Distributionally Robust Games via Coherent Risk Measures

Published 19 May 2026 in cs.GT | (2605.19302v1)

Abstract: We study strategic interaction in data-driven games where players face uncertainty about payoff distributions inferred from finite samples. To model calibrated attitudes toward such uncertainty, we formulate distributionally robust games with a special focus on coherent utility (risk) measures, including Mean-semideviation and Conditional Value-at-Risk. This framework treats risk sensitivity as a primitive feature of player preferences while retaining a formal connection to distributional robustness. We make a number of contributions that are enumerated next. (1) We use prior results for the existence of distributionally robust equilibria to show the existence of equilibria in data-driven settings for various ambiguity sets, and (2) show that these games are inherently continuous, rather than finite matrix games, which fundamentally alters equilibrium structure and precludes direct extensions of standard correlated equilibrium notions. (3) We bound the loss in expected utility that a player can expect from being risk-averse. (4) We further characterize the computational complexity of equilibrium computation, proving PPAD-completeness in general and PPAD membership for several coherent utility measure games. (5) We present multilinear complementarity program formulations for several coherent utility measure games. (6) Numerical experiments reveal the robustness and out of sample performance of the game solutions. Our results unify risk-theoretic modeling and equilibrium analysis, providing a principled foundation for risk-aware strategic decision-making in data-driven environments.

The paper introduces a framework for distributionally robust games by incorporating coherent risk measures into players' strategic decision-making.

It shows that risk-adjusted utilities yield non-convex payoffs and PPAD-complete equilibrium computation under various ambiguity sets.

Experimental results indicate that increasing risk aversion improves out-of-sample performance and stabilizes equilibria in strategic settings.

Distributionally Robust Games with Coherent Risk Measures: Summary and Analysis

Introduction and Motivation

The paper "Distributionally Robust Games via Coherent Risk Measures" (2605.19302) introduces and analyzes a framework for modeling strategic interactions where players are uncertain about payoff distributions inferred from empirical data and explicitly encode risk sensitivities via coherent utility (risk) measures. This approach distinguishes itself from work on robust games that focus on worst-case design, and from prior distributionally robust games (DRGs) that employ ambiguity sets based on statistical distances or moments, by making the risk attitude a primitive of player preferences. Central to the framework are coherent risk measures such as mean-semideviation, mean-deviation, and Conditional Value-at-Risk (CVaR), which connect risk aversion to distributional robustness via their dual representation.

Theoretical Results: Structure, Existence, and Complexity

The work formalizes distributionally robust games as continuous games in the space of mixed strategies, with utilities evaluated under the worst-case distribution in a specified ambiguity set. It demonstrates, by leveraging duality properties of coherent risk measures, that games whose payoffs are evaluated using these measures—termed coherent utility measure games (CUMGs)—admit straightforward closed-form inner optimization for robust payoff evaluation.

A key structural finding is that DRGs, and thus CUMGs, are not finite matrix games—the risk-adjusted payoffs for mixed strategies are generally not convex combinations of pure-strategy payoffs, which invalidates standard correlated equilibrium definitions and restricts the direct application of classical techniques such as support enumeration and the Lemke-Howson algorithm. The paper provides conditions under which distributionally robust equilibria (DREs) exist in pure (lifted) continuous strategy spaces for general ambiguity sets, including Wasserstein and f-divergence balls as well as the coherent risk measure-induced ambiguity sets.

