Impact of Volatility on Time-Based Transaction Ordering Policies

Published 29 Dec 2025 in cs.GT, econ.EM, and q-fin.TR | (2512.23386v1)

Abstract: We study Arbitrum's Express Lane Auction (ELA), an ahead-of-time second-price auction that grants the winner an exclusive latency advantage for one minute. Building on a single-round model with risk-averse bidders, we propose a hypothesis that the value of priority access is discounted relative to risk-neutral valuation due to the difficulty of forecasting short-horizon volatility and bidders' risk aversion. We test these predictions using ELA bid records matched to high-frequency ETH prices and find that the result is consistent with the model.

The paper demonstrates that volatility induces a systematic variance discount effect on bids in time-based transaction ordering policies.

It employs heteroskedastic Tobit regressions with high-frequency ETH price data to correlate market volatility with bidder behavior.

The findings imply that optimizing auction mechanisms and calibrating reserve prices can enhance transaction efficiency during high volatility.

Impact of Volatility on Time-Based Transaction Ordering Policies

Introduction

The paper "Impact of Volatility on Time-Based Transaction Ordering Policies" (2512.23386) by Sunghun and Park examines the role of volatility in time-based ordering policies within decentralized financial systems, focusing particularly on the Arbitrum Express Lane Auction (ELA). This study is a pioneering empirical analysis into how these mechanisms are influenced by the innate challenges of predicting short-horizon volatility, which is crucial for those participating in these auctions seeking to optimize their strategies and returns.

Background and Motivation

Arbitrum's Express Lane Auction is a pivotal component of the Timeboost transaction ordering policy, which grants latency-sensitive traders exclusive priority access for a minute through a second-price auction mechanism. This advantage is primarily coveted by high-frequency traders engaged in cross-exchange arbitrage, where even milliseconds can determine profitability.

Given that the valuation of priority access is inherently linked to volatile price movements in assets like ETH, the paper hypothesizes a discount in bidders' valuations analogous to the Variance Risk Premium (VRP) observed in traditional financial variance swaps. This discount is attributed to the challenges bidders face in accurately forecasting future volatility over short horizons.

Theoretical Framework

The authors construct a theoretical model outlining how risk-averse bidders value the express lane, conceptualizing it as a single-round auction within a conditionally independent private value framework. Bidders estimate their potential arbitrage profits, which are sensitive to the integrated variance of risky assets, and adjust for the inherent uncertainty in these forecasts due to stochastic volatility and idiosyncratic risk factors.

The model draws parallels with variance swaps, where market prices often reflect a discount relative to theoretical constructs due to traders’ risk aversion—a phenomenon rigorously documented and attributable to both variance risks and other latent risks.

Empirical Analysis

The empirical component of the study utilizes a robust dataset of ELA bids, correlated with high-frequency ETH price data from Binance, over a period from May to October 2025. This data enables the analysis of bidding behavior under varying market conditions, particularly differentiating responses under high and low volatility.

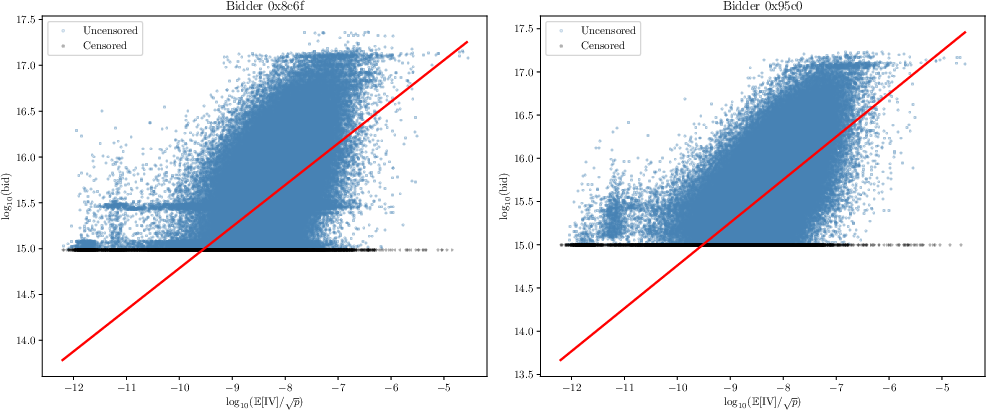

Figure 1: Scatter plot of each bidder's bids and price-adjusted integrated variance. Both are shown in log scale for visibility.

