- The paper introduces MACROCAST, a TSFM that eliminates temporal contamination and revision bias through vintage-consistent training.

- It employs a lightweight RNN with a two-phase approach: extensive synthetic pretraining followed by vintage-specific econometric fine-tuning.

- MACROCAST significantly reduces RMSFE in real-time macroeconomic forecasting across 123 series compared to traditional benchmarks like AR(1).

MACROCAST: A Vintage-Consistent Time Series Foundation Model for Real-Time Macroeconomic Forecasting

Introduction and Motivation

The paper "MACROCAST: A Vintage-Consistent Time Series Foundation Model for Real-Time Macroeconomic Forecasting" (2606.28670) addresses the practical and methodological limitations prevalent in the application of Time Series Foundation Models (TSFMs) to real-time macroeconomic forecasting. While TSFMs such as Chronos-2, Moirai2-Small, and TimesFM demonstrate transfer learning capabilities across diverse domains, their deployment in economic practice is undermined by two core leakage issues: temporal contamination and revision bias. Temporal contamination arises when a model’s training set includes information unavailable to a forecaster at test time. Revision bias is introduced when models are trained on fully-revised historical macroeconomic releases rather than preliminary, vintage data as seen by actual forecasters, causing in-sample data to systematically differ from out-of-sample reality. These issues are especially problematic in macroeconomic forecasting, where benchmark accuracy must reflect true real-time uncertainty, not artifacts of retrospective data cleaning.

Model Architecture and Training Protocols

MACROCAST is based on a lightweight RNN architecture, specifically leveraging the TempoPFN design, which utilizes a linear gated recurrence to preserve efficiency and interpretability while circumventing the prohibitively high quadratic complexity of self-attention architectures. The model comprises approximately one million parameters—one to two orders of magnitude below Chronos-2 (120M) and Moirai2-Small (10M)—enabling rapid vintage-specific retraining even on modest hardware.

The training regime is two-phased:

- Synthetic Pretraining: The model is first exposed to approximately ten million strictly synthetic univariate time series, sampled from an expanded composition of generators. These generators represent a diverse set of statistics: trends, periodic components, abrupt regime shifts, anomalies, heavy-tailed noise, and, critically, complex cross-dependencies instrumental for capturing the macroeconomic structure. This phase is entirely free from real-world data, ensuring strict exclusion of both temporal and revision leakages.

- Vintage-Consistent Fine-Tuning: The pretrained weights are subsequently fine-tuned on synthetic panels generated from econometric models (Bayesian VARs, dynamic factor models, ARIMA) fit exclusively to data as it appeared in each vintage from the ALFRED repository. Only vintage-specific panels are used for simulation, with no direct training on actual observations. This approach guarantees the fine-tuned model is conditioned solely on information historically available at each forecasting origin, facilitating genuine real-time estimation and eliminating both forms of leakage.

Empirical Evaluation and Numerical Outcomes

The empirical evaluation implements a rigorous pseudo out-of-sample protocol on the FRED-MD macroeconomic panel, spanning 123 series, with forecast origins anchored to true historical vintages (August 1999 to December 2024). All models—including MACROCAST, Chronos-2, Moirai2-Small, Bayesian VAR, dynamic factor, and AR(1)—are estimated using only data released at the corresponding vintage. Forecasts are scored against six-month delayed "actuals" to neutralize short-term revisions yet still reflect later updates relevant for policy.

Performance is summarized via RMSFE ratios (model RMSFE divided by AR(1) RMSFE), share of series with RMSFE improvement, and statistical significance from Diebold-Mariano tests.

Key findings:

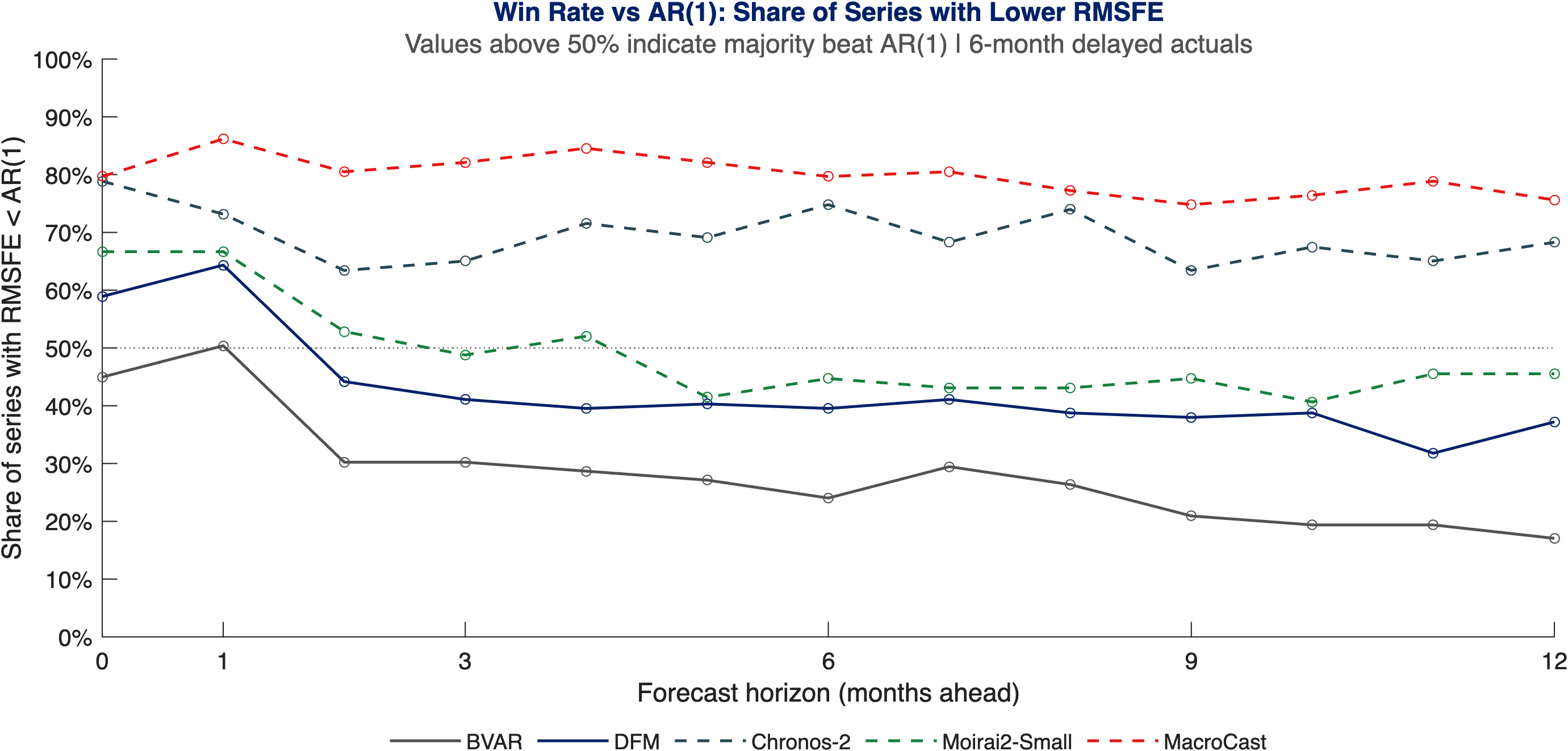

- MACROCAST achieves lower RMSFE than AR(1) in approximately 80% of series-horizon pairs, and in 86% at h=1.

- MACROCAST matches or surpasses Chronos-2, the strongest available TSFM, and substantially outperforms both BVAR and DFM benchmarks—all without exploiting privileged information.

- Median RMSFE ratios for MACROCAST are <1 at almost every horizon and group, with especially robust gains for headline labor market and housing indicators.

