- The paper introduces a framework that refines the QR model by incorporating state-space reduction, empirical timing, and self-consistent market feedback.

- It quantifies event clustering and latency races through empirical inter-event time distributions, aligning simulated outputs with observed market data.

- The model accurately replicates market impact and execution risks, providing a robust tool for strategy evaluation and metaorder analysis.

Bridging the Reality Gap in Limit Order Book Simulation

Introduction

"Bridging the Reality Gap in Limit Order Book Simulation" (2603.24137) develops an executable and data-driven framework for simulating equity market microstructure with high fidelity, targeting the core challenge of producing realistic event dynamics and execution outcomes—specifically for large-tick assets. The approach refines the Queue-Reactive (QR) model by introducing state-space dimensionality reduction, empirical event-time modeling, and a self-consistent market-impact feedback mechanism. Together, these innovations bridge persistent gaps between Markovian simulation behaviors and empirical regularities relevant to trading strategy backtesting and optimization.

From Queue-Reactive to Reality-Reflective Modeling

The classic QR model conditions event intensities on queue sizes but remains Markovian, resulting in exponentially distributed inter-event times and no path-dependence—critical limitations for studying phenomena like latency races and market impact.

To mitigate the data sparsity and overfitting risk inherent in high-dimensional state conditioning, the book state is projected onto a tractable two-dimensional representation: best-level volume imbalance and the bid-ask spread. This projection exploits the empirical sufficiency of order book imbalance for capturing short-term predictive structure while enabling robust estimation from limited data.

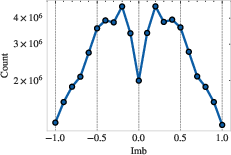

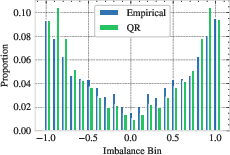

Figure 1: Left: The imbalance bin at zero is more populated than bins corresponding to highly imbalanced books, indicating that the state projection adequately captures statistical density where it matters.

Event type distributions, activity levels, and conditional statistics in the simulated environment demonstrate quantitative agreement with real data, validating the marginal fidelity of the reduced state-space baseline.

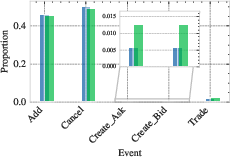

Figure 2: Empirical event-type distributions indicate the QR model reproduces the Add/Cancel/Trade proportions with high accuracy.

Nevertheless, the baseline exhibits severe limitations: its exponential inter-event time assumption fails to capture the pronounced clustering of events observed in high-frequency markets, and its lack of history-dependent feedback results in unrealistic market impact responses.

Empirical Microstructure: Latency Races and Event Clustering

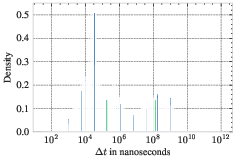

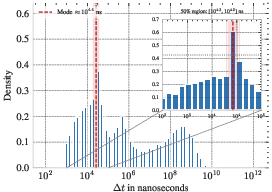

Detailed analysis of inter-event times in market data exposes a multi-modal structure, with a sharp peak around 29 microseconds—direct evidence of exchange round-trip latency and simultaneous order arrivals consistent with latency races.

Figure 3: Left: The empirical inter-event time distribution (log-scale) reveals a dominant mode corresponding to exchange-level round-trip latency. Several modes are evident, distinguishing true reaction times from independent asynchronous arrivals.

Implementing an empirical (or parametric GMM-based) event timing model within the QR framework, the simulation accurately mirrors the observed distribution of event clustering. This enhancement preserves the original event sequence but enables the simulation of competitive fill dynamics essential for realistic high-frequency trading (HFT) backtesting and queue-position modeling.

Market Impact and Path-Dependence

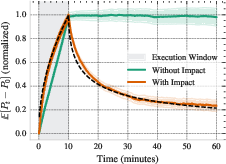

The second major extension is a feedback mechanism for market impact. The model accumulates signed trade flow through a power-law decay kernel, introducing a state variable ϕt that modulates event rates. The event probability adjustment is mean-reverting but asymmetric: only events opposed to the recent flow are amplified, reflecting empirical partial reversion post-metaorder.