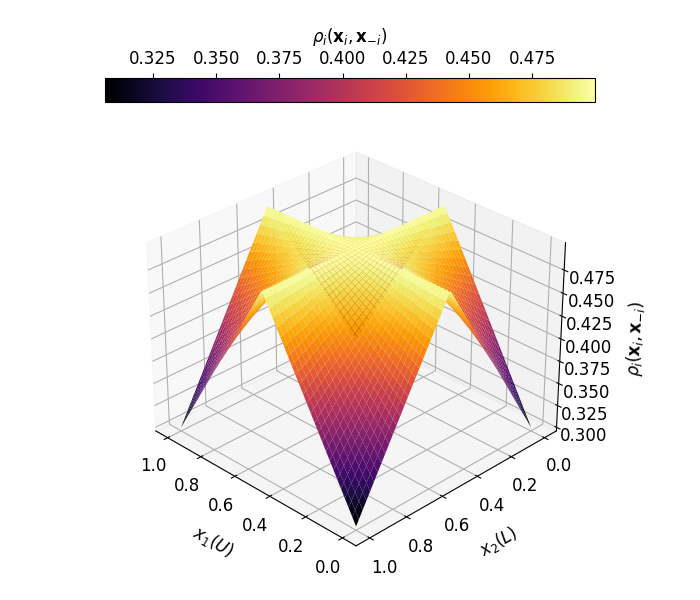

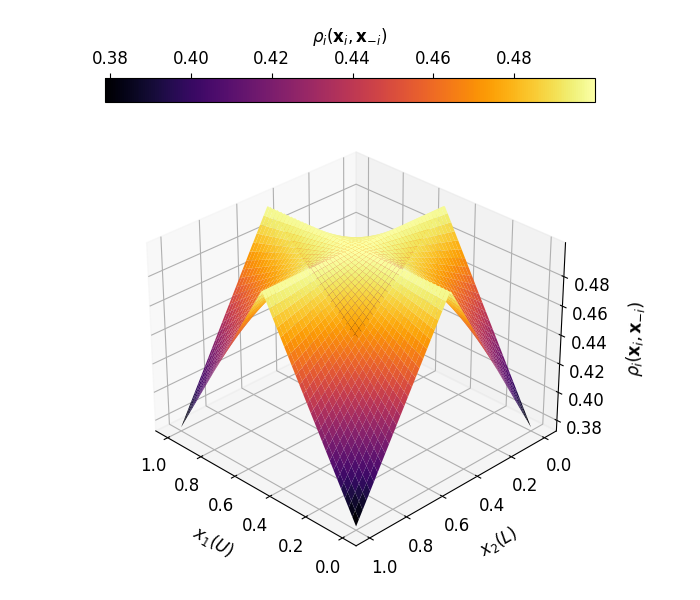

Figure 1: The payoff for DRG (left) and mean-semideviation game (right); the DRG payoff is non-convex over mixed strategies, mandating continuous-game machinery.

The authors prove that the worst-case expected utility for a mixed strategy dominates the convex combination of worst-case payoffs for pure strategies, exemplifying the fundamental departure from conventional finite games.

Regarding equilibrium computation, it is shown that finding approximate DREs is PPAD-complete in general, even for data-driven distributions, mirroring complexity barriers for Nash equilibria in matrix and concave games. For CUMGs with nontrivial ambiguity (i.e., risk aversion parameter γ>0), the paper proves that the equilibrium computation problem resides in PPAD, given the closed-form nature of the risk-adjusted utility functions and their Lipschitz continuity.

Risk Sensitivity, Utility Bounds, and Robustness Guarantees

A central contribution is the quantification of the price of risk aversion: the paper establishes explicit bounds on the shortfall in expected payoff for a risk-averse player relative to the empirical-optimal strategy, encapsulating the impact of the risk penalty and sample size K. For each coherent measure (mean-semideviation, mean-deviation, CVaR), these bounds involve sample-based deviations (MAD, empirical CVaR) and concentration terms scaling as O(1/K) plus a risk adjustment scaling with γ. In particular, the choice of the robustness parameter should decay as $1/K$ to ensure vanishing conservatism with increasing data, paralleling variance regularization regimes in single-agent robust optimization.

Algorithmic Formulation: Complementarity Programs

The authors derive multilinear complementarity program (MLCP) formulations characterizing equilibria in CUMGs, for which the risk-adjusted utility—involving maximum, absolute value, or CVaR inner terms—can be handled with auxiliary variables and the structure of the complementarity constraints. Unlike standard matrix games, these MLCPs are not reducible to linear complementarity, even in the two-player setting, thereby excluding algorithms such as Lemke-Howson.

