Analytic approximation for Bachelier option prices and applications

Published 3 May 2026 in q-fin.CP | (2605.02040v1)

Abstract: It is well-known that, in the Bachelier model, when asset prices and volatilities are uncorrelated, the implied volatility coincides with the fair value of the volatility swap. In this paper, via classical Itô calculus and Taylor expansions, we write the price for out-of-the-money (OTM) and in-the-money (ITM) options as an expansion with respect to the moneyness, where the coefficients are related to the negative (non-integer) powers of the future mean volatility. As an a application, we use it as a control variate to reduce the variance of Monte Carlo option prices in the correlated case.

The paper introduces an exact analytic expansion for European option prices in the Bachelier model using Itô calculus and Taylor series.

The paper demonstrates high accuracy in pricing and implied volatility estimation compared to Monte Carlo methods under Heston and SABR frameworks.

The paper shows that the analytic expansion allows closed-form computation of Greeks and serves as an effective variance-reducing control variate.

Analytic Expansions of Bachelier Option Prices: Methodology and Applications

Introduction

This paper proposes a fully analytic expansion for European option prices within the Bachelier model, focusing on the uncorrelated case between asset prices and stochastic volatility. Developing closed-form approximations for both option prices and implied volatilities under the Bachelier framework is nontrivial, especially when volatility is itself stochastic and potentially rough. The authors leverage Itô calculus and Taylor expansions to express option prices as a series with coefficients involving negative (non-integer) powers of the future mean volatility. Beyond theoretical derivation, the analytic formula is shown to be highly effective both for accurate price/implied volatility computation and as a variance-reducing control variate for Monte Carlo methods under correlation.

Analytic Expansion of Bachelier Option Prices

Within the uncorrelated Bachelier model, the paper derives the following key expansion: the European call price V can be written as a power series in moneyness centered around the at-the-money level. The leading term is the Bachelier price calculated with the volatility swap, and higher-order corrections involve negative moments of the forward variance process. The formula provides an exact analytic representation, as opposed to traditional approaches relying on small-parameter asymptotics.

where Bac denotes the Bachelier price function, v^ the volatility swap, MT the realized average variance, and M0 the initial value of its conditional expectation. Notably, the expansion is exact and does not rely on the smallness of moneyness or time to maturity.

