- The paper presents a clustered LP method that recovers conditional average responses through k-means clustering and robust GMM estimation.

- It bridges state-dependent and TVP-VAR approaches by enabling flexible nonparametric modeling of dynamic IRFs with maintained causal interpretability.

- Empirical and simulation evidence demonstrates its ability to detect regime changes and enhance analysis of monetary policy transmission under uncertainty.

Clustered Local Projections for Time-Varying Models: Methodology, Theory, and Empirical Evidence

Introduction

"Clustered Local Projections for Time-Varying Models" (2604.18778) introduces a novel method for estimating impulse response functions (IRFs) within time-varying parameter frameworks. The approach directly associates parameter variation with a low-dimensional matrix of observables, and iteratively clusters the data using k-means, followed by estimation of IRFs via GMM and hypothesis testing for cluster distinction. The clustered LP paradigm bridges gaps in traditional state-dependent and TVP-VAR methodologies by facilitating flexible nonparametric modeling while preserving causal interpretability even under endogenous regime drivers.

Theoretical Framework

The core specification embeds time-varying local projections: yt+h=βth(Zt−1)εt+γth(Zt−1)′wt+vt+h, with βth(Zt−1) allowed to vary nonparametrically as a function of relevant, possibly multivariate, observables Zt−1. Parameter identification presupposes exogeneity of the structural shock εt and stationarity of yt, Zt. The theoretical analysis proves that when Zt−1 is exogenous, the clustered LP estimator recovers the conditional average response (CAR) within each cluster, and for endogenous Zt−1 it yields a weighted average of conditional marginal effects (CMR), maintaining causal interpretability following [kolesar2025dynamiccausaleffectsnonlinear].

Classification is achieved via k-means on Zt−1, partitioning the sample into K clusters; IRFs are subsequently estimated jointly across clusters and horizons via GMM. Hypothesis testing using Wald statistics iteratively optimizes cluster count by controlling for multiple testing error.

Estimator and Algorithmic Details

The proposed algorithm consists of:

- Classification: K-means partitions the sample on the observable drivers βth(Zt−1)0.

- Estimation: IRFs for each cluster and horizon are jointly estimated via GMM, facilitating efficient covariance structure and robust inference.

- Evaluation: Pairwise Wald tests are conducted to assess statistical distinction of cluster-level IRFs across specified horizons. Bonferroni correction ensures conservative error control. Iteration proceeds until IRFs are mutually distinct across all clusters at chosen significance.

This procedure does not target a "true" regime count; rather, it yields a sample-determined piecewise-constant approximation, with potential for refinement as sample size increases and finer differences become detectable.

Monte Carlo Simulation Evidence

Univariate and Bivariate Threshold Models

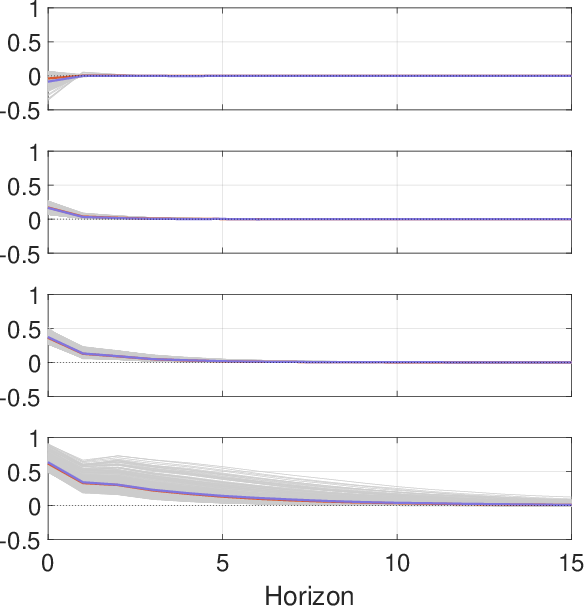

The method is evaluated via Monte Carlo simulations under several DGPs:

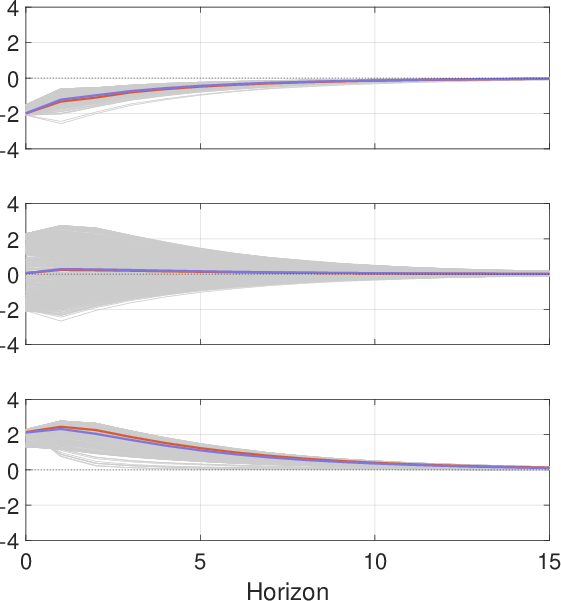

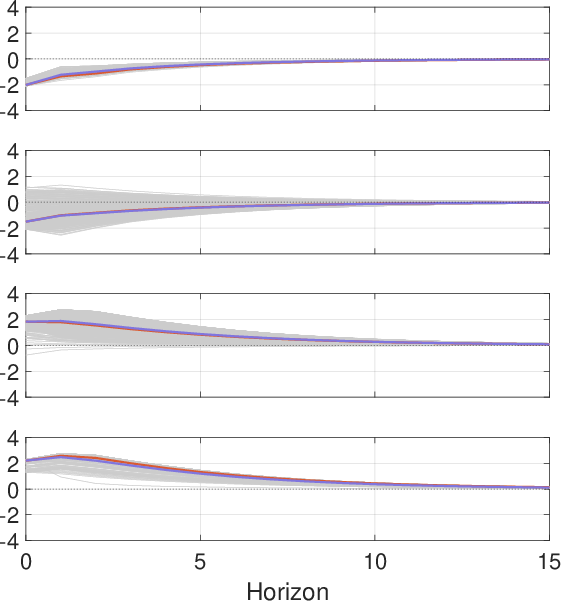

- Univariate Threshold Model:

Figure 1: Partitioning and estimation results for a univariate threshold DGP, with IRFs for each βth(Zt−1)1 (gray), clustered LP estimates (purple), and βth(Zt−1)2 (red) across βth(Zt−1)3 clusters.

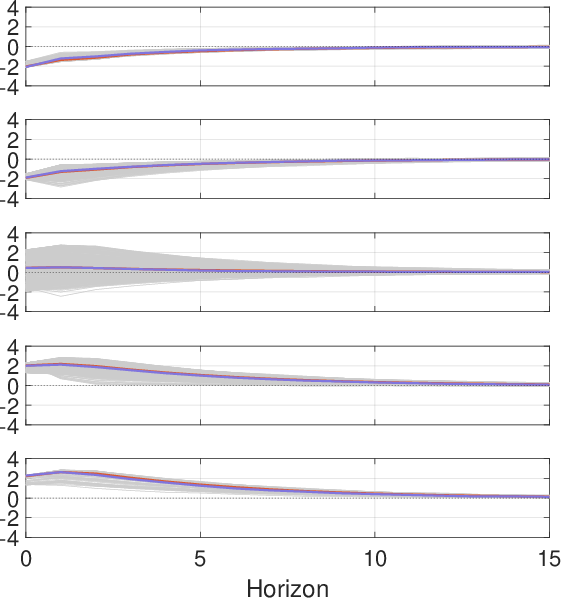

- Bivariate Threshold Model:

Figure 2: Partitioning and performance results for a bivariate threshold DGP, illustrating IRF clustering and recovery of CARs for βth(Zt−1)4.

Simulations demonstrate that the iterative algorithm reliably detects and recovers true regimes when discrete regime structure is present, and closely approximates conditional average responses when parameter variation is continuous or asymmetric, thus validating both theoretical claims and practical utility.

