- The paper demonstrates an exact LP reformulation of a two-stage ARO model for VPP bidding, ensuring robust handling of renewable and price uncertainties.

- The study introduces a custom greedy recourse algorithm and a projected subgradient method (PSM-PAVA) that reduce computational time by over two orders of magnitude compared to traditional methods.

- The model effectively integrates DER dispatch, storage scheduling, and risk-adjusted offer curves to optimize day-ahead market participation under uncertainty.

Stochastic Linear Programming for VPP Day-Ahead Market Participation

This paper investigates the optimal day-ahead market offering problem for Virtual Power Plants (VPPs) aggregating distributed energy resources (DERs), under coupled uncertainties in renewable output and market prices. The authors present a structured two-stage stochastic adaptive robust optimization (ARO) model and demonstrate an efficient reformulation as a stochastic linear program (LP), introducing novel algorithmic advances that enable significant computational improvements over established methods.

The operational challenge addressed involves VPPs submitting stepwise price-quantity offer curves to the day-ahead market, with subsequent real-time deployment of DERs (solar PV, storage, and loads) under realized uncertainties. The paper formulates this as a two-stage stochastic ARO problem: first-stage decisions represent pre-committed day-ahead offers, while second-stage recourse actions correspond to real-time dispatch, optimizing expected profit while hedging against worst-case PV uncertainties and sampled price trajectories.

Hybrid Uncertainty Modeling

- Price Modeling: The day-ahead price process is described by a Markov chain, capturing inter-hour correlations and allowing efficient scenario generation.

