Early Detection of Latent Microstructure Regimes in Limit Order Books

Published 22 Apr 2026 in cs.LG, q-fin.TR, stat.ME, and stat.ML | (2604.20949v1)

Abstract: Limit order books can transition rapidly from stable to stressed conditions, yet standard early-warning signals such as order flow imbalance and short-term volatility are inherently reactive. We formalise this limitation via a three-regime causal data-generating process (stable $\to$ latent build-up $\to$ stress) in which a latent deterioration phase creates a prediction window prior to observable stress. Under mild assumptions on temporal drift and regime persistence, we establish identifiability of the latent build-up regime and derive guarantees for strictly positive expected lead-time and non-trivial probability of early detection. We propose a trigger-based detector combining MAX aggregation of complementary signal channels, a rising-edge condition, and adaptive thresholding. Across 200 simulations, the method achieves mean lead-time $+18.6 \pm 3.2$ timesteps with perfect precision and moderate coverage, outperforming classical change-point and microstructure baselines. A preliminary application to one week of BTC/USDT order book data shows consistent positive lead-times while baselines remain reactive. Results degrade in low signal-to-noise and short build-up regimes, consistent with theory.

The paper introduces a causal three-regime model for latent microstructure detection in LOBs, ensuring early warning with positive lead-time.

It employs a trigger-based detector with MAX aggregation across channels like depth erosion and HMM entropy, validated through rigorous simulation and real-data experiments.

Depth erosion is confirmed as a key early indicator, underscoring the practical benefit of real-time adaptive monitoring for preempting liquidity stress.

Early Detection of Latent Microstructure Regimes in Limit Order Books

Problem Formulation and Causal Regime Modeling

This paper ("Early Detection of Latent Microstructure Regimes in Limit Order Books" (2604.20949)) addresses the limitations inherent in conventional early-warning signals for limit order books (LOBs), such as order flow imbalance (OFI) and volatility-based indicators. These standard detectors are fundamentally reactive, responding only to stress regimes after onset, thereby guaranteeing zero or negative detection lead-time relative to market dislocation.

The authors introduce a causal three-regime data-generating process (DGP)—consisting of stable, latent build-up, and stress states—subject to regime persistence and temporal drift. Transitions are deliberately restricted to enforce causal ordering, ensuring that observable stress is always preceded by a latent build-up phase. The emission model incorporates additive structured drift active only in the build-up regime, enabling a monotonic change in LOB features preceding overt stress.

The identifiability of the latent regime sequence is formally proved under mild drift and regime persistence assumptions, leveraging the distinguishability of monotonic drift dynamics against stationary noise. The transition matrix design precludes direct transition from stable to stress and mandates recovery through stable, modeling realistic LOB regime cascades and facilitating theoretical guarantees for early detection.

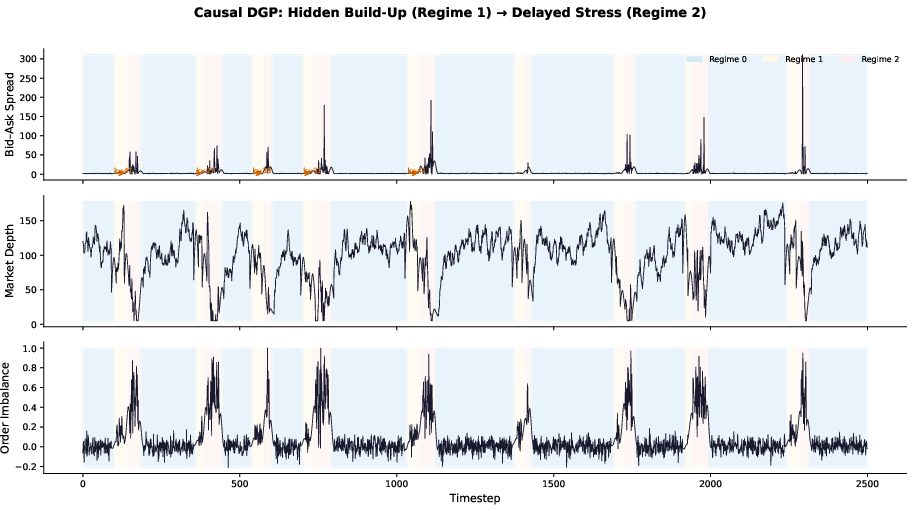

Figure 1: Simulated LOB features across regimes. The build-up regime (shaded orange) displays gradual depth erosion and mild spread widening before stress onset, while imbalance remains within the stable distribution, evidencing the failure of flow-based detectors.

