Causality versus Serial Correlation: an Asymmetric Portmanteau Test

Published 5 Jun 2026 in econ.EM | (2606.07715v1)

Abstract: This paper studies specification testing in dynamic linear models in the presence of omitted variables. The null hypothesis of interest is weak exogeneity: shocks have zero conditional expectation given their own past and the past of omitted variables. Existing tests based on quadratic forms of serial cross-correlations suffer from size distortions because their variance incorporates symmetric dependence in both directions, including causality from past shocks to present omitted variables (inverse causality). This paper proposes an asymmetric Portmanteau test that isolates violations of weak exogeneity from inverse causality, is asymptotically normal under the null, and does not require a parametric specification of the joint dynamics. An empirical application examines the Economic Policy Uncertainty shock series and rejects its weak exogeneity. Addressing this failure by controlling for omitted variables changes the estimated inflation response from negative to positive, suggesting a supply-side shock interpretation.

The paper introduces an asymmetric Portmanteau test that isolates the influence of omitted variable dynamics by correcting for inverse causality when testing weak exogeneity.

The methodology decomposes traditional statistics into sum-of-squares and cross-products, achieving asymptotic normality and improved finite-sample size control.

Empirical analysis with EPU shocks shows the test differentiates between short-run dynamics and genuine exogeneity violations, impacting policy interpretation.

Asymmetric Portmanteau Testing: Distinguishing Causality from Serial Correlation in Dynamic Linear Models

Motivation and Problem Formulation

The inferential validity of structural models in macroeconometrics, including SVARs and local projections, hinges critically on the correct specification of exogeneity for identified shocks. In practical implementations, misspecification arising from omitted variables can result in structural shock series that are not truly exogenous with respect to all relevant informational histories. Standard Portmanteau tests based on quadratic forms of serial cross-correlations, such as those developed by Hong, are widely employed to detect temporal dependencies. However, these statistics are intrinsically symmetric: their variance incorporates dependencies in both directions—specifically, from lagged omitted variables to current shocks (the target of exogeneity testing), but also the "inverse causality" channel, from past shocks to present omitted variables.

This confounding of directional effects leads to systematic size distortions and interpretational difficulties, especially because macroeconomic structural shocks are expected to propagate to omitted macro variables over time, sometimes in highly persistent or nonlinear ways. The null of "weak exogeneity"—that structural shocks have zero conditional mean given all relevant past information (including omitted variables)—therefore cannot be reliably tested with symmetric statistics that do not distinguish between causal directions.

Methodology: The Asymmetric Portmanteau Statistic

The core innovation is an asymmetric Portmanteau test designed to isolate violations of weak exogeneity, specifically excluding contamination from inverse causality. The classical Portmanteau statistic is given, for two zero-mean stationary multivariate processes Xt (shock) and Zt (omitted variables), by:

Tω=j=1∑T−1ω(j)Q(j),Q(j)=∥ΓXZ(j)∥F2

where ΓXZ(j) is the sample cross-covariance at lag j, and ω(j) are kernel-based weights.

This statistic is decomposed into a sum of squares and a sum of cross-products. The latter term introduces a symmetry such that inference on weak exogeneity can be invalidated by the presence of reverse (inverse) causality.

The proposed correction is to subtract the portion of the statistic attributable to inverse causality, yielding the asymmetric form:

Tωc=Tω−Cω

where Cω captures cross-products associated with time orderings not aligned with the weak exogeneity direction, as formally defined in the paper. The resulting test statistic has the key property that its mean and variance under the null depend only on the weighting scheme and moments of the omitted variable process, not on the detailed joint dynamics between X and Z.

The induced conditional moment restrictions on Zt0 (notably conditional homoskedasticity and homokurtosis) are readily testable and empirically interpretable, and their stringency is a deliberate trade-off to avoid any parametric modeling of the (potentially large-dimensional and misspecified) omitted variable space.