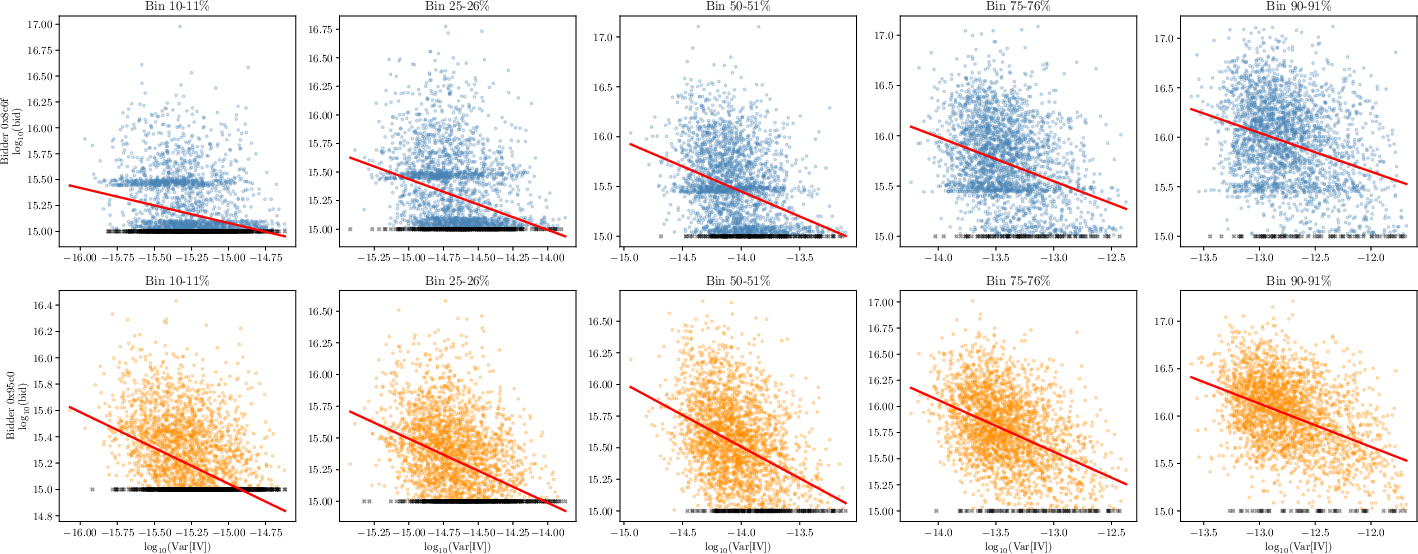

Heteroskedastic Tobit regression models elucidate the dynamics between bidders' expected profits and their corresponding bids as adjusted for volatility expectations and uncertainties. Significant findings include the observation of a systematic discount, corroborating the hypothesis of risk aversion among participants.

Figure 2: Scatter plots of each bidder's bids grouped by percentile of E[IV]/P. A heteroskedastic tobit regression was done for each subsample. For visibility, the figure is in log scale.

Results and Implications

The analysis confirms the existence of a variance discount effect within ELA, linking higher forecast variances with reduced bid valuations due to added risk aversion. This implies that during periods of heightened volatility, overall auction efficiency and revenue capture for Timeboost diminish.

Practically, these findings suggest the potential for optimization of the auction mechanism, perhaps through lengthening auction timeframes or adopting subscription models to stabilize bidding behavior and outcomes. Additionally, these models provide a basis for calibrating reserve prices to maximize strategic revenue extraction.

Discussion and Future Work

While the current model offers compelling insights, it simplifies complex market mechanisms, omitting variables like Total Value Locked (TVL) or cross-asset interactions. Future research could integrate these elements and refine volatility estimations, testing more sophisticated bidder valuation models in varied blockchain contexts.

Concluding, this paper lays foundational groundwork for understanding and engineering time-based ordering policies within decentralized finance, stressing the importance of nuanced volatility treatment to optimize financial mechanisms and align participant incentives more effectively.

Conclusion

Through comprehensive empirical and theoretical exploration, this study affirms a significant volatility discount exists in time-based transaction ordering auctions. These insights foster a deeper understanding of dynamic transaction ordering environments, encouraging further scholarly examination of their efficiency and efficacy under diverse conditions.

“Emergent Mind helps me see which AI papers have caught fire online.”

Philip

Creator, AI Explained on YouTube

Sign up for free to explore the frontiers of research

Discover trending papers, chat with arXiv, and track the latest research shaping the future of science and technology.Discover trending papers, chat with arXiv, and more.