- The paper introduces the annualized settlement wedge (ASW) to measure how locked-up capital and delayed settlements discount near-certain contracts.

- It employs empirical analysis to extract ASW term structures and demonstrates that design features like yield-bearing collateral compress these discounts.

- The findings challenge reading raw prediction market prices as unbiased probabilities, advocating for maturity-conditioned calibration in forecast evaluation.

Measurable Settlement Discounting in Collateralized Prediction Markets

Overview

The paper "When Certainty Is Not Worth It: Capital Lock-Up and Settlement Discounting in Prediction Markets" (2605.31431) provides a rigorous empirical and theoretical investigation of how capital lock-up and delayed settlement systematically induce a measurable discount in pricing on collateralized prediction markets (PMs), with direct implications for price calibration, forecast evaluation, and market design. The central thesis is that observed prices in these venues correspond not to frictionless probabilities, but rather to discounted expected payoffs where the discount reflects required compensation for delayed settlement, opportunity cost of capital, liquidity needs, and residual platform or oracle risk. The authors introduce the notion of an annualized settlement wedge (ASW) to quantify this factor, extract its term structure from persistent near-certainty PM contracts, and analyze how protocol architectures—namely, conversion and yield-bearing collateral—compress or reshape this wedge.

Capital Lock-Up and Pricing Frictions

Collateralized oracle-settled PMs operate through mechanisms where trading an outcome-conditional claim (such as a YES/NO token) requires locking up collateral until the event is resolved and the outcome is finalized via an oracle. The timeline of an event comprises both the economic resolution of uncertainty and the formal settlement/redeemability interval, with the latter often extended due to dispute windows, delayed oracle calls, or platform-specific processes. During the period when the outcome is essentially known but cannot be redeemed, the holder forgoes outside returns, incurs liquidity cost, faces residual nonzero platform/oracle risk, and must wait for capital redeployment.

Within this context, the price Pi,t for a contract i with settlement payoff Xi∈{0,1} and remaining time to settlement τi,t, satisfies: Pi,t=Et[Xi]D(τi,t),

where D(τ)≤1 captures the settlement discount, operational, opportunity, and risk cost components. The observed price, for a near-certain contract at horizon τ, will fall below the [0,1] benchmark, and the wedge will be more pronounced for longer horizons.

Empirical Recovery of the Settlement Discount

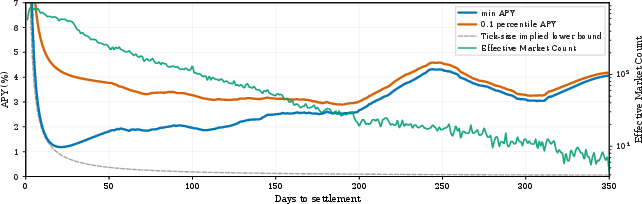

The authors construct a stringent upper-tail sample of PM contracts where one side remains highly priced (≥0.9) for at least seven consecutive days, filtering out reversals to minimize residual uncertainty. Via this approach, they estimate the near-certainty price frontier and convert it to an annualized settlement wedge (ASW):

Figure 1: Frontier-implied ASW by time to settlement. ASW is a reduced-form required return on locked PM capital; the term structure is positive, maturity-dependent, and exceeds the tick-size lower bound even at short horizons.

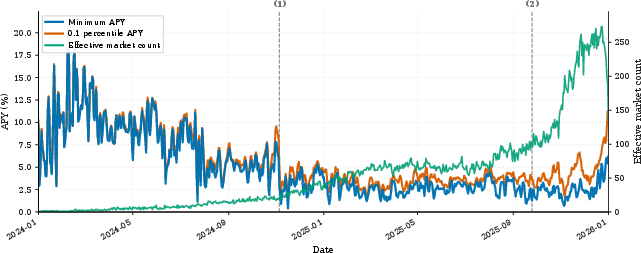

Time-series analysis of the lower-tail frontier demonstrates that the ASW is time-varying, with periods of capital scarcity producing higher lower-tail ASW and platform interventions (such as yield support) producing compression.

Figure 2: Time-series evolution of lower-tail frontier-implied ASWs, with concurrent effective market support highlighting capital supply and participation changes.

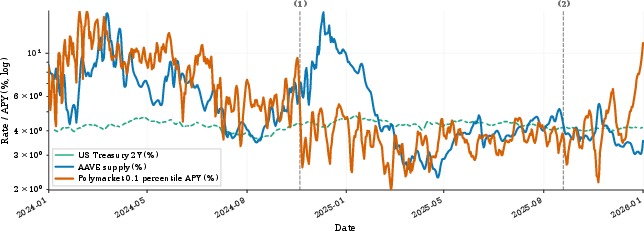

Comparison against external benchmarks (AAVE variable supply rates and US Treasury yields) reveals only modest and context-dependent co-movement, supporting the assertion that PM settlement risk is driven more by platform- and design-specific frictions than by external risk-free rates.

Figure 3: Comparison of external yield benchmarks with Polymarket’s lower-tail ASW; demonstrates regime-specific correlations and distinct attribution relative to DeFi and Treasury rates.

