- The paper decomposes institutional liquidity into distinct channels and identifies their non-uniform impacts on market execution and trader welfare.

- It employs a synthetic microstructure laboratory, simulating 57,600 observations across 320 markets to quantify changes in spreads, depth, and price impact.

- The analysis reveals that tighter spreads and deeper books do not uniformly benefit all traders, with slow participants facing higher risks during market shocks.

Institutional Liquidity in Prediction Markets: Identification, Measurement, and Synthetic Insights

Motivation and Scope

The paper "What Happens When Institutional Liquidity Enters Prediction Markets: Identification, Measurement, and a Synthetic Proof of Concept" (2604.10005) interrogates the structural transformation of prediction markets as institutional liquidity becomes salient. It shifts focus from pure information aggregation, as measured by forecast calibration, to deeper market microstructure questions—namely, how market-maker coverage, liquidity incentives, and automation/algorithmic trading transform execution quality, internal consistency, price efficiency, and most critically, trader-level welfare and pass-through.

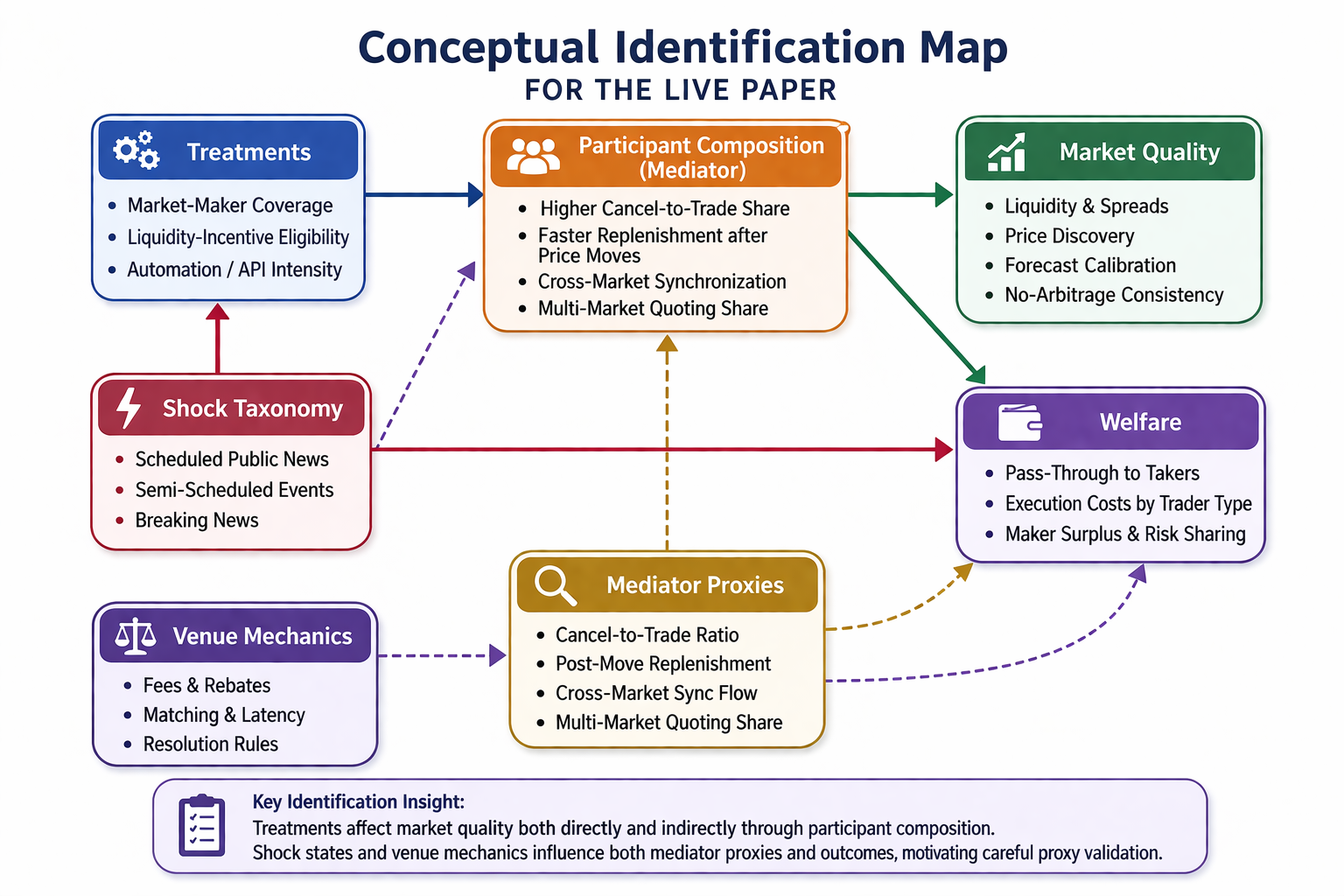

The core thesis is that institutional liquidity achieves more than tighter spreads and deeper books; its distributional consequences are non-uniform, and theoretical welfare improvements may not translate into realized benefits for slow or less sophisticated traders, especially during adverse selection-prone shock states. The paper emphasizes explicit channel decomposition, identification mapping, mediator validation, and synthetic proof-of-concept measurement, refusing the simplistic institutional-liquidity dummy approach.

Figure 1: Conceptual identification map for the live paper: distinct channels for institutional liquidity entry and mediators, with shock states and venue mechanics complicating outcome measurement and proxy validation.

Decomposition of Institutional Liquidity Entry

The study establishes that institutional liquidity is not monolithic. It decomposes entry into four analytically separable channels:

- Designated Market-Maker Coverage: Formal appointments, quoting obligations, or program-driven liquidity provision.

- Liquidity-Incentive Eligibility: Exchange-driven subsidies for displayed or resting liquidity.

