- The paper presents two quantum algorithms that price discretely monitored lookback options via imaginary time evolution in the Black-Scholes framework.

- It employs the VarQITE method with hardware-efficient quantum circuits to tackle jump conditions caused by discrete updates of the running maximum.

- Enhanced fidelity through simultaneous evolution in an extended state space outperforms sequential jump handling, despite requiring increased qubit overhead.

Quantum Algorithms for Pricing Discretely Monitored Lookback Options

Overview

The paper "Pricing Lookback Options on a Quantum Computer" (2604.00389) presents a quantum computational approach for pricing discretely monitored lookback options within the Black-Scholes model. The core contribution is the development and analysis of two quantum algorithms employing imaginary time evolution to solve the path-dependent partial differential equations (PDEs) that arise in this context. These PDEs are mapped onto dynamics governed by non-Hermitian Hamiltonians, tackled via the Variational Quantum Imaginary Time Evolution (VarQITE) algorithm. Special attention is given to the algorithmic treatment of jump conditions induced by discrete monitoring of the running maximum—a critical complication absent in vanilla European or Asian option pricing.

The underlying asset follows standard Black-Scholes dynamics:

dSη=Sη(rdη+σdWη)

where r is the risk-free rate, σ is the volatility, and Wη is Brownian motion. The lookback option payoff at maturity T is (YT−ST)+, with Yη being the running maximum of Sη at discrete time points. The pricing challenge arises from the path dependence and discrete updating, leading to PDEs with jump conditions.

Option pricing is reframed as the imaginary-time evolution of a quantum state, which encodes the option value as a function of the current asset price and running maximum, governed by a non-Hermitian Hamiltonian extracted from the Feynman-Kac representation of the Black-Scholes PDE. After Wick rotation, the PDE is recast as Schrödinger-type imaginary time evolution.

Figure 1: Schematic representation of the sequential quantum evolution algorithm, in which continuous and jump Hamiltonians alternate according to the monitoring schedule.

Algorithmic Approaches

Method 1: Sequential Evolution with Jump Hamiltonians

This technique divides the time axis into continuous segments between monitoring dates, evolving the quantum state under a continuous Black-Scholes Hamiltonian H^C, punctuated by application of a dedicated jump Hamiltonian H^J at monitoring epochs to encode the effect of discrete path updates.

- Hamiltonian Construction: r0 is obtained via finite-difference spatial discretization and encodes the standard Black-Scholes PDE for lookback options. r1 incorporates the jump condition by acting on the discretized grid at monitoring times, with special structure to "reset" the running maximum as required.

- Quantum Evolution: The overall process alternates between time-evolution under r2 and abrupt update under r3.

- Implementation: The state is evolved using the VarQITE algorithm, which maps imaginary time evolution into parameter updates of a hardware-efficient quantum circuit.

Figure 2: Sequence of continuous imaginary time evolution steps, each interrupted by a non-unitary jump encoded by r4.

