End-to-End PDE-Based Quantum Algorithms for Multi-Asset Option Pricing under Local and Stochastic Volatility

Published 26 May 2026 in quant-ph and q-fin.CP | (2605.26610v1)

Abstract: Multi-asset option pricing under local- and stochastic-volatility models leads naturally to high-dimensional parabolic PDEs. We develop an end-to-end quantum PDE framework for European option pricing under local-volatility Black--Scholes and Heston models. The framework takes classical contract and model data as input and returns classical estimates of selected option values. We solve the pricing PDEs after finite-difference discretization on spatial grids. For $N=2n$ grid points per spatial direction and $d$ assets, the end-to-end gate complexity for single-point recovery, counted in elementary CNOT gates and one-qubit Pauli-axis rotations, has leading grid-size dependence $\widetilde{O}(d2 N{2+d/2})$ for local-volatility Black--Scholes and $\widetilde{O}(d2 N{d+2})$ for Heston. Relative to grid-based finite-difference baselines, these scalings correspond to polynomial improvement factors $N{d/2}$ and $Nd$, respectively. These estimates translate to Clifford+T resources via standard compilation. We complement the complexity analysis with numerical benchmarks against standard classical methods. In the Heston setting, the framework recovers option prices across strikes together with the associated implied-volatility smile/skew. Overall, this work provides a complete end-to-end quantum pricing pipeline with explicit resource accounting and theoretical performance guarantees.

The paper develops an end-to-end quantum algorithm pipeline that discretizes high-dimensional PDEs and employs Schrödingerisation for pricing European options.

It achieves a polynomial speedup over classical finite-difference methods while accurately recovering market-relevant implied volatility smiles for both Black–Scholes and Heston models.

Resource estimates, explicit circuit formulations, and rigorous numerical validations demonstrate the framework's practical potential in mitigating the curse of dimensionality in quantum finance.

End-to-End Quantum Algorithms for Multi-Asset Option Pricing under Local and Stochastic Volatility

Overview

The paper "End-to-End PDE-Based Quantum Algorithms for Multi-Asset Option Pricing under Local and Stochastic Volatility" (2605.26610) develops a comprehensive quantum algorithmic pipeline for pricing European-style options using parabolic PDEs in both multi-asset Black–Scholes (local volatility) and Heston (stochastic volatility) models. The proposed quantum framework discretizes high-dimensional PDEs on spatial grids, prepares payoff and ancillary states, evolves pricing dynamics via unitarized ODE embedding (Schrödingerisation), and retrieves classical estimates of option prices with explicit gate complexity analysis. The framework achieves polynomial quantum speedup relative to classical finite-difference baselines, with rigorous resource estimates and numerical validation—including accurate recovery of market-relevant implied-volatility smiles from quantum-computed prices.

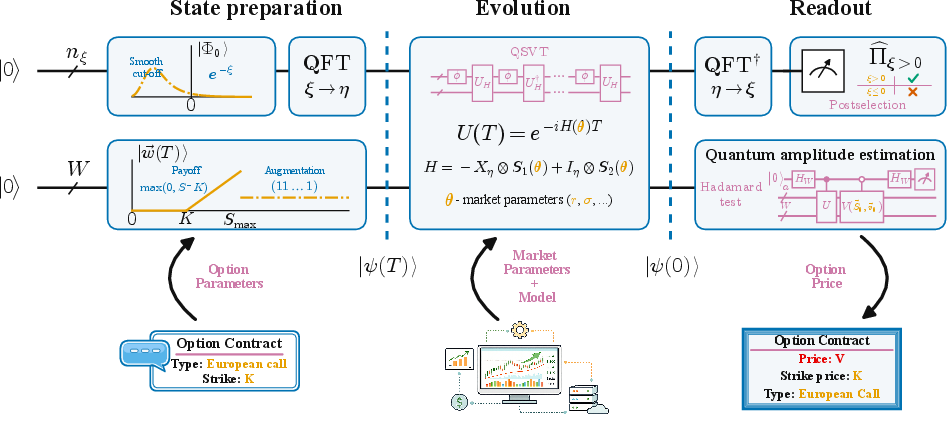

Quantum PDE Pricing Pipeline

The algorithm consists of three principal stages: state preparation, quantum evolution, and classical readout.

State Preparation: Payoff functions (e.g., vanilla, basket, worst-of) and smooth auxiliary cut-off states are encoded as quantum states via block-encoding and quantum singular value transformation (QSVT), using polynomial or piecewise polynomial approximations for efficient circuit implementation. Specialized routines ensure compatibility with the boundary conditions necessary for PDE-based pricing.