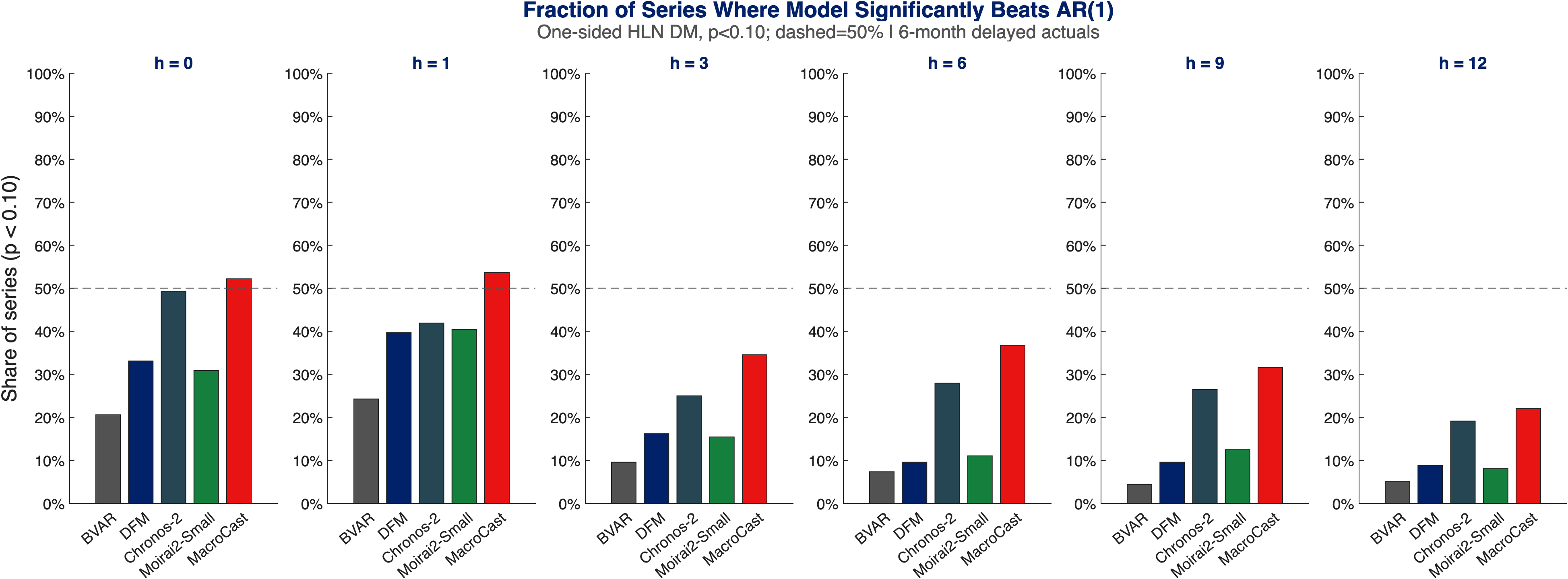

- Statistical significance (majority-vote DM test at p<0.10) is attained by MACROCAST for the majority of series at the shortest horizons.

Figure 1: Share of series where each model achieves a lower RMSFE than AR(1) across forecast horizons; MACROCAST leads at nearly all horizons, decisively beating the benchmark for most series.

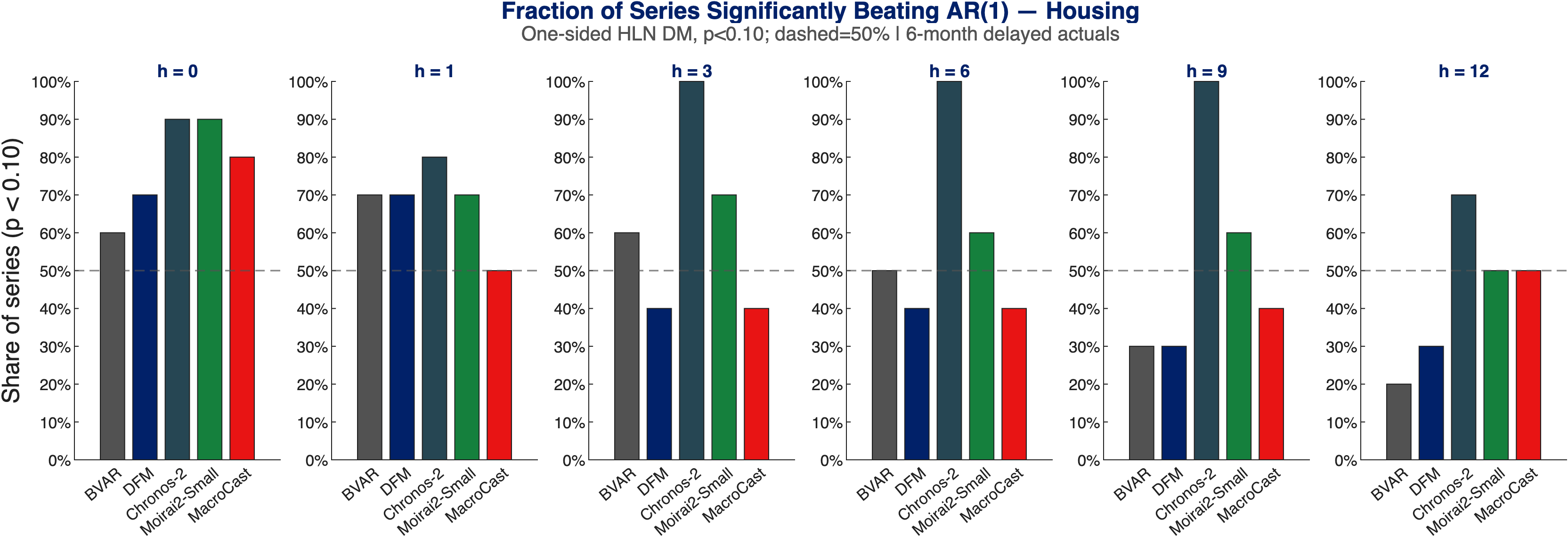

Figure 2: Share of series where the model’s performance over AR(1) is statistically significant, indicating the reliability of observed gains.

