- The paper introduces a Stackelberg-CVaR model that integrates explicit risk aversion in take-or-pay contracts and proves existence and uniqueness conditions for the equilibrium.

- The methodology employs closed-form characterizations and finite candidate maximizations to efficiently solve the bilevel nonconvex pricing and capacity decision problem.

- The quantitative analysis shows that increased firm risk aversion reduces resource commitments and optimal investments while enhancing profit guarantees under uncertainty.

Stackelberg Equilibria for Risk-Aware Take-or-Pay Infrastructure Contracts

The paper "Shared Infrastructure Investment and Pricing: Stackelberg Equilibria in Risk-Aware Take-or-Pay Contracts" (2606.12167) addresses the challenge of incentivizing efficient deployment and pricing of costly shared infrastructure whose utilization and revenue depend on future stochastic firm demand. The setting is modeled as a Stackelberg game: an infrastructure provider (InP) acts as leader by deciding on infrastructure capacity and access pricing ex ante, before future utilization is realized, while multiple firms—heterogeneous in revenue and risk aversion—choose their resource commitments under take-or-pay contracts.

The critical innovation is the explicit incorporation of conditional value-at-risk (CVaR) to model follower risk preferences. CVaR captures heterogeneity and focuses resource selection on downside-tail profit risk in the presence of uncertain future revenues, congestion from resource sharing, and firm-specific operational costs. Each follower's strategic choice thus solves a mean-profit-minus-CVaR optimization, and the strategic interactions form a generalized Nash equilibrium (GNE) due to shared capacity constraints and congestion. The joint leader-follower system forms a bilevel (Stackelberg) problem with nonconvex dependence on leader actions through the anticipation of these follower responses.

The analysis derives three central theoretical results: (1) a sufficient condition for the existence and uniqueness of the GNE among risk-averse, interacting firms for any fixed leader decision; (2) the existence of a Stackelberg equilibrium (SE) in which the leader's optimal choice of capacity and price anticipates followers' unique GNE; and (3) a lower bound on each firm's realized probability of positive profit (PoP) at equilibrium, directly relating realized profit probabilities to model parameters and the CVaR confidence levels.

Stackelberg Solution Algorithm and Structural Properties

The solution procedure leverages analytic structure to efficiently compute an approximate SE with bounded suboptimality gap. Explicitly, the follower subgame is shown to admit a closed-form characterizing equation for each firm's optimal resource commitment in terms of its own CVaR, the access price, the operational and congestion costs, and the overall capacity constraint. These equations are monotone and can be solved by scalar root-finding (bisection).

The upper-level (InP) problem is non-convex but, because only finitely many regime-changing breakpoints appear due to the structure of capacity constraints and take-or-pay contracts, optimal price and capacity selection reduces to a finite set of candidate maximizations.

A key theoretical contribution is the establishment of a sufficient uniqueness condition on the curvature of operational and congestion costs (in terms of the ratio δ/γ for quadratic costs) so that for any leader actions, the GNE among followers is unique, ensuring well-defined best-response maps for the Stackelberg analysis.