Quantum Evolution via Schrödingerisation: The spatially discretized pricing PDE yields a high-dimensional sparse ODE (V˙(t)=AV(t)+b), which is embedded into a larger Hilbert space enabling unitary quantum evolution. Schrödingerisation transforms non-conservative dynamics to unitary form by introducing an auxiliary register. Hamiltonian simulation is achieved via block-encoding of the finite-difference operator, supporting structured boundary conditions (Dirichlet, Neumann, Robin) and leveraging QSVT for efficient evolution.

Figure 1: Quantum workflow for solving the Black–Scholes and Heston PDEs, illustrating amplitude encoding, auxiliary registers for Schrödingerisation, state preparation, evolution via Hamiltonian simulation, and projective readout.

Readout and Amplitude Estimation: The normalized PDE solution—option values at each grid point—is stored as amplitudes of the final quantum state. Single-point price retrieval is accomplished via quantum amplitude estimation, with success probability boosted through oblivious amplitude amplification. Overall normalization is propagated and corrected via auxiliary postselection and analytic integration over payoff functions.

Model Coverage and Numerical Validation

Local Volatility Black–Scholes

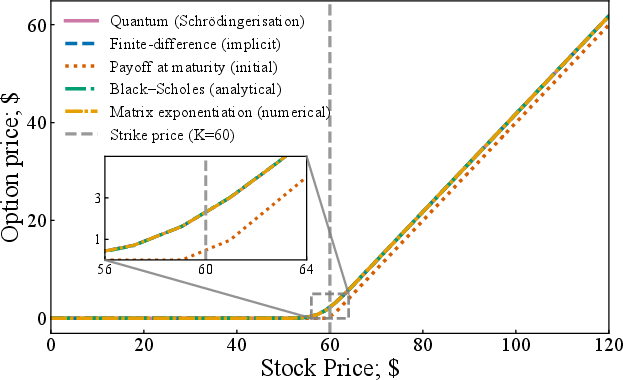

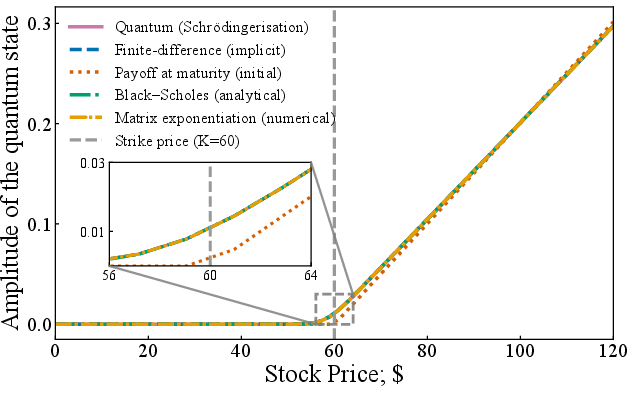

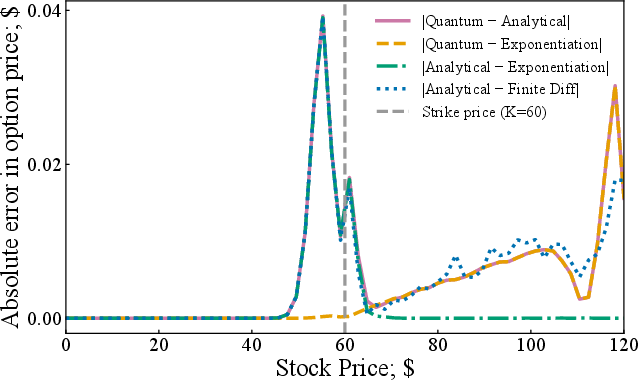

The classic Black–Scholes PDE is generalized to multi-asset settings with spot-dependent local volatility and asset correlation, resulting in high-dimensional, sparse PDEs with severe curse-of-dimensionality (Nd grid scaling). Payoffs compatible with efficient quantum boundary treatments (notably worst-of) are constructed to avoid reduced-dimension boundary closures. Analytical and numerical benchmarks support pipeline validation.

Figure 2: Solver comparison for 1D Black–Scholes: quantum, finite-difference, matrix exponentiation, and analytical benchmarks, showing convergence and error sources in amplitude encoding.

Stochastic Volatility Heston

PDE-based pricing under the Heston model involves an additional variance dimension per asset and mixed derivatives arising from spot–variance correlation. Boundary conditions (e.g., homogeneous Neumann for volatility) are handled within the Schrödingerisation and block-encoding framework. The pipeline recovers full smile/skew effects in implied volatility, matching classical and semi-analytical references.