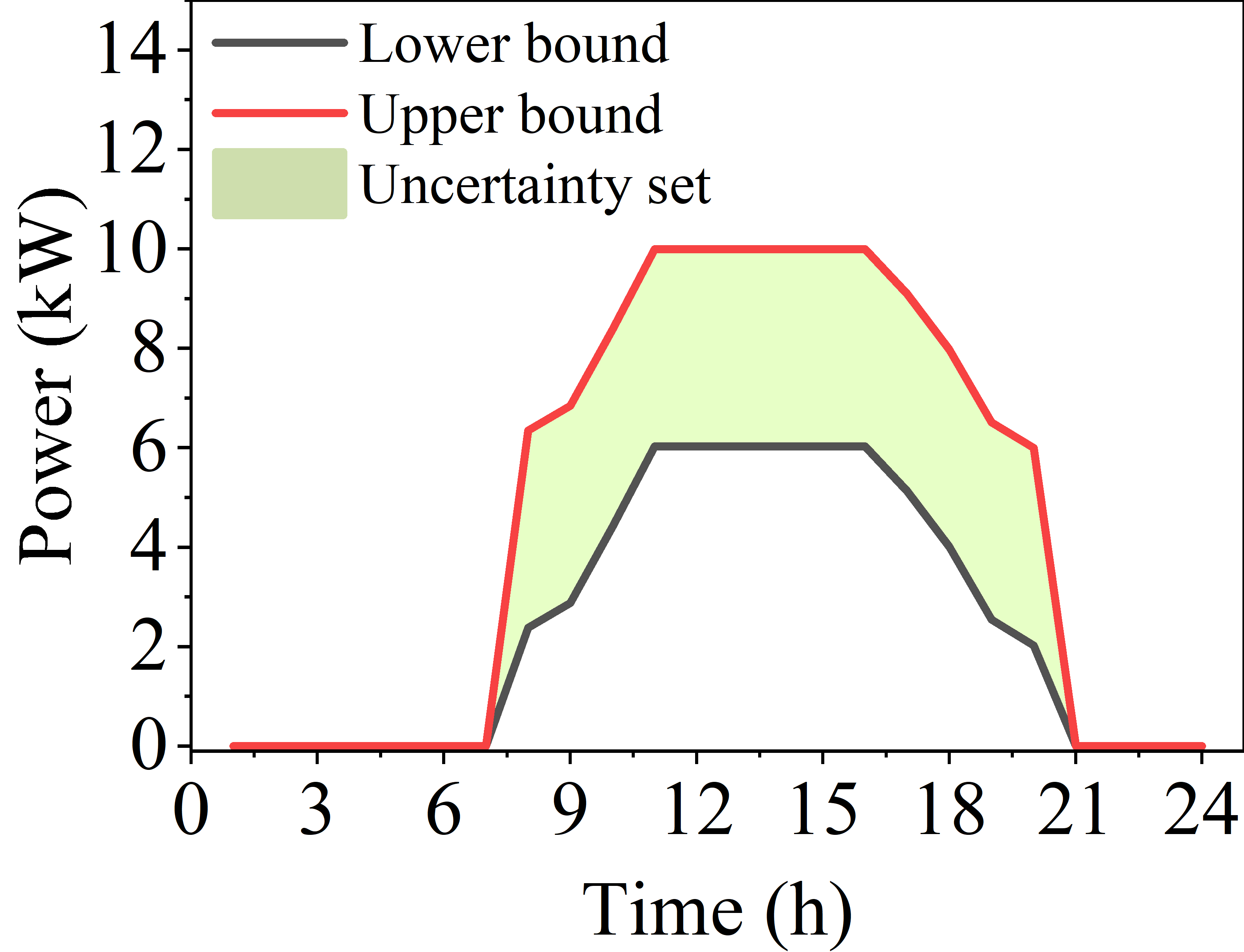

- Renewable (PV) Uncertainty: Modeled via budgeted uncertainty sets—static, knapsack-style sets reflecting forecast error bounds and an aggregate deviation budget Γ.

Second-Stage Structure

The second-stage problem leverages device-accurate models for solar PV, aggregated load, and an energy storage unit (state-of-charge dynamics, power/energy limits). Critical nonconvexities—such as storage complementarity—are eliminated via structural properties, allowing a tractable LP reformulation.

A central technical contribution is the decoupling of the robust second-stage max-min structure:

- PV dispatch: Proven to optimally saturate the upper availability bounds in adversarial scenarios.

- Storage scheduling: The nested resource allocation with piecewise-linear costs reduces to a separable convex LP with cumulative sum constraints.

This allows the original two-stage ARO to be equivalently recast as a two-stage stochastic LP with separable recourse, preserving exactness under mild conditions on model parameters.

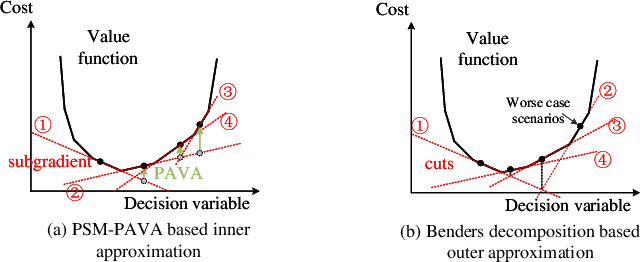

Figure 1: Two ways of approximation of the value function.

Algorithmic Advancements

Greedy Oracle for Recourse Evaluation

Recognizing the nested structure of the second-stage LP, the authors design a custom greedy algorithm for recourse evaluation. This exploits the monotonic cumulative constraints and the convex piecewise-linear cost decomposition, achieving optimality with substantially reduced computation compared to general-purpose LP solvers. The greedy algorithm guarantees feasibility and optimality through incremental, lexicographically ordered updates to resource allocations.

Projected Subgradient Method (PSM-PAVA)

For the full two-stage problem, a projected subgradient method (PSM) is combined with pool-adjacent-violator algorithm (PAVA) style projections to maintain compliance with box and monotonicity constraints on offer curves. The method employs spectral stepsize selection and constructs valid subgradients using the recourse oracle, capitalizing on scenario-wise decomposability. Crucially, the algorithm maintains constant per-iteration computational cost, in contrast to accumulation-based cuts in Benders-type or column-and-constraint generation (CCG) schemes.

Figure 2: Pre-determined uncertainty parameters.