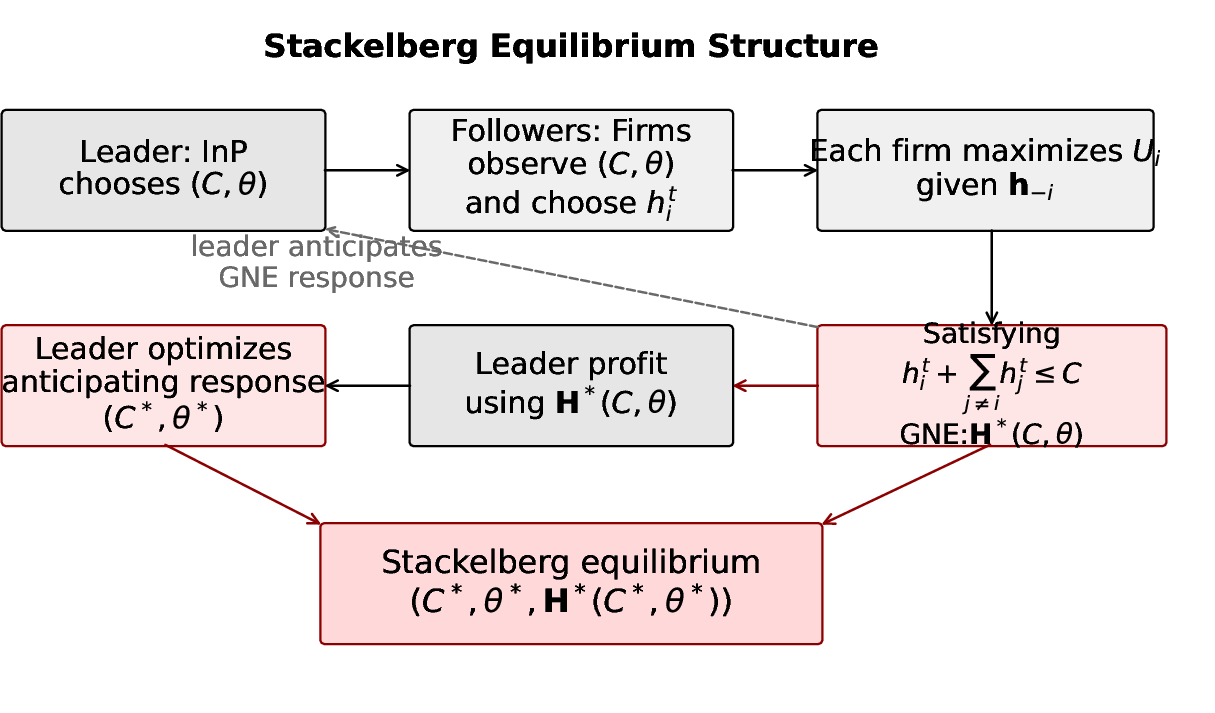

The solution structure and equilibrium sequence are illustrated in the decision diagram below:

Figure 1: Sequential structure of the proposed Stackelberg game.

Quantitative Analysis: Dependence on Risk, Uncertainty, and Market Size

The paper performs an extensive set of Monte Carlo simulations in a case study motivated by Mobile Edge Computing (MEC), using real-world cost parameters and market sizes of up to 10 heterogeneous firms (service providers, or SPs).

A principal numerical finding is that the propagation of follower (firm) risk aversion upstream through the Stackelberg structure fundamentally alters the InP's optimal investment and pricing decisions:

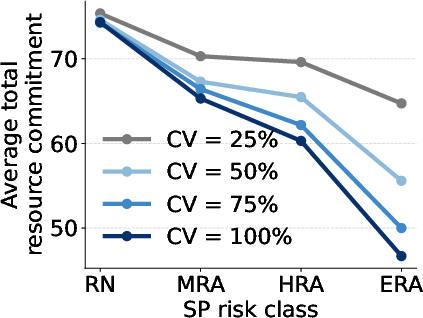

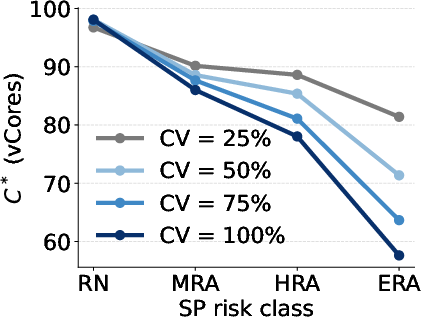

- Risk aversion sharply reduces resource commitments and capacity investment: As aggregate SP risk aversion increases (as measured by the risk-penalty coefficient βi and CVaR confidence level αi), both total committed resources and system-wide capacity fall rapidly.