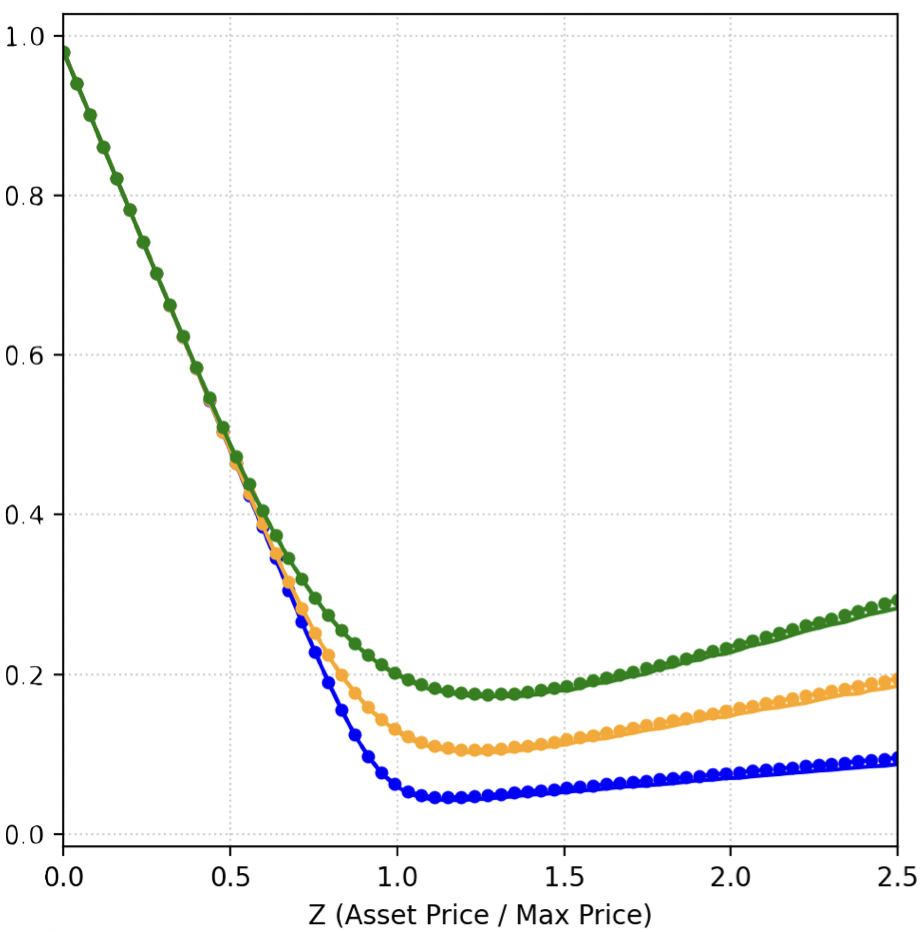

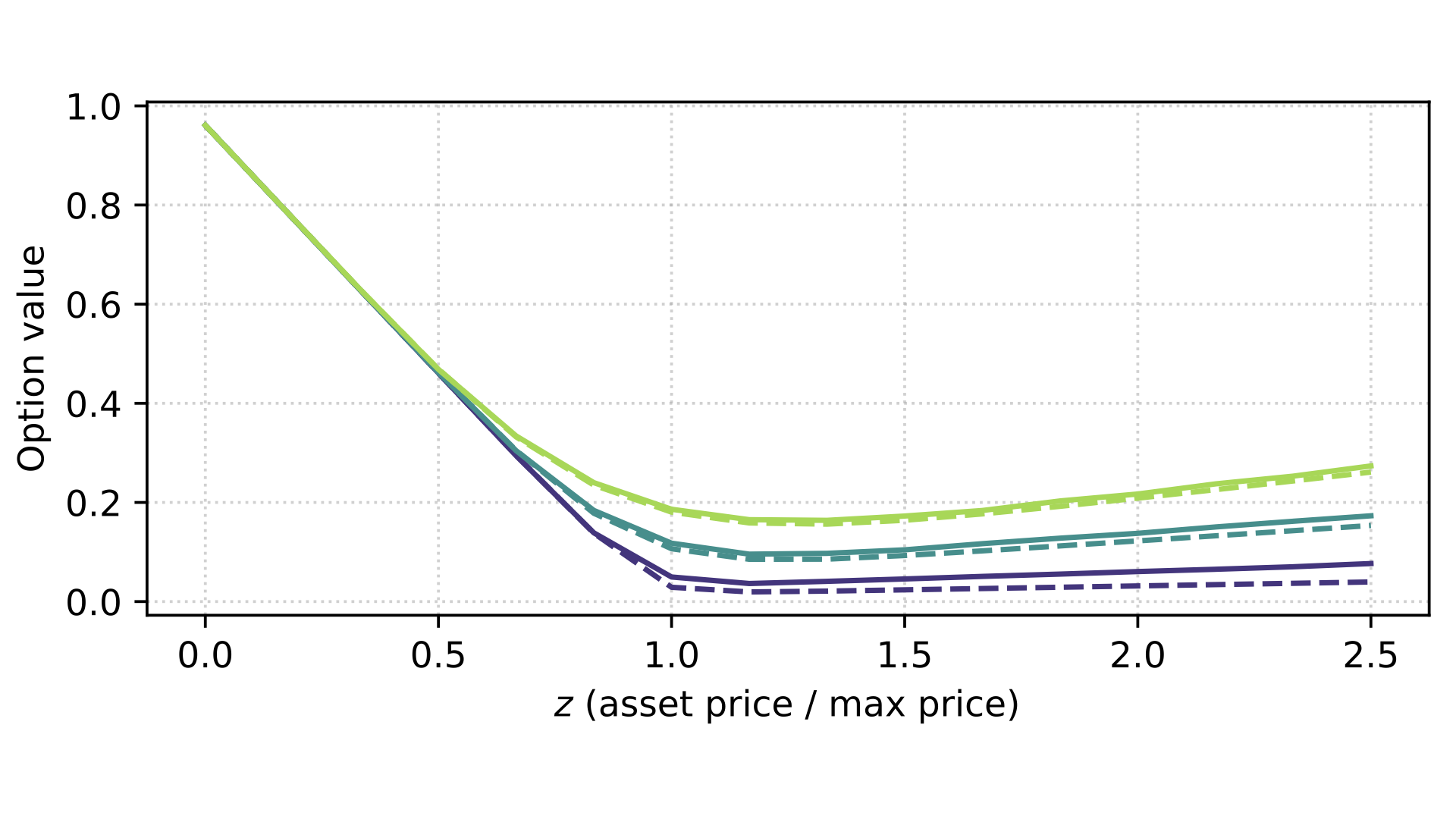

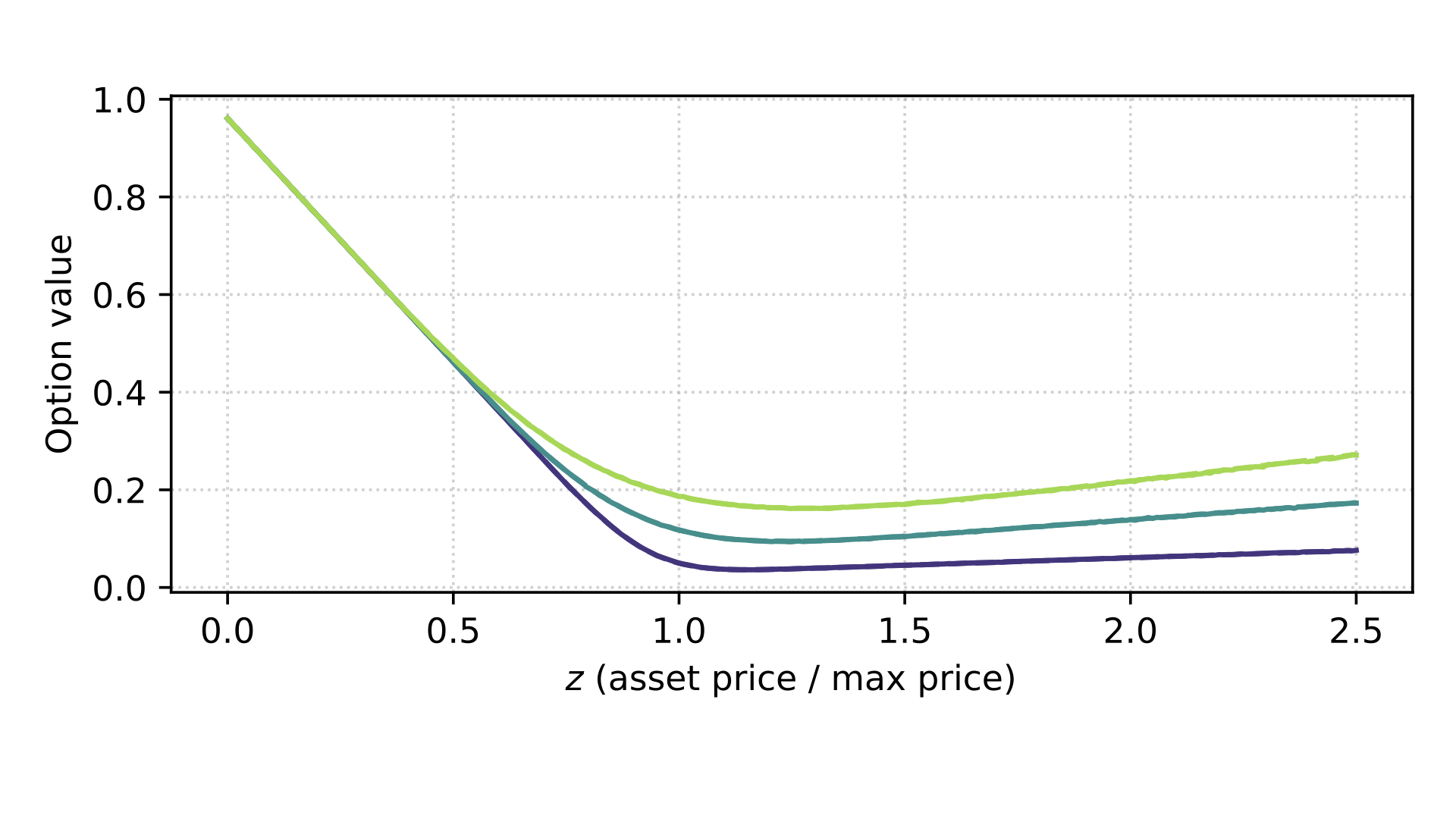

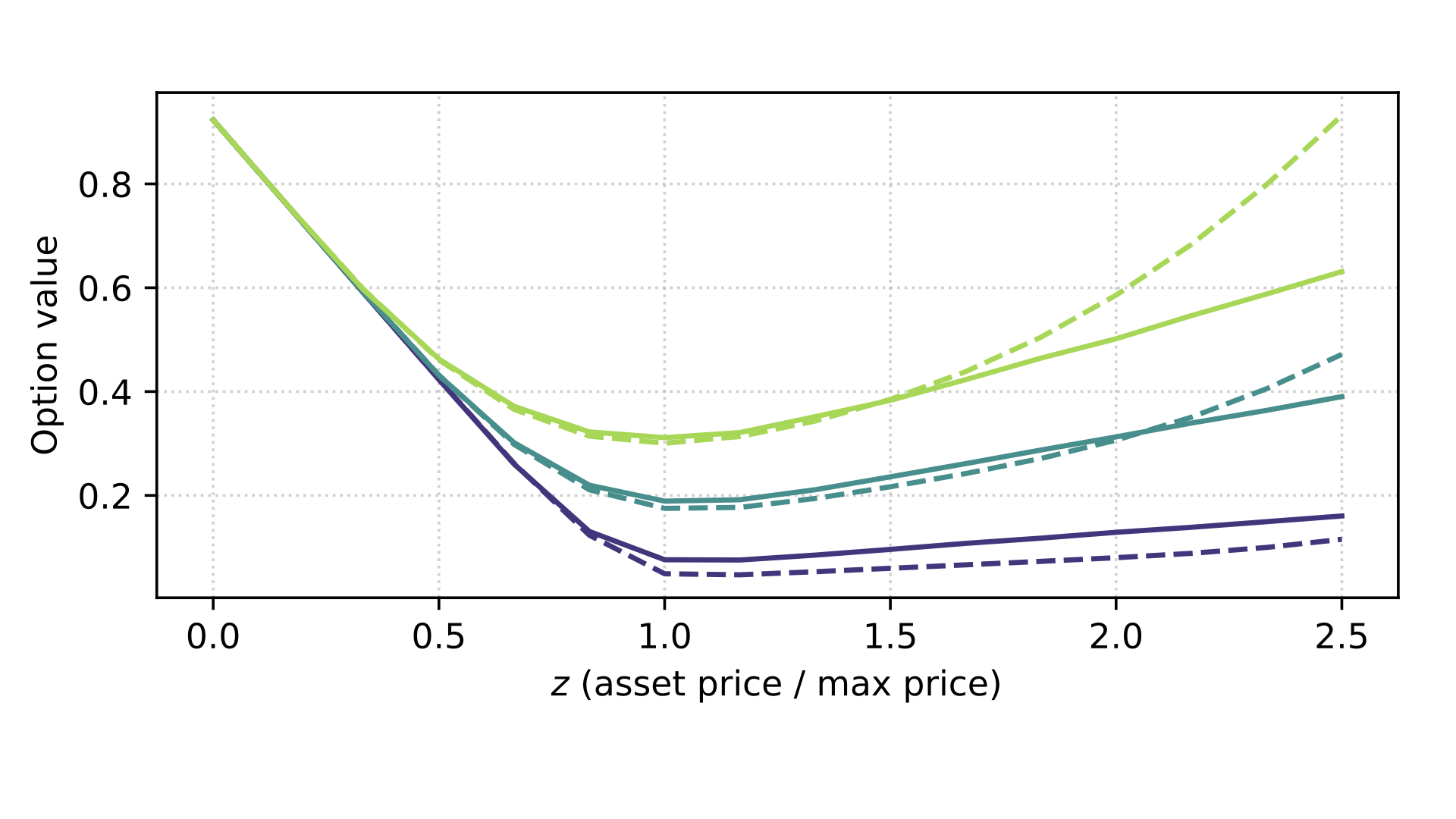

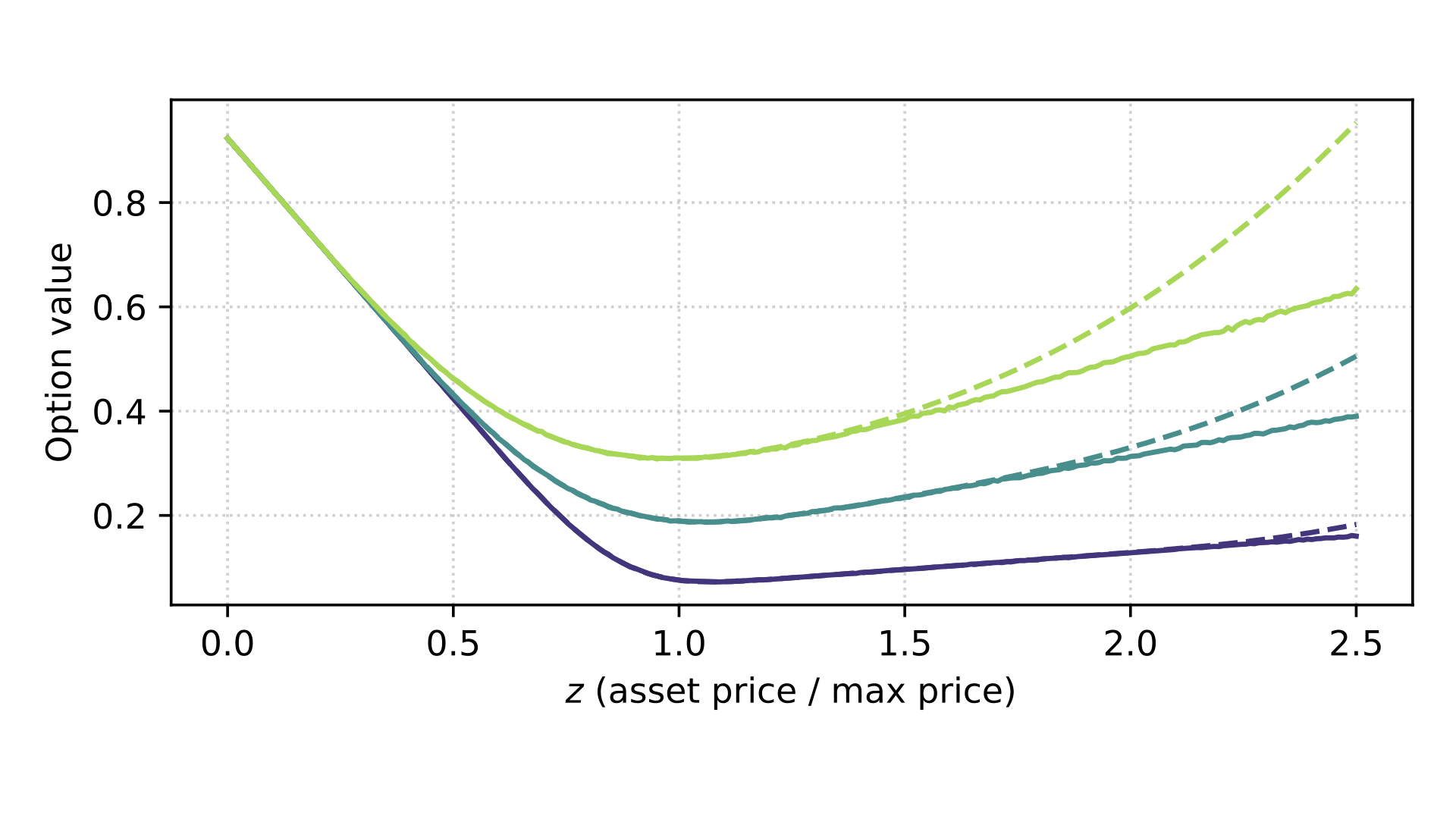

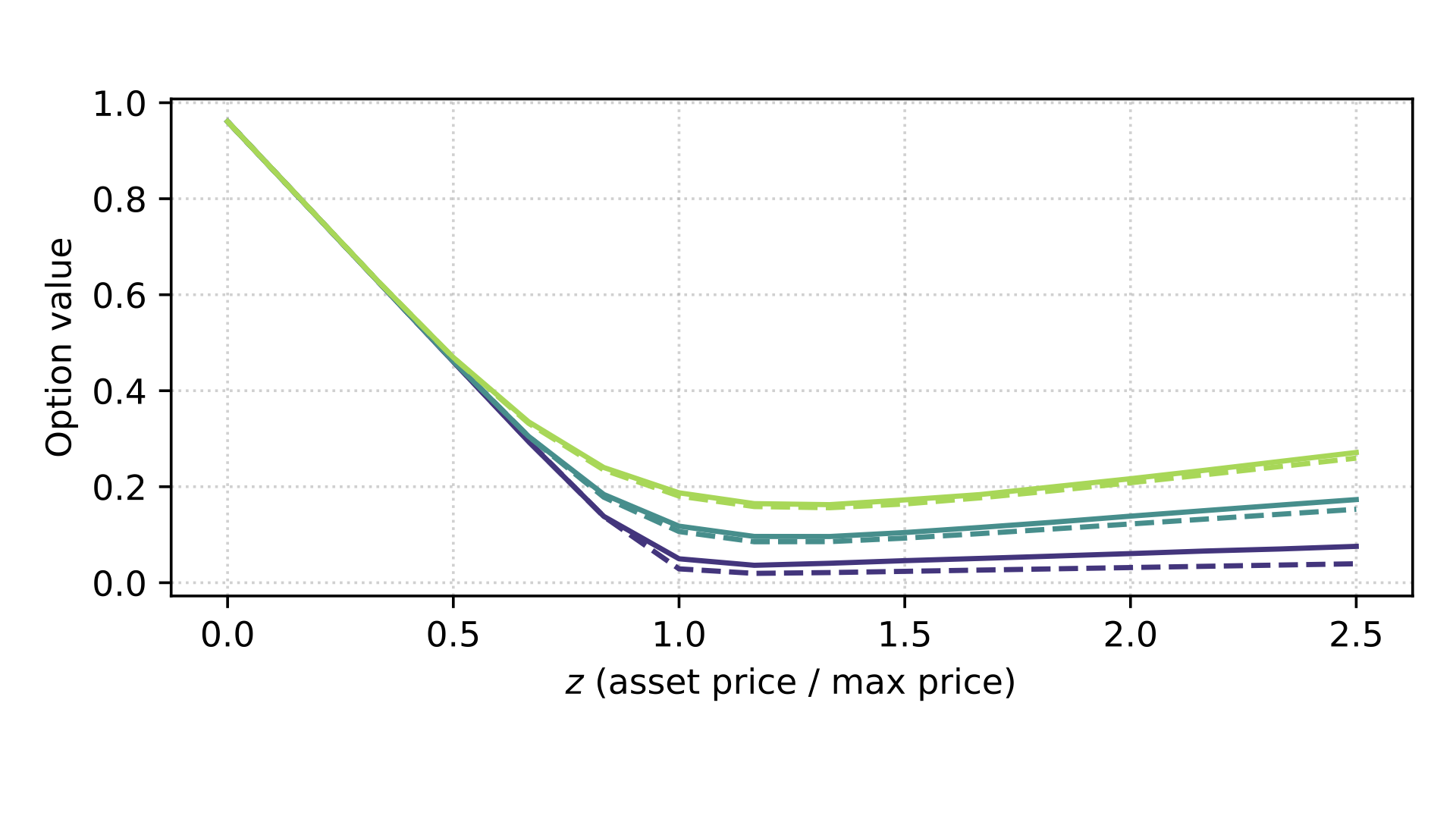

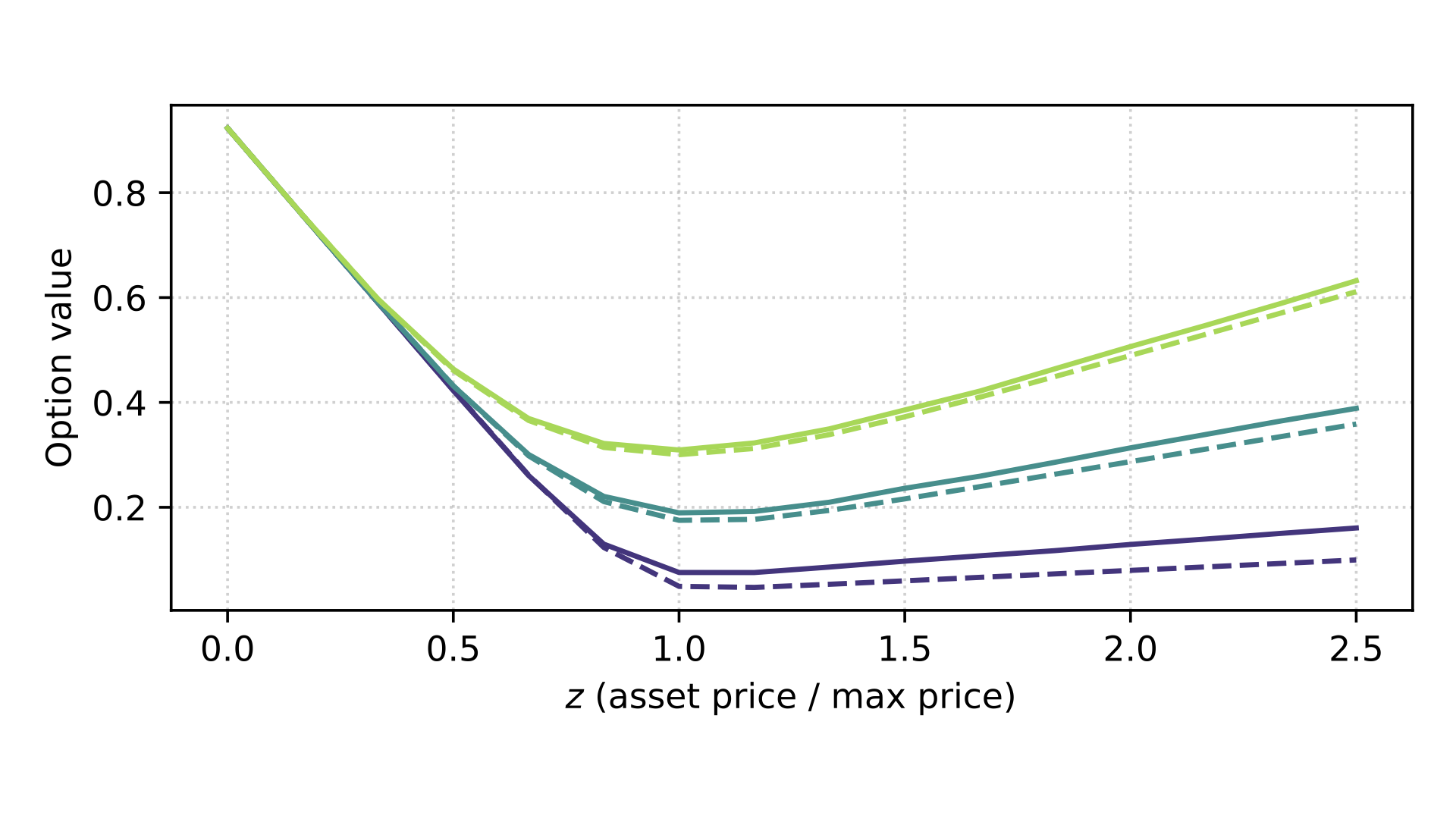