Practical Performance: Numerical Evaluation

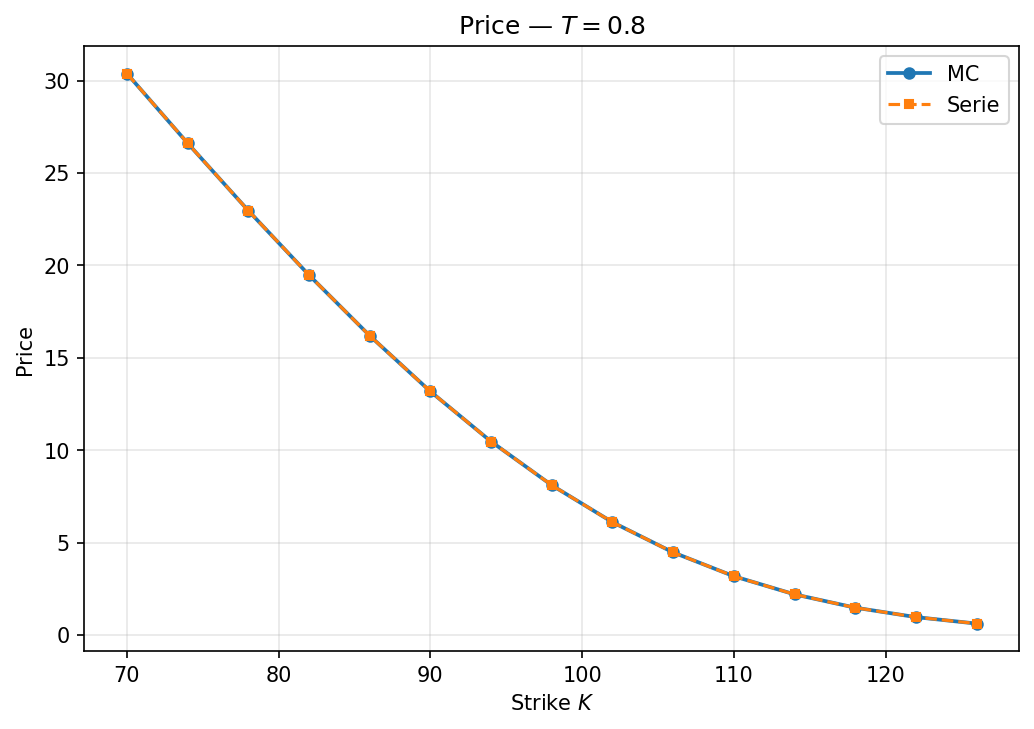

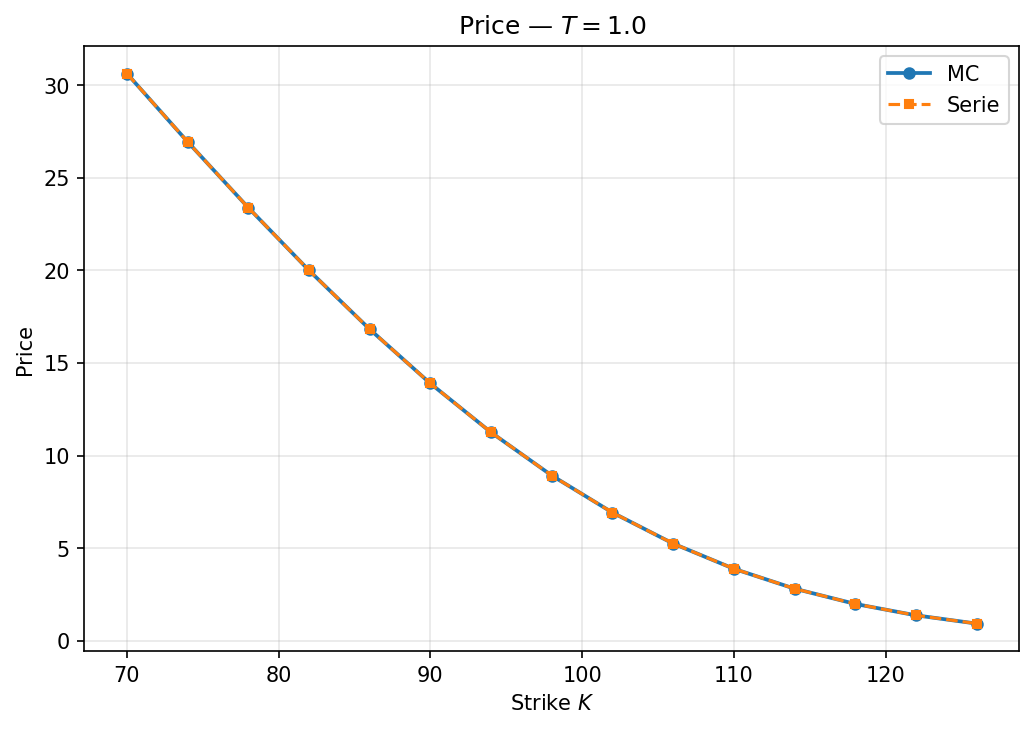

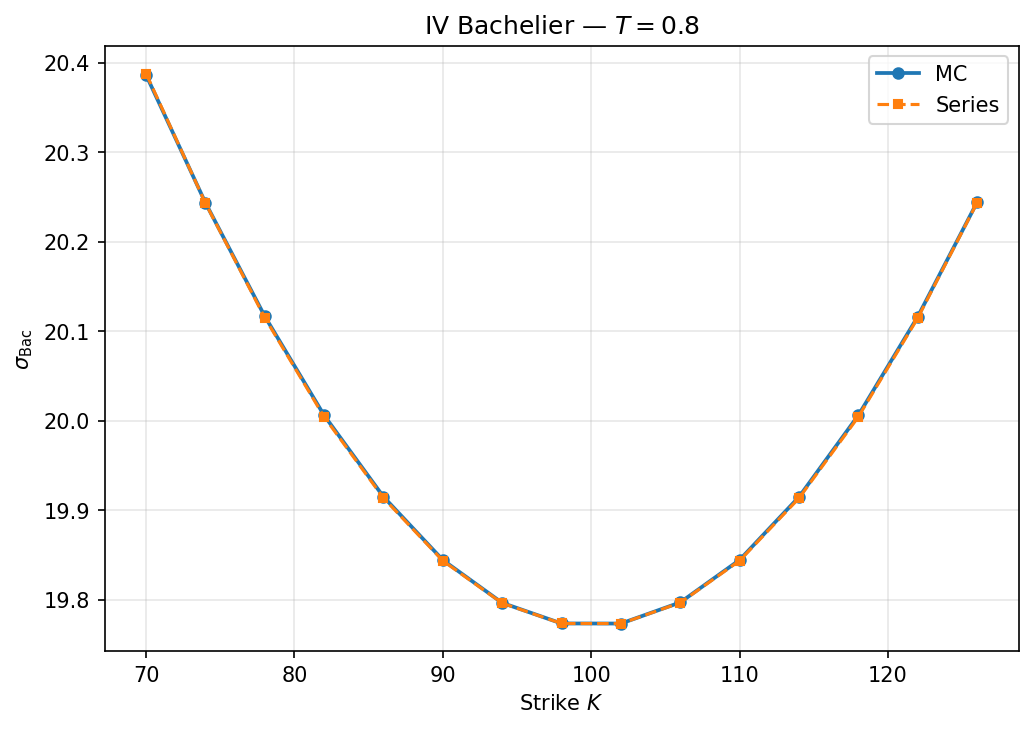

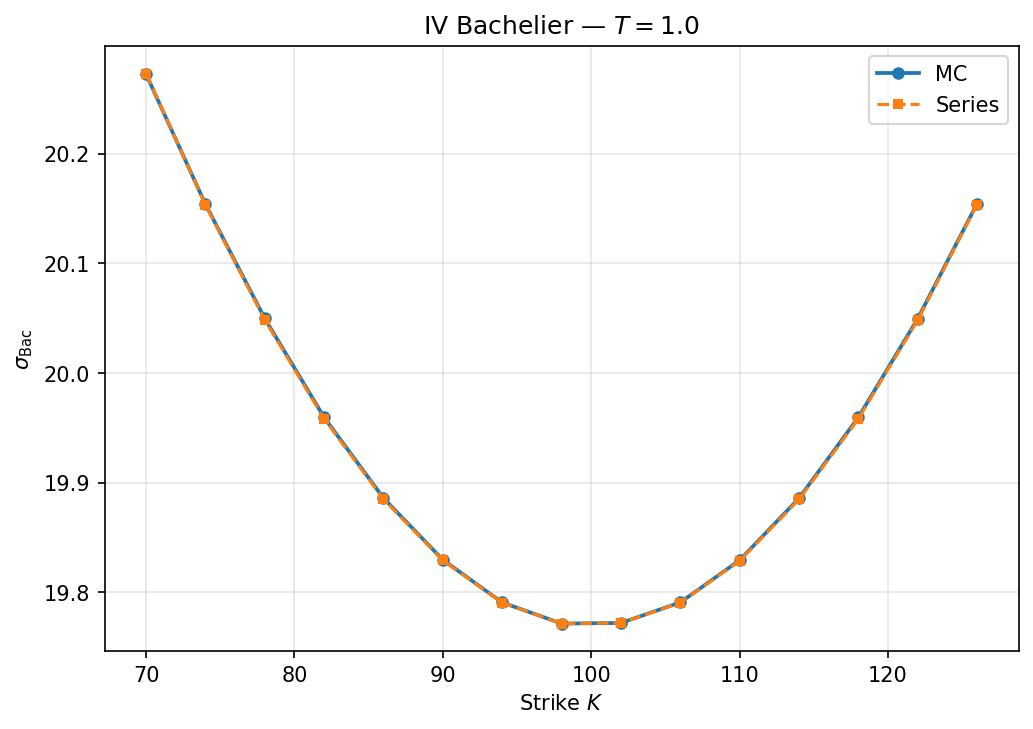