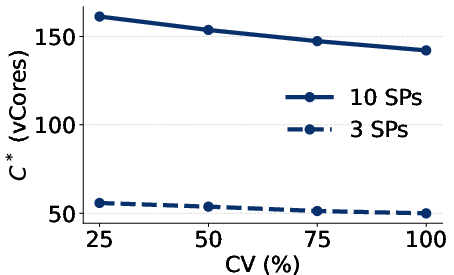

Figure 2: Total resource commitment under different risk classes and CVs.

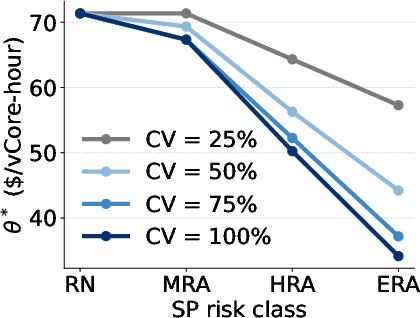

- Pricing adapts jointly to risk and utilization: The equilibrium access price declines with risk aversion, but may increase in response to higher operational or congestion costs.

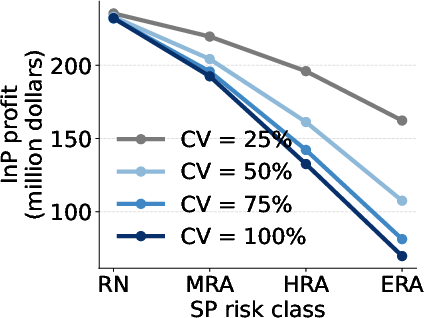

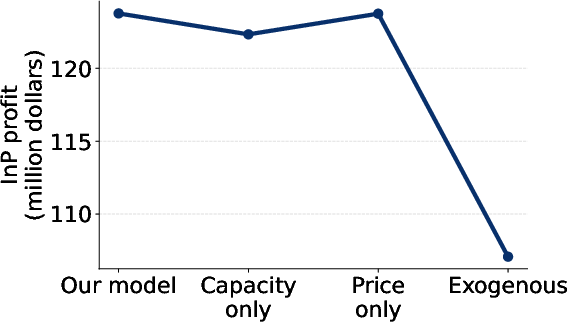

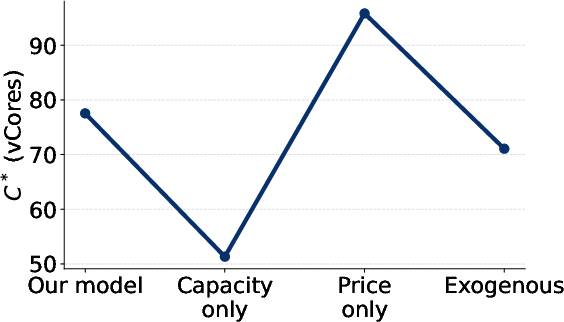

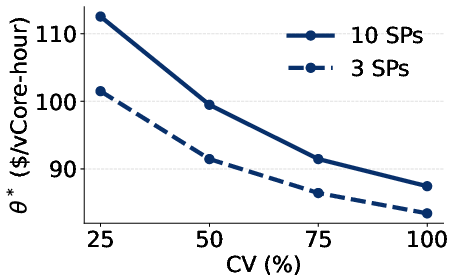

- InP profit and capacity utilization decline with firm risk aversion: High follower risk aversion lowers InP profit, especially at high revenue uncertainty, as seen in the following:

Figure 3: InP profit under different risk parameterizations and uncertainty.

