Published 27 Mar 2026 in q-fin.PR and q-fin.CP | (2603.26514v1)

Abstract: In this paper, we develop a general rough volatility model for commodities that provides an automatic calibration of the initial term structure of the futures prices and an appropriate treatment of the Samuelson effect. After the theoretical analysis of this general model, we focus on the rBergomi and rHeston models and their calibration to market data of vanilla futures options on WTI Crude Oil. Finally, numerical results illustrate the performance of the proposed rough volatility models for commodities pricing.

The paper extends rough volatility frameworks to commodity derivatives, incorporating the Samuelson effect via a novel fictitious spot concept.

It employs rBergomi and rHeston models driven by fractional Brownian motion to achieve exact calibration to futures curves and capture short-maturity smile dynamics.

Empirical results on WTI Crude Oil options validate the model with Hurst parameter estimates in the range [0.14, 0.21] and demonstrate improved out-of-sample performance.

Rough Volatility Dynamics in Commodity Markets: An Expert Analysis

Introduction

"Rough volatility dynamics in commodity markets" (2603.26514) presents a rigorous extension of rough volatility frameworks to the context of commodity derivatives. The authors systematically derive a general forward variance model for commodity markets, ensuring consistency with the Samuelson effect and exact calibration to the initial futures curve. The paper provides both theoretical justification and comprehensive numerical evidence, focusing on the rBergomi and rHeston models calibrated to options on WTI Crude Oil. The analysis is framed in terms of the fictitious spot, a device that efficiently mediates between the peculiarities of physical delivery in commodities and the requirements of modern stochastic volatility modeling.

Theoretical Construction

The foundational construction seeks to overcome the disconnect between standard equity-based stochastic volatility models and the realities of commodity derivatives, primarily the divergence between spot and rolling futures at expiry due to delivery mechanisms. The fictitious spot, St, is defined such that Ft(T)=Et[STlast], enabling a martingale framework for futures in the presence of complex physical settlement features.

with explicit relationships ensuring that the mean-reverting drift and volatility terms yield automatic and consistent calibration to the observed futures term structure.

The paper establishes that, given martingale properties for an appropriately constructed Yt, a wide class of rough (and classical) stochastic volatility models can be ported directly into the commodity context, provided that the Samuelson effect and futures calibration requirements are maintained.

Specification: rBergomi and rHeston for Commodities

The rBergomi model is instantiated with a forward variance process driven by a fractional Brownian motion (fBm) with Hurst parameter H<0.5, capturing the "rough" empirical features of asset volatility. The rHeston model provides a mean-reverting fBm-driven variance process. Both frameworks are supported by rigorous existence theorems and martingality proofs, ensuring arbitrage-freeness in the calibrated model.

Crucially, the construction allows the direct transfer of key equity-inspired rough volatility mechanisms to commodities, but with a necessary adaptation for the initial curve and mean reversion.

The Samuelson Effect and Mean Reversion

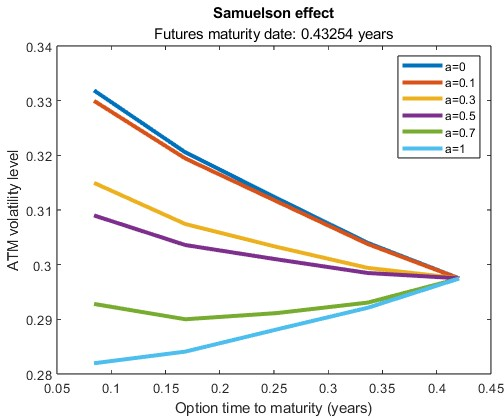

The model explicitly encodes the Samuelson effect—the empirically documented phenomenon of increasing futures volatility as expiry approaches—by the mean reversion speed parameter a(t) in the fictitious spot SDE. The impact is directly visualized; higher mean reversion intensifies the short-maturity implied volatility term structure.