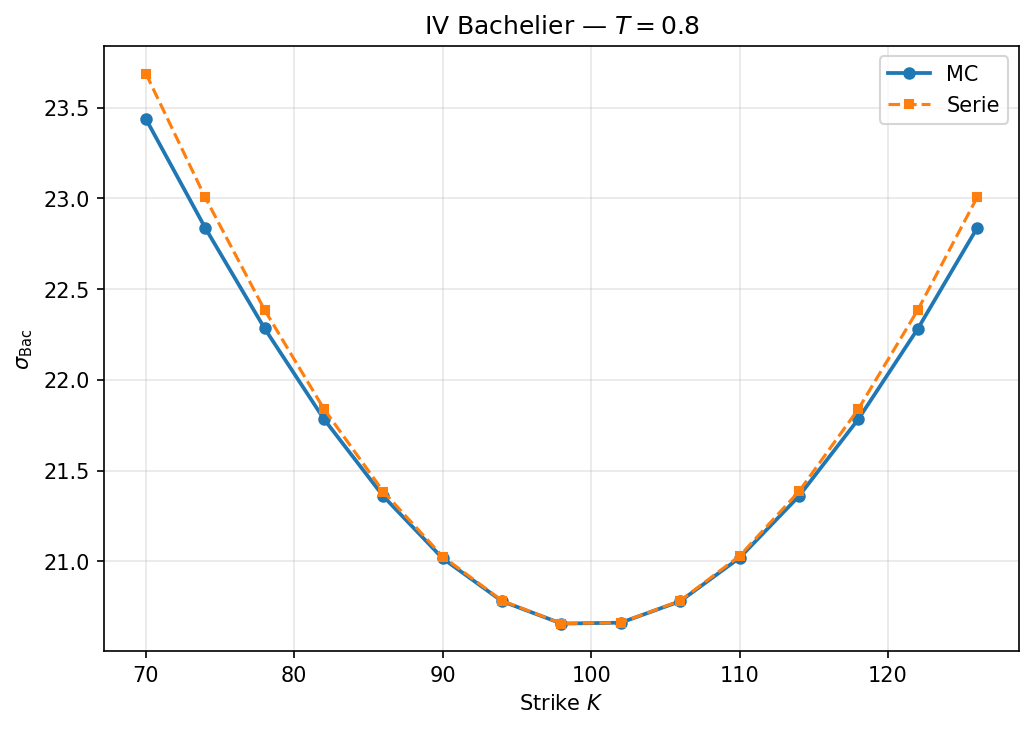

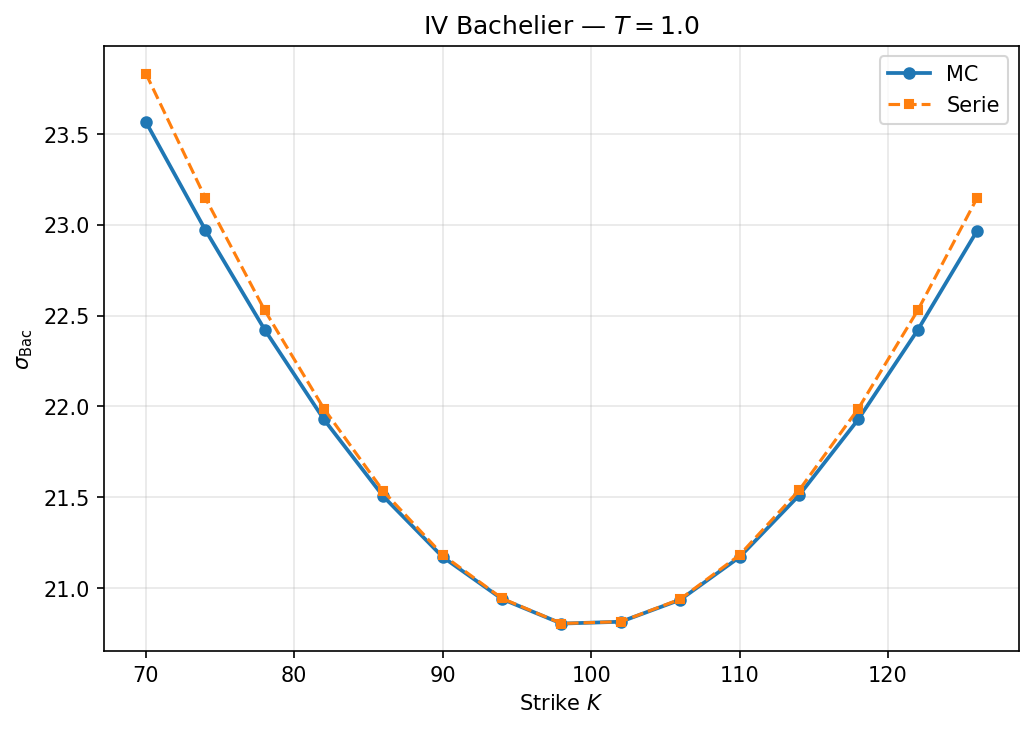

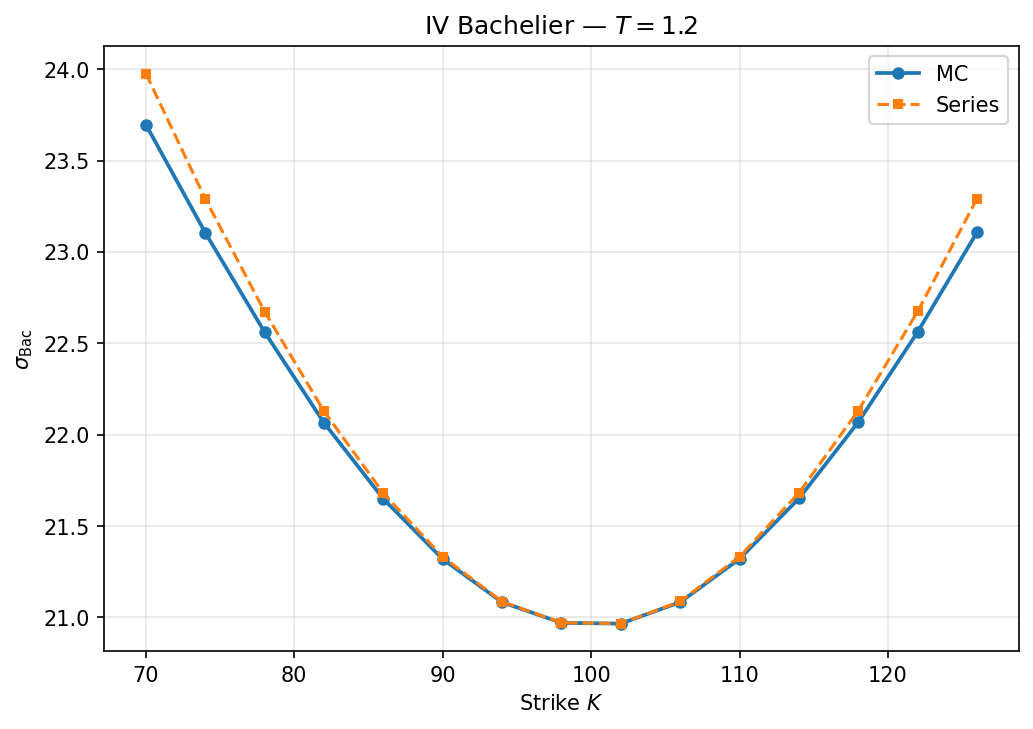

The expansion is benchmarked on two prominent stochastic volatility frameworks: Heston and SABR. The analytic approximation demonstrates high accuracy in option price and implied volatility computation, indistinguishable from Monte Carlo benchmarks when a moderate number of terms (typically under 10) are retained for practical strikes and maturities.

