- The paper presents a jackknife-based approach that constructs robust Wald, LM, and D statistics for inference in linear IV models with many weak instruments.

- The methodology overcomes size distortions in traditional tests, showing improved power in simulations and empirical setups like Mendelian randomization.

- The framework is practical for high-dimensional settings such as shift-share designs and biobank data, ensuring consistent and robust inference under heteroskedasticity.

Jackknife-Based Inference in Linear IV Models with Many Weak Instruments

Introduction and Motivation

The paper "Jackknife Instrumental Variable Inference" (2604.15437) provides a comprehensive treatment of inference in linear regression models with potentially endogenous regressors, many instruments, and heteroskedasticity. This is a critical extension of classical IV theory, as modern applications increasingly employ high-dimensional or weak instruments, where traditional methods like 2SLS and Anderson-Rubin tests encounter severe size and power distortions. The authors address the challenge by establishing a unified framework for hypothesis testing, building a "trinity" of Wald, Lagrange Multiplier (LM), and distance (D-type) statistics based on robust jackknife estimators (e.g., SJIVE, HLIM, JIVE variants).

The framework covers both full parameter vector and general linear restrictions and provides asymptotic results under many-instrument, many-weak-instrument asymptotics. Crucially, the approach does not assume instrument homoskedasticity, accommodating realistic settings such as shift-share/Bartik designs, Mendelian randomization, and machine learning IV methods.

Statistical Framework and Methodology

The core innovation is the construction of test statistics via jackknife-based objective functions. The jackknife device yields estimators that are consistent when the number of instruments (k) grows proportionally with the sample size (n), under heteroskedasticity and endogeneity. Specifically, the paper formalizes two classes of objective functions:

- Ratio of Quadratic Forms: This gives rise to estimators like SJIVE [BC15], designed to mimic the structure of the LIML estimator but robust to heteroskedasticity and weak identification.

- Quadratic Forms (JIVE1/JIVE2): These are computationally simpler and correspond structurally to more classical forms of jackknife IV estimation.

Conventional test statistics such as the Wald and LM tests are generalized by constructing them from these robust objective functions. The novel D-type (distance) statistic provides an analogue to the likelihood ratio in the GMM/ML context but adapted for jackknife-based IV.

The asymptotic distributions of these statistics are nonstandard: under the null, they converge to weighted sums of chi-square variables (i.e., chi-bar-square distributions) whose weights and eigenvalues are functions of the data-generating process and instrument structure. The authors show that, for a class of modified statistics, the limit can be made a standard chi-square distribution, a property that is often desirable for practitioners.

