- The paper introduces a two-stage stochastic optimization model that co-optimizes day-ahead and reserve bids while integrating risk control through CVaR.

- It demonstrates that risk-averse scheduling reduces profit volatility by aligning planned and real dispatch, albeit at the expense of expected profitability.

- Dynamic network tariffs incentivize demand shifts by redistributing loads, but excessive tariff variations can erode profits due to flexibility saturation.

Risk-Aware Multi-Market Scheduling of Virtual Power Plants with Dynamic Network Tariffs

Distributed Energy Resources (DERs)—including rooftop PV systems, heat pumps, battery energy storage (BESS), and electric vehicles (EVs)—are increasingly critical for modern power systems. Virtual Power Plants (VPPs) efficiently aggregate DERs to unlock flexibility for grid operations and multi-market participation. However, the volatility of DERs coupled with localized grid constraints and operational uncertainties necessitates robust, scalable scheduling frameworks. This paper ("Risk-Aware Multi-Market Scheduling of Virtual Power Plants with Dynamic Network Tariffs" (2604.26424)) addresses two central challenges: (i) co-optimization of VPP participation in the day-ahead and reserve markets under uncertainty and network tariffs, and (ii) quantification of the impact of dynamic tariffs on VPP profitability and flexibility.

The authors present a two-stage stochastic optimization model, representing first-stage market offers and second-stage physical dispatch contingent on realized uncertainties. Price forecasts for energy and ancillary services, operational parameters (e.g., load, PV output, ambient temperature), and physical network constraints are modeled across a scenario set. The risk preferences of VPP operators are integrated via Conditional Value-at-Risk (CVaR), allowing direct control over downside exposure. Benders decomposition is leveraged for tractable parallel solution over extensive scenario sets, facilitating high-resolution DER and network modeling beyond the capacity of conventional monolithic programs.

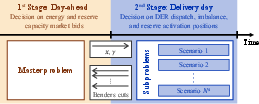

Figure 1: Visualization of Benders decomposition structure for the two-stage stochastic scheduling problem, with explicit separation of master bids and scenario-specific subproblems.

Model Structure and Case Study Setup

The master problem determines energy and reserve bids (first-stage variables), while scenario subproblems resolve dispatch decisions, reserve activations, and imbalance positions under scenario-specific uncertainties. Financial flows are exhaustively represented: day-ahead, reserve capacity, reserve activation revenues, operational costs, imbalance penalties, and nodal dynamic tariffs. Physical feasibility incorporates explicit device-level constraints (charging/discharging rates, thermal dynamics, capacity factors), power flow equations (linear DistFlow), and network voltage, current, and nodal injection limits.

For case study validation, the authors use a realistic low-voltage Swiss distribution network: 97 buses, 150 kW peak non-dispatchable load, 150 kWp PV, 85 kW HPs, 75 kWh BESS, and 40 EV charging events. Price and operational uncertainties are sampled using Latin hypercube with scenario count Ns=1000. All calculations are parallelized on a HPC cluster. The network topology is shown below.

Figure 2: The test network used in the case study, depicting all buses, lines, and substation locations.

Empirical Analysis: Risk Aversion and Market Interaction

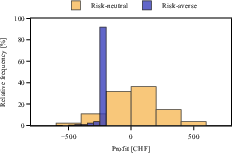

The optimization yields a direct trade-off between expected profit and volatility as quantified by profit distributions (see Figure 3). Risk-neutral strategies (mean optimization) maximize expected profit but exhibit high volatility and exposure to adverse imbalance events. Risk-averse CVaR strategies substantially reduce volatility but sacrifice expected profitability—results indicate an expected profit swing of over 270 CHF in favor of stability. The CVaR approach forces closer alignment between scheduled and physical dispatch, mitigating imbalance penalties but necessitating greater internal flexibility (e.g., increased BESS throughput and EV cycling).

Figure 3: Distribution of VPP net profits for risk-neutral and risk-averse strategies, with expected values indicated.

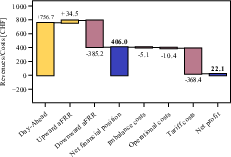

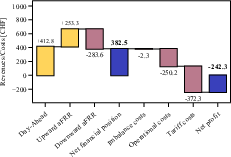

Figure 4: Revenue and cost breakdown for (a) risk-neutral and (b) risk-averse strategies, illustrating shifting reliance on flexibility resources and market positioning.

Risk-neutral bidding exhibits aggressive arbitrage, prioritizing short day-ahead exposure and downward reserve activation. This yields mismatches between contracted and actual energy withdrawal, amplifying the risk of imbalance penalties. Conversely, risk-averse scheduling hedges against extreme outcomes, diversifies across markets, and enhances internal flexibility use (notably BESS operation increased by 146%).

Dynamic Network Tariffs: Operational and Economic Effects

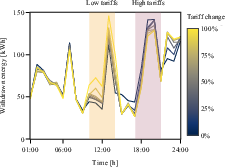

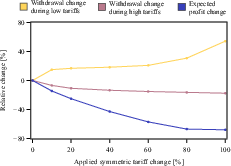

Dynamic network tariffs, modeled as time-varying node charges, incentivize demand shifts to alleviate congestion and reinforce local grid operations. The sensitivity analysis examines symmetric tariff changes (decreases during midday, increases during evening peaks). Moderate tariff signals (10–20% variation) are effective in shifting load intraday, redistributing withdrawals during low- and high-tariff hours. However, stronger tariff signals (>20% variation) yield diminishing returns: flexibility gain saturates, while expected profit is eroded by up to 65%. These results underscore the nonlinearity of tariff response and the practical limits of tariff-based flexibility procurement.

Figure 5: (a) VPP net energy withdrawals at the point of common coupling under dynamic tariff signals. (b) Relative changes in profit and withdrawals as tariff variation increases, showing nonlinear and saturating response in flexibility.

Implications and Future Developments

The presented framework integrates market, physical, and regulatory dimensions with device-level granularity, enabling realistic scheduling for VPPs subject to network tariffs and uncertainty. Strong numerical results demonstrate scalable computation—solving models with 106+ variables and 108+ constraints—using Benders decomposition. Observed saturation in flexibility response to tariffs provides actionable guidance for policymakers: modest tariff variations achieve substantial load shifting, but excessive intervention is economically suboptimal.

Practical implications include:

- Enhanced VPP scheduling realism through explicit DER and network modeling

- Direct quantification and management of profit-risk trade-offs

- Informed design of dynamic tariffs to avoid over-incentivization and profit erosion

- Parallelizable computation for large scenario sets

Limitations relate to scenario-based modeling of uncertainty, assumed independence of forecast errors, and exclusion of intraday markets. Future research directions include joint-copula-based scenario generation to capture tail dependencies, inclusion of intraday market participation, and reduced scenario requirements via advanced uncertainty propagation.

Conclusion

This work establishes a risk-aware, decomposed optimization architecture for VPP multi-market scheduling responding both to wholesale markets and dynamic network tariffs. The empirical results demonstrate nuanced profit-volatility trade-offs, internal flexibility utilization, and nonlinear tariff–flexibility interactions. These findings advance academic and practical understanding of VPP operations in modern, flexible power systems. Further enhancements are anticipated via improved uncertainty modeling and broader market scope.