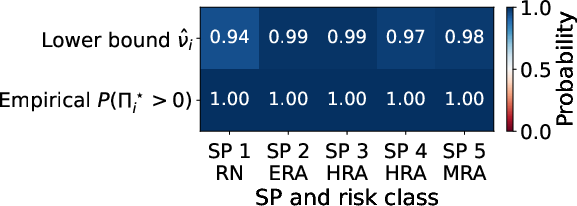

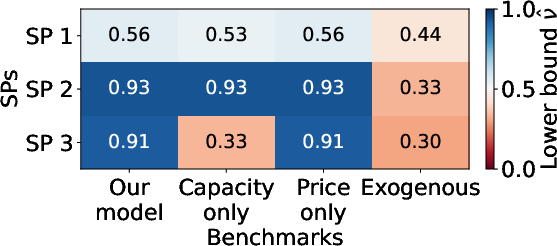

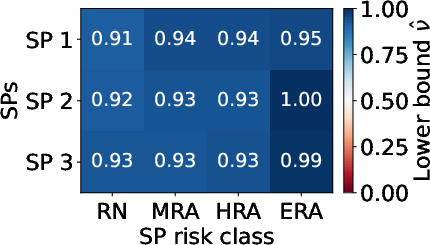

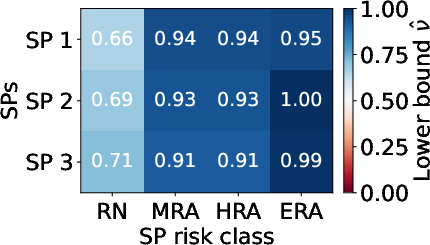

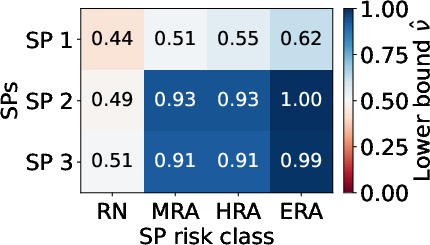

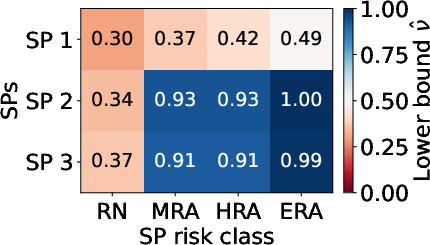

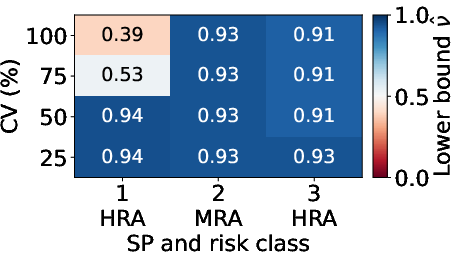

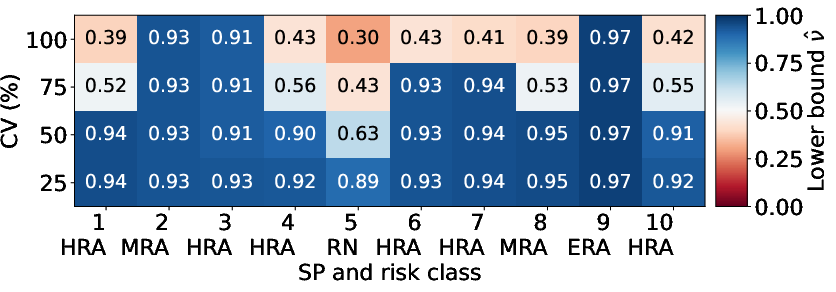

- Theoretical guarantees on firm profitability (PoP) rise with risk aversion: The global lower bound on the probability of a firm achieving positive profit—the CVaR-driven guarantee—is strictly increased as risk aversion grows. Notably, the bound becomes tightest for the most risk-averse agents, while for risk-neutral followers it is weakest, especially under high uncertainty.

Figure 4: Lower bound on the PoP ν^i under different risk classes and CVs.