- Automation/API Intensity: Technological capability for rapid quoting/reacting via APIs; this is a proxy for algorithmic/professional flow.

- Participant-Composition Shifts: Endogenous change in professional share, measured via messaging and quoting proxies rather than as a primitive treatment.

The empirical design is modular, mapping treatment activation, staggered adoption, and mediator evolution. Explicit identification challenges are addressed, including proxy contamination by venue mechanics/toxicity and endogenous timing around shock events.

Empirical Agenda and Identification Challenges

A compelling empirical agenda is defined, with key methodological points:

- Modular data panels capturing microstructure (order-book, trades, resolutions, metadata) with treatment coding by channel.

- Staggered-adoption and event-study methodology (e.g., Goodman-Bacon decomposition, Sun-Abraham group-time ATTs) with robust clustering and placebo checks.

- Heterogeneity analysis by economically salient contract attributes: information density, hedgeability, resolution clarity, and time-to-resolution, avoiding over-reliance on event categories.

- Welfare decomposition: explicit accounting for taker surplus, maker profit, informed rents, and true risk-sharing; trader-type proxies are required for granular pass-through estimates.

Synthetic Proof-of-Concept Laboratory

To test measurement and identification pipelines without venue-level or private data, the paper deploys a synthetic microstructure panel. This simulates latent belief evolution with discrete news shocks, modular treatment activation points for institutional channels, and endogenous professional-share proxies. The synthetic panel generates outcome families (spread, depth, price impact, calibration, consistency) across 320 markets and 57,600 market-time observations.

Execution and Efficiency Metrics

The paper’s measurement stack includes:

- Effective and Realized Spread: Standard microstructure definitions relative to trade midpoints and post-trade horizons.

- Depth, Price Impact, Adverse Selection: Per-period liquidity and short-horizon price response to order flow.

- Forecast Quality: Brier scores, expected calibration error (ECE).

- Internal Consistency: Complementary book gaps, simplex gaps, and cross-venue semantic dispersion.