Large-Sample and Finite-Sample Properties

Asymptotic Validity

Under standard regularity conditions, the asymmetric statistic is shown to be asymptotically normal under the null of weak exogeneity, provided appropriate kernel decay and moment conditions hold. The asymptotic variance is consistently estimable and depends only on the autocovariance structure of the omitted variable. Notably, the more stringent rate requirement for the bandwidth parameter Zt1 (Zt2) is necessitated by the need to limit the effect of the sum-of-squares component for nearly uncorrelated processes, but can be relaxed under additional weak dependence conditions.

Under fixed alternatives—including linear and nonlinear dependence from past Zt3 to present Zt4—the test achieves the same local power as classic Portmanteau statistics, as the correction term vanishes to leading order.

Monte Carlo Evidence

Comprehensive simulation exercises confirm the size advantages: in DGPs where weak exogeneity holds but Zt5 depends on past Zt6 (via linear, nonlinear, or conditional variance effects), the benchmark Portmanteau test overrejects, especially when omitted variables are persistent or the innovation distribution is heavy-tailed. In contrast, the asymmetric statistic exhibits rejection rates much closer to nominal size across the simulated DGP spectrum.

For alternatives with true violations of weak exogeneity, power curves for the asymmetric statistic and the benchmark Portmanteau are similar; both detect departures when linear dependencies are strong, and neither is powerful against strictly nonlinear alternatives not generating covariance structure.