Numerical Results: Robustness, Variance Reduction, and Calibration

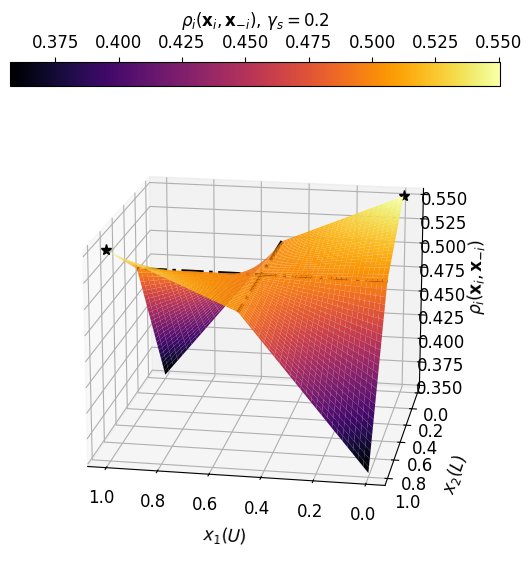

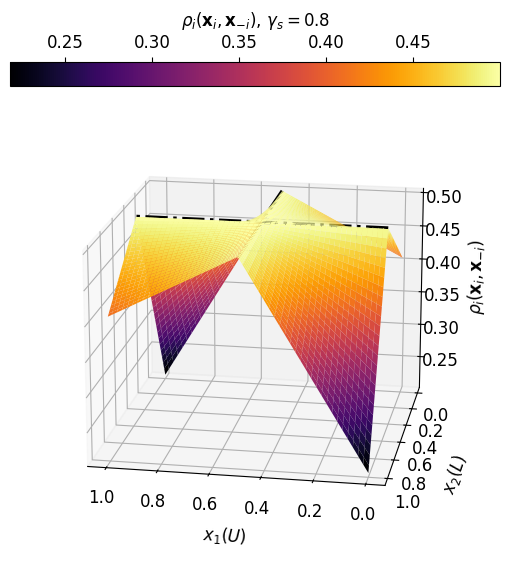

Experiments focus on how risk-aware equilibria differ from risk-neutral ones, especially in finite-sample settings, and demonstrate strength in out-of-sample (OOS) performance and robustness to payoff perturbations. In coordination games with an empirical distribution coming from large samples, increasing downside risk aversion shrinks and stabilizes the set of equilibria, making them less sensitive to data fluctuations.

Figure 2: MSD payoffs for the Coordination game with p^=0.6 and γs=0.2; the equilibrium set and payoff surface is smoothed by risk aversion.