Synthetic Results: Channel-Specific Effects

The modular synthetic exercise delivers strong numerical outcomes:

- Average quoted spread compresses from 6.93 to 5.95 cents (−14.1%); effective spread declines from 6.88 to 5.55 cents (−19.3%); depth grows from 156.4 to 206.4 (+32.0%); price impact subsides from 13.1 to 11.95 basis points (−8.9%).

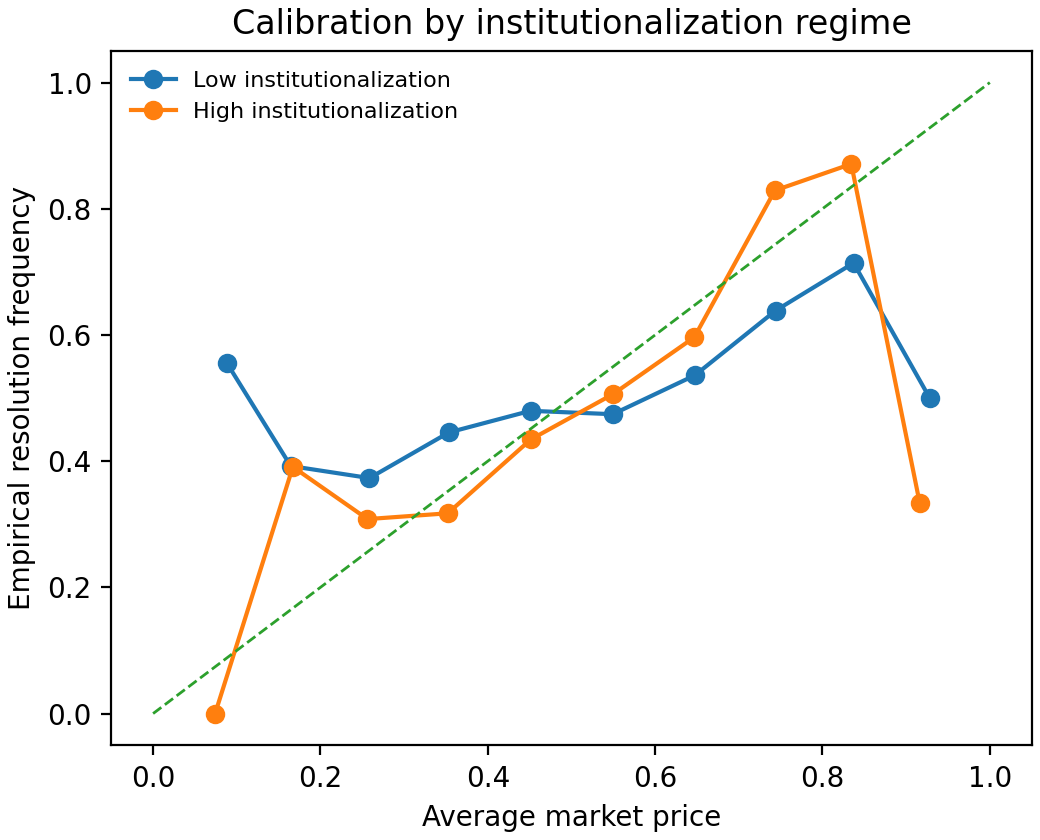

- Calibration effects are weak/mixed: Brier score marginally worsens (0.229 → 0.231), ECE modestly improves (0.049 → 0.043). These results challenge the assumption that institutional liquidity always enhances forecast quality.

- Market-maker activation yields largest spread and impact improvements, followed by liquidity incentives and API intensity; the latter primarily affects internal consistency.