Numerical Evaluation and Comparative Analysis

Greedy Algorithm Versus Commercial LP Solvers

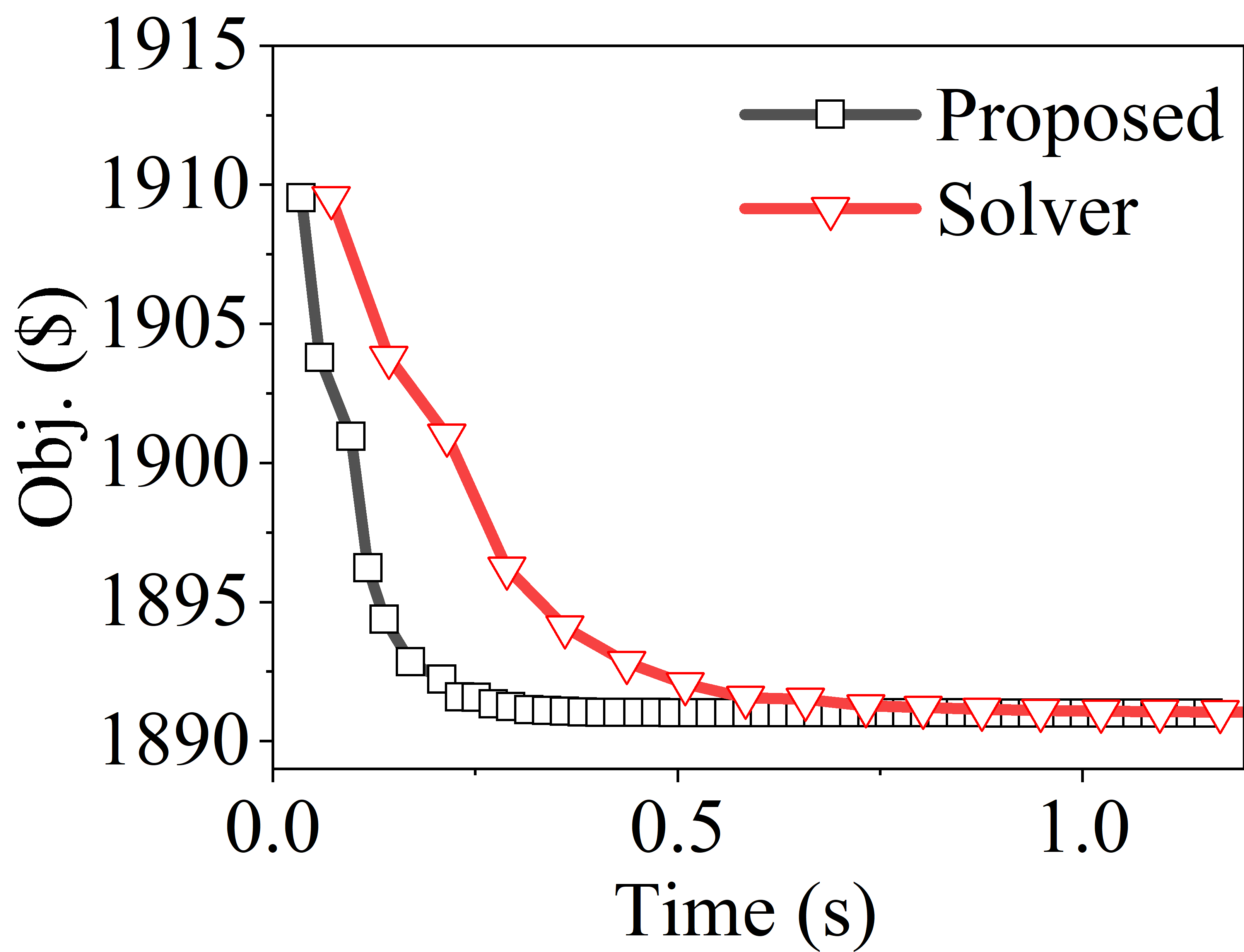

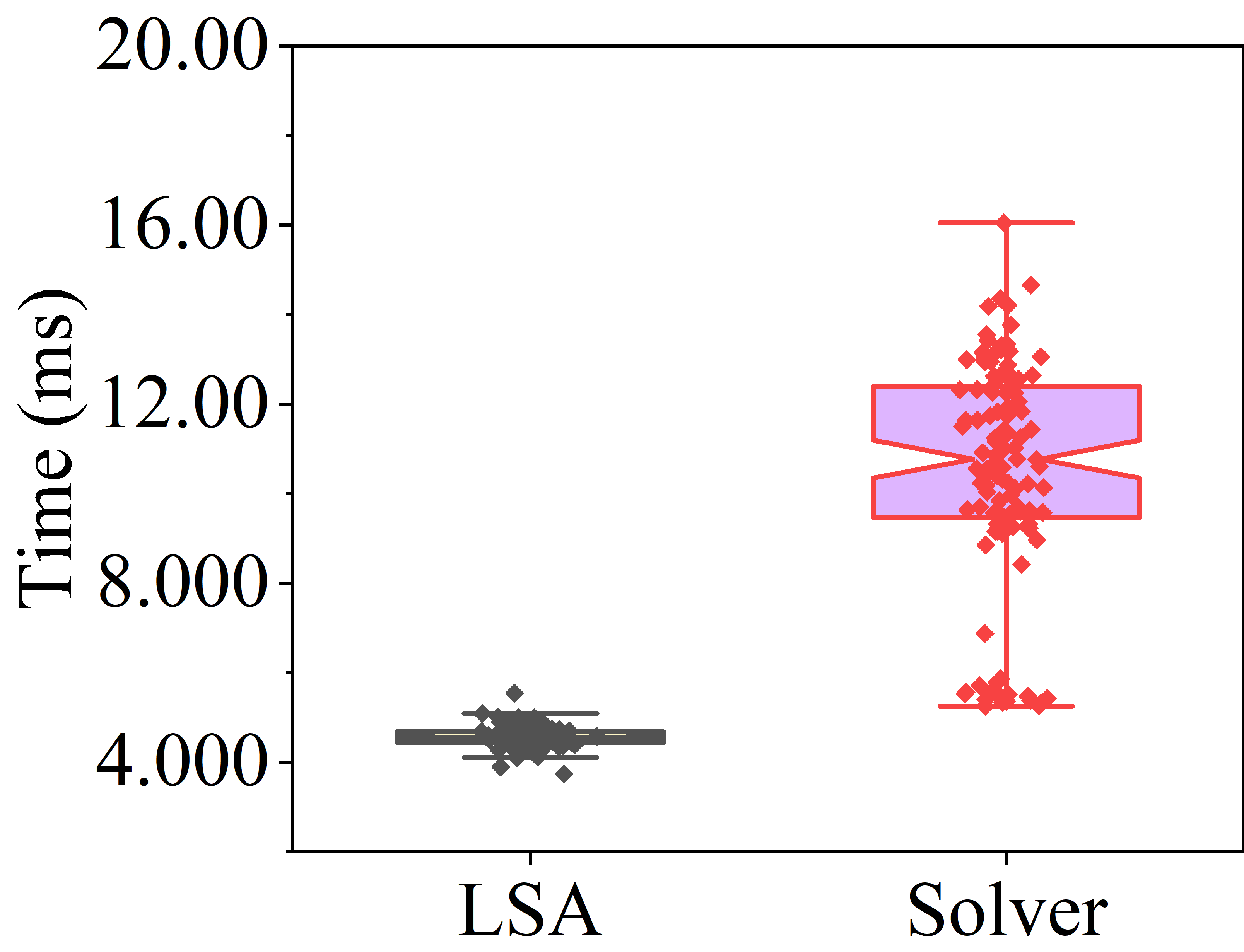

Empirical benchmarks demonstrate that the greedy recourse oracle achieves identical objective values to commercial solvers (e.g., Gurobi), with up to 2× faster per-iteration solution times as the number of price scenarios increases (see Table 1 in the paper). This computational efficiency is achieved without compromising exactness.