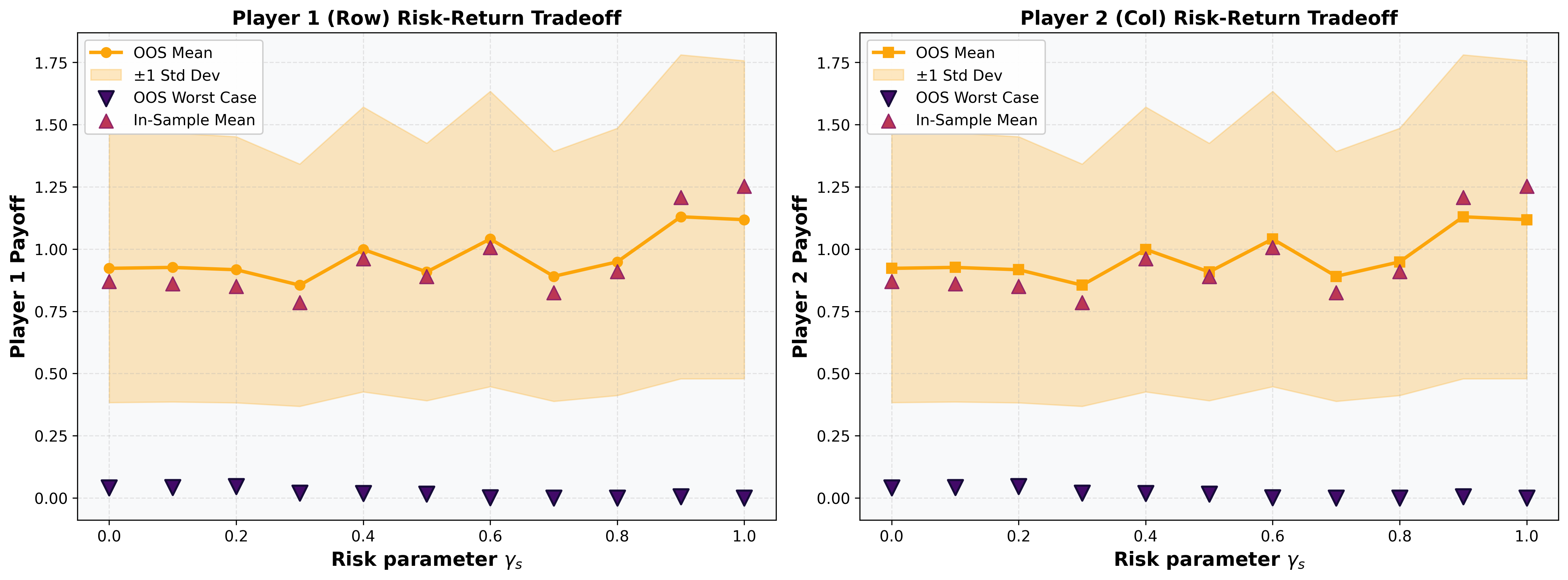

For low-sample (small-K) variants of Prisoner’s Dilemma, risk aversion delivers monotonic improvements in OOS performance and reduces variance, with the optimal degree depending on the particular risk penalty—non-monotonicities can arise due to structural changes in the equilibrium correspondence.

Figure 3: OOS-mean payoff ±1 s.d. in small-K Prisoner's Dilemma as a function of K0; risk-sensitivity yields higher OOS utility and lower spread.