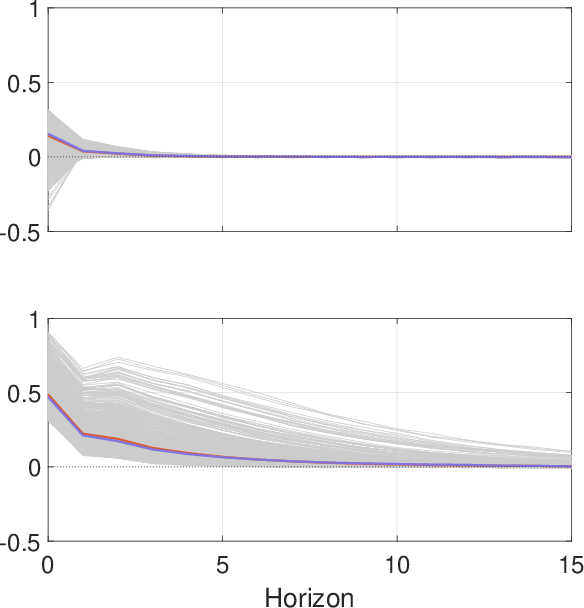

Absolute Value Model

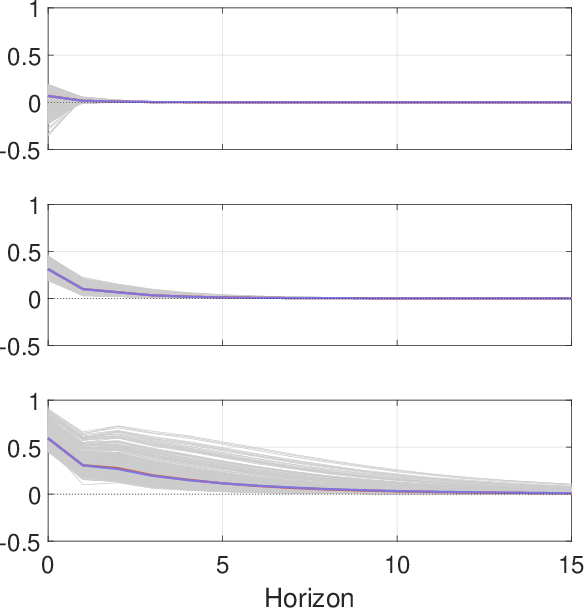

Figure 3: Simulation results for a DGP with parameters evolving as absolute value functions of βth(Zt−1)5, showing clustered LP estimates closely match true CAR, even absent discrete regime switching.

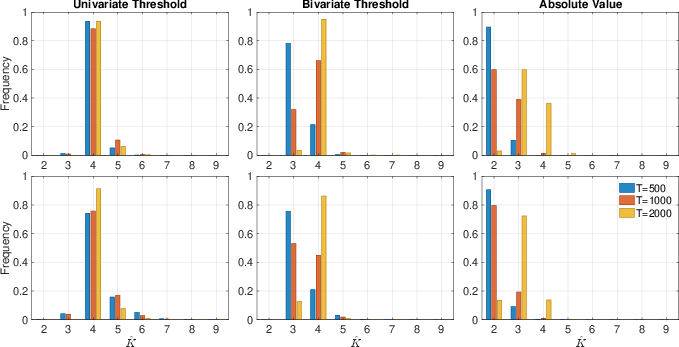

Cluster frequency estimation (Figure 4) indicates conservative cluster selection under small sample sizes and continuous parameter evolution, further evidencing robustness and adaptability.

Figure 4: Frequency histogram for selected cluster count βth(Zt−1)6 across DGPs and sample sizes, illustrating algorithmic conservatism under limited data.

Empirical Application: Monetary Policy Transmission Under Uncertainty

The clustered LP method is applied to U.S. financial data (February 1988–December 2023) to assess transmission of contractionary monetary policy shocks to medium- and long-term Treasury yields, conditioning on macroeconomic and monetary policy uncertainty indices (MacroUncer, MPU). Traditional event study and state-dependent LP approaches provide limited granularity, often presupposing synchronicity and regime classification.

