Granular Instrumental Variables in Large Panels: Identification and Inference Across Strong, Nearly Weak, and Weak GIV

Published 2 Jul 2026 in econ.EM and stat.ME | (2607.02095v1)

Abstract: I develop the asymptotic theory of instrument strength for Granular Instrumental Variables (GIV) in large panels with both $N$ and $T$ growing. The strength of the GIV depends on the presence of dominant units. I formalise what dominance means and characterise three regimes of instrument strength. When a few units dominate the aggregate, the instrument is strong. The GIV estimator is consistent and asymptotically normal at the standard $\sqrt{T}$ rate. When large units stand out but do not dominate, the instrument weakens. But I show that the parameter of interest remains recoverable. The GIV estimator remains consistent and asymptotically normal, now at a rate slower than $\sqrt{T}$. When units are comparable in size and none stands out, the instrument is weak in the standard sense. The GIV estimator is inconsistent and has a non-standard distribution. Wald inference is reliable only outside the weak regime. When the instrument is weak, I recommend Anderson-Rubin confidence sets. In practice, the instrument must be constructed in a first stage. I show that the feasible estimator attains the same rate, but its asymptotic variance picks up an additional term from the first-stage estimation. Valid inference must use standard errors that account for this term. I apply the GIV estimator with the correct standard errors to recover the short-run demand elasticities of three commodities: refined copper, crude oil, and natural gas.

The paper establishes a rigorous asymptotic theory characterizing strong, nearly weak, and weak GIV regimes based on the Pareto tail index μ.

It extends PCA-based error estimation to derive an influence function for first-stage estimation error, ensuring robust convergence rates.

Empirical simulations and commodity demand elasticity applications confirm that the granular IV method yields valid inference where traditional IV methods fail.

Granular Instrumental Variables in Large Panels: Identification, Inference, and Regimes of GIV Strength

This paper develops an advanced asymptotic theory for Granular Instrumental Variables (GIV) in high-dimensional panel settings, dissecting the identification and inferential properties of GIV estimators as both cross-sectional (N) and time-series (T) dimensions diverge. It rigorously characterizes instrument strength and estimator consistency across regimes dictated by the cross-sectional distribution of exposure ("granularity")—formally, power-law tails in unit size—and the growth rates of N and T.

Granularity: Power Laws and Instrument Strength

Granularity, the presence of dominant market participants, is modelled as unit sizes following a Pareto law with tail index μ. The value of μ becomes the critical statistic governing GIV strength:

Strong Instrument Regime: For μ∈(0,1), the existence of large outliers sustains strong cross-sectional signal. The GIV estimator attains standard T-consistency and asymptotic normality.

Nearly Weak Regime: For μ>1 but N/T→0, concentration weakens but remains sufficient for identification. Convergence slows to T0, T1.

Weak Regime: For T2 and T3, all units are comparable; instrument power vanishes in the limit and the estimator is inconsistent.

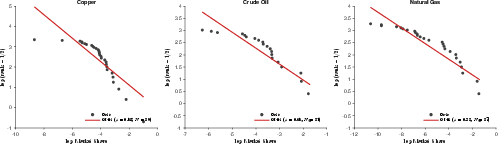

Instrument strength is formally connected to the asymptotic behavior of the Herfindahl index, T4, which decays as T5, T6, or T7 in the three regimes, respectively. Figure 1 visualizes the observed empirical distributions and fitted power-law exponents.

Figure 1: Log-rank versus log-share for the supply panels used in GIV estimation. Each point is one country's time-averaged market share. The red line shows the Gabaix–Ibragimov fitted slope T8.

Asymptotic Properties and Inference by Regime

Strong and Nearly Weak Regimes

In both strong and nearly weak regimes, the GIV estimator remains asymptotically normal—at rate T9 in the former and N0 in the latter. Identification critically depends on N1; the threshold at N2 determines whether dominant units survive dilution as N3. The analysis formally separates these regimes, linking to the nearly weak identification framework of Antoine and Renault (2021) for the intermediate case.