Theoretical Guarantees for Early Detection

Two complementary theoretical results are derived. First, a drift-to-noise ratio (η=α/v⊤Σv) condition is shown to be sufficient for strictly positive expected lead-time: early detection is guaranteed when η>2log(1/δ)/T1. Second, a closed-form lower bound for the probability of early detection (P(τ<σ)) is specified, monotonic in SNR and build-up duration, via rigorous coupling between CUSUM stopping time and partial sum concentration under monotonic drift.

These bounds demonstrate that the feasibility of early detection depends structurally on regime dwell times and the SNR in observed features. Coverage is analytically constrained: episodes with low SNR or short build-up phases are provably hard to detect pre-stress, as confirmed in simulation.

Methodology: Trigger-Based Detector with MAX Aggregation

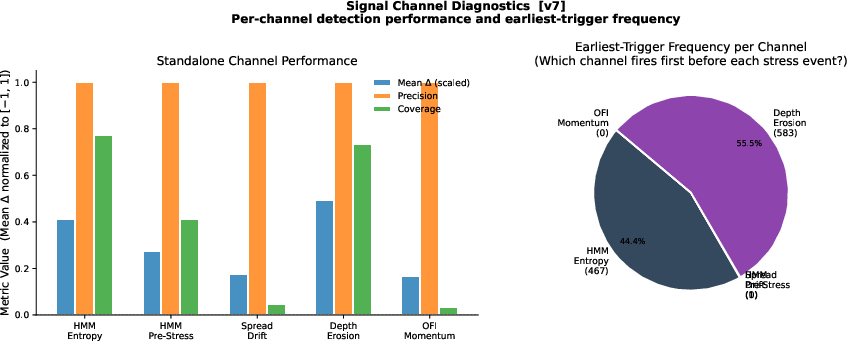

The proposed detector aggregates multiple LOB signal channels—HMM entropy, depth erosion, spread drift, and OFI momentum—via a theoretically motivated MAX rule, justified under explicit sparsity and weak-correlation assumptions. The detection logic incorporates a rising-edge condition (requiring a positive derivative in the composite score), adaptive thresholding based on the empirical CDF of signal scores, and suppression of burst detection.

The MAX aggregation is shown to enhance recall without compromising precision in the presence of channel sparsity. The rising-edge trigger reliably activates at the onset of score climbs, terminating early in drift transitions rather than at regime peaks.

Figure 2: Per-channel detection diagnostics in simulation. Depth erosion and HMM entropy account for nearly all early triggers, while spread drift and OFI momentum contribute robustness but never fire first.