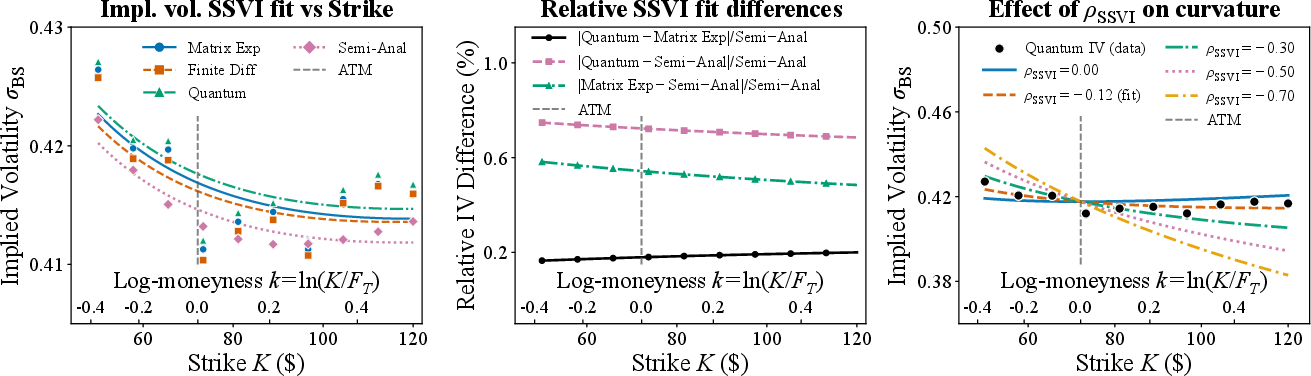

Figure 3: Fixed-maturity Heston implied-volatility smile in log-moneyness coordinates; quantum solver results compared to classical and semi-analytical benchmarks, with sensitivity analysis to SSVI skew parameter.

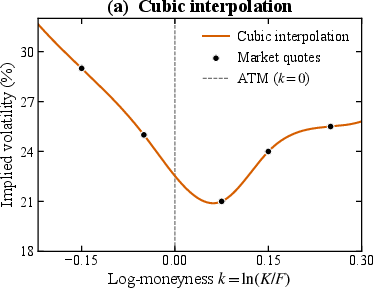

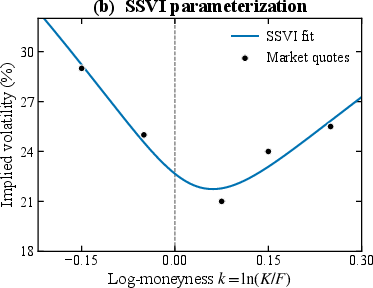

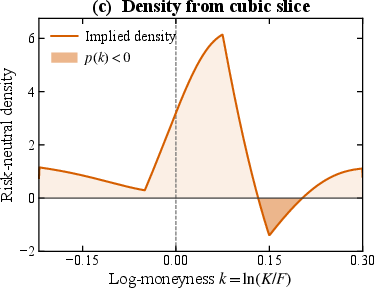

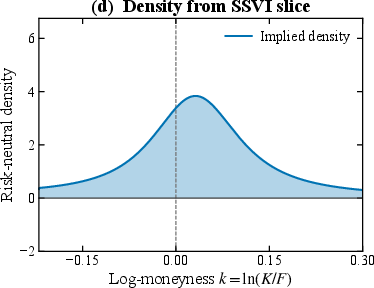

Arbitrage-free SSVI regularization is used for interpolating sparse strike slices and diagnosing butterfly arbitrage (negative implied densities). Quantum-computed prices exhibit no static arbitrage and produce realistic implied-volatility smiles.

Figure 4: Arbitrage-free regularization of implied volatility slices and implied density extraction: cubic interpolation vs. SSVI fits; quantum and classical outputs compared under financial constraints.