Figure 1: ATM implied volatility with respect to the options maturity date of a simulated mid-curve option for different mean reversion speeds. The Samuelson effect is more pronounced as the mean reversion speed increases.

This mechanistic integration of the Samuelson effect distinguishes the model from prior works, which often fail to reproduce the empirically observed maturity-structural effects unless mean reversion is properly handled.

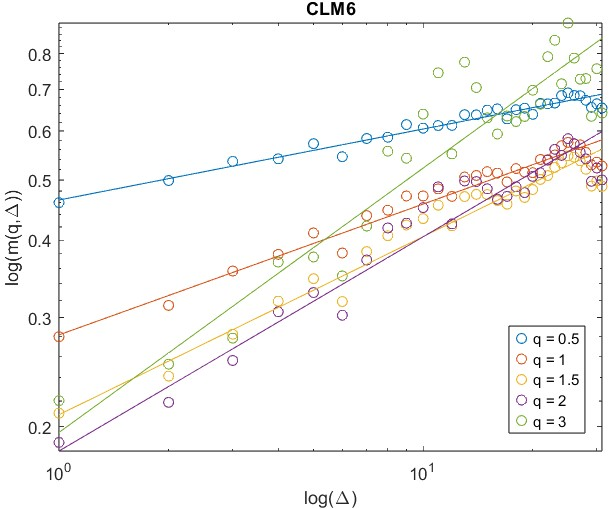

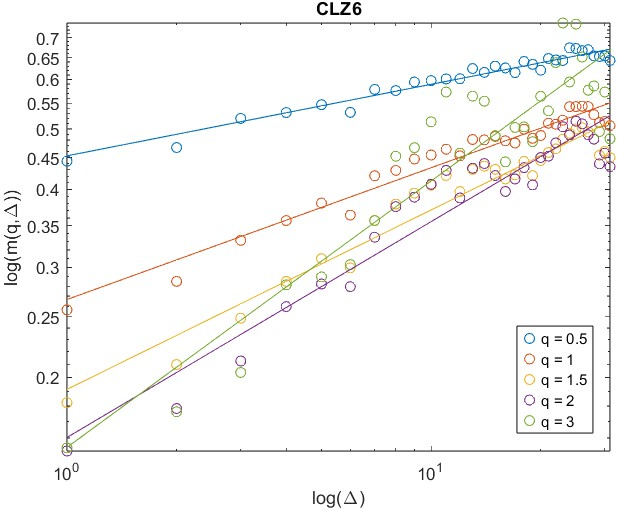

Empirical Estimation: Hurst Parameter in Crude Oil

Empirical analysis confirms the roughness of volatility in the WTI Crude Oil market. The methodology mirrors the approach of Gatheral et al., utilizing realized volatility proxies and linear regression of logm(q,Δ) on logΔ to estimate the Hurst parameter.

Figure 2: Linear regression of logm(q,Δ) on logΔ for the WTI Crude Oil futures contracts listed, supporting the presence of rough volatility (Ft(T)=Et[STlast]0).

All estimated values of Ft(T)=Et[STlast]1 reside in Ft(T)=Et[STlast]2, corroborating prior evidence of commodity volatility roughness and justifying the deployment of rough volatility models in these markets.

Simulation and Calibration

For numerical implementation, the authors employ the Hybrid and Hybrid Quadratic schemes for the rBergomi and rHeston models, respectively. Notably, the calibration targets both term structure and smile features, using piecewise linear parameterizations of the initial forward variance curve for flexibility.

Mean reversion (Ft(T)=Et[STlast]3) is not directly calibrated from vanillas due to weak sensitivity but is fixed at empirically validated levels.

The calibration loss function penalizes fit errors outside the bid-ask at-the-money strikes, forcing realistic fit across the smile.