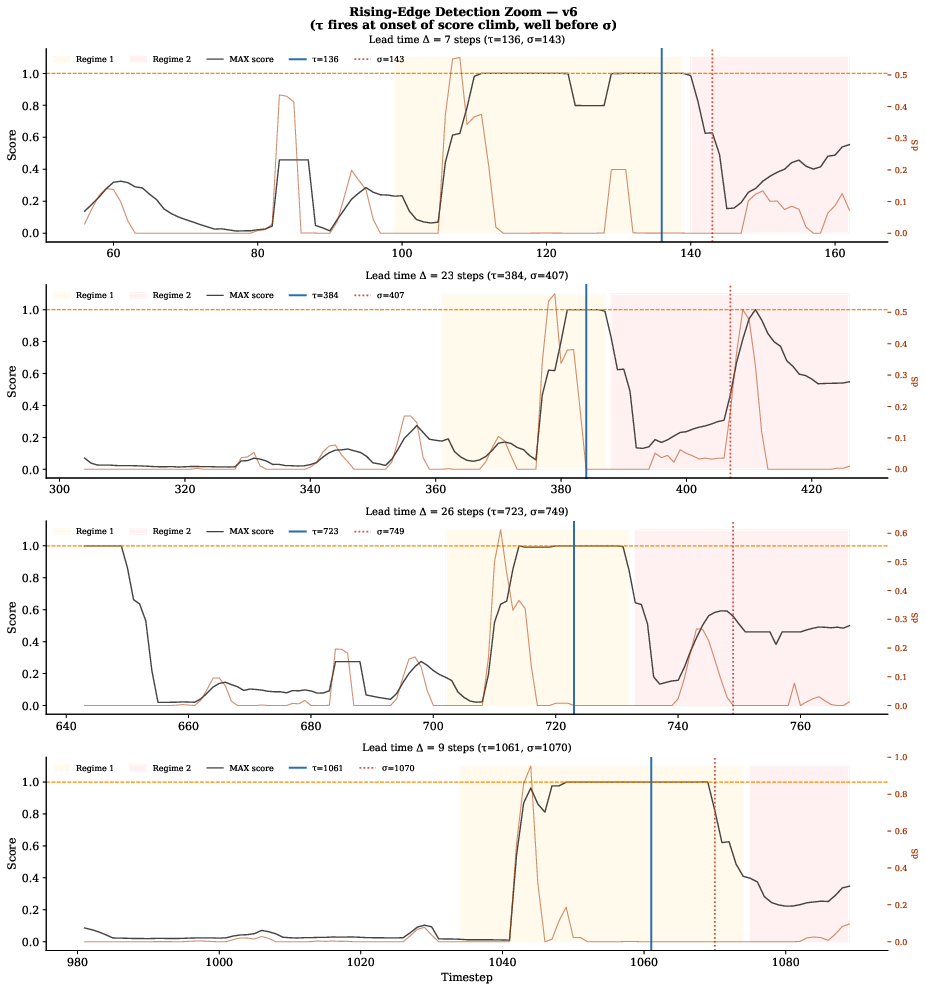

Figure 3: Rising-edge detection on representative stress episodes. Triggers (blue) consistently precede stress onset (red dotted), delivering lead-times from +7 to +26 timesteps.

(Figure 4)

Figure 4: Adaptive trigger performance over a 3000-timestep run. MAX instability score rises in build-up, fires before stress, and remains silent in stable phases. No trigger fires on pure noise or reactive volatility spikes.

Empirical Validation: Simulation and Real-Data Evidence

Extensive simulation across 200 runs produces mean lead-time +18.6±3.2 timesteps, precision 1.00±0.00, and coverage 0.54±0.06. Baseline detectors (CUSUM, BOCPD, imbalance, volatility) exhibit either negative lead-times or poor precision. HMM posterior thresholding improves lead-time but does not match the trigger logic.

Conditional analysis of missed detections reveals that coverage deficiencies occur exclusively in parameter cells with low SNR and short build-up—exactly where theoretical bounds predict vacuous detection probability. Robustness grids confirm monotonic scaling of performance with SNR and dwell time.

The precision–recall frontier shows the adaptive trigger dominates baselines across all threshold percentiles. Ablation studies demonstrate that removing the rising-edge condition, substituting SUM aggregation, or omitting HMM entropy channel reduces coverage and/or precision markedly.

(Figure 5)

Figure 5: Threshold sensitivity and precision–recall curves. Adaptive trigger retains strong performance across a broad threshold range. Baselines remain reactive and offer poorer precision–recall trade-off.

Economic Interpretation and Practical Implications

Depth erosion emerges as the most causally proximate and interpretable leading indicator of latent build-up in LOB liquidity, consistent with microstructure theory models of liquidity withdrawal and informed trading. High entropy in HMM filtering signals model uncertainty, which often precedes regime transitions.

Conventional OFI and volatility measures are structurally reactive, failing to deliver positive lead-time by targeting stress consequences rather than precursors. The economic mechanism validated is that depth deterioration anticipates, rather than follows, liquidity stress, making depth-based detection both theoretically and empirically superior for early warnings.

For practitioners, this suggestion is technically compelling: real-time monitoring systems should prioritize structural depth metrics and explicitly model latent regime transitions, using rising-edge triggers and adaptive thresholds for robust, statistically defensible advance detection.

Preliminary Real-Data Application

A pilot study on BTC/USDT LOB data (1 Hz, 1 week, 5 stress events) applies the detector pipeline using rolling HMM fitting, causal feature z-scoring, and adaptive thresholding. Early detection is achieved in 4/5 episodes, with mean lead-time +38±21 seconds, perfect precision (no false alarms), and coverage $0.80$. Baseline detectors show negative lead-times and lower precision. The lead-trigger channel is exclusively depth erosion, as in simulation.

Limitations include small sample size and reliance on spread-based proxy labels. Intraday non-stationarity challenges model calibration, suggesting future work integrating session-adaptive HMMs and heavy-tailed emission distributions.

Limitations, Trade-Offs, and Future Directions

Theoretical bounds analytically constrain coverage in low SNR / short build-up episodes. The precision–recall frontier and trade-off proposition show that higher lead-time entails lower coverage—a fundamental performance constraint, not a tuning artifact.

Real-data calibration requires robust sessional adaptation and higher-quality stress labelling. Channel structural correlations may attenuate MAX aggregation advantages. Extending statistical validation to larger market samples and refining emission models are explicit future avenues.

Conclusion

The study rigorously formalizes and quantifies the feasibility of early detection of latent build-up pre-stress microstructure regimes in LOBs. Its contributions include identifiability results, explicit drift–noise and probability bounds, and a trigger-based detector validated in simulation and preliminary real markets. Structural liquidity metrics, notably depth erosion, are established as superior early indicators, moving the evaluation emphasis from mere precision and recall to detection lead-time. While limitations and open issues remain, the methodology provides a robust framework for advancing market monitoring and situational awareness in electronic trading venues.