Effect on Price Calibration and Forecast Evaluation

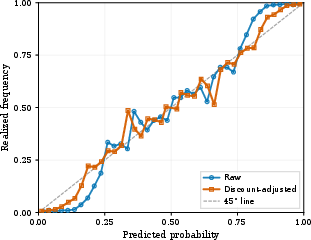

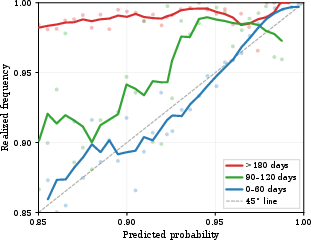

Raw forecast calibration in PMs—comparing quoted price to realized frequency—exhibits a pronounced horizon-dependent underconfidence: longer-horizon near-certainty contracts trade increasingly below their eventual payoff due to the settlement wedge rather than pure misperception of probability. The authors implement discount adjustment using the empirically estimated D^(τ) curves, which significantly attenuates the horizon gradient in price-realization mismatch (by 48–88%, depending on the percentile frontier used), with the effect robust to event-level cross-fitting.

Figure 4: Raw and discount-adjusted reliability for contracts with settlement horizons above 180 days. After discount adjustment, reliability aligns more closely with the diagonal.

Regression analysis quantifies the attenuation in the horizon coefficient, verifying that adjustment using the empirical frontier shrinks the long-horizon "miscalibration" to statistical insignificance under the most conservative discount estimates.

Further, graphical analyses (see Appendix) visually confirm the convergence of adjusted price wedges toward zero gradient across maturities.

Market Architecture, Capital Efficiency, and Comparative Statics

NegRisk Conversion

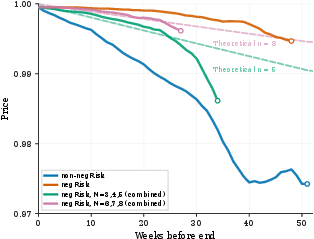

An explicit design lever, the "negRisk" adapter, allows bundled conversion of mutually exclusive NO legs of a multi-outcome contract into economically equivalent cash and a residual YES exposure. This architecture splits the settlement wedge across the NO basket, thus compressing the per-contract discount by a factor determined by the number of outcomes.

Figure 5: Empirical 99.9th-percentile price frontier by weeks before end; negRisk (with higher n) events adhere closely to model-implied support lines, confirming effective mechanical reduction of the settlement wedge.

Yield-Bearing Collateral

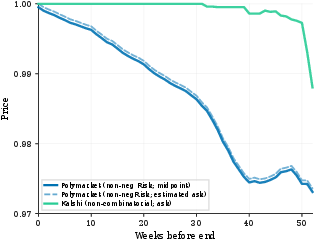

Platforms that compensate open positions with yield (e.g., Kalshi, or Polymarket’s targeted reward program) exhibit a notably flatter ASW term structure, as the opportunity cost for waiting is directly offset.

Figure 6: Empirical 99.9th-percentile price frontier by weeks before end; Kalshi's yield-bearing design shows less deviation from par than Polymarket for comparable horizons.

The cross-platform comparison, while not a causal effect estimate due to platform compositional differences, supports the theoretical mechanism: capital-efficiency and yield-bearing design features materially shape both the settlement wedge and the information quality of quoted prices.

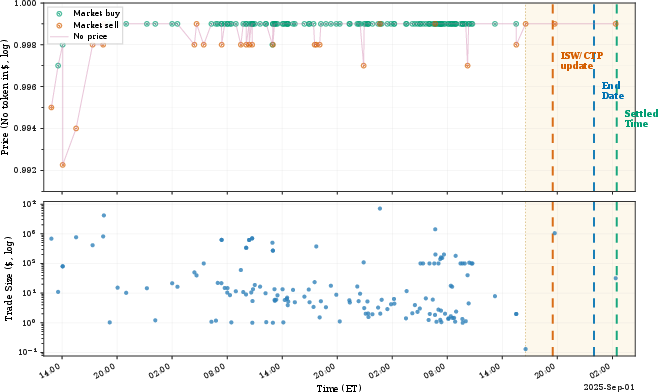

Trading Implications and Liquidity Provision

Short-horizon, post-event settlement delays create opportunities for liquidity providers to earn nontrivial annualized carry by absorbing the last-mile latency; these trades, while low-risk, are capital and operations intensive. Actor-level analysis demonstrates profit concentration among a handful of top liquidity providers exploiting this wedge via aggressive post-event bidding.

Theoretical and Practical Implications

The results refute the practice of directly reading PM prices as unbiased probabilities on collateral-locked, delayed-settlement venues. The settlement wedge arises endogenously from market design and platform architecture; price deviations from frequencies at long horizons primarily reflect financial friction, not informational inefficiency. Consequently, cross-platform forecast comparison, efficiency evaluation, and market intervention should explicitly separate pure information aggregation from funding and settlement frictions.

Market design features that improve capital mobility—such as conversion and yield-bearing mechanisms—lead to systematically more reliable prices by minimizing the wedge. Conversely, targeted support mechanisms can have unintended consequences if not carefully aligned with the structure of capital lock-up across the platform.

Conclusion

The paper establishes that prediction market prices in collateralized, delayed-settlement platforms are discounted probabilities—systematically reflecting the cost of delayed redemption, capital inefficiency, and market microstructure. The measurable annualized settlement wedge explains most of the horizon-dependent calibration patterns previously attributed to miscalibration or behavioral bias, and its magnitude and structure are directly manipulable by protocol design choices. These insights warrant a recalibration of forecast interpretation in PMs, demanding maturity-conditioned calibration and emphasizing capital efficiency as a primary route for pricing improvement.

Reference:

"When Certainty Is Not Worth It: Capital Lock-Up and Settlement Discounting in Prediction Markets" (2605.31431).