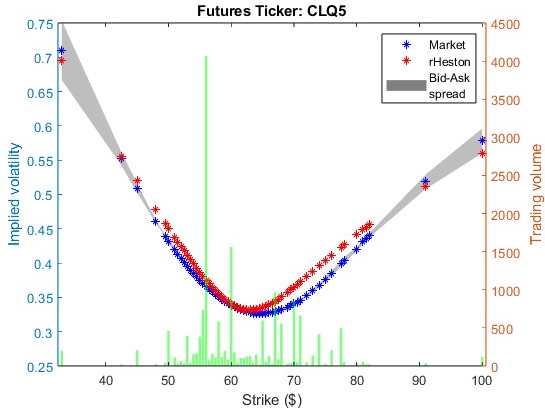

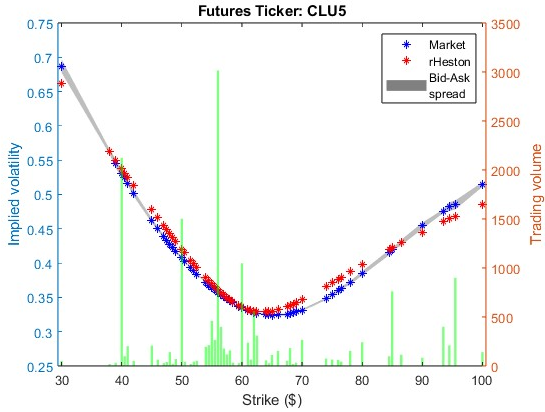

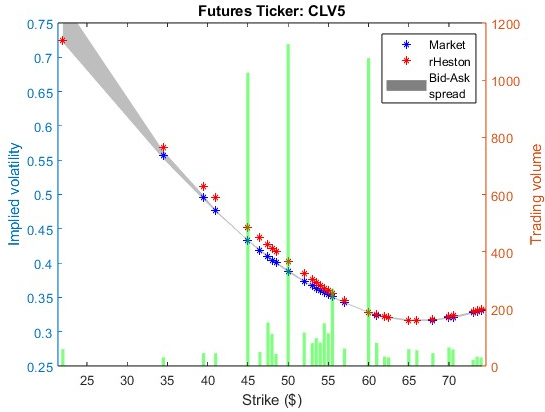

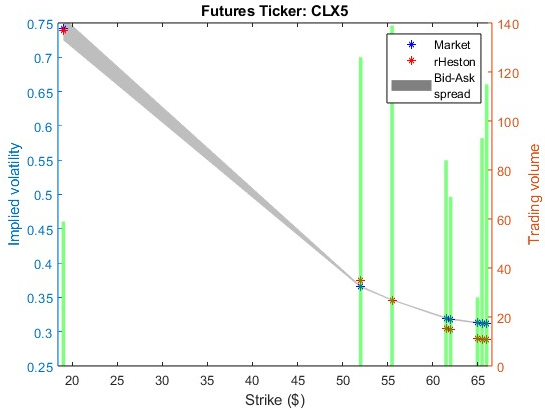

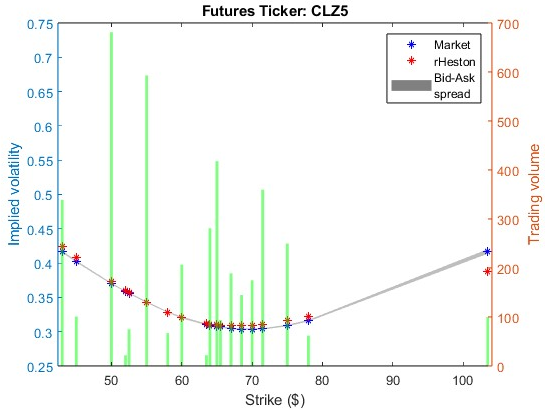

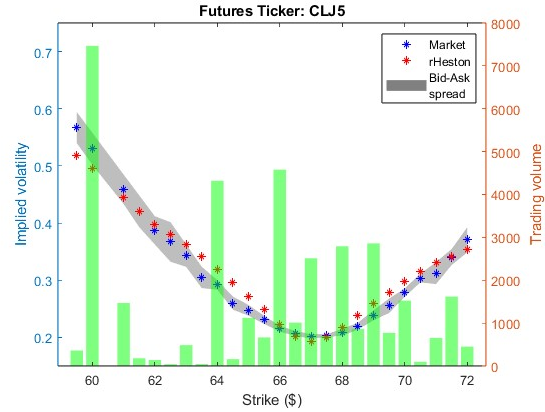

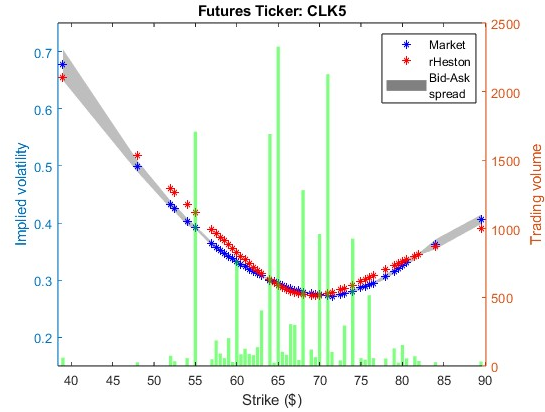

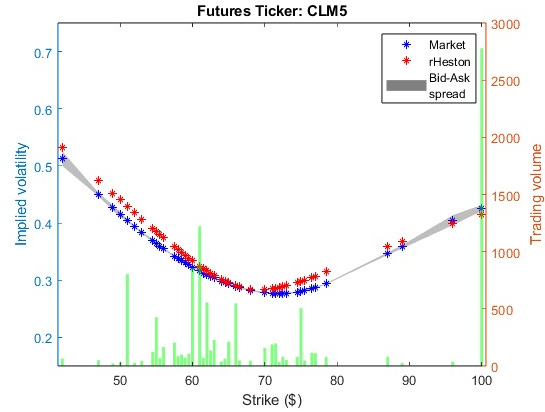

Empirical Results: Out-of-Sample Option Surfaces

Calibrations on WTI options from two dates (March 14, 2025 and June 4, 2025) demonstrate quantitative advantages of rough models, though classical models can match the fit at the cost of extreme parameter values for vol-of-vol and mean reversion. In both data sets, the rough models capture smile dynamics, especially for short maturities, with lower loss values.

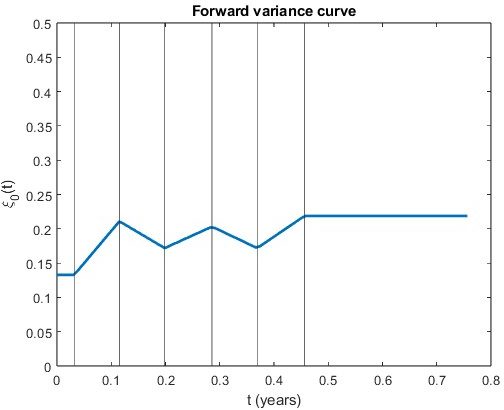

Figure 3: Optimized time-dependent parameter (forward variance curve for rBergomi, rHeston, Bergomi, and Heston models) calibrated to March 14, 2025 data; verticals denote maturity dates.

Rough models show lower estimated Ft(T)=Et[STlast]4 (e.g., 0.0778 for rBergomi) compared to standard equity values, consistent with empirical roughness in commodities.