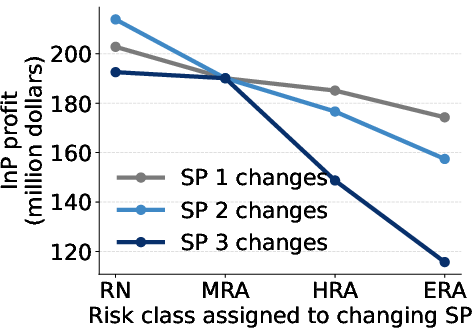

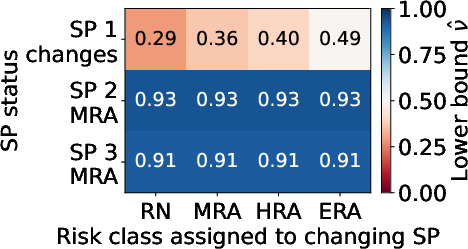

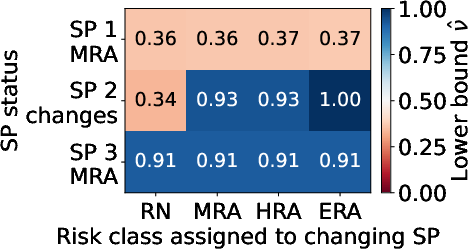

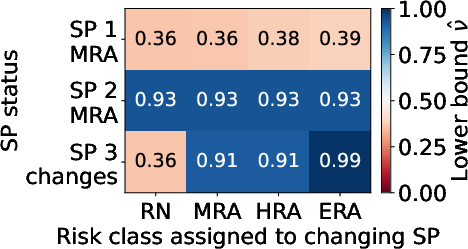

- Individual risk attitude and market share shape equilibrium impacts: Changing the risk class of a single large SP has a disproportionate effect on InP profit and overall utilization compared to smaller SPs:

Figure 5: InP profit when one SP changes risk class at CV=100%.

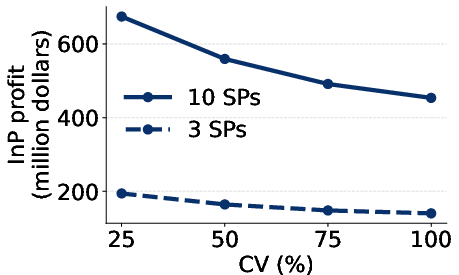

- Scalability and qualitative robustness: Scaling up to 10 SPs preserves the qualitative equilibrium patterns—aggregate resource commitments and prices increase, but the lower bound on PoP remains primarily controlled by the individual SP’s own risk preference and revenue size.

Figure 6: InP profit, capacity, and price for 3 and 10 SPs as revenue uncertainty varies.

Figure 7: Lower bound on the PoP for 3 and 10 SPs under heterogeneous risk classes and varying CV.

Risk Measures and Profit Guarantees

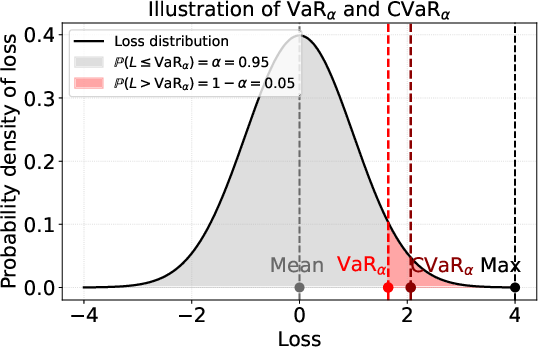

A unique feature of this formulation is the rigorous ex-ante guarantee on realized firm profitability that arises from the incorporation of CVaR in the equilibrium definition. The bound is twofold: one component is a function of the mean-variance relationship of ex-post profit, while the other, arising from CVaR calibration, allows followers to explicitly demand a minimal probability of positive profit by choosing sufficiently high αi, as shown in the schematic below.

Figure 9: Illustration of VaRα and CVaRα for a loss random variable L.