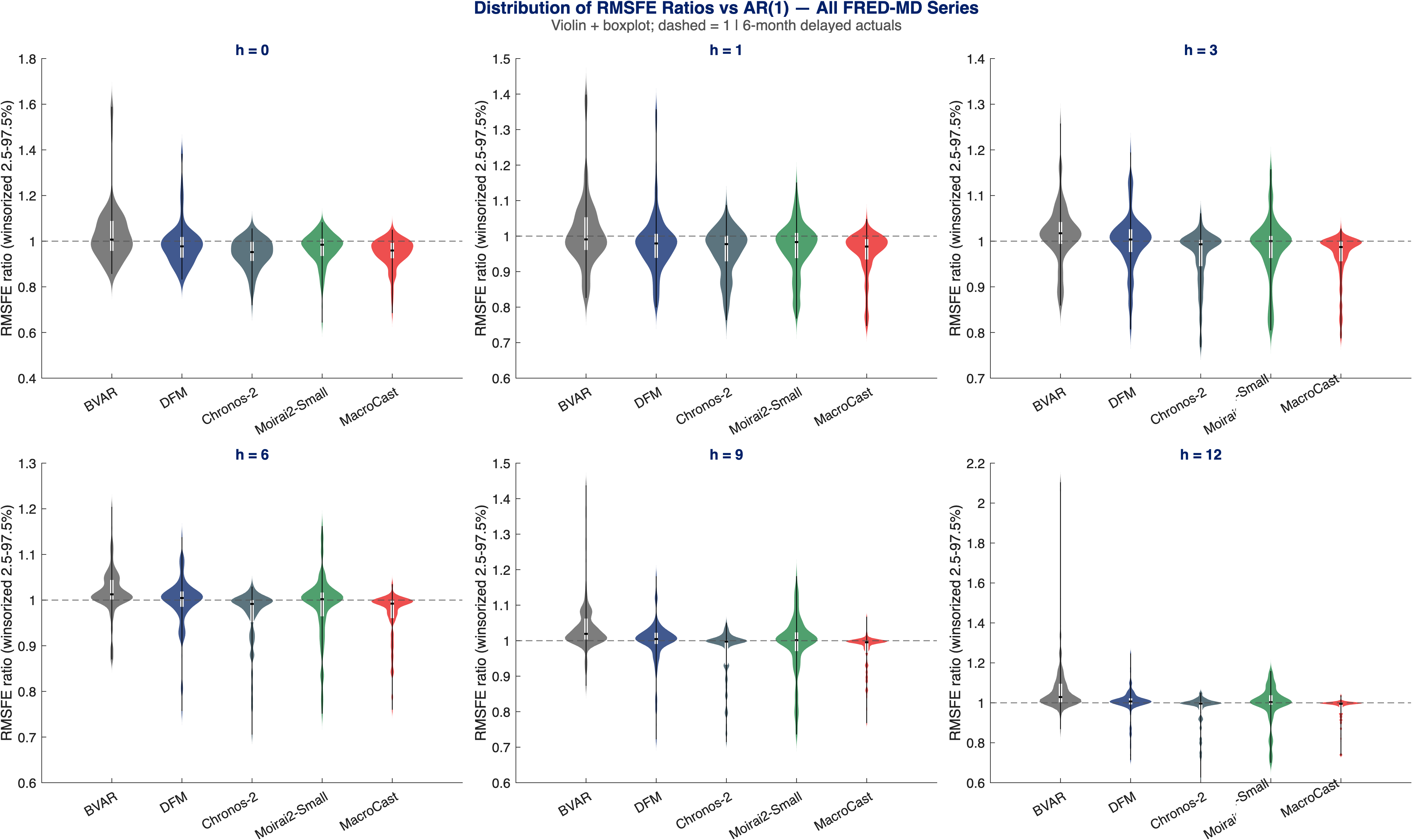

The cross-sectional distribution of RMSFE ratios (Figure 3) illustrates that MACROCAST's improvements are not driven by a small set of outliers but are broadly distributed and stable, with minimal right-tail risk.

Figure 3: Distribution of RMSFE ratios (relative to AR(1)) across 123 series at several horizons; MACROCAST demonstrates tight concentration below unity, evidencing reliable, moderate improvements for most series.