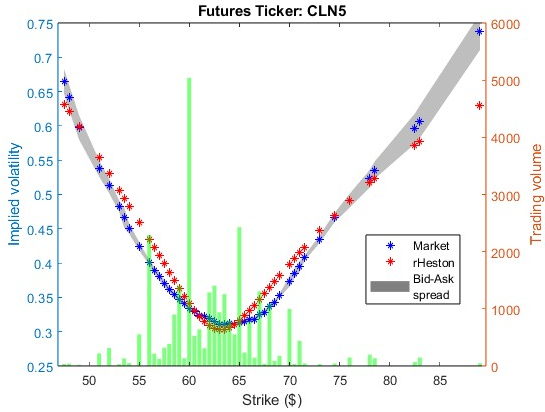

Figure 4: Calibration results of the rBergomi model fit to March 14, 2025—volatility surfaces are accurately captured, especially for short maturities.

Correspondingly, rHeston and classical models are compared, with rough models requiring more moderate Ft(T)=Et[STlast]5 and Ft(T)=Et[STlast]6 values for a similar fit.

Maturity-Dependent Correlation Extension

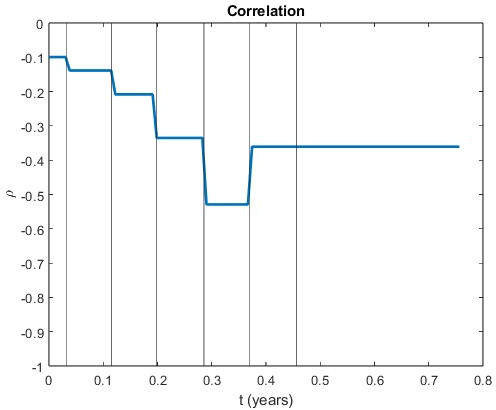

Allowing the spot-volatility correlation parameter Ft(T)=Et[STlast]7 to vary by maturity further enhances calibration accuracy. This extension, amounting to a multi-factor structure, is empirically justified by improved fit at both the short and long ends of the term structure and allows even finer control of the skew dynamics.

Figure 5: Time-dependent correlation and initial forward variance curve for March 14, 2025 calibration; decreasing Ft(T)=Et[STlast]8 for longer maturities indicates more negative spot-vol correlation.

When activated, this extension leads to reduced loss values and improved smile fit, particularly for contracts far from at-the-money or with extreme maturities.

Numerical Robustness and Model Implications

While the rough models obtain superior quantitative fits, the capability of the classical models to replicate option smiles by pushing Ft(T)=Et[STlast]9 and dSt=(α(t)+β(t)St)dt+ξttStdWt1,dξtu=λ(t,u)dWt2,0 to high values highlights a lack of identifiability: several model classes can absorb the relevant empirical features but only via extreme (and arguably nonphysical) parameters in the smooth case.

The implications for both practitioners and theoreticians are manifold:

Practically, the model delivers a fully automated calibration pipeline for commodity volatility surfaces respecting market term structures and stylized facts (Samuelson effect), filling a longstanding gap in commodity derivative pricing.

Theoretically, the approach provides a universal recipe for transferring advanced rough volatility models from equities to commodities without loss of calibration tractability or economic interpretability.

Future Directions: Robustness of model selection with respect to out-of-sample stability, extension to multi-commodity portfolios, and an investigation into deep calibration surrogates and American option pricing are naturally motivated. There remains a need for theoretical identification strategies to disambiguate between "rough" and "extreme smooth" model regimes when both yield similar fits.

Conclusion

This work systematically extends rough volatility modeling to commodity options markets, balancing theoretical consistency with practical calibration. The automatic fit to both initial futures and implied volatility surfaces, integration of the Samuelson effect, and empirical validation on crude oil solidify its utility. The principal technical insight is that rough volatility models—well-established in equity and crypto—are not only applicable, but, under careful construction, supremely adapted to commodities, where volatility dynamics are both rough and structurally dependent on maturity and delivery effects.

The methodology is immediately extensible to other commodity classes exhibiting dSt=(α(t)+β(t)St)dt+ξttStdWt1,dξtu=λ(t,u)dWt2,1 and delivers a platform for ongoing research into robust, arbitrage-free pricing of physically delivered derivatives in non-equity contexts.