Weak Regime and Robust Inference

For N4 and slow growth of N5 relative to N6, instrument relevance cannot be presumed. The limiting distribution becomes non-standard, rendering usual Wald inference unreliable. Here, the Anderson–Rubin (AR) test is recommended—a procedure immune to instrument weakness, as it exploits the invariance of the N7 null distribution.

These inference recommendations are codified for empirical use:

When the empirical tail index is below 2, use robust Wald intervals.

For N8, invert the AR statistic for valid confidence sets.

First-Stage Factor Estimation in High-Dimensional Panels

Crucially, in realistic applications the GIV must be constructed from estimated idiosyncratic shocks, extracted via principal component analysis (PCA) from high-dimensional interactive fixed effect panels. The paper extends the classic PCA asymptotics of Bai (2003) to GIV, deriving an explicit influence function expansion for the error N9. The central results established are:

The feasible GIV estimator achieves the same convergence rate as the infeasible (oracle) estimator, given the restriction T0.

Its asymptotic variance is strictly larger, with an explicit additional term due to first-stage estimation error. Standard errors must therefore be adjusted, for which the paper provides a consistent HAC variance estimator.

Illustrating the theory, the paper estimates short-run demand elasticities for refined copper, crude oil, and natural gas using global monthly panel data. All supply panels are found empirically to possess power-law tails with T1 for copper and gas, and confidence intervals that extend slightly above 1 for oil, thus supporting both strong and nearly weak identification in practice.

Table 1 summarizes the estimated elasticities; OLS delivers strongly biased or even signed-reversed results, while GIV produces plausible negative elasticities with standard errors tightly matching theoretical predictions.

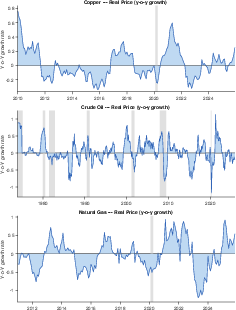

Figure 2: Year-on-year real price growth rates for copper, crude oil, and natural gas (deflated indices), demonstrating the volatility and sample coverage.

Simulation Evidence and Practical Guidance

Extensive Monte Carlo simulations, calibrated to empirical panels, confirm the theory:

Strong regime: Bias and RMSE are negligible, coverage of nominal intervals is accurate.

Nearly weak regime: Bias stays small, but intervals widen as expected; Wald confidence intervals remain robust.

Weak regime: OLS and GIV estimates diverge, coverage inflates, and intervals explode, highlighting the necessity for AR-based inference.

Simulation further demonstrates the sensitivity of GIV inference to both T2 and T3, offering practical diagnostics for applied researchers.

Theoretical Contributions and Comparisons

Compared to prior literature, notably Banafti (2022), the paper extends the domain to all T4 and demonstrates that the additional first-stage variance induced by factor estimation does not vanish in the strong regime—contrary to previous claims based on stronger (and sometimes incompatible) assumptions. The results are robust under more general mixing and moment assumptions, and the paper provides detailed proofs resolving longstanding technical gaps in high-dimensional GIV asymptotics.

Implications and Future Directions

These results have substantial implications for empirical work exploiting cross-sectional granularity for identification, particularly in macro-finance and industrial economics. The sharp delineation of inference regimes allows practitioners to tailor their estimation and inference strategy to the observed cross-sectional structure. The methodology provided for standard error correction is directly implementable in applied research using large, granular panels.

Theoretically, the results invite further work on panel IV methods when granularity is endogenous or where power-law structure itself is subject to change, as well as on extensions to non-linear and dynamic settings.

Conclusion

The paper rigorously formalizes the conditions under which GIV delivers identification and valid inference in large panels, advancing both theory and practice. Three distinct regimes are mapped to the cross-sectional distribution of exposure and sample size growth paths, with a transparent inferential roadmap. It clarifies, with both mathematical and empirical rigor, the requirements for valid use of granularity-based identification, providing robust tools and guidance for researchers leveraging the heavy tails common in economic and financial data.

“Emergent Mind helps me see which AI papers have caught fire online.”

Philip

Creator, AI Explained on YouTube

Sign up for free to explore the frontiers of research

Discover trending papers, chat with arXiv, and track the latest research shaping the future of science and technology.Discover trending papers, chat with arXiv, and more.