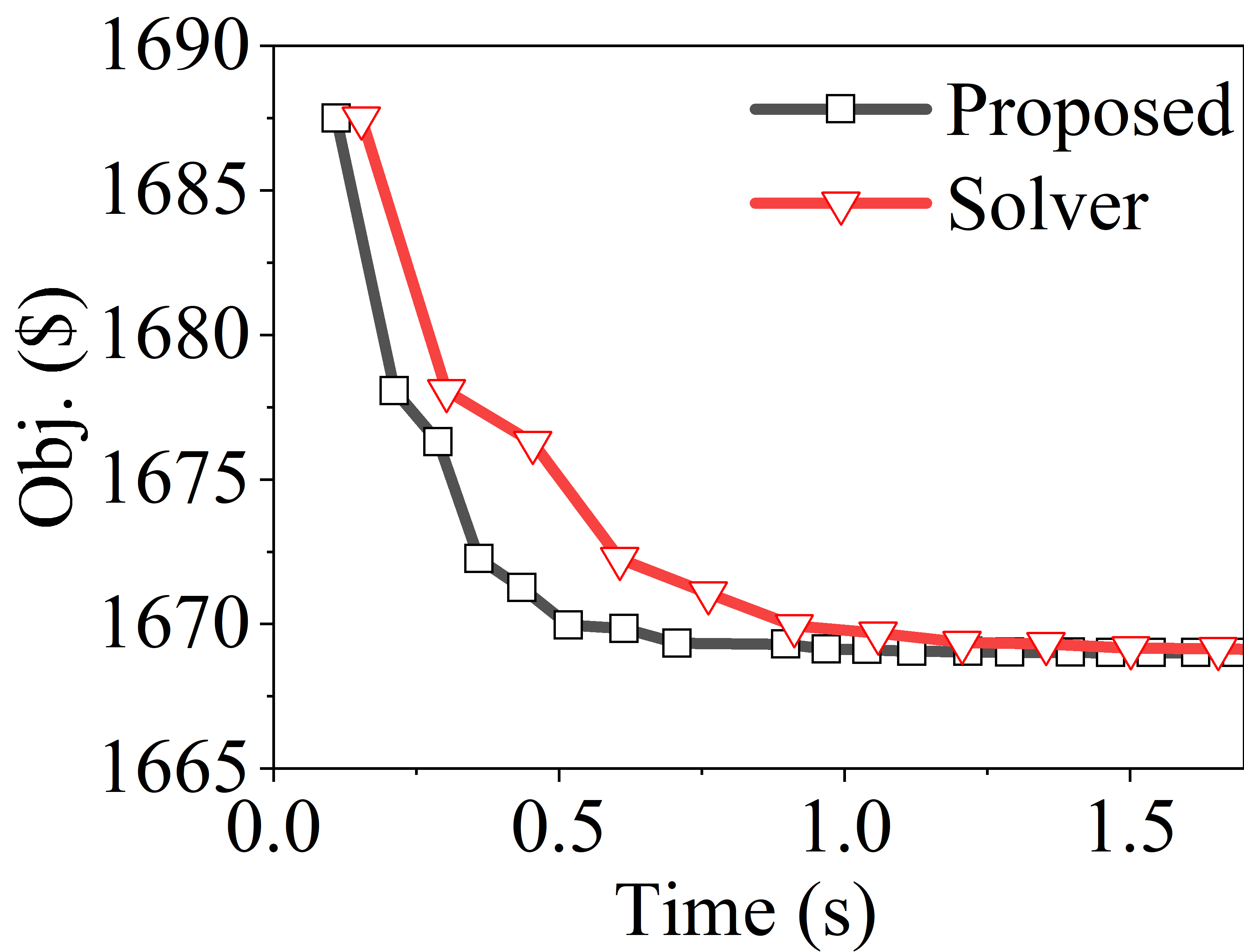

Figure 3: Performance comparison of the proposed greedy algorithm and the benchmark commercial LP solver under different numbers of price trajectories. The top row illustrates the iteration process and optimality, while the bottom row reports the computational time per iteration (maximum iterations = 50, Γ=6).

