- The paper demonstrates that state-dependent LPs yield causal impulse responses when the conditional mean is linear in the aggregate shock with a state-dependent coefficient.

- It introduces a sieve-based nonparametric estimator that improves estimation under nonlinearity and delivers uniform inference for dynamic heterogeneous effects.

- Monte Carlo simulations and an application to monetary policy reveal that linear LPs may produce biased results, highlighting the advantage of the nonparametric approach.

Causal Identification in State-Dependent Local Projections

Introduction and Conceptual Motivation

The paper "Causal State-Dependent Local Projections" (2605.05404) fundamentally reexamines the conditions under which state-dependent local projections (LPs) yield causal impulse responses in settings where the response to aggregate shocks may be heterogeneous across cross-sectional units. LPs have become standard for characterizing dynamic causal effects due to their robustness to model misspecification and ease of use. However, the validity of their causal interpretation, especially when the effect of the shock is allowed to vary with observable states (i.e., functional heterogeneity), remains a central identification challenge.

The authors provide an explicit, minimal sufficient condition under which state-dependent LPs deliver causal impulse responses: the conditional mean of the response variable at each horizon must be linear in the aggregate shock, with a coefficient that can be an arbitrary function of the state. This condition is satisfied in a broad class of canonical micro–macro models, including first-order perturbation solutions of heterogeneous-agent models and many macro-finance panel models, but fails in the presence of nonlinearities or state-dependent propagation mechanisms. This mapping from microeconomic theory to reduced-form identification is a key conceptual advance.

Functional Sufficiency for Causal State Dependence

The essential identification result is that, under exogenous shocks, if the conditional mean of the outcome at each forecast horizon admits a representation

E[Yi,t+h∣Ft−1,Xt]=gh(Zi,t−1)Xt+ri,h(Ft−1)

where gh(Zi,t−1) is an unknown function and ri,h(Ft−1) is arbitrary, then the LP coefficient function gh(⋅) directly recovers the causal state-dependent impulse response at horizon h. Importantly, this restricts nonlinearity to operate only via the heterogeneity in exposure (via gh), while excluding nonlinearity in the shock or in the dynamic response mechanism.

The problem of identifying causal effects in the presence of heterogeneity is thus sharply framed: while average effects can be causally estimated even under misspecification via scalar LPs, restricting the functional form of heterogeneity (e.g., via linear interaction terms) generically destroys the causal interpretation unless the true function is linear. The interaction coefficient does not represent a causal effect at any unit or a convex average across subgroups, due to non-convex weighting (see below).

Sharp Characterization of the Identification Failure from Linear State Dependence