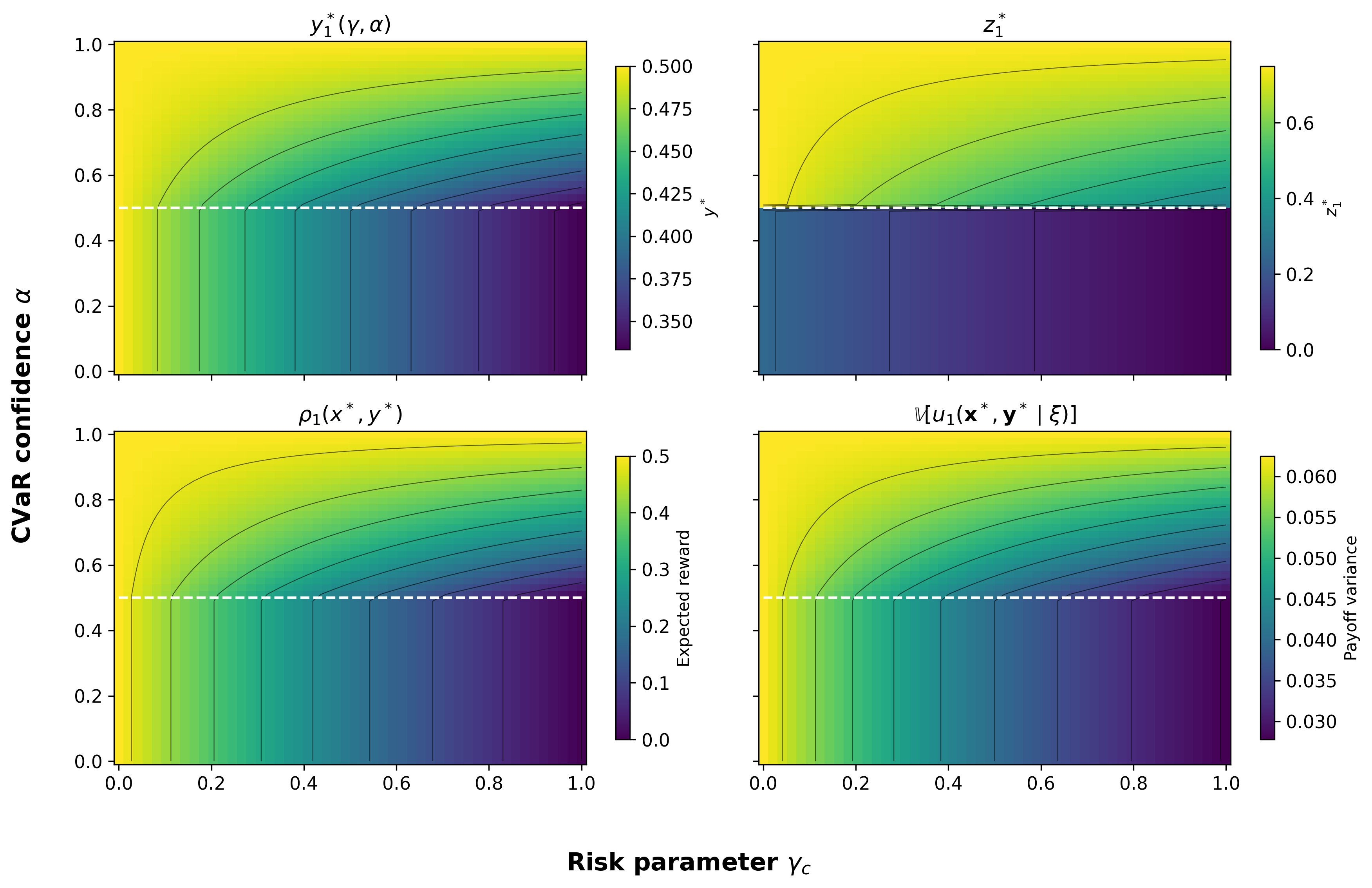

For CVaR games, one can calibrate tail-risk aversion and achieve explicit probabilistic guarantees on payoff quantiles (VaR), with tight control of the variance via the robustness parameter.

Figure 4: Player 2's strategy K1 and Player 1's risk-adjusted payoff K2 in CVaR equilibrium as functions of K3 and K4; the regime shift at K5 is apparent, with monotonic variance reduction in K6.

Implications and Future Directions

The formulation and analysis of distributionally robust equilibria via coherent risk measures places strategic game theory on firmer footing for data-driven and risk-aware applications, spanning finance, economics, and multi-agent AI settings. Notably, the explicit connection to risk preferences enables interpretable comparative statics: the effect of varying tail-risk aversion or semideviation is analytically traceable to equilibrium structure and resilience properties. Practically, this equips designers of robust multi-agent systems with principled tools for tuning conservatism in response to data uncertainty and incentives.

Theoretically, the framework positions DRGs as occupying an "intermediate regime" between classical matrix games and generic continuous games, introducing nontrivial computational and conceptual challenges—for example, the breakdown of classical correlated equilibrium and the necessity of continuous-game apparatus for equilibrium existence and computation. These aspects invite several lines of future research: algorithmic development beyond complementarity-based formulations (e.g., scalable first-order methods leveraging the structure of risk measures), correlated equilibrium refinements for continuous games, and the extension to dynamic, repeated, and asymmetric-information environments—potentially drawing on advances from robust and risk-aware Markov decision processes.

Conclusion

This work offers a unified, interpretable, and computationally tractable framework for distributionally robust game-theoretic modeling using coherent risk measures. It fundamentally alters the geometry and interpretation of strategic equilibria under uncertainty, both constraining and enriching equilibrium structure and providing strong OOS and robustness properties. Extending these results to encompass dynamic and informationally complex environments stands to further deepen our understanding of robust strategizing in uncertain domains.