Figure 1: Approximation of option prices for the Heston model demonstrates high accuracy of the analytic expansion relative to Monte Carlo benchmarks.

Figure 2: The implied volatility smile for the Heston model is closely matched by the analytic expansion over a range of maturities.

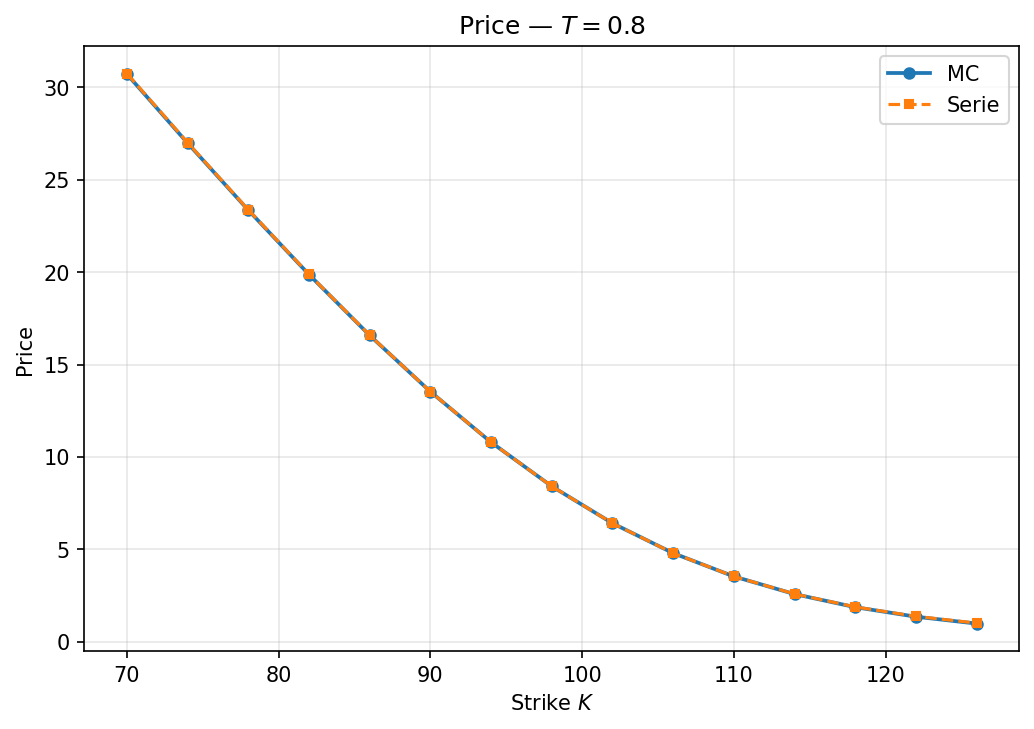

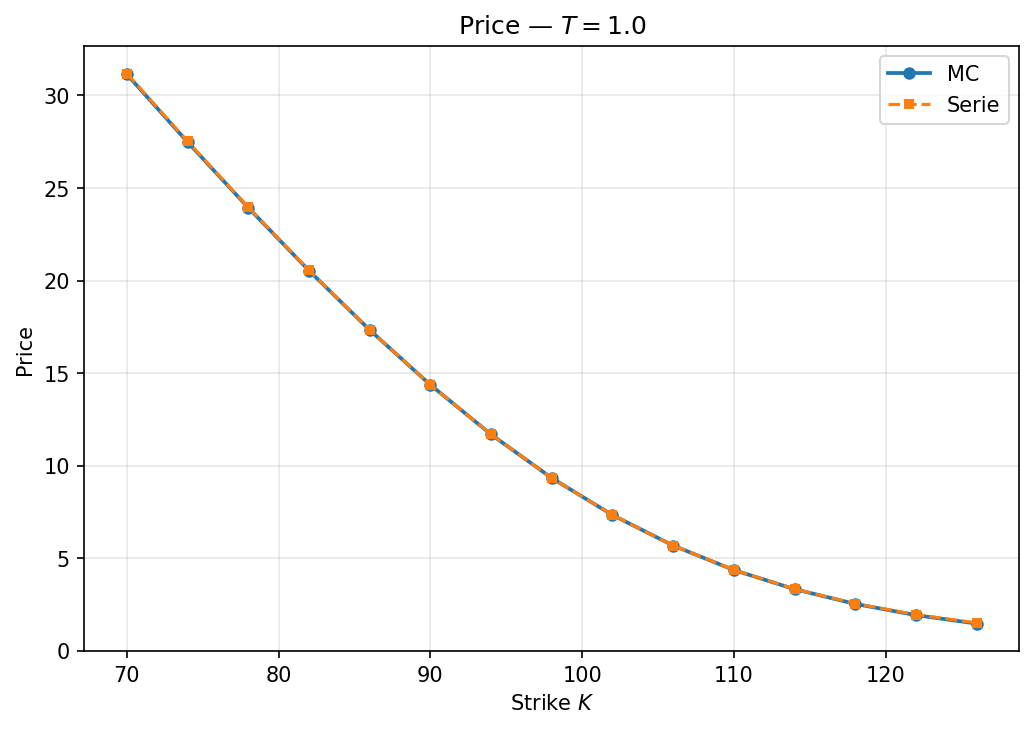

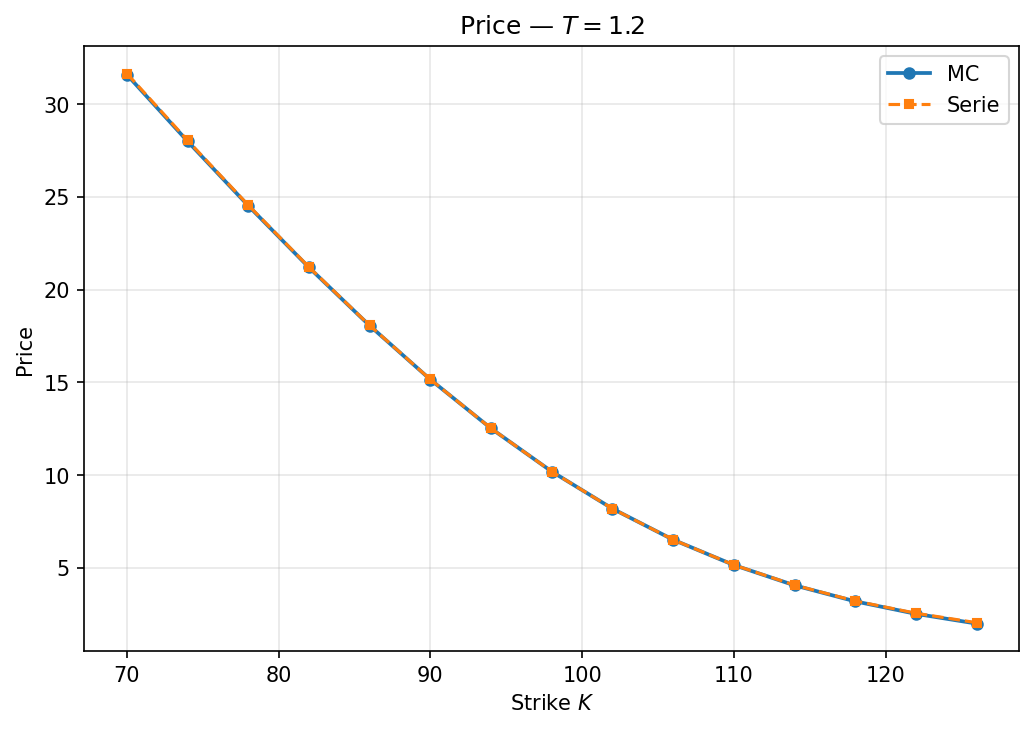

Figure 3: Analytic expansion compared to Monte Carlo shows high-fidelity price approximation under the SABR model.

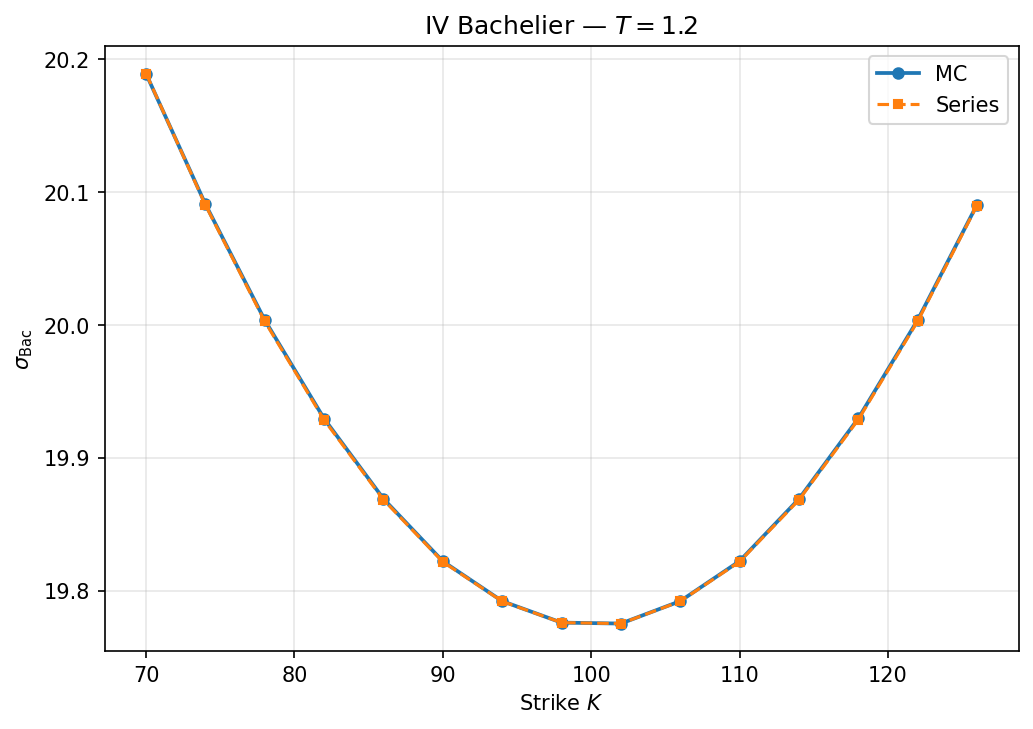

Figure 4: Analytic expansion accurately represents the implied volatility smile in the SABR model, with small errors across a wide moneyness range.

Empirical evaluation demonstrates the number of necessary terms in the expansion varies by strike and maturity but remains modest for high-precision needs, supporting practical use.