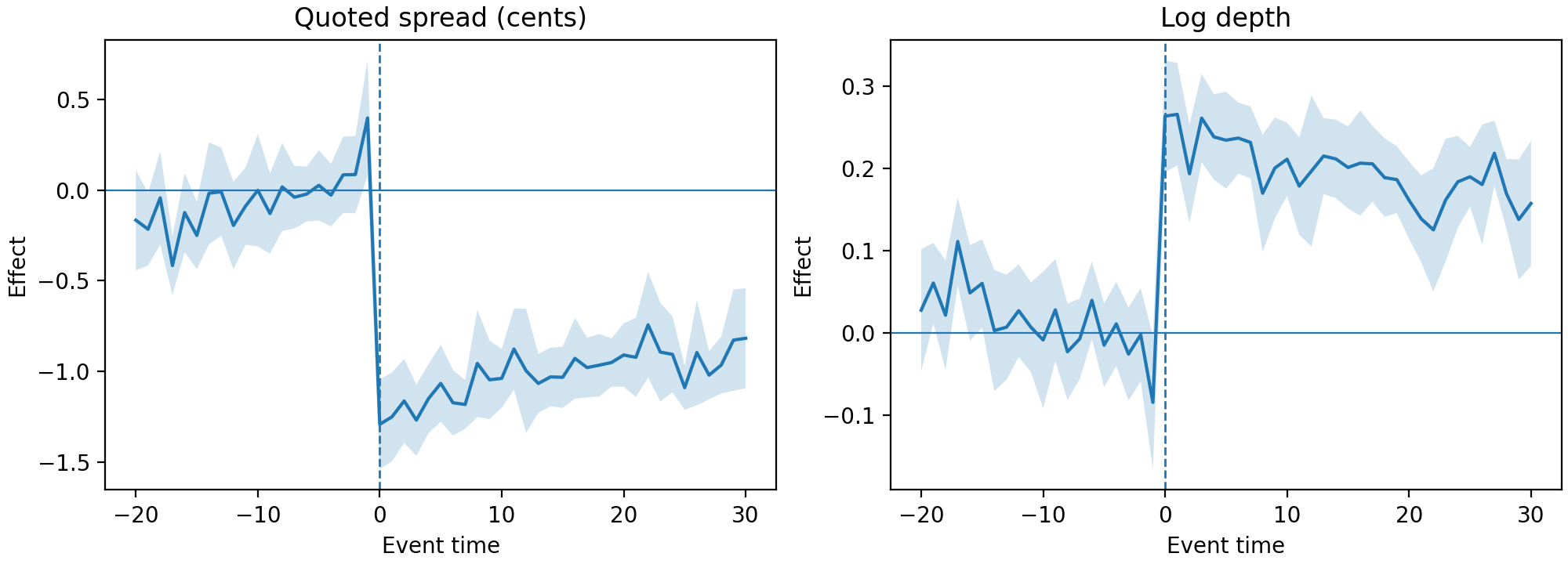

Figure 2: Event-study paths for spread and depth around synthetic market-maker activation, illustrating immediate liquidity gains in the synthetic environment.