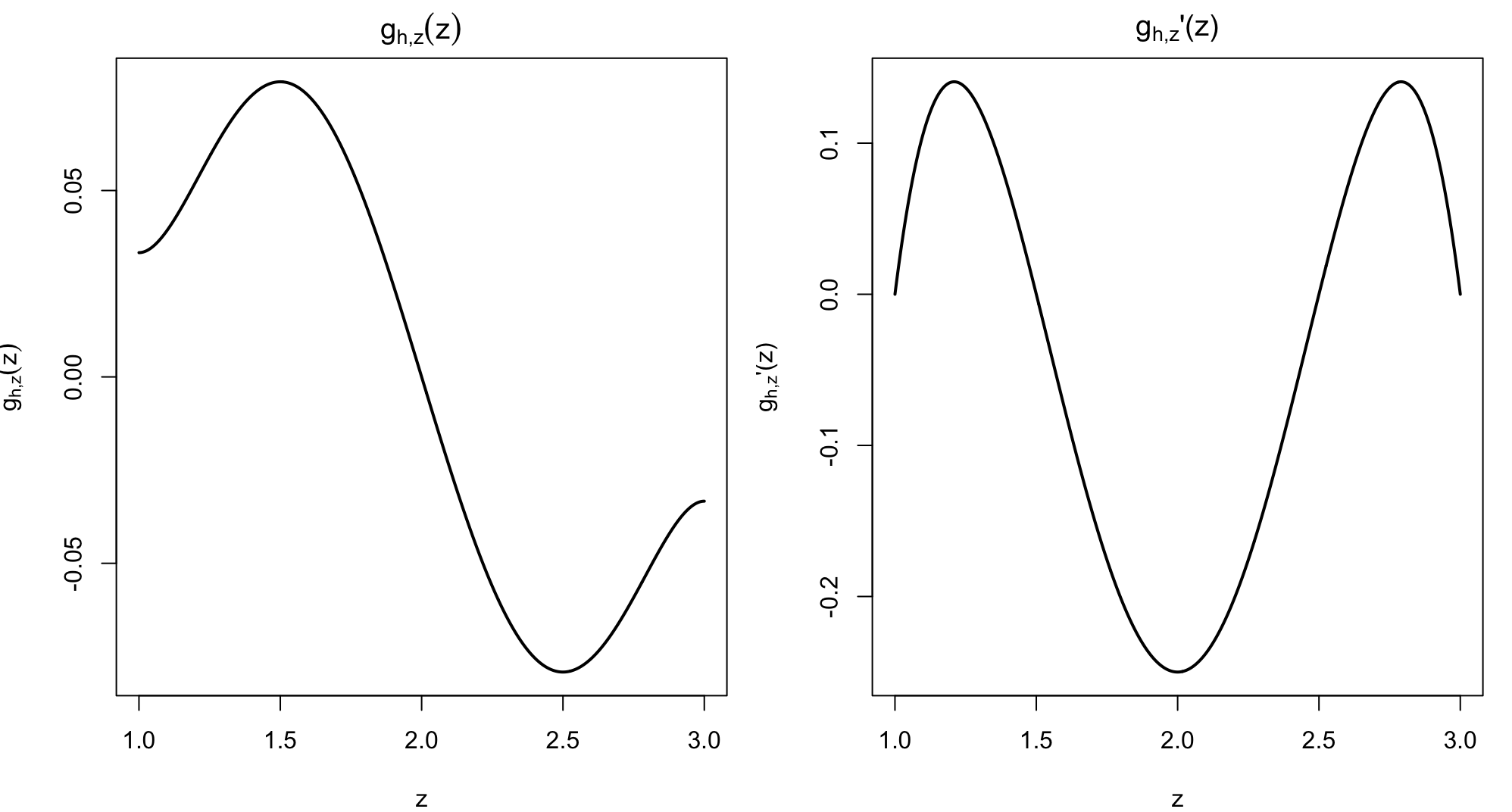

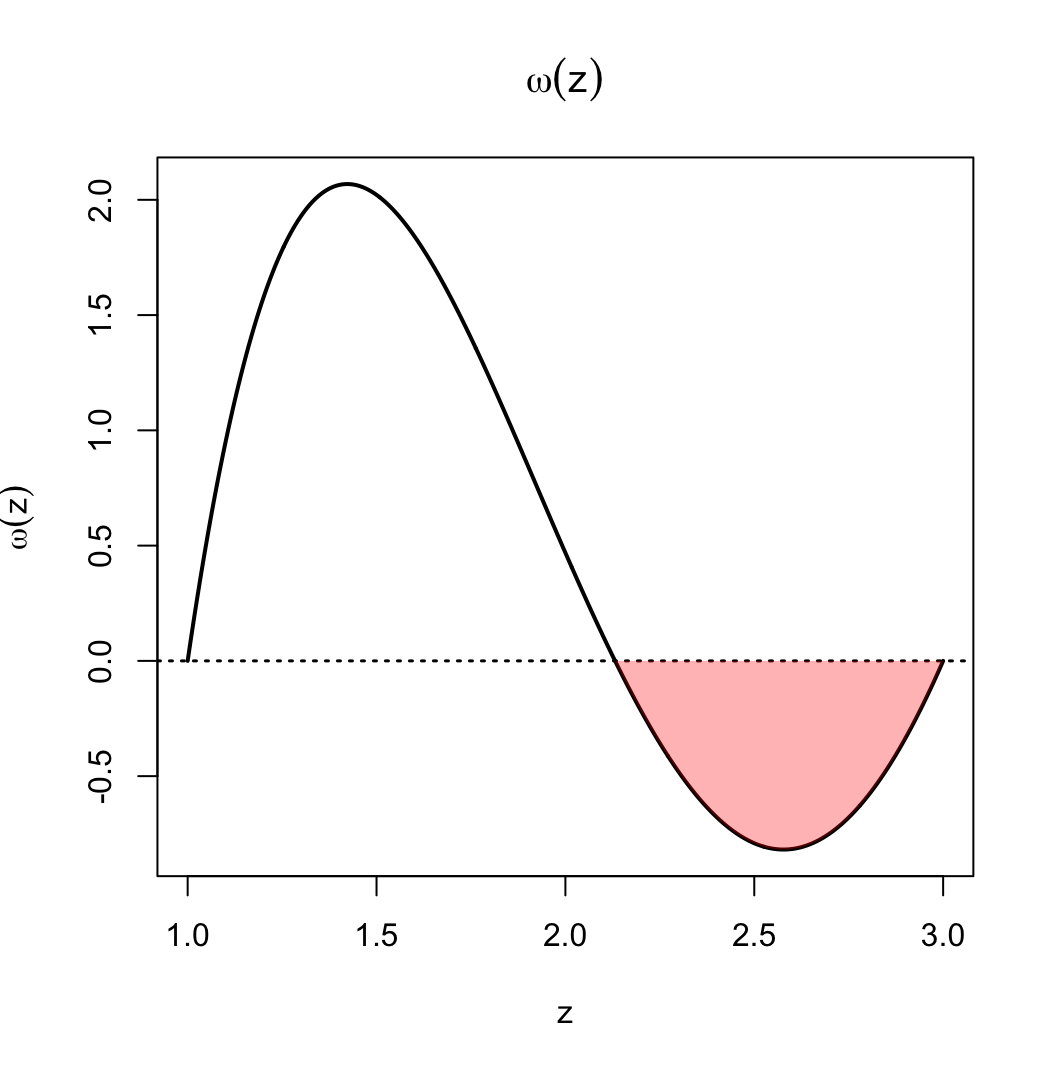

A core theoretical insight is provided through an explicit demonstration that, when the true state-dependent impulse response gh(z) is nonlinear, the coefficient on the interaction term in a linear state-dependent LP is not interpretable either as a local or global average effect. Instead, it is a possibly non-convex weighted average of the derivative gh′(z), with weights that may be negative in some regions, depending on the joint distribution of the shock and the state (see the explicit calculations and visualization below).

Figure 2: True nonlinear function gh(z) and its derivative gh′, illustrating non-monotone and non-convex state dependence.

Figure 4: Weight function gh(Zi,t−1)0 used in linear projection; the presence of negative weights invalidates straightforward causal interpretation.

This result is stark: empirically estimated linear interaction coefficients can be near zero or even assume the opposite sign of the marginal effect in large portions of the state space. Thus, conditioning on the state requires robust, nonparametric modeling for valid heterogeneity inference.

Nonparametric Sieve Estimation Framework

To address this, the authors develop a sieve-based nonparametric LP estimator that recovers the functional causal object gh(Zi,t−1)1 directly under the sufficient condition. The structure of the estimator leverages the exogeneity of the aggregate shock (martingale difference sequence), allowing for direct identification and efficient estimation. The practical implementation combines cubic B-spline expansions for the state response function with standard OLS infrastructure and data-driven basis selection (AIC, GCV, LASSO).

The estimator admits both pointwise and uniform inference, accommodating the feature that in applied work, a principal inferential object is often the global shape of the impulse response function rather than a single pre-specified value. The theoretical contributions include uniform consistency and Gaussian approximation rates suitable for high-dimensional panels and time series.

Monte Carlo Evidence and Empirical Illustration

Extensive simulation studies show that the sieve estimator delivers substantial gains in recovering the true state-dependent impulse response—especially when the true gh(Zi,t−1)2 is nonlinear. The root integrated mean squared error (RIMSE) for the sieve estimator remains an order of magnitude smaller than for linear LPs at short horizons, and the difference remains substantial even as the horizon increases and the response function becomes more linear.