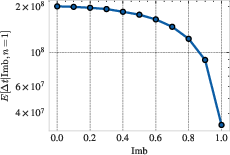

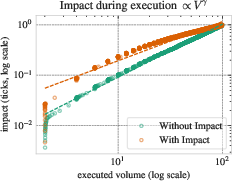

Figure 4: Left: The market impact of a metaorder with and without feedback reveals concave execution-phase impact and partial reversion, consistent with empirical metaorder studies. Right: The log-log slope during execution demonstrates the transition from linear to concave impact with the feedback kernel.

Crucially, by simulating large child-order metaorders, the model quantitatively matches both the peak and post-trade reversion of price impact, aligning with the square-root law and the no-arbitrage theory of impact decay. Calibration flexibility permits tuning against empirical curves or theoretical forms.

Realism in Strategy Evaluation: Case Studies

Two trading strategies illustrate the impact of the model enhancements:

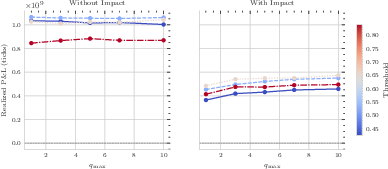

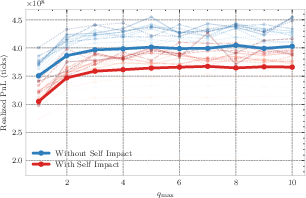

- Mid-Frequency Alpha Strategy: This strategy responds to an exogenous Ornstein-Uhlenbeck signal. When self-impact is included in the kernel, realized P&L becomes highly sensitive to maximum inventory, and excess trading capacity leads to edge erosion due to the accumulating adverse impact of one’s own flow, a phenomenon absent in no-impact simulations.

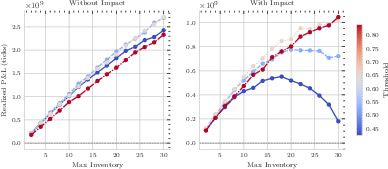

Figure 5: Left: Realized P&L as a function of order size qmax plateaus due to limited available depth, confirming the effectiveness of realistic queue modeling.

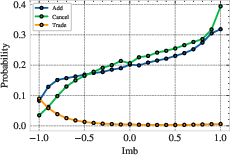

- Latency-Race HFT Strategy: A high-frequency strategy monitors order book imbalance and triggers at extreme thresholds, subject to fill uncertainty arising from latency races. The fill probability is directly linked to whether subsequent events are within the exchange latency window, accurately modeling competitive fill risk and self-impact cost.

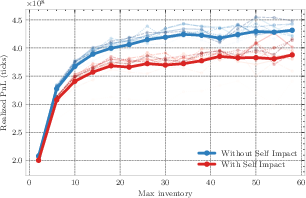

Figure 6: Realized P&L for the HFT strategy flattens earlier and at a lower level under self-impact, quantifying the incremental cost of the strategy's own footprint—an effect invisible in Markovian or passive-impact models.

Quantitatively, the studies show that ignoring self-impact and proper event timing leads to systematic overstatement of expected strategy performance, especially in aggressive regimes.

Parameter Stability and Model Robustness

Temporal robustness is confirmed by re-estimating parameters on multiple six-month non-overlapping intervals: event probabilities and conditional inter-event time shapes are statistically stable, indicating that the reduced state and conditional event models capture enduring microstructural features rather than noise.

Implications and Future Work

This framework provides a robust recipe for constructing limit order book simulators: state projection, empirical/probabilistic conditional estimation, and modular adaptation to event timing and feedback effects. It directly addresses practitioner needs for realistic, interactive simulation environments for strategy testing, risk management (including execution cost and impact), and optimization under microstructure constraints.

The modular structure allows for future enhancements, including:

- Integrating Hawkes or similar processes for order-flow autocorrelation (long memory in trade signs).

- Path conditioning beyond the current state (e.g., including queue age or survivor biasing for order persistence).

- Extension to small-tick assets or alternative asset classes via alternative state projections or liquid tick models.

- Further empirical calibration using proprietary fill/miss data for high-fidelity fill modeling in latency race simulations.

Conclusion

By addressing both event clustering (latency race phenomena) and history-dependent market impact in a reduced and empirically validated framework, "Bridging the Reality Gap in Limit Order Book Simulation" establishes a practical and extensible methodology for constructing LOB simulators that maintain essential microstructural realism for a broad range of academic and industrial applications. These developments are immediately relevant for advanced strategy assessment, optimal execution, and market microstructure research, and they offer a systematic path forward for adapting QR models to ongoing advances in market technology and participant behavior.