Analytic Computation of Greeks

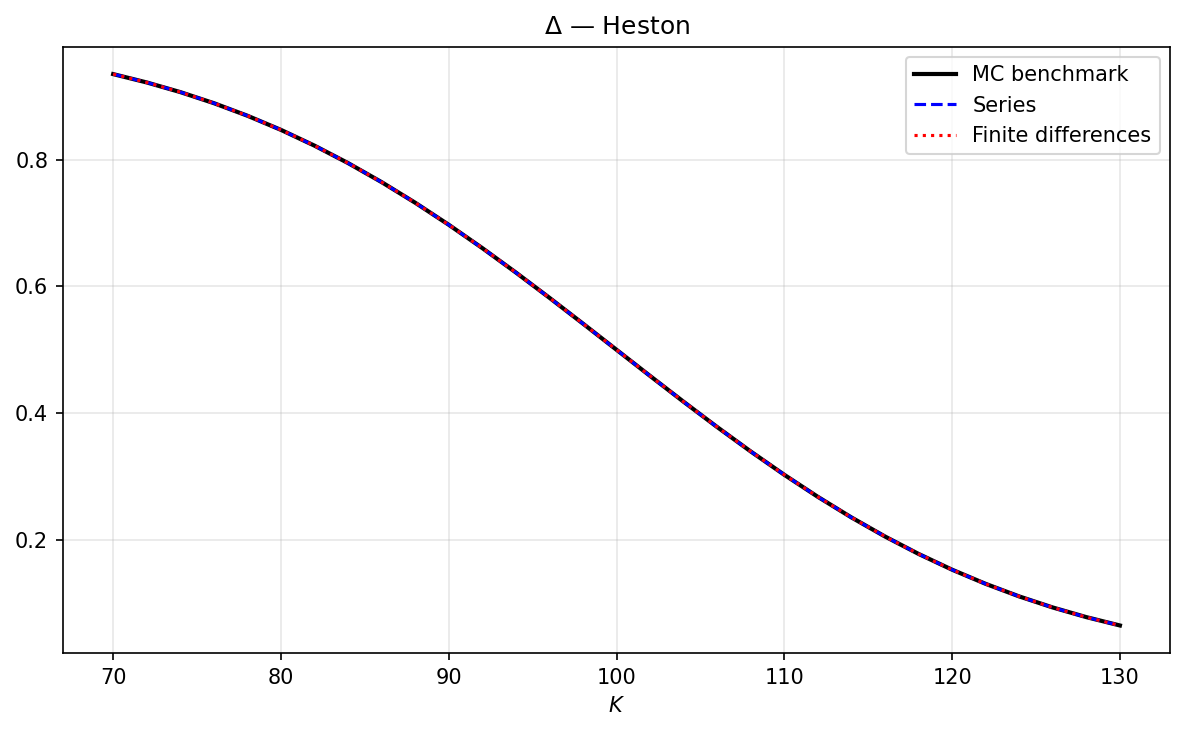

The analytic formula is directly differentiable, enabling closed-form computation of option sensitivities ("Greeks"). The methodology is validated numerically for both Delta and Gamma, with results matching finite difference and conditional Monte Carlo methods, but with significantly lower computation time. This makes the approach particularly attractive for real-time scenario analyses or calibration procedures in markets with non-lognormal underlying dynamics.

Figure 5: Greek Delta computed analytically matches both finite difference and Monte Carlo calculations for the Heston-Bachelier case.

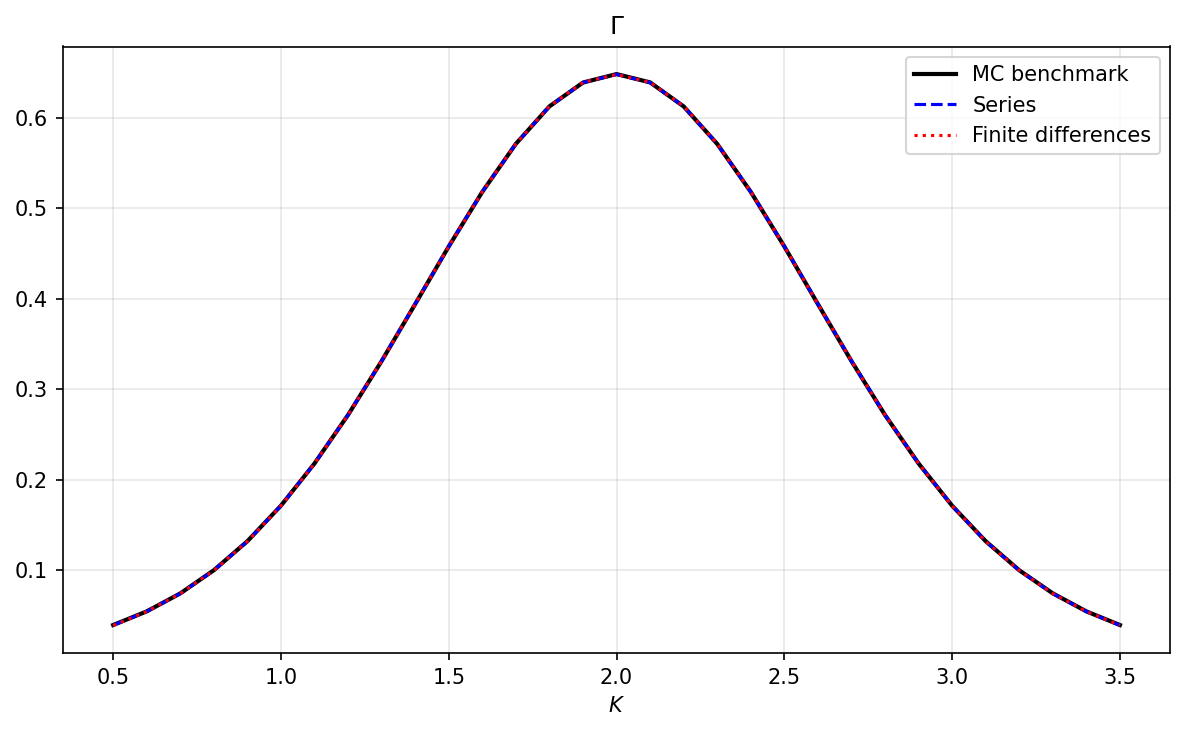

Figure 6: Gamma computed via analytic expansion also matches alternative approaches, with superior computational efficiency.