State-Dependent Local Projections

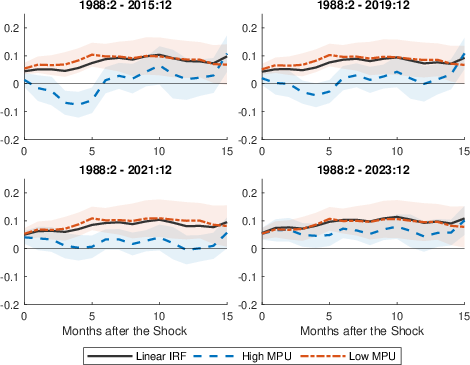

State-dependent LP estimates based on high/low MPU and MacroUncer demonstrate time-varying heterogeneity in IRFs, particularly pronounced during the Covid-19 pandemic. Linear models grossly misestimate policy effectiveness under high uncertainty regimes.

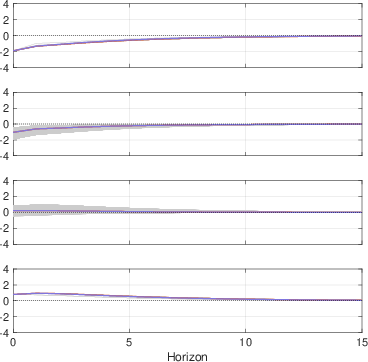

Figure 5: State-dependent LP IRFs for the 5-year yield, stratified by monetary policy uncertainty, demonstrating distinct regime responsiveness and time-variation.

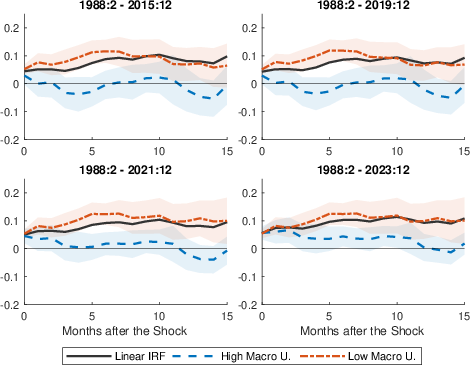

Figure 6: State-dependent LP IRFs stratified by macroeconomic uncertainty, revealing attenuated yield responses during high uncertainty states.

Clustered LP Classification Results

The clustered LP algorithm partitions the data into four clusters reflecting all combinations of macroeconomic and monetary policy uncertainty regimes, revealing periods where uncertainties are not synchronous.