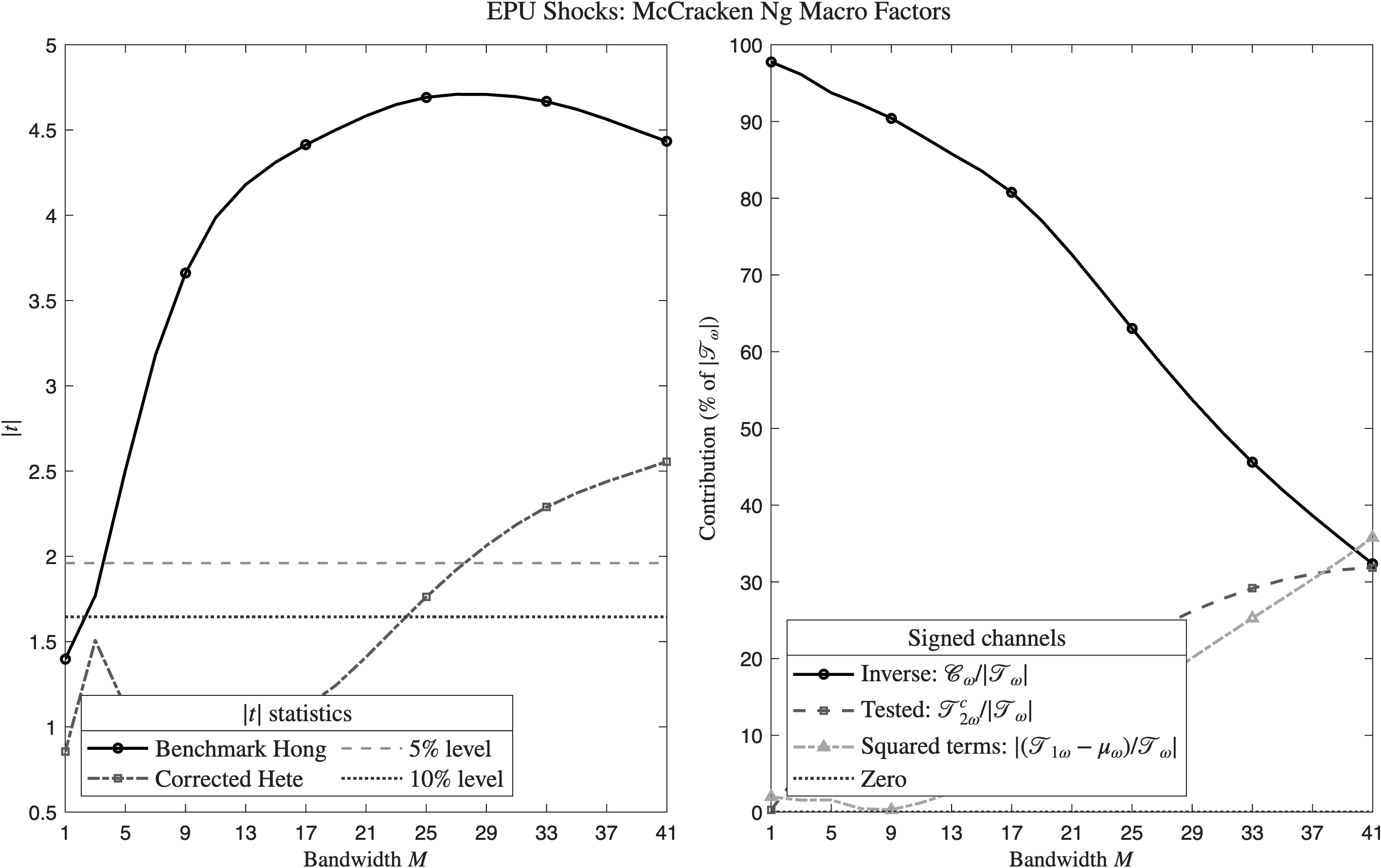

Empirical Illustration: Exogeneity of EPU Shocks

The empirical application tests exogeneity for the Economic Policy Uncertainty (EPU) shocks of Baker, Bloom, and Davis, using McCracken-Ng static factors as a proxy for omitted aggregate macroeconomic information. Using both the standard and the asymmetric statistic, divergent conclusions are drawn regarding the exogeneity of EPU shocks.

Figure 1: Comparison of standard and asymmetric Portmanteau statistics for EPU shocks, highlighting differing rejection horizons and attribution to inverse causality.

At short horizons (small Zt7), the benchmark test rejects exogeneity, but these rejections are almost entirely explained by the inverse causality channel—dependence from past EPU shocks to current omitted factors. Only at higher bandwidths (medium- to longer-term lags) does the asymmetric statistic register significant dependence from omitted variable histories to the shock series, targeting the direction of weak exogeneity.

This distinction has critical applied implications: it prevents practitioners from misattributing evidence of exogeneity violations to short-run dynamics or omitted controls that are in fact driven by post-shock feedback. In the case of the EPU shock, controlling for macro factors alters the estimated inflation response to EPU-induced shocks from negative to positive, offering support for a supply-side interpretation of these shocks in line with recent theoretical models.

Implications and Future Directions

The asymmetric Portmanteau approach makes a robust contribution to macroeconometric inference by enabling specification testing in the presence of unknown or complex omitted variable dynamics, with minimal assumptions and without explicit joint modeling. This is particularly consequential when tracking the evolution of identifiability and invertibility in SVAR and local projection environments with increasingly large information sets.

The methodology can be generalized—via replacement of the cross-covariance with nonlinear dependence measures—to test for more complex forms of weak exogeneity, forsaking only pairwise (linear) dependence. Extensions to high-dimensional omitted variable spaces and kernel distance-based dependence metrics could further increase test sensitivity without inflating size.

In summary, the asymmetric Portmanteau test closes a critical gap in specification testing under incomplete information, particularly for highly persistent and non-Gaussian macroeconomic time series.

Conclusion

The paper "Causality versus Serial Correlation: an Asymmetric Portmanteau Test" (2606.07715) provides a rigorous diagnostic for weak exogeneity of shocks in dynamic linear models with omitted variables. By disentangling causal directions in the serial cross-correlation structure, the paper establishes robust theoretical guarantees and delivers substantial improvements in finite-sample inference. The empirical analysis underscores the importance of clarity about the information set driving structural identification and demonstrates practical policy implications, especially regarding the interpretation of uncertainty shocks in macroeconomic analysis. This contribution is foundational for robust structural inference in the context of partial or over-parameterized macroeconomic environments.