Control Variate Applications in Monte Carlo Simulation

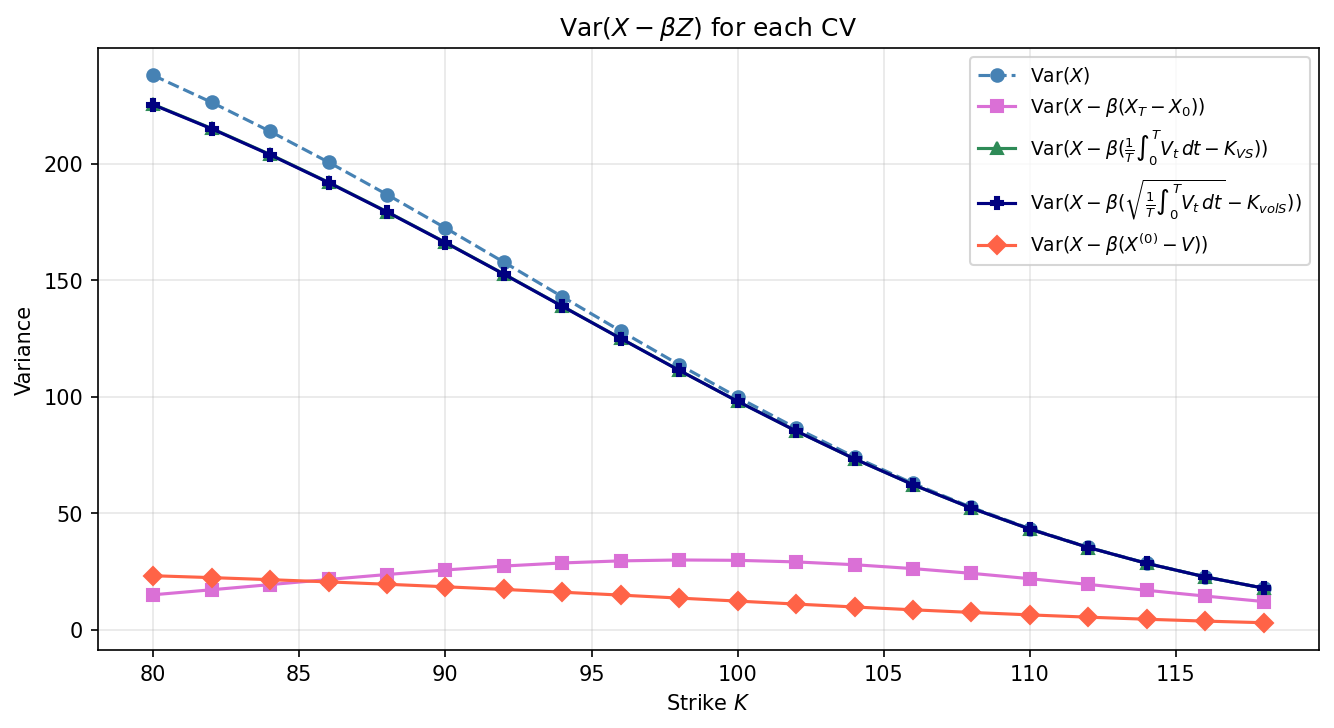

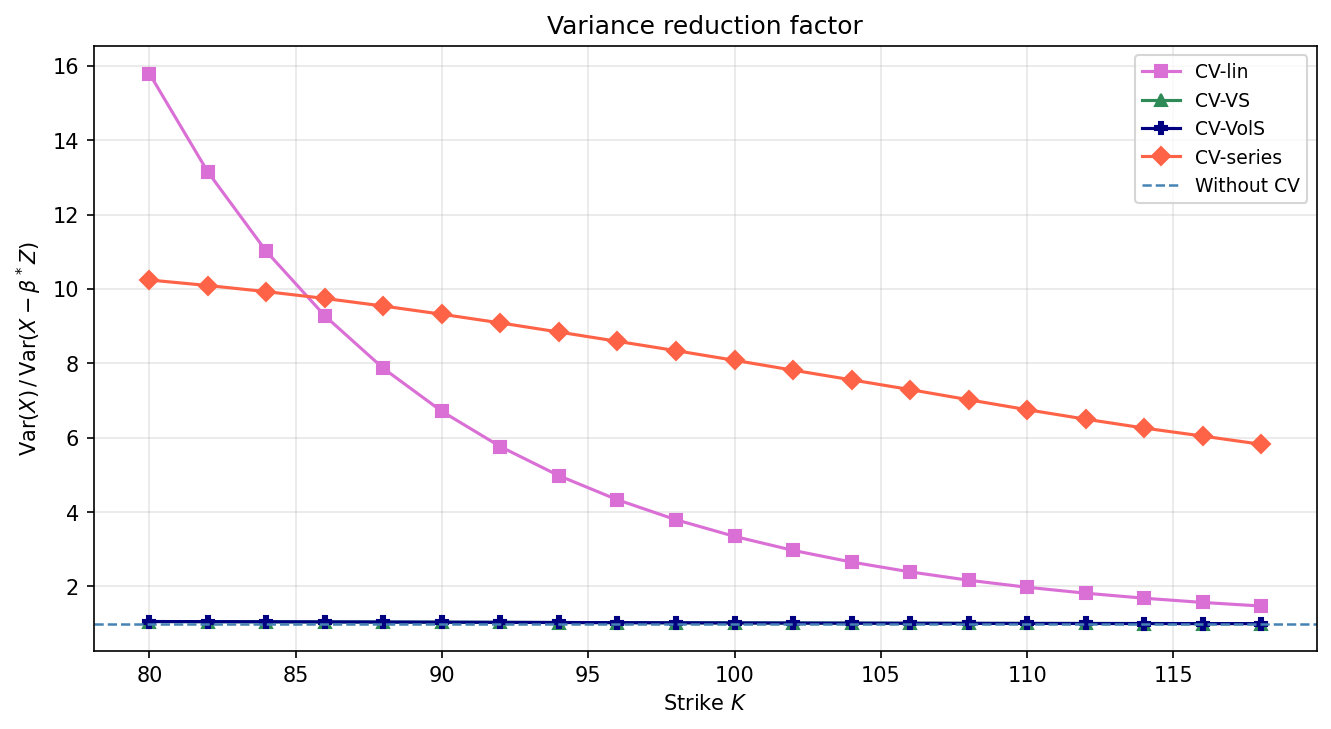

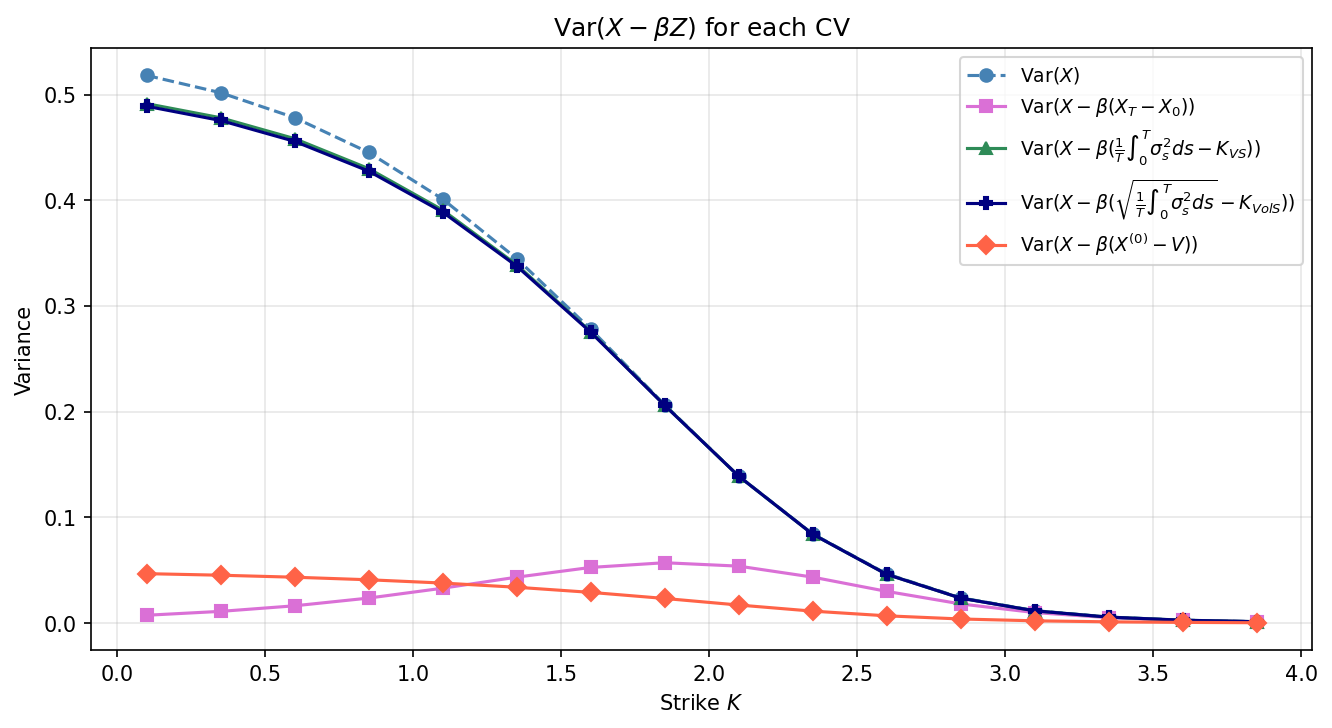

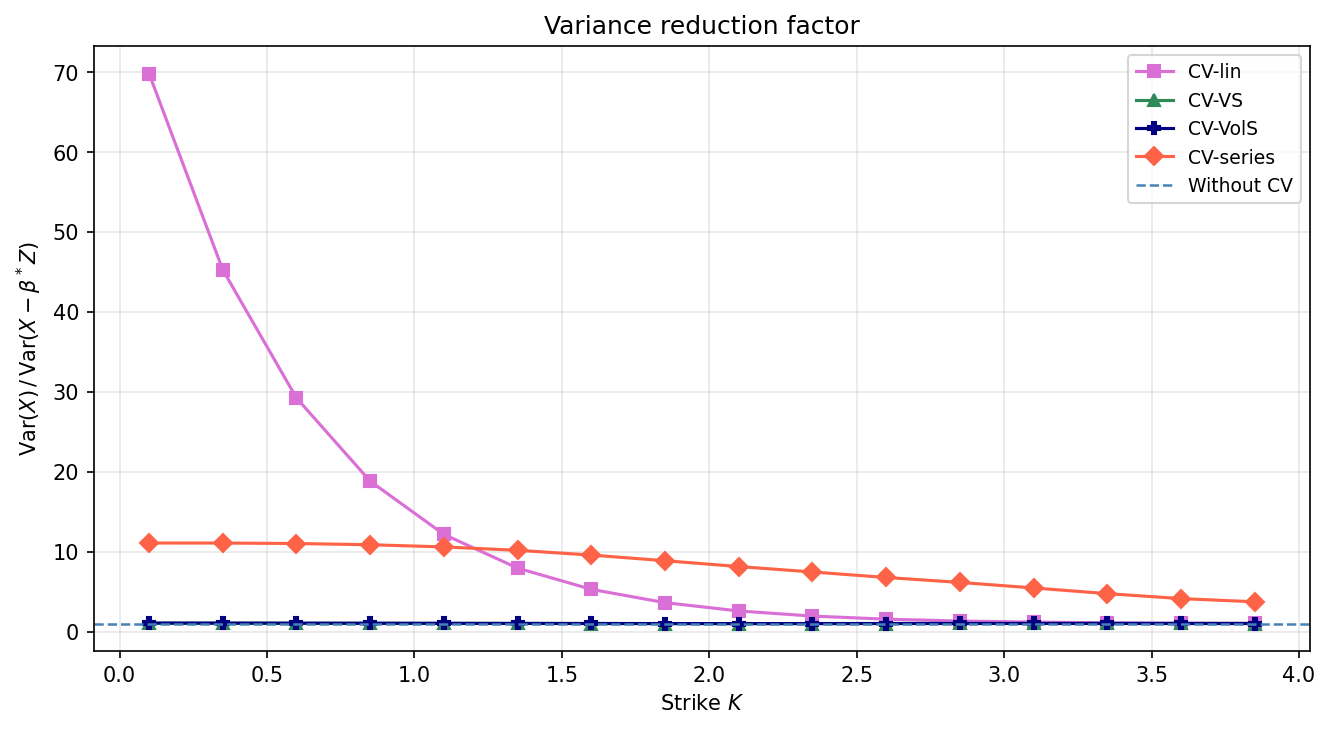

The analytic expansion is deployed as a control variate to efficiently reduce variance in Monte Carlo simulations for option pricing, particularly valuable when correlation is present (i.e., departures from pure Bachelier dynamics). Comparison with standard control variates (linear, variance swap, volatility swap) demonstrates that the analytic expansion-based control variate achieves greater variance reduction, especially in out-of-the-money regimes. The optimality is less pronounced near at-the-money for large correlations, and deep in-the-money where linear control variates dominate due to the payoff structure.

Figure 7: Variance and reduction factor for various control variates in the Heston-Bachelier correlated scenario (model I); the analytic expansion control variate is most effective for OTM options.

Figure 8: Control variate performance for the SABR model (model II) confirms the expansion-based control is superior except for deep ITM payoffs.

Figure 9: In the SABR-IR scenario (model III), the analytic series retains superior variance reduction for most strikes aside from deep ITM cases.

Theoretical and Practical Implications

Theoretically, the expansion links pricing corrections to explicit negative moments of the realized variance, making the impact of stochastic volatility (and its higher moments) transparent. The approach generalizes previous asymptotics, applying to all strikes and maturities, and is robust under models where volatility is non-Markovian or rough.