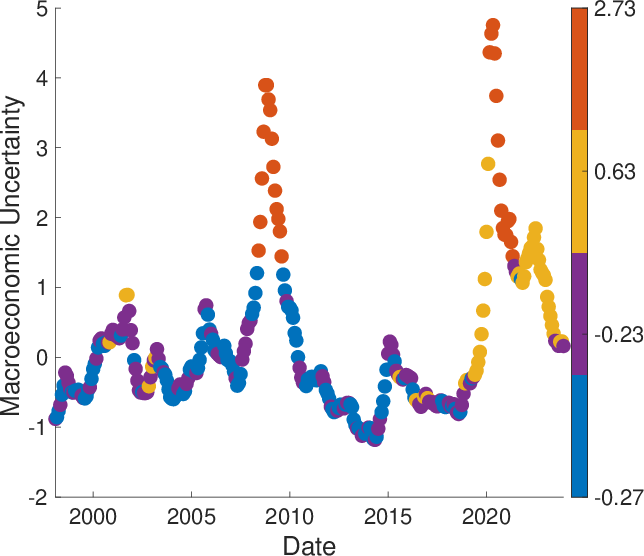

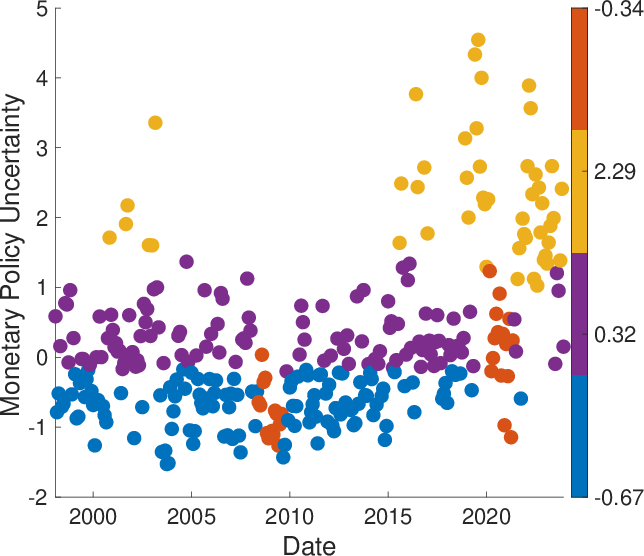

Figure 7: Scatterplots of macroeconomic and monetary policy uncertainty series classified into four clusters, visually confirming non-synchronization and distinct grouping.

Cluster means reveal distinctive characteristics, with some periods (e.g., Great Recession, Covid-19) featuring high macro uncertainty but low policy uncertainty, and vice versa.