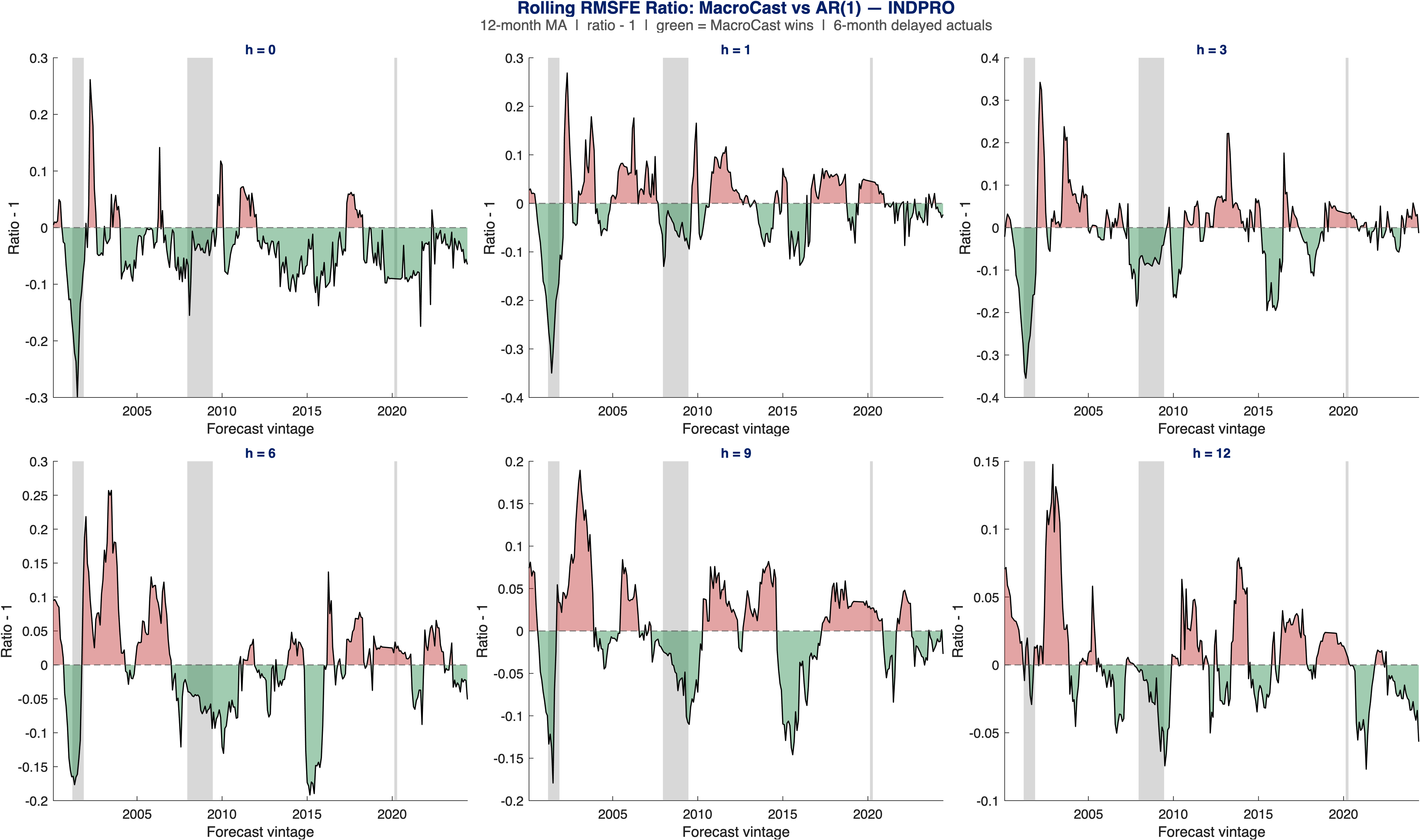

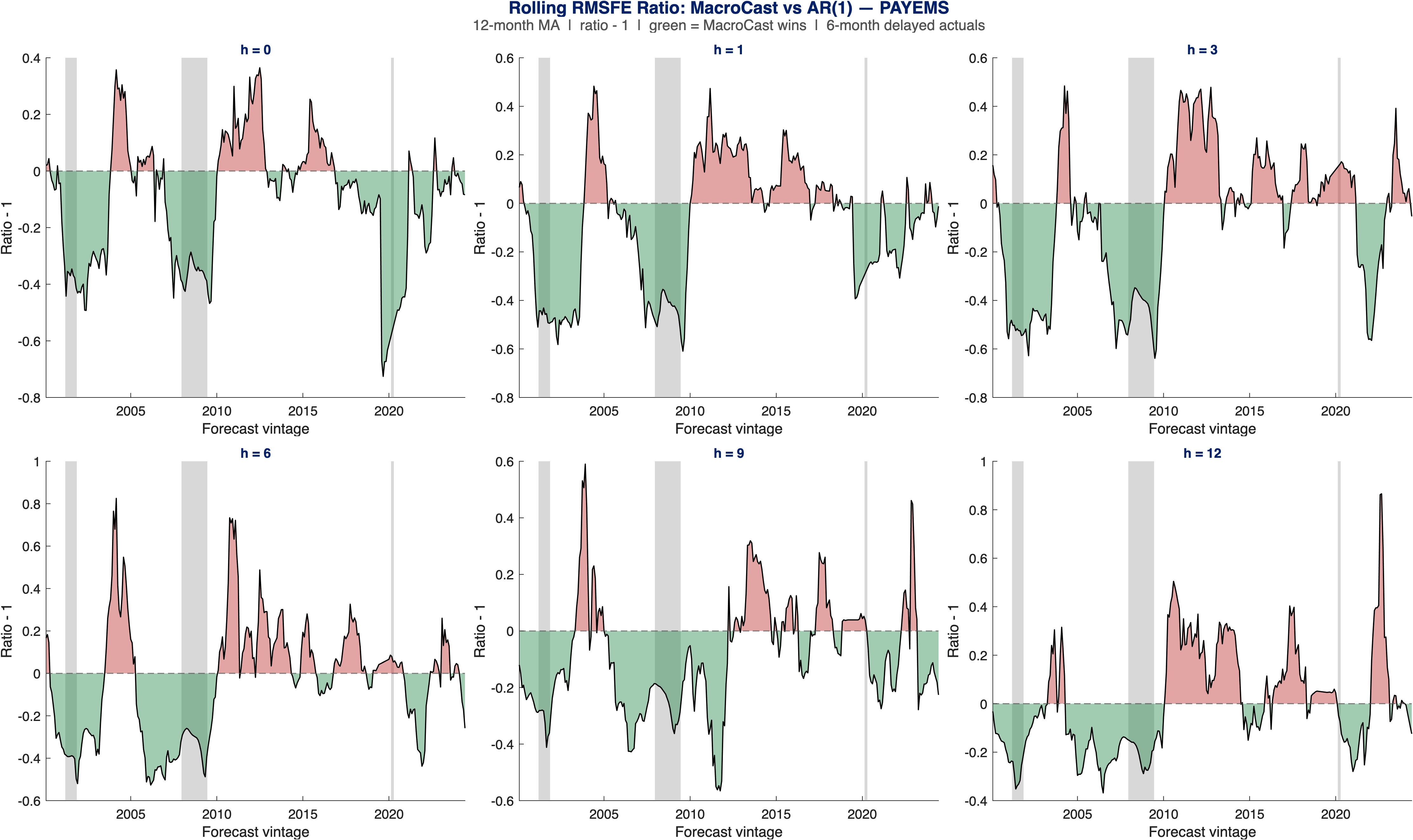

For several benchmark series (e.g., PAYEMS, INDPRO, FEDFUNDS, CUMFNS, UNRATE), MACROCAST's rolling 12-month performance is competitive throughout the business cycle. Notably, it exhibits resilience at turning points—especially during the GFC and COVID-19 episodes—where traditional autoregressive methods often falter.

Figure 4: Rolling 12-month RMSFE for INDPRO vs AR(1); MACROCAST maintains or exceeds benchmark performance at all horizons across macro-financial regimes.

Figure 5: Rolling RMSFE for nonfarm payroll employment, with MACROCAST consistently outperforming AR(1), especially during periods of volatility.