Numerical Observations

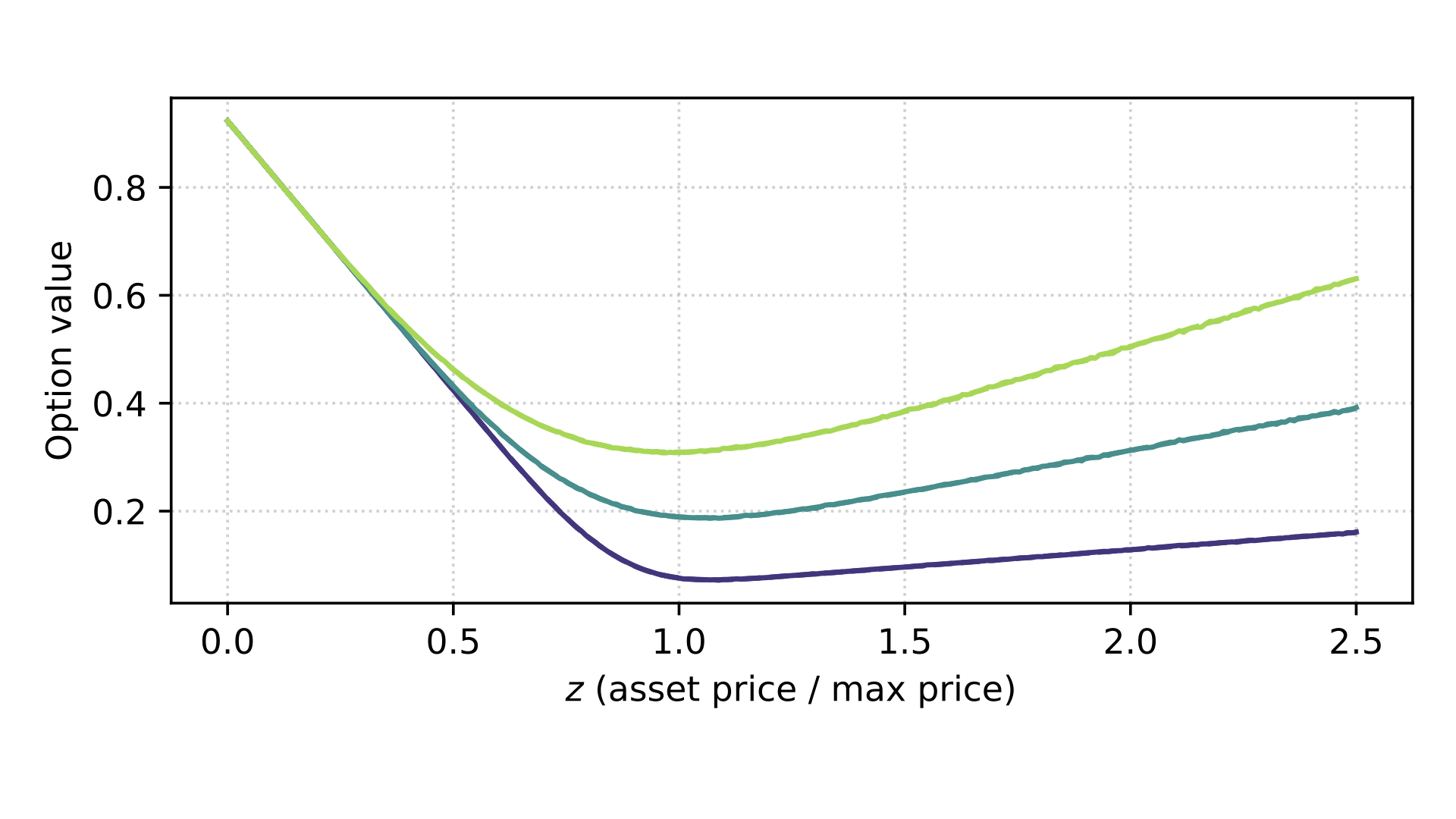

- The accuracy is contingent on the spatial discretization (qubit count): 4-qubit implementations show substantial deviation from Monte Carlo benchmarks; 8-qubit implementations yield much improved accuracy.

- Cumulative error is observed for long maturities or high volatility, driven by the repeated application of jump operators.

Method 2: Simultaneous Evolution of Extended State Space

The second approach removes explicit jumps by redefining the problem as simultaneous evolution of multiple correlated functions, each representing the option value on subdomains determined by the monitoring schedule. This increases the dimensionality of the state vector but yields a system of PDEs that are everywhere continuous, circumventing direct jump handling.

- Hamiltonian Construction: A block Hamiltonian r5 is defined, with block structure coupling the functions representing different monitoring segments.

- Qubit Overhead: The state vector's size is increased to accommodate all functions; for r6 monitoring dates and r7 spatial grid points, the required quantum state has r8 components.

- Quantum Evolution: The entire system is evolved via VarQITE as a single, higher-dimensional imaginary time evolution, with explicit encoding of the relationship between the functions to reflect the original jump conditions.

Figure 3: High-level depiction of the extended state space utilized for simultaneous evolution, eliminating explicit Hamiltonian jumps.