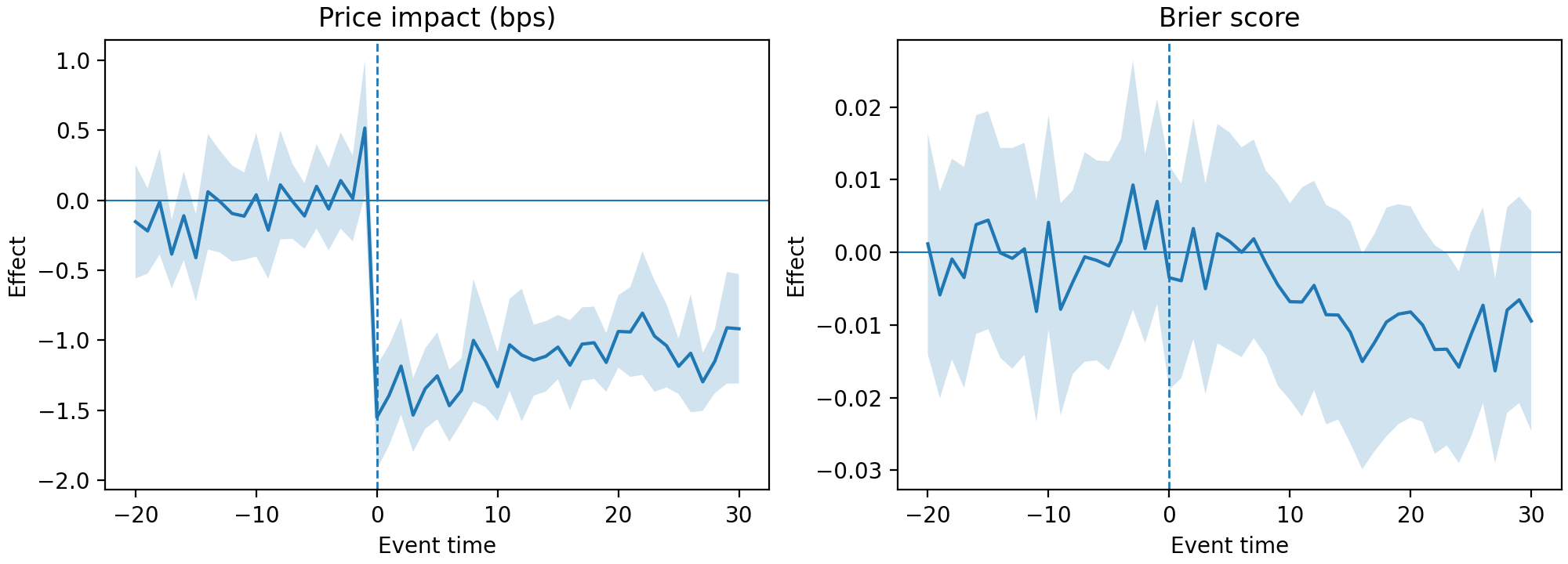

Figure 3: Event-study paths for price impact and Brier score, revealing mixed forecast-quality dynamics alongside execution improvements.

Figure 4: Calibration curve in the synthetic proof-of-concept, highlighting limited forecast-quality gains from high-institutional-liquidity regimes.