Application: Monetary Policy and Heterogeneous Firm Investment

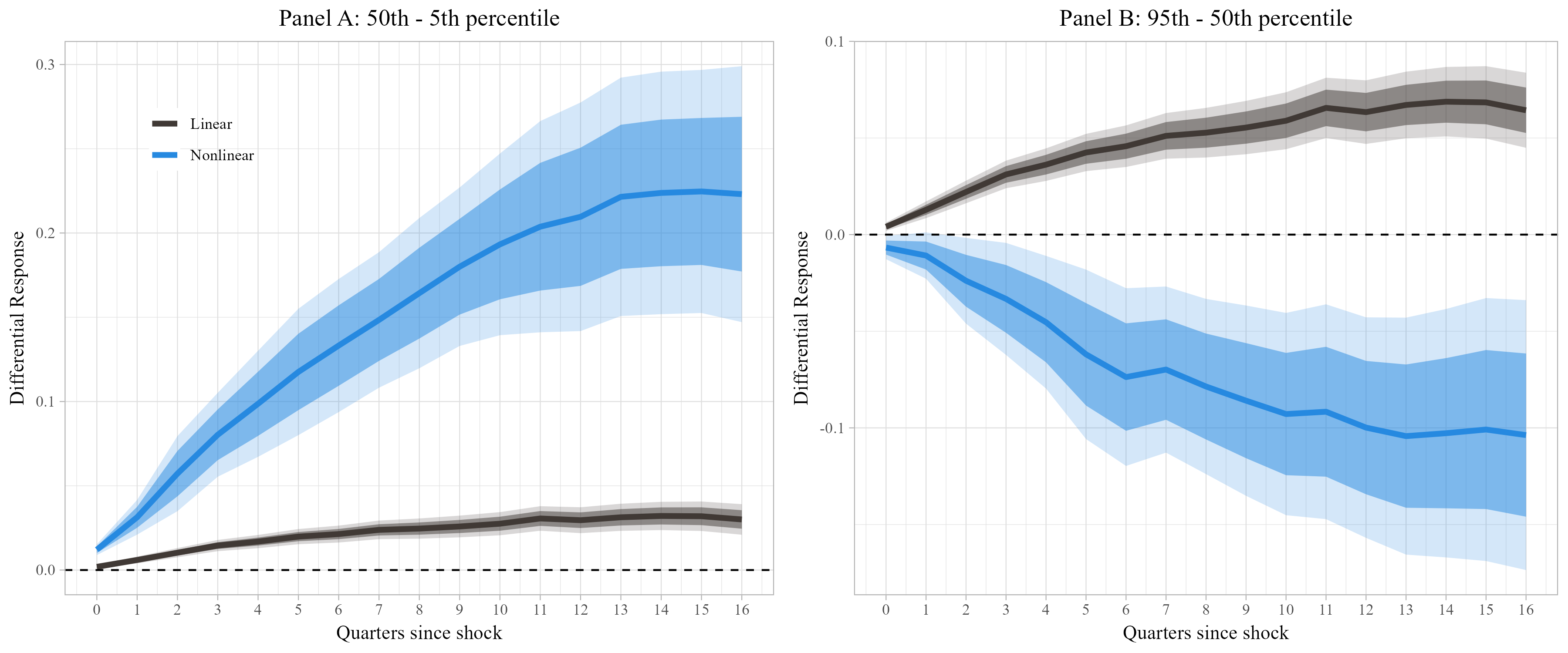

An empirical application to the effect of monetary policy shocks on firm investment, conditioning on heterogeneity in financial vulnerability (distance to default), illustrates the substantive consequences of imposing functional form misspecification. When using linear state dependence, the inference suggests a monotonic increase in responsiveness with financial soundness. The nonparametric approach, by contrast, uncovers a non-monotonic, hump-shaped relationship, with the strongest response concentrated near the center of the financial health distribution, not in the right tail.

Figure 5: Differential investment responses across quantiles of financial conditions: the nonlinear LP reveals pronounced non-monotonicity overlooked by the linear LP.