Tightness of Guarantees

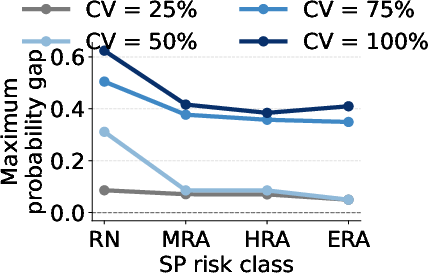

The gap between the realized empirical PoP and the theoretical lower bound ν^i is largest in high-uncertainty, risk-neutral cases—where agents do not hedge against tail losses—but shrinks substantially for risk-averse agents, confirming robustness.

Figure 10: Maximum gap across SPs between the empirical PoP and the theoretical lower bound on the PoP.

Practical and Theoretical Implications

This Stackelberg-CVaR contract model has significant consequences for the structuring of infrastructure investments and contract offerings in settings with demand uncertainty and heterogeneous, strategic firms.

- Practical contract design: Take-or-pay contracts with explicit CVaR clauses offer both the infrastructure provider and the firms ex-ante clarity on exposure to downside revenue risk, and enable tailoring of capacity and pricing to the risk tolerance of firm cohorts.

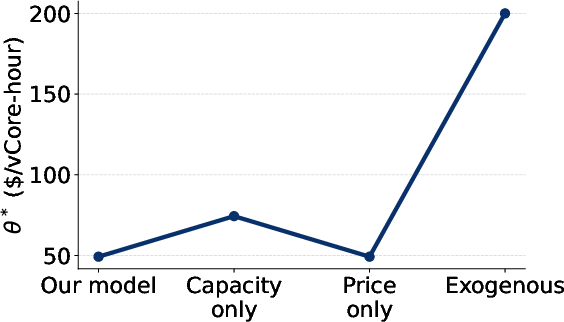

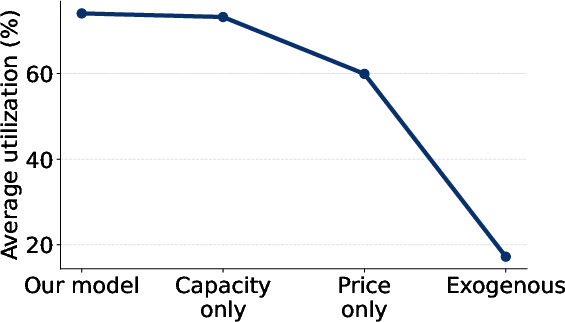

- Strategically-aware infrastructure deployment: Ignoring follower risk aversion or stochastic variation results in systematic over-investment, higher system idle capacity, and weaker realized profit guarantees to firms, potentially discouraging infrastructure adoption and impeding technology-scale rollouts.

- Computational tractability: The proposed polynomial-time algorithm, with monotonicity properties and explicit regime regime-decomposable candidate structures, yields efficiently computable equilibria even at large scale, supporting application to multi-firm industrial or digital infrastructure scenarios.

Future Directions

The present framework opens several avenues for further exploration:

- Endogenization of competition among multiple infrastructure providers: Multi-leader Stackelberg formulations, possibly with horizontal or vertical differentiation, can be developed using similar CVaR-based equilibrium refinement techniques.

- Dynamic and multistage investment: While the current analysis treats a static horizon, extending to stochastic dynamic games with investment, expansion, or contract renegotiation offers clear applicability (e.g., sequential MEC rollouts or EV charger buildouts).

- Integration with learning and reinforcement learning paradigms: As demand or revenue processes may be partially observable or nonstationary, combining equilibrium computation with online estimation or exploration is a promising direction for practical AI-enabled infrastructure management.

Conclusion

The paper rigorously formulates and analyzes infrastructure investment and pricing under Coupled Stackelberg-CVaR contracts, providing novel theoretical and computational guarantees for profit probability in risk-aware contracting games. The practical analysis reveals that optimal capacity and pricing decisions must internalize risk propagation from strategic firms to cost recovery, and that CVaR-driven contracts enable robust, efficient cost-sharing and capacity allocation in the presence of revenue uncertainty and heterogeneous attitudes toward risk (2606.12167).