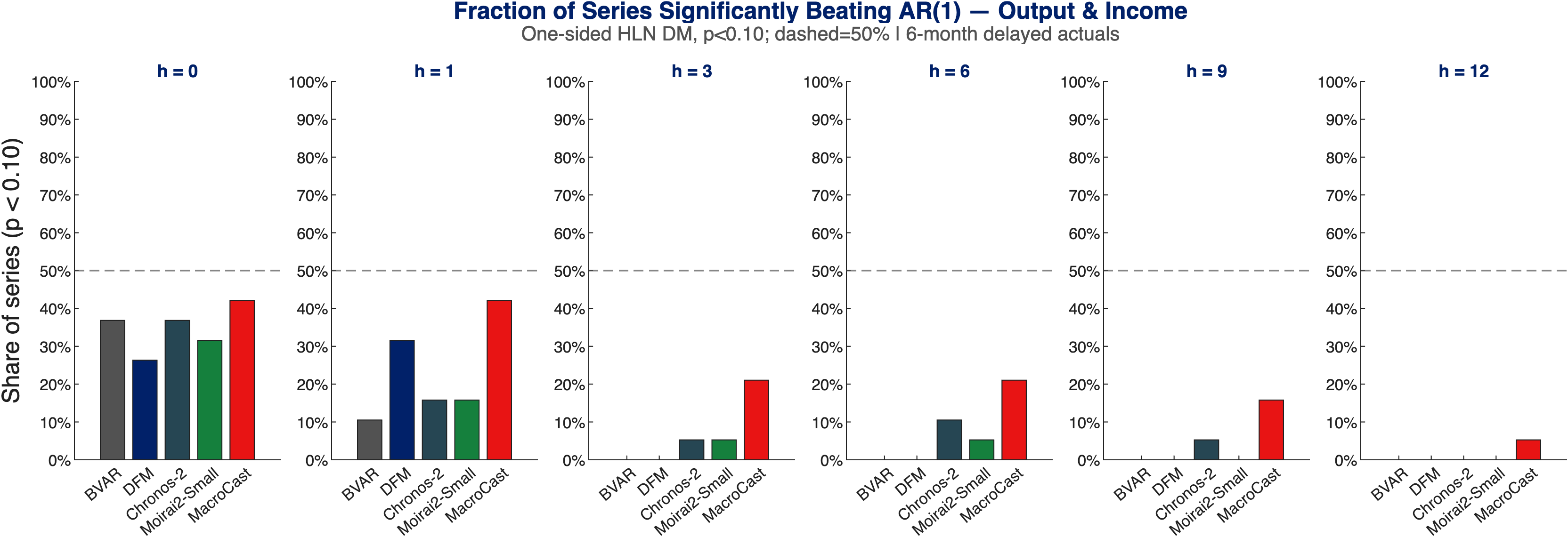

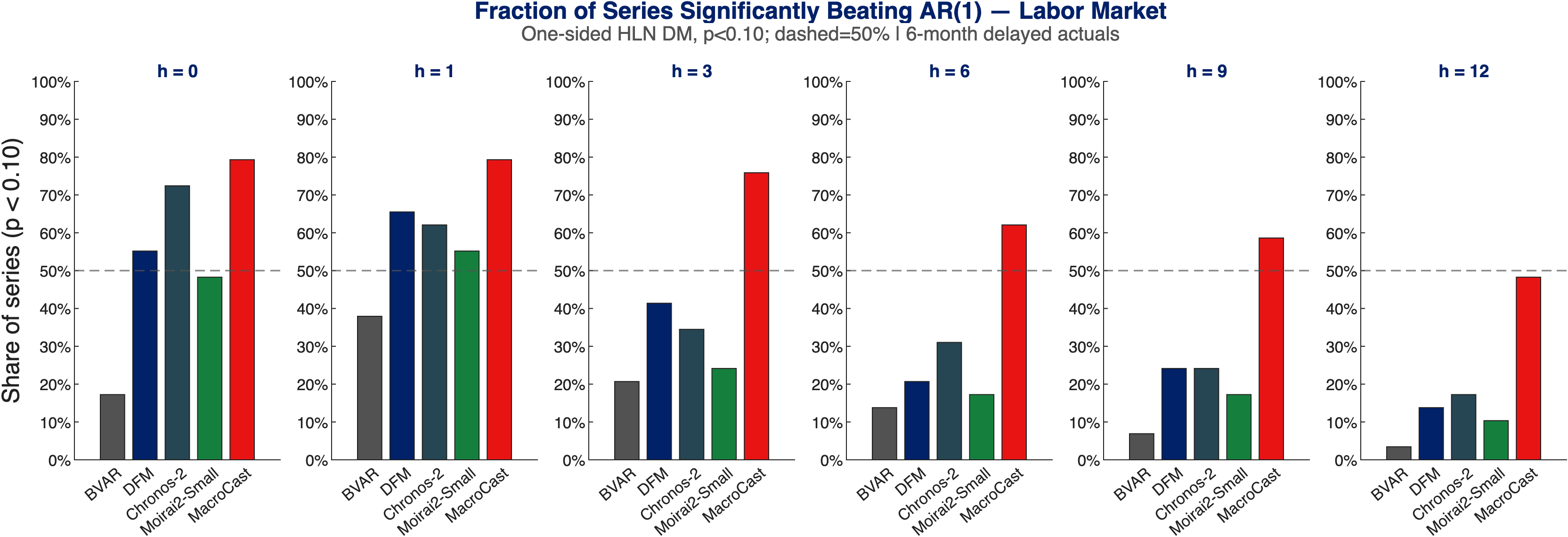

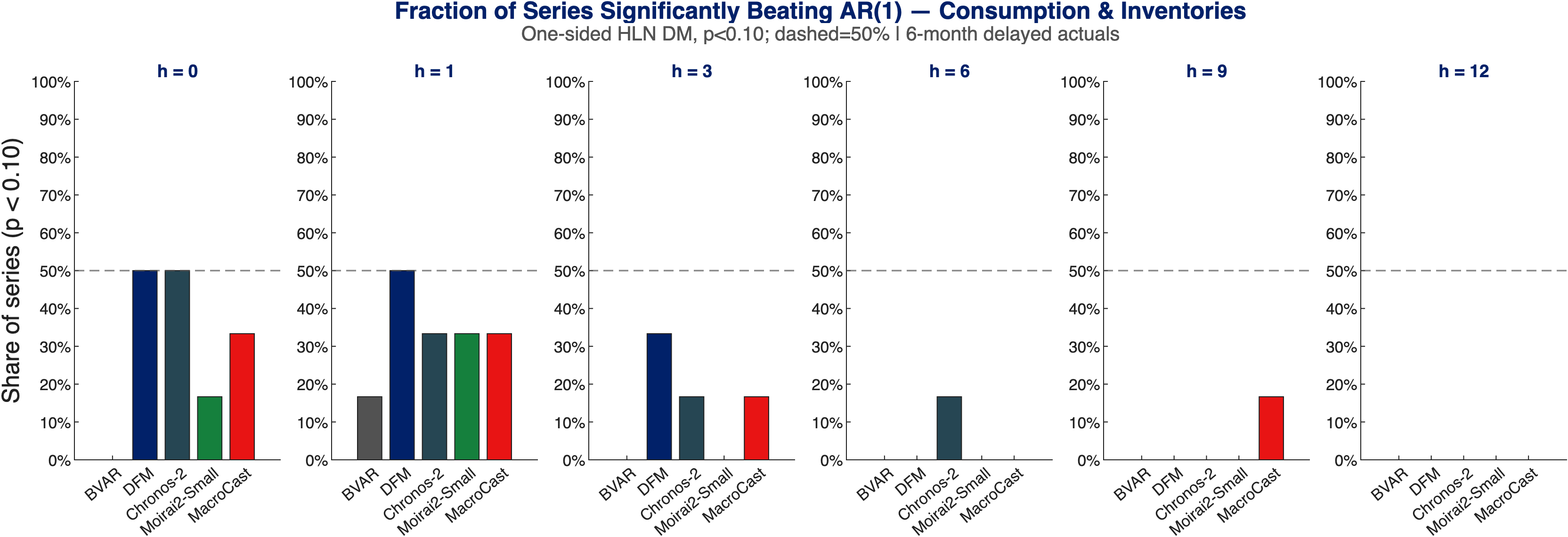

Disaggregated Analysis by Economic Sector

A sectoral breakdown shows that MACROCAST's dominance generalizes across all major macroeconomic aggregates. Its advantages are most pronounced in labor markets and housing, where nonstationarities and structural breaks challenge both simple and shrinkage-based benchmarks.

Figure 6: Fraction of series significantly beating AR(1) by FRED-MD group, demonstrating MACROCAST’s broad-based effectiveness, particularly in labor, housing, and interest-rate domains.

These results are robust to the inclusion/exclusion of outlier-pandemic periods and persist across horizon lengths up to 12 months.

Practical and Theoretical Implications

MACROCAST's vintage-consistent protocol sets a new baseline for macroeconomic forecasting with TSFMs by ensuring the model is both temporally and revision-fair. This architecture and training regime enable realistic rolling forecast exercises and facilitate continuous updating as new vintages are released. The low computational footprint (9 minutes per fine-tune) makes it deployable in resource-constrained academic and policy settings where large-scale transformer fine-tuning is infeasible.

Theoretical implications are equally significant. By synthesizing econometric structure (DFM, BVAR, ARIMA) and deep sequential learning within a leakage-controlled regime, MACROCAST demonstrates that domain-specific knowledge can be effectively integrated into modern neural timeseries frameworks without abandonment of inductive transfer. The design aligns with recent findings that naïve zero-shot TSFM adaptation to macrodata often under-delivers due to misspecified inductive biases.

Directions for Future Research

- Integration of Nowcasting/Mixed-Frequency Data: Extending the approach to mixed-frequency/real-time flow of data and soft indicators.

- Scenario/Counterfactual Analysis: Leveraging MACROCAST’s probabilistic outputs for shock decomposition or macro policy simulation.

- Structural Interpretability: Enhancing interpretability of RNN latent states through post-hoc mapping to macroeconomic factors.

- Cross-Jurisdiction Generalization: Assessing performance and retrainability in non-US macroeconomic domains with higher revision frequency or less stable institutional publication schedules.

Conclusion

MACROCAST establishes a rigorously leakage-free protocol for deploying TSFMs in real-time macroeconomic forecasting. By leveraging a compact and efficient recurrent architecture with synthetic and econometric-inspired fine-tuning solely on vintage data, it achieves forecast accuracy on par with, or superior to, the strongest existing TSFMs and traditional Bayesian benchmarks. Its design facilitates fast, frequent retraining as data vintages accumulate, making it highly scalable and reliable for operational policy environments. The leakage-tight pipeline made explicit in MACROCAST is likely to become a new standard for principled real-time economic forecasting with foundation models.