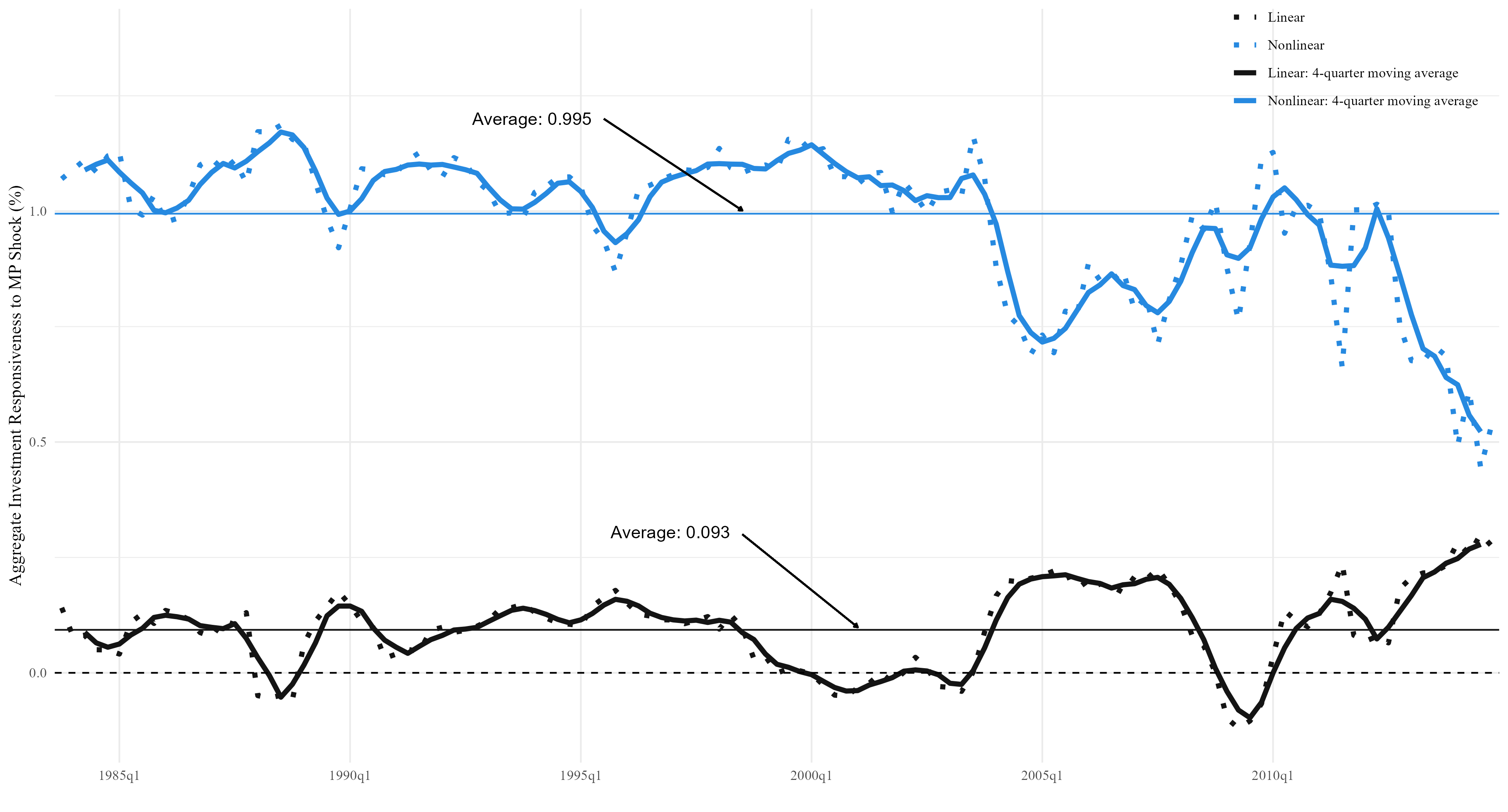

This pattern is materially consequential for aggregation: the linear specification substantially underpredicts the overall effect of monetary policy on aggregate investment, particularly during periods when the mass of firms accumulate near the regions of maximal nonlinearity.

Figure 6: Aggregate investment response as predicted by linear vs nonlinear local projections, highlighting significant bias in standard linear approaches.

Broader Implications and Future Directions

The distinction between scalar LPs (which yield convex-average causal estimates even under misspecification) and state-dependent LPs (which require a correct model for heterogeneity) points to a general lesson for empirical causal inference: modeling heterogeneity is a much more demanding exercise, and nonparametric approaches should be a default unless strong theory justifies linearity in state dependence. The identification result also explains the empirical literature's success in panel micro–macro contexts—where the required conditional mean restriction is theoretically satisfactory—while circumscribing the validity of similar methods in purely aggregate settings or in the presence of global nonlinear dynamics.

On the econometric front, this framework can be extended to more complex dependence structures, joint state–shock nonlinearities, or to settings where the state is only imperfectly observed or endogenous. The nonparametric LP paradigm also naturally aligns with recent advances in machine learning applied to structural econometric modeling, including random forest and deep learning approaches to heterogeneous treatment effects, with the caveat that causal identification still requires attention to DGP structure.

Conclusion

This paper clarifies the foundational conditions for causal inference using state-dependent LPs and demonstrates both the pitfalls of linear state dependence and the necessity and feasibility of nonparametric approaches. Its methodological contributions—rigorous identification arguments, nonparametric estimation and inference tools, and clear empirical illustrations—set improved standards for heterogeneous impulse response estimation in applied macroeconomics and panel econometrics. The implications are both practical, for the analysis of policy transmission via micro heterogeneity, and theoretical, in highlighting the boundaries of credible causal inference in dynamic panel and time series models.