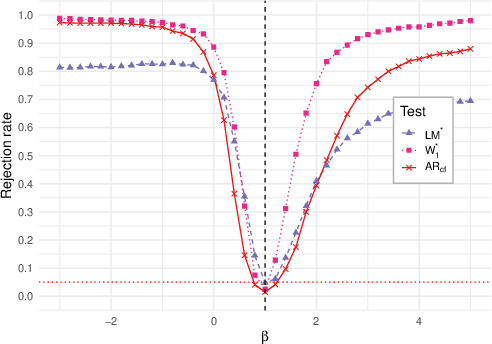

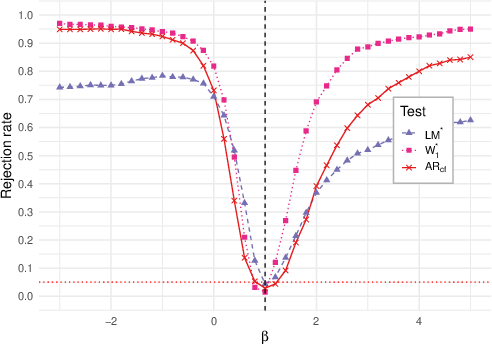

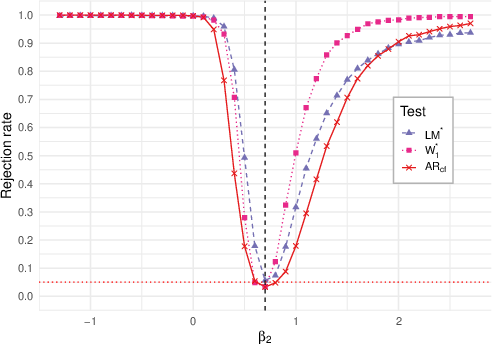

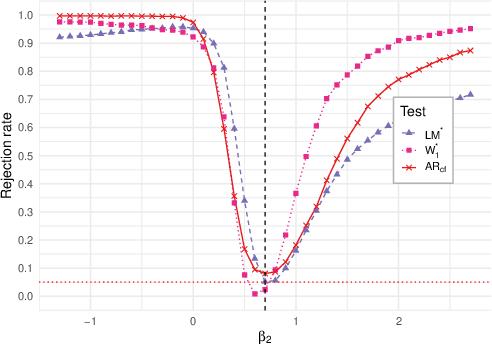

Figure 1: Simulated finite-sample rejection probabilities for jackknife-based and Anderson–Rubin-type statistics under SJIVE specification, highlighting comparative size distortions.

Asymptotic Theory

The main theoretical contributions are:

- Limiting Distributions: Under a general set of regularity conditions (instrument strength, fourth moment bounds, positive minimal eigenvalues, etc.), the Wald, LM, and D statistics derived from jackknife-based estimators are shown to converge to well-defined chi-bar-square or, after transformation, chi-square limits.

- Consistency and Robustness: By exploiting jackknife covariance estimators and suitable matrix theory arguments, the tests are uniformly consistent and robust to many weak instruments even under heteroskedasticity. The D-type statistic, in particular, is new in this context and fills a gap in the robust IV testing literature.

- Hypothesis Structure Generality: The framework rigorously treats both tests on full parameter vectors and general linear restrictions, which is often omitted in previous weak-instrument research.

These statements are validated by extensive simulations showing robust empirical size and power even in settings with many weak or nearly collinear instruments, where classical methods fail.