Practically, the analytic expansion enables fast and accurate determination of prices and Greeks, facilitates efficient calibration (due to closed-form sensitivities), and accelerates simulation-based pricing under correlated dynamics via superior variance reduction.

Furthermore, the approach outlines how analytical corrections extend to the computation of implied volatilities, providing systematic expansions beyond at-the-money regimes.

Future directions include extending the expansion to cases with strong asset-volatility correlation, and investigating its application to barrier and path-dependent options in the Bachelier setting. Additionally, leveraging the expansion in deep learning surrogates for option price maps could yield further computational gains in large-scale calibration or scenario analysis pipelines.

Conclusion

The paper presents a rigorous analytic expansion for Bachelier option prices under stochastic volatility, yielding both theoretical insight and practical computational tools. Numerical results confirm high accuracy for prices and Greeks and demonstrate a significant improvement in Monte Carlo variance reduction when the expansion is used as a control variate. The methodology facilitates efficient pricing and risk management in markets where the Bachelier model is relevant, especially in negative rate or commodity settings, and points the way to further extensions for correlated or rough volatility environments.

“Emergent Mind helps me see which AI papers have caught fire online.”

Philip

Creator, AI Explained on YouTube

Sign up for free to explore the frontiers of research

Discover trending papers, chat with arXiv, and track the latest research shaping the future of science and technology.Discover trending papers, chat with arXiv, and more.