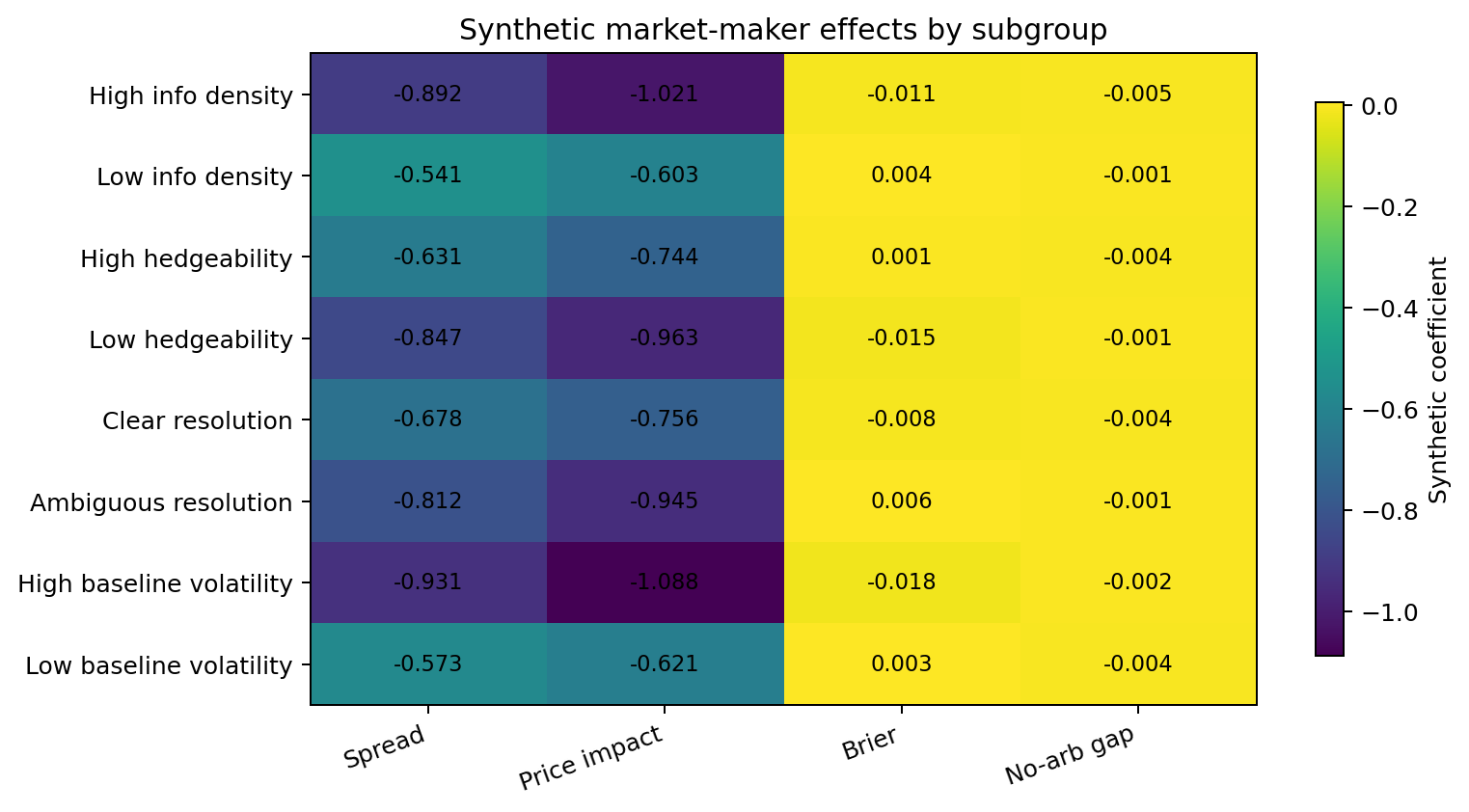

Heterogeneity and Shock-State Interactions

The synthetic panel demonstrates outcome heterogeneity:

Welfare Incidence: Pass-Through and Distributional Effects

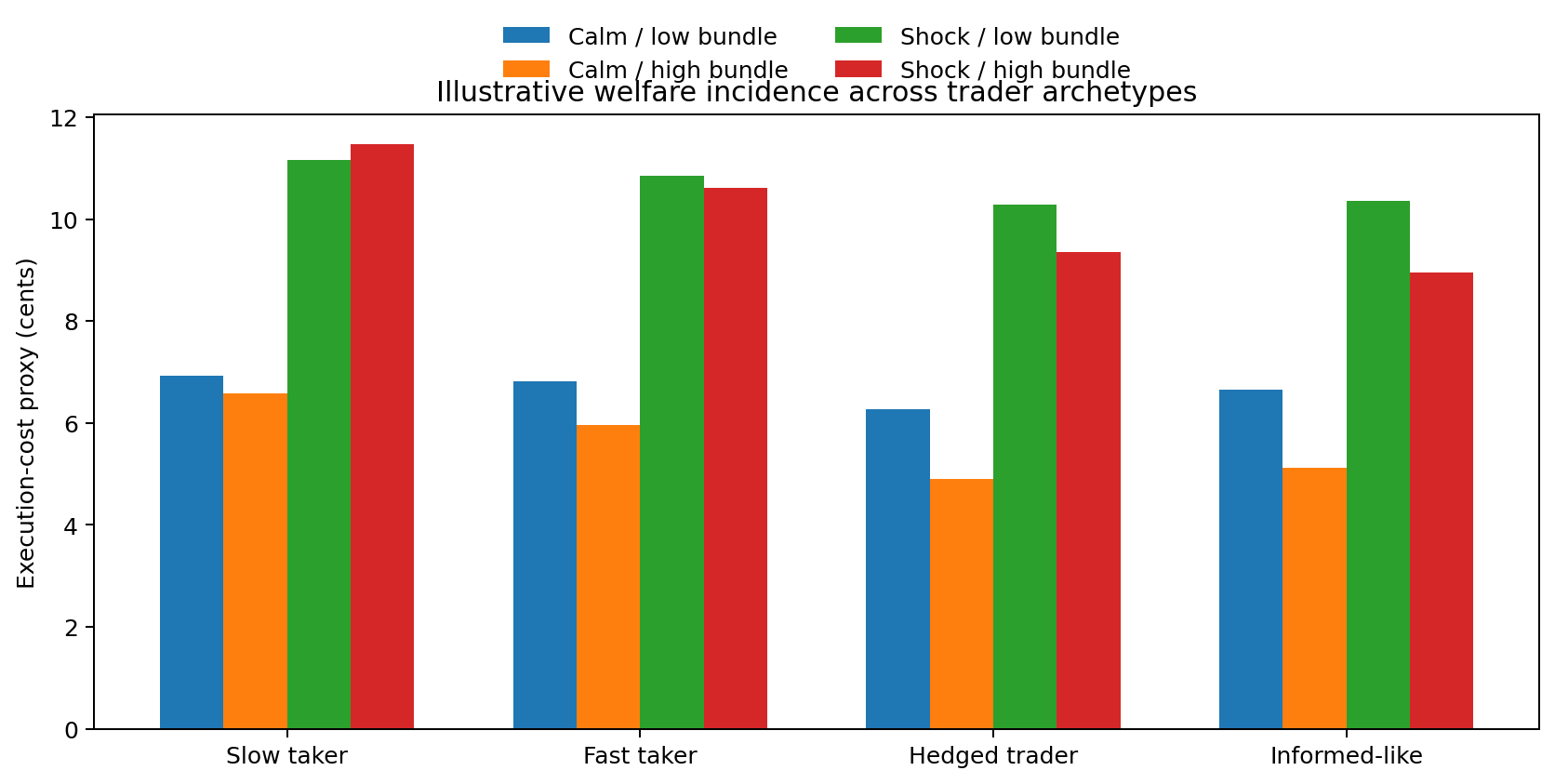

The central welfare implication is that tighter spreads and deeper liquidity are not uniformly passed through to all trader archetypes. Fast, hedged, and informed-like traders receive disproportionately higher execution-quality gains; slow takers may experience welfare loss during shock states regardless of average market improvement. Pass-through and shock wedge estimands are formalized, grounding trader-level welfare claims in measurable execution-price objects, rather than quoted spreads.

Figure 6: Welfare incidence bars across trader archetypes, illustrating highly unequal pass-through in both calm and shock states.

Implications and Future Directions

The theoretical implication is that institutional liquidity, while improving average microstructure, may exacerbate adverse selection risk for unsophisticated flow and create welfare wedges that are not visible in quoted market metrics. Practically, empirical work must rigorously validate type proxies, leverage mediator analysis, and rely primarily on pass-through-based welfare estimation with public data. Regulatory and market-design questions will center on whether liquidity programs and automation systematically disadvantage certain trader segments in shock-driven prediction settings.

Future research in AI-driven prediction-market microstructure will likely focus on:

- Granular identification of trader types using advanced data labeling and behavioral clustering.

- Algorithmic design for equitable liquidity pass-through, potentially adjusting exchange rules or incentive structures.

- More robust study of cross-venue consistency and semantic price dispersion, especially as automated quoting becomes ubiquitous.

Conclusion

The transition of prediction markets to an institutional, electronically intermediated regime necessitates modular channel decomposition, careful mediator validation, and welfare-centric measurement. Average liquidity gains and price efficiency improvements are not guaranteed to translate into equitable trader welfare, particularly under shock-state adverse selection. The synthetic proof-of-concept underscores the need for empirical rigor and trader-level pass-through analysis, providing a blueprint for future live-data research and market-design optimization.