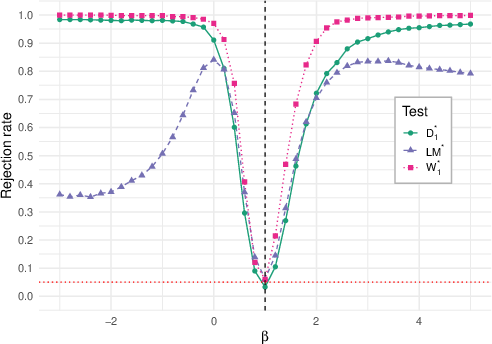

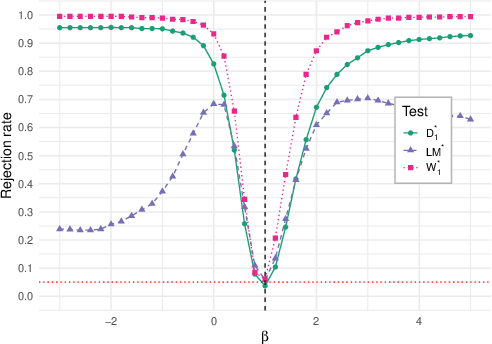

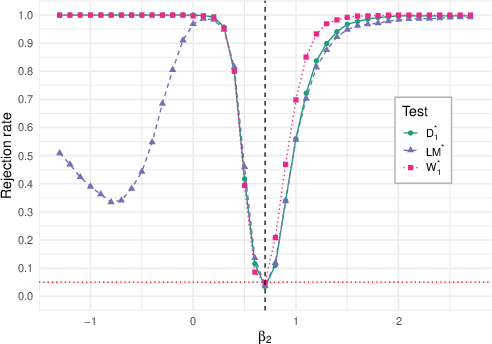

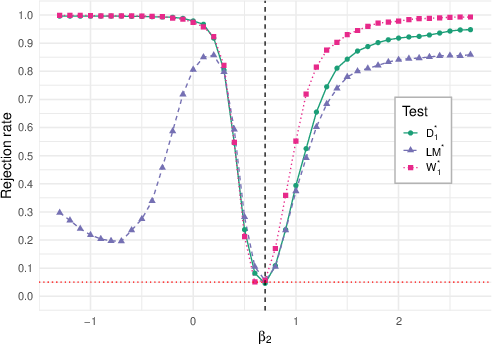

Figure 2: Power curves for Wald, LM, and Distance (D) tests under SJIVE across varying instrument strengths α and signal parameters r.

Monte Carlo Simulations

The simulation study is extensive and technically detailed, featuring DGPs that mimic common empirical setups (single vs. multiple endogenous regressors, varying n, k, and instrument strength). The simulation results are strong, with several explicit findings:

- For moderate sample sizes (e.g., n=200), the D and Wald tests exhibit less size distortion than Anderson-Rubin variants, especially when instrument strength is weak or moderate (e.g., r=32,64). For example, with α=0.05 and r=32, the rejection rate for D under SJIVE is n0 vs. Anderson–Rubin at n1.

- Power dominance: Wald and D-type statistics possess higher power than LM in most scenarios. Anderson-Rubin, even with cross-fit variance, is markedly conservative and exhibits lower power.

- Pathological Behaviors: Certain LM variants (especially those based on HLIM/JIVE2) lose significant power against distant alternatives, confirming theoretical predictions in the literature.

Figure 3: Comparative power and null rejection rates across test statistics for DGP2 (two endogenous regressors) under SJIVE specification.

Empirical Illustration: Alcohol, BMI, and Mendelian Randomization

A notable empirical section applies the methodology to UK Biobank data, assessing the impact of alcohol consumption on BMI using up to 91 SNPs as instruments. The empirical design is a canonical many-instrument problem. The findings are robust—across all test statistics and both chi-bar-square and chi-square reference distributions, the null hypothesis of no effect is strongly rejected (all n2). This uniformity is stable across both the full sample and non-trivial subsamples (down to n3).

The results underscore:

- Practical feasibility: The tests are computationally tractable at biobank scale.

- Robust inference: Even in high-dimensional, potentially weak-instrument settings, the tests avoid overrejection and retain power.

Figure 4: Illustration of empirical distribution of test statistics from the Mendelian randomization example (effect of alcohol on BMI), showing high levels of statistical significance for all jackknife-based tests.

Theoretical and Practical Implications

This framework unifies and extends prior results on weak-instrument-robust inference, addressing both theoretical and practical demands:

- Theory: Provides new central limit theorems, limiting distribution characterizations (both chi-bar-square and chi-square), and generic consistency proofs for jackknife-based estimators under high-dimensionality.

- Practice: Delivers operational algorithms for robust inference in weak and/or many-instrument settings—including high-dimensional Mendelian randomization and Bartik applications. The tests routinely outperform traditional Anderson-Rubin procedures.

Potential extensions include adaptation to fixed-effects panel IV, clustered data, and methods for constructing robust confidence sets under weak identification. The framework’s flexibility appears suitable for settings encountered in modern econometrics and causal inference using high-dimensional or machine learning-derived instruments.

Conclusion

The paper offers a technically rigorous and implementable suite of hypothesis tests for linear IV models under realistic, challenging conditions—many, potentially weak instruments, heteroskedasticity, and non-trivial hypothesis structures. The proposed trinity of jackknife-based tests is both theoretically justified and empirically validated, with clear advantages over classical approaches in terms of size, power, and computational complexity. The results are directly relevant for empirical researchers working with high-dimensional IV settings, including genetics, labor, and macroeconomics, and provide an extensible foundation for future robust inference in instrumental variable models.