Projected Subgradient Versus CCG

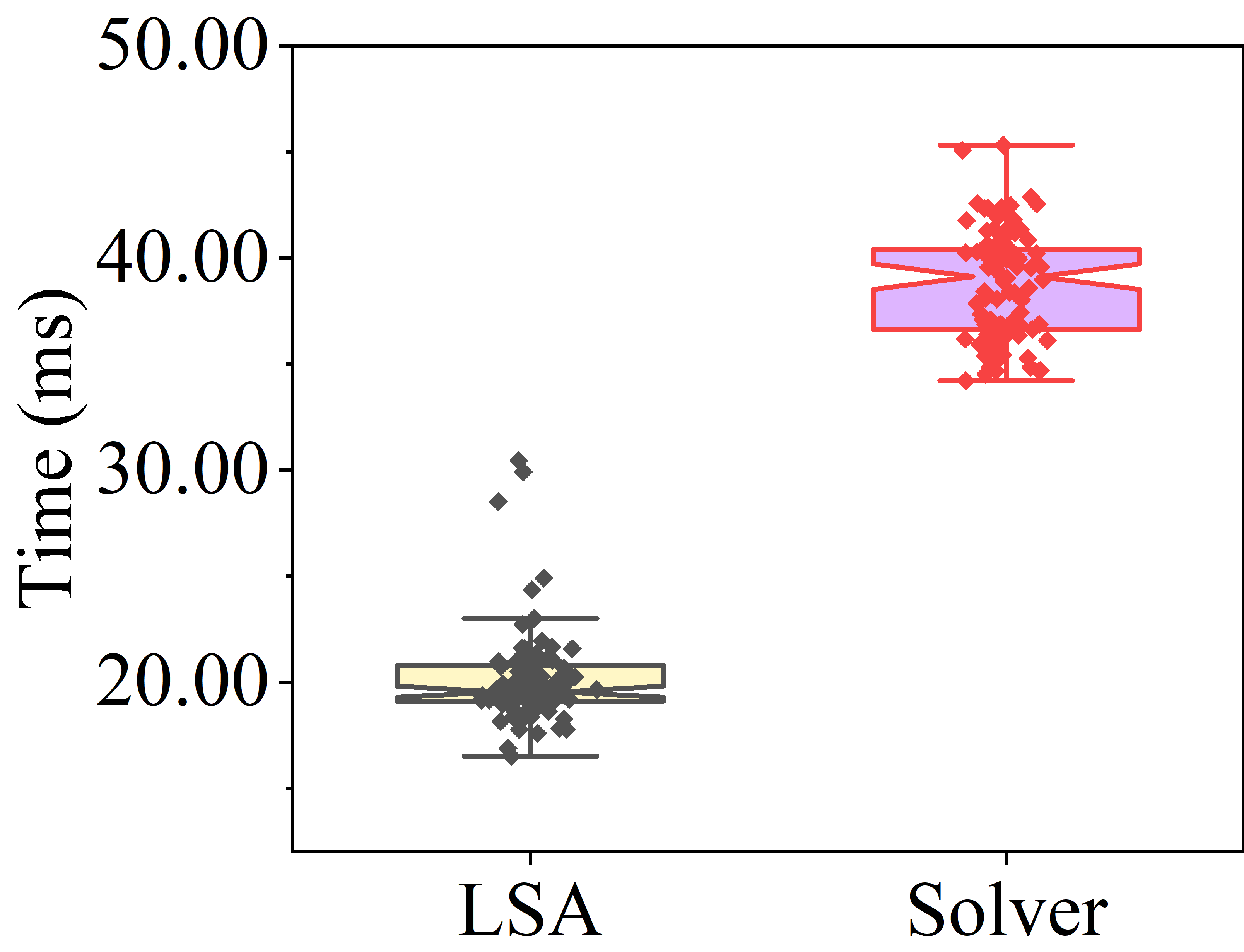

The combination of the LP reformulation and the PSM-PAVA algorithm enables dramatic speedups relative to the CCG algorithm applied to both the original ARO and the stochastic LP. For large scenario sets (up to 500), the PSM-PAVA solution time improves by over two orders of magnitude—decomposable into a 2× gain from recourse reformulation and 70× gain from algorithmic design (see Table 2 in the paper).