Impulse Response Results Across Regimes

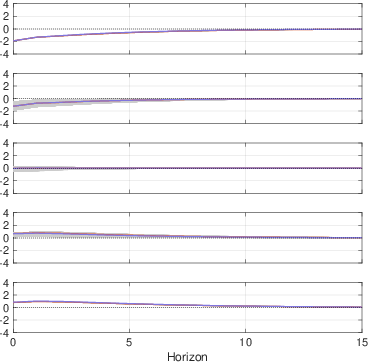

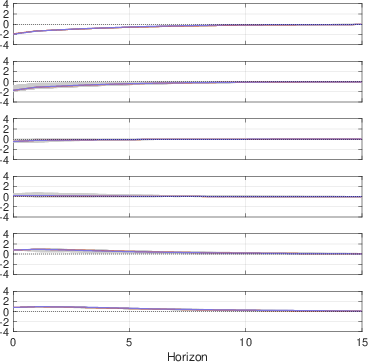

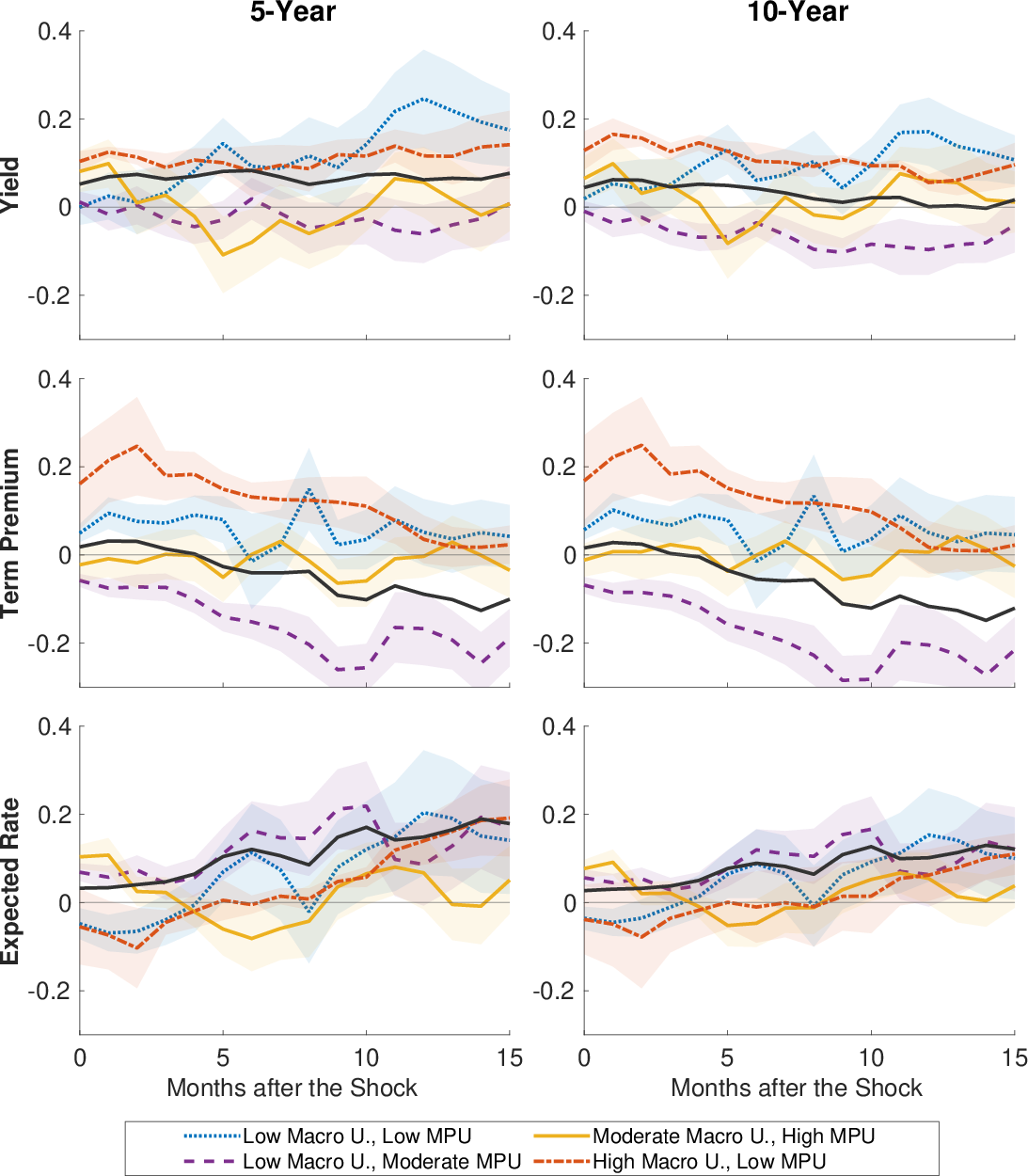

Clustered LP IRFs indicate that on impact and in the very short-run, macroeconomic uncertainty dominates yield response heterogeneity. At longer horizons, MPU governs persistence and magnitude, with yield responsiveness an order of magnitude higher during low MPU twelve months post-shock. Conventional linear LPs average across these distinct responses, underestimating/overestimating effects in specific uncertainty regimes.

Figure 8: Clustered LP IRFs for 5- and 10-year yields (and components) across uncertainty regimes, showing regime-dependent transmission magnitudes and dynamic structure.

Disaggregation reveals that term premium responses are particularly amplified under macroeconomic uncertainty, while expectation components are far more sensitive to MPU. These findings substantiate claims that macro and monetary policy uncertainty operate through orthogonal yet complementary channels—amplifying risk compensation and governing adaptive expectation revision, respectively.

Implications and Future Directions

The clustered local projections estimator enables credible identification and estimation of IRFs under flexible, observable-driven parameter variation. Its empirical performance suggests practical superiority to traditional state-dependent or TVP-VAR approaches, especially in settings with multiple interacting sources of time variation and nonlinearity. The methodology has direct implications for policy analysis, asset pricing, and macro-financial forecasting under uncertainty.

Theoretically, the approach advances causal interpretation in nonlinear, time-varying environments, generalizing the state-dependent LP literature. Practically, future research may extend clustered LP methods to higher-dimensional applications, refine automated classification, and integrate instrumental variable identification for broader structural analysis.

Conclusion

Clustered local projections provide a robust, data-driven methodology for estimating impulse response functions in time-varying models. The approach reliably recovers causal summaries, enables nuanced regime detection, and generates empirically valid insights into monetary policy transmission under multifaceted uncertainty. Simulation and empirical evidence support its efficacy and interpretability, and continued methodological development is warranted to optimize estimation in high-dimensional and endogenous settings.