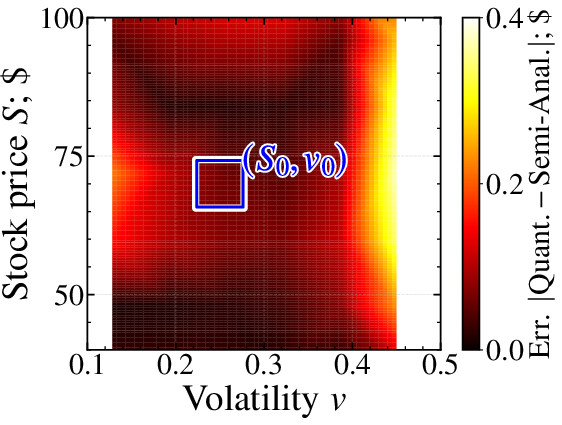

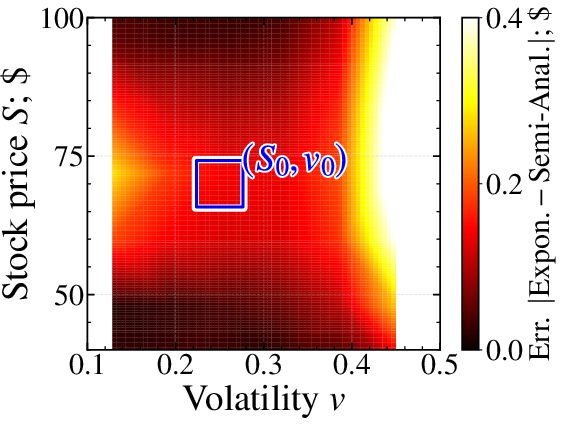

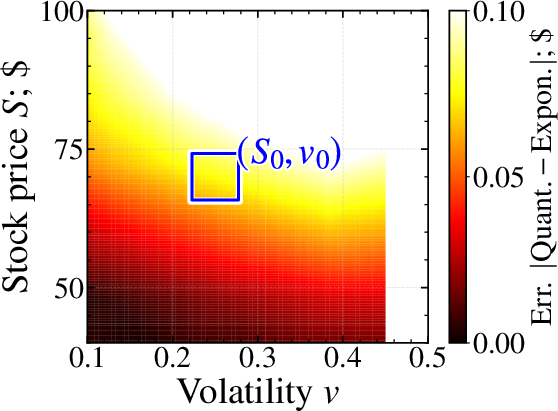

Absolute error analysis for quantum and classical Heston PDE solvers demonstrates discretization and auxiliary register effects, with errors well-controlled in regions of financial interest.

Figure 5: Absolute-error heat maps for quantum, matrix exponentiation, and semi-analytical Heston PDE solutions across (S,v) grid; quantum solution errors dominated by spatial truncation.

Complexity Analysis and Quantum Advantage

Explicit gate complexity estimates are provided for both Black–Scholes and Heston pipelines:

Multi-Asset Black–Scholes: For N=2n grid points per spatial axis and d assets, the end-to-end gate complexity for single-point retrieval is O(d2N2+d/2), reflecting an improvement factor Nd/2 relative to classical methods.

Multi-Asset Heston: For d assets (with $2d$ dimensions), the corresponding complexity is O(d2Nd+2), yielding Nd0 speedup in grid size.

These scalings are polynomial in Nd1 and exponential in the number of assets Nd2, mitigating but not completely eliminating the curse of dimensionality. Quantum advantage becomes more pronounced as the dimensionality increases (>2 assets), particularly in practical settings where classical methods are infeasible due to state space explosion.

Technical Contributions and Implications

Explicit Circuits and Resource Estimation: The paper provides rigorous gate-counts in terms of CNOTs and single-qubit rotations (Clifford+Nd3 translation covered), accounting for state preparation, Hamiltonian simulation, normalization recovery, and amplitude estimation. All circuit components adapt to the structure of the underlying PDE and boundary conditions.

Algorithmic Generality: The pipeline is sufficiently general to accommodate multi-asset, correlated local volatility, and fully stochastic volatility models under parabolic PDEs, provided payoffs and boundaries are compatible. Early-exercise and path-dependent contract extensions require augmented state spaces and are left to future work.

Numerical Consistency: Quantum-computed prices match classical and analytical baselines in benchmark regimes; the framework robustly recovers market-relevant implied-volatility surfaces, supporting practical applicability in financial engineering.

Future Directions

The main bottleneck remains the single-amplitude readout, whose complexity scales as Nd4 or Nd5 for Black–Scholes and Heston, respectively. More favorable extraction mechanisms are plausible (e.g., forward Kolmogorov formulations or expected-payoff estimation) and constitute ongoing research. Extension to path-dependent contracts and early exercise (American options) will require iterative or variational quantum PDE solvers, potentially benefiting from advances in quantum Monte Carlo and hybrid quantum-classical approaches.

Conclusion

This work establishes a technically rigorous end-to-end quantum pipeline for high-dimensional PDE-based option pricing under both local and stochastic volatility. The framework achieves polynomial quantum speedups in grid size and explicit financial validation, supporting its potential for scalable quantum finance applications as quantum hardware matures. Further development will focus on broadening contract coverage, optimizing readout, and integrating quantum advantage with practical market workflows.