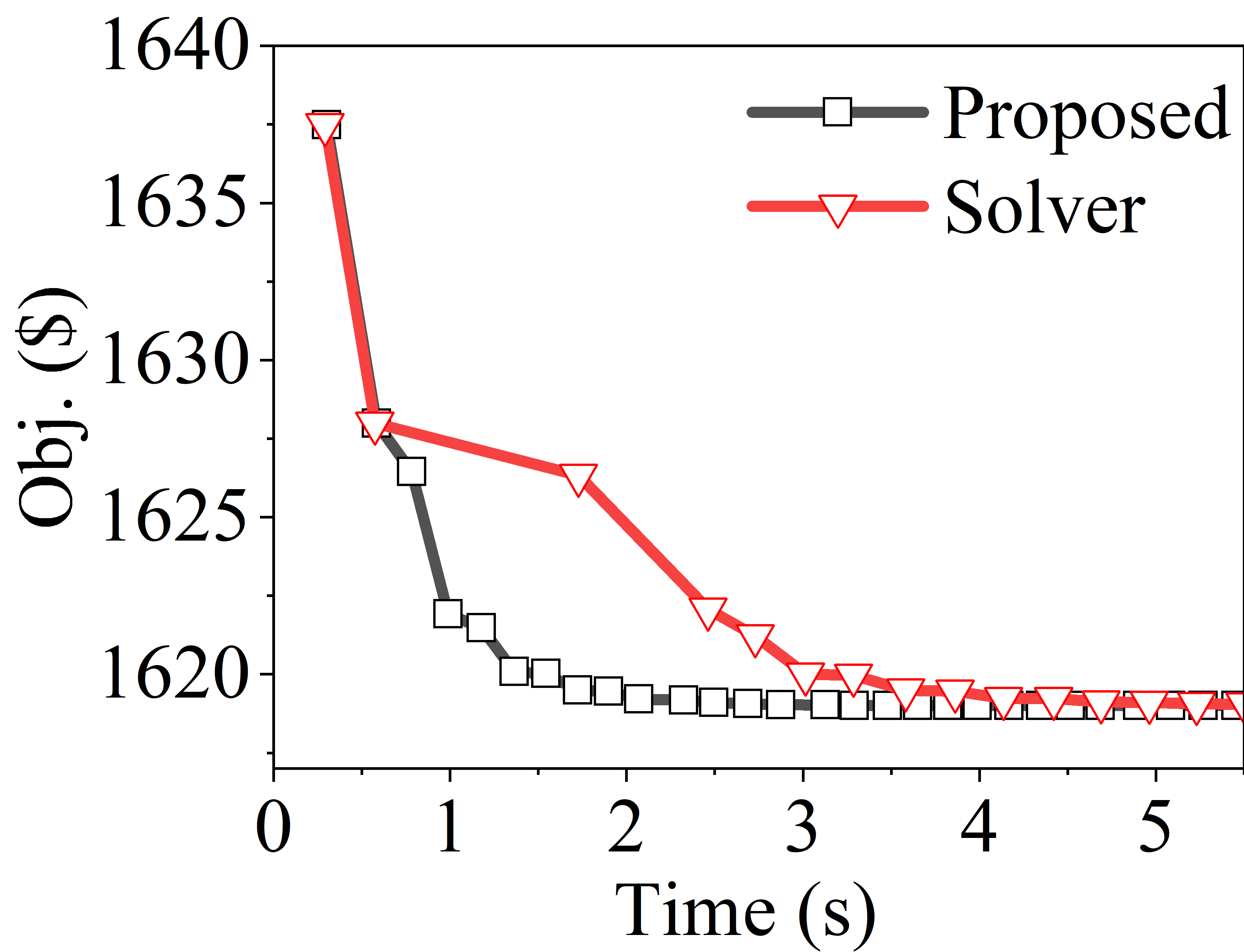

Figure 4: Performance comparison of the iteration process, optimality and computational time for the PSM-PAVA and traditional CCG algorithm for the 2S-ARO problem (Maximum iteration =600; Γ=6).

Economic and Operational Implications

Day-Ahead Market Bidding Characteristics