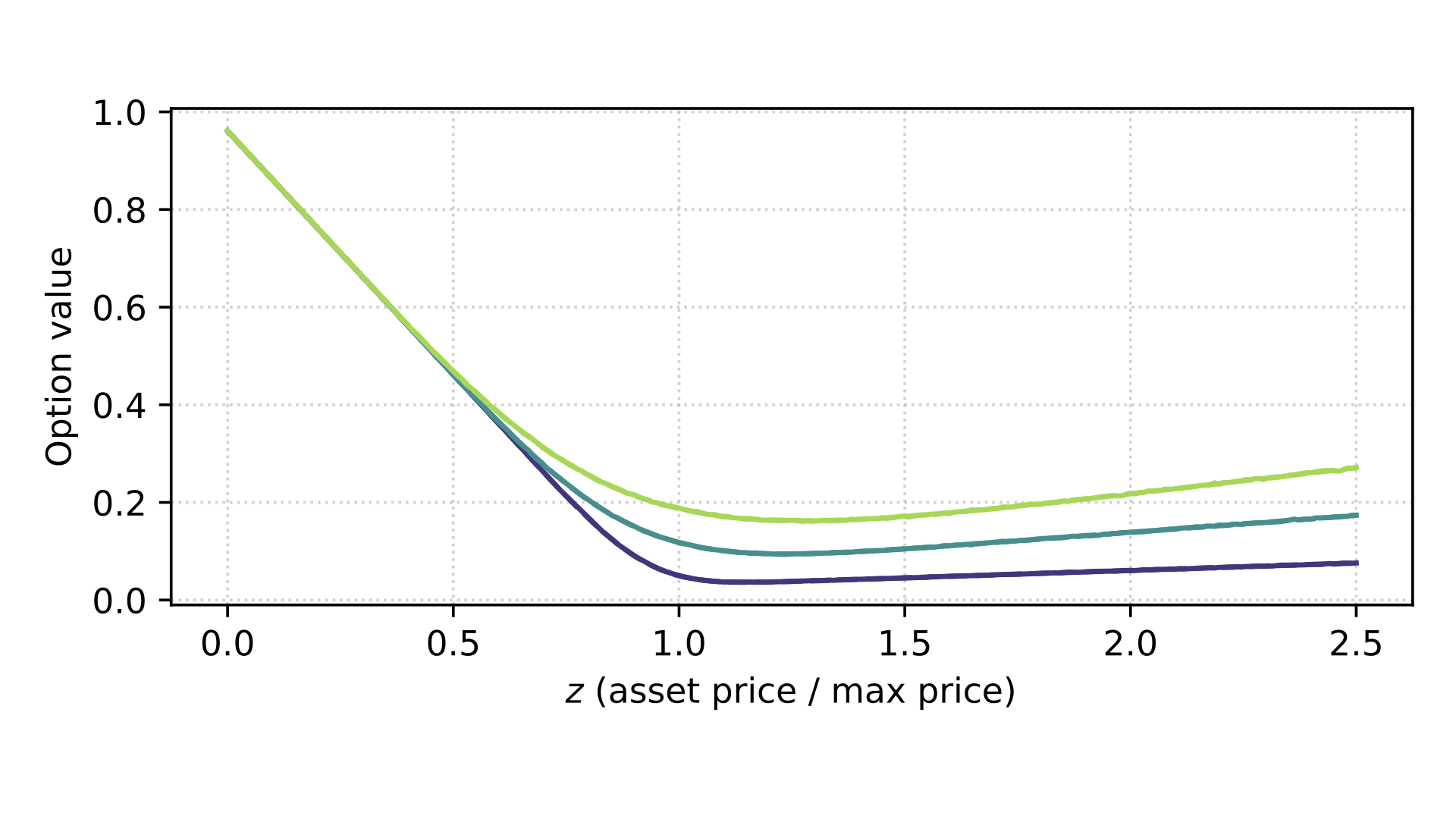

Numerical Observations

Algorithm 2 achieves superior fidelity, closely tracking the Monte Carlo solution for both short and long maturities. The principal trade-off is increased qubit count and more complex Hamiltonian decomposition, as is evident from the substantial increase in the number of Pauli terms required for quantum simulation.

Figure 4: Block structure of the extended Hamiltonian, coupling the evolution of value functions associated with different monitoring intervals.

Quantum Implementation: VarQITE and Ansatz Optimization

Both algorithms utilize the VarQITE technique to implement non-unitary imaginary time evolution through parameterized quantum circuits. A specialized ansatz consisting of only r9 and σ0 gates is used to ensure real-valued quantum states, essential for interpreting the price vector.

Numerical Results and Hamiltonian Complexity

- Spatial Discretization: Increasing the number of qubits yields exponential improvements in spatial resolution (grid spacing σ1), which is critical for accurate option price estimation.

- Hamiltonian Sparsity and Pauli Decomposition: Method 2 yields denser Hamiltonians (more Pauli strings) than Method 1, reflecting its higher expressivity and capability to model the coupled evolution accurately.

Table: Pauli Operator Count for σ2

| Method |

σ3 |

σ4 |

| Algorithm 1: σ5 |

208 |

208 |

| Algorithm 1: σ6 |

192 |

192 |

| Algorithm 2: σ7 (mean per period) |

456 |

2180 |

This increase in Hamiltonian complexity is necessary to capture the coupled non-smooth dynamics in the jump-free formulation.

Implications and Future Perspectives

This work rigorously establishes the feasibility of quantum algorithms in addressing path-dependent, jump-discontinuous derivatives pricing via imaginary time evolution. The simultaneous evolution method demonstrates that quantum circuits can encode and solve high-dimensional, piecewise-smooth PDE systems, pointing toward tractable quantum solutions for even more complex financial derivatives with challenging path-dependencies and non-smooth payoffs.

Practical implementation on NISQ devices is constrained by qubit count, ansatz expressibility (barren plateau), and Hamiltonian complexity. Nonetheless, the exponential convergence properties with qubit count and the avoidance of explicit amplitude estimation bottlenecks make these methods promising as quantum hardware continues to scale.

Theoretically, this framework connects quantum simulation, variational quantum algorithms, and financial PDEs with discontinuous solutions, providing a blueprint for broader classes of stochastic path-dependent control problems in finance and beyond. Future advances will include deployment on fault-tolerant hardware and exploration of alternative (possibly provable) quantum PDE solvers.

Conclusion

Two quantum algorithms capable of pricing discretely monitored lookback options have been introduced and analyzed, with special focus on handling the jump conditions that critically distinguish these derivatives from more canonical cases. The simultaneous evolution algorithm based on extended function space and block Hamiltonians notably outperforms the sequential jump Hamiltonian method in both accuracy and stability, at the cost of qubit and circuit overhead. These results outline clear technical pathways for the quantum valuation of increasingly sophisticated financial products characterized by path-dependence and discontinuities.