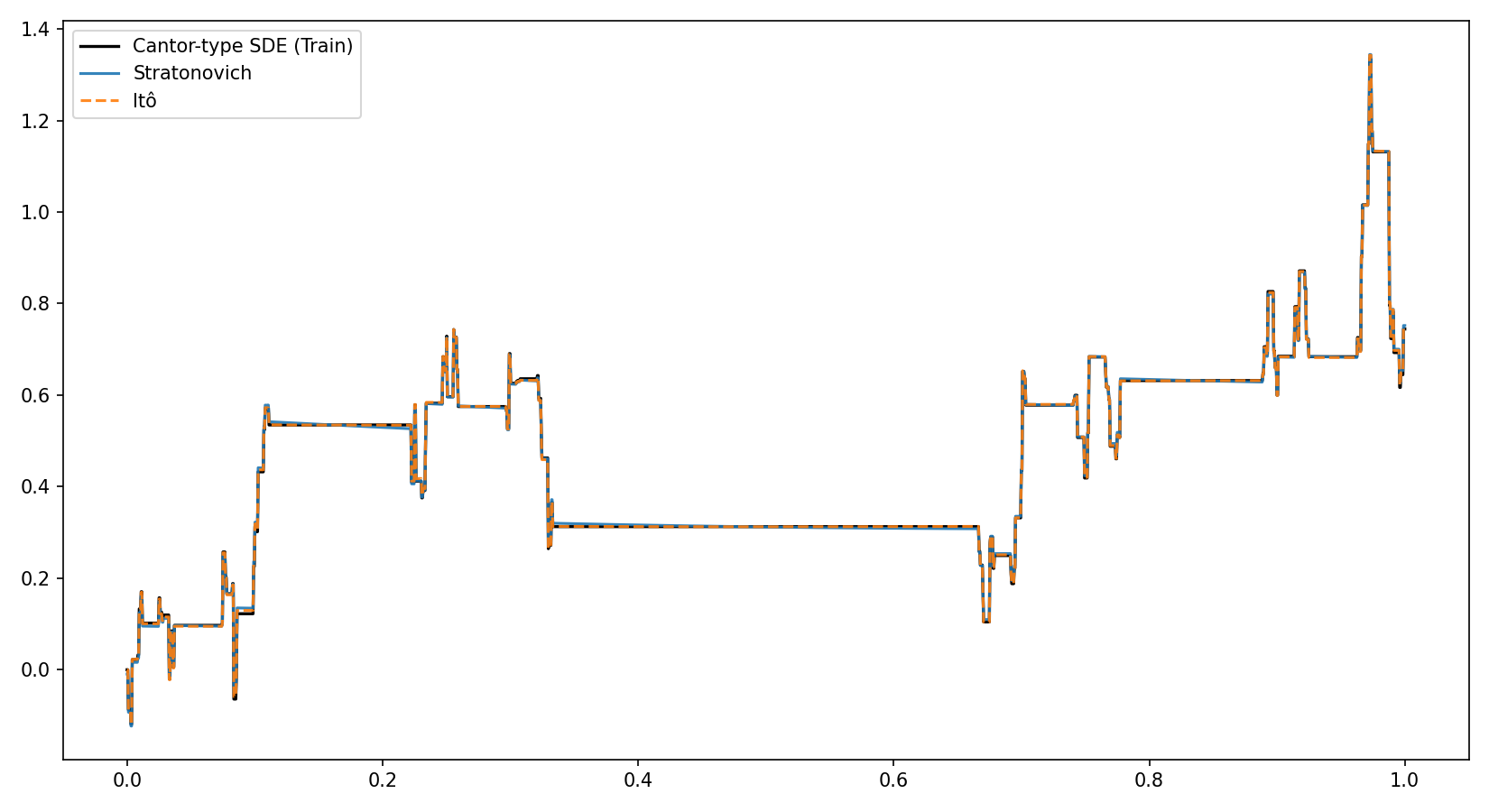

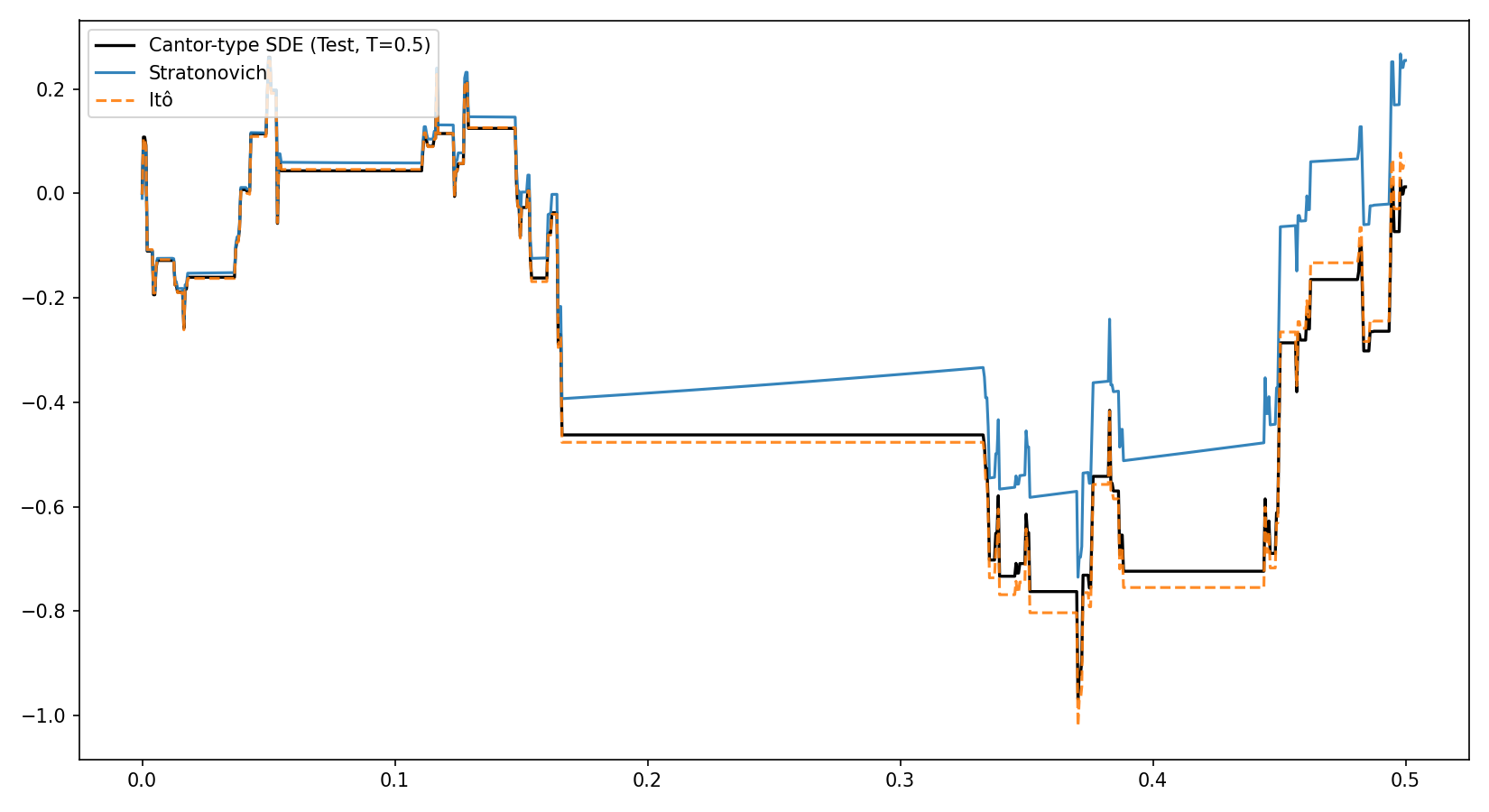

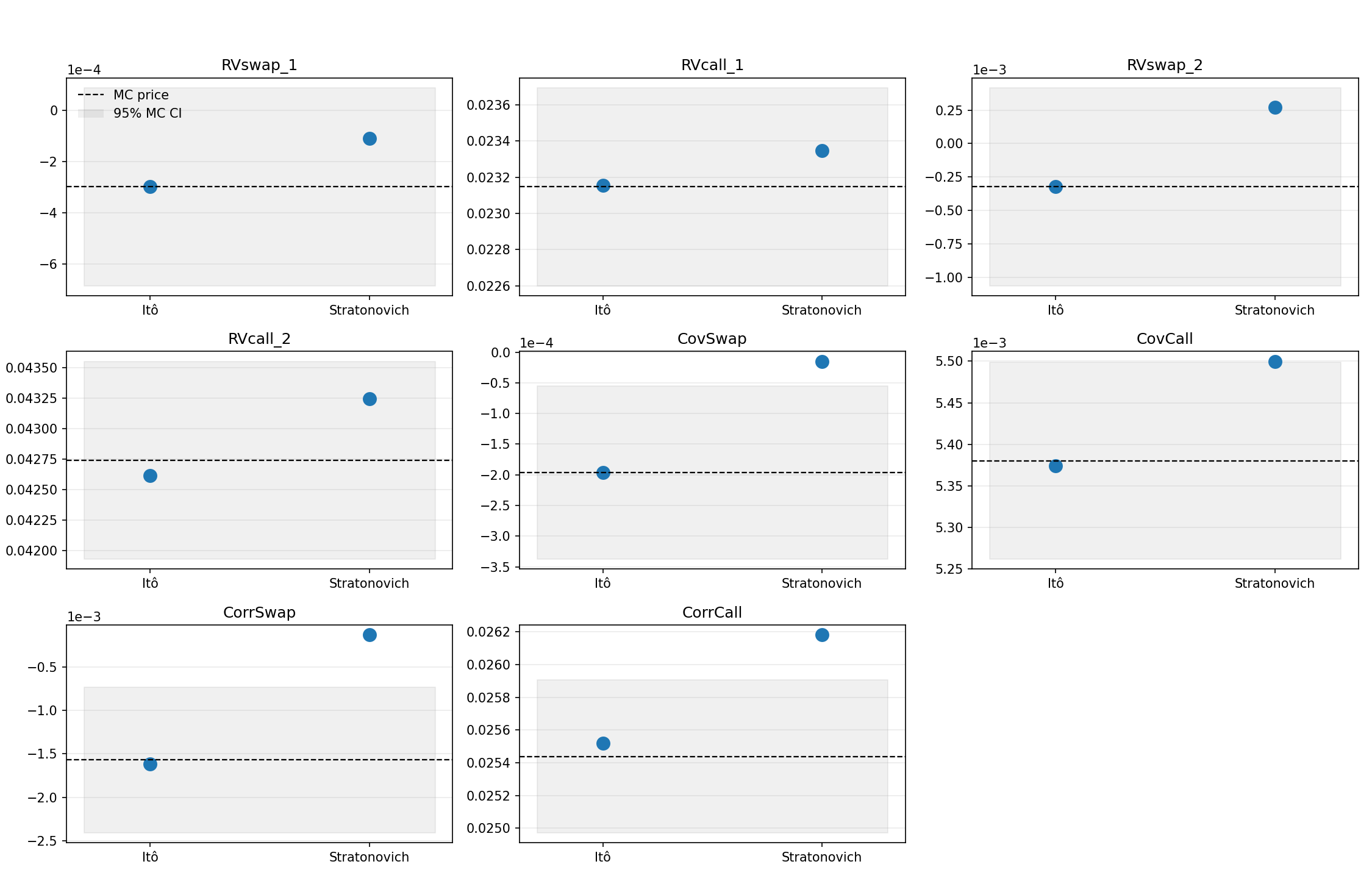

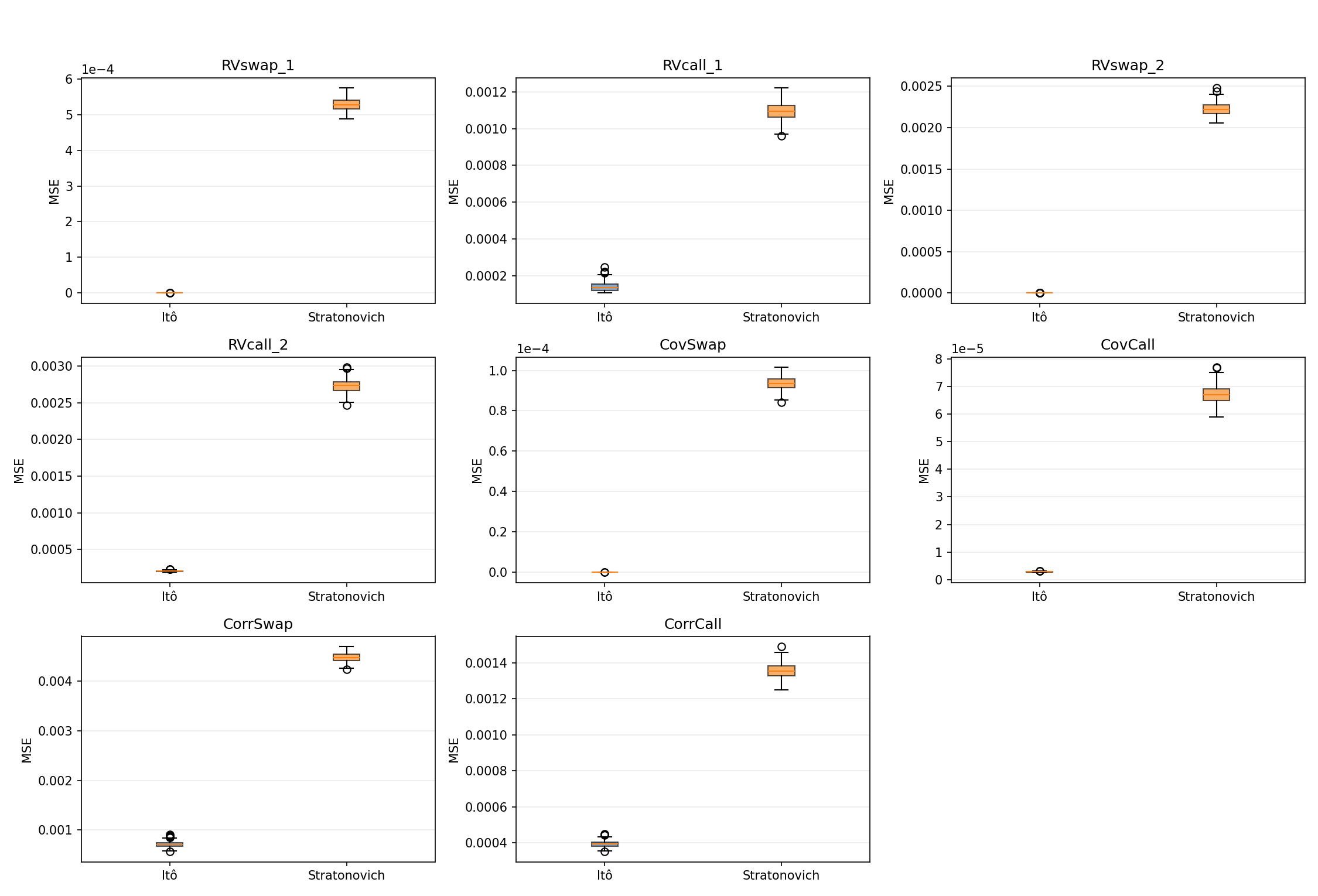

For models with nontrivial quadratic variation (e.g., singular time-changed SDEs, payoffs depending on realized variance/covariance/correlation), extending the path by quadratic variation yields significantly improved out-of-sample performance and more accurate pricing:

Figure 2: In-sample calibration illustrating advantage of Itō signature for singular time-changed SDE, out-performing Stratonovich signature.

Signature-based payoff regression and pricing—with extension by quadratic variation—results in lower mean-squared errors and prices closely matching Monte Carlo benchmarks, especially for payoffs depending explicitly on realized quadratic variation, covariance, and correlation:

Figure 3: Comparison of signature-regressed prices with Monte Carlo prices for derivative payoffs dependent on realized quadratic variation.

Figure 4: Signature regression pricing for correlation/covariance options, showing Itō signature superiority for extended path models.

Implications, Theory, and Outlook

The main implication is the theoretical justification for using Itō signatures—extended by time and quadratic variation—as universal bases for regression and calibration of path-dependent functionals, particularly in finance where quadratic variation is information-rich and modeling via Itō calculus is standard. This also motivates the use of signature-based regression beyond classical settings, such as in modeling assets with irregular or singular volatility dynamics.

From a practical standpoint, the results inform model calibration, pricing, and potentially hedging strategies, suggesting that quadratic variation extension should be incorporated in signature-based learning models for option pricing and risk management.

Future directions include generalizing the signature approach to jump processes and rough volatility models, investigating statistical estimation and consistency for signature-based methods (including Lasso estimator variants), and further studying the algebraic and geometric properties required for universal approximation in broader stochastic settings.

Conclusion

This paper rigorously extends the universal approximation property to signatures of rough paths that are not weakly geometric, by path extension with time and rough path bracket terms. It proves the suitability of Itō-type signatures for regression and functional approximation and demonstrates their practical advantages for calibration and pricing in financial applications, especially where quadratic variation encodes critical information. The results unify signature-based learning approaches under both Stratonovich and Itō viewpoints and provide robust foundations for signature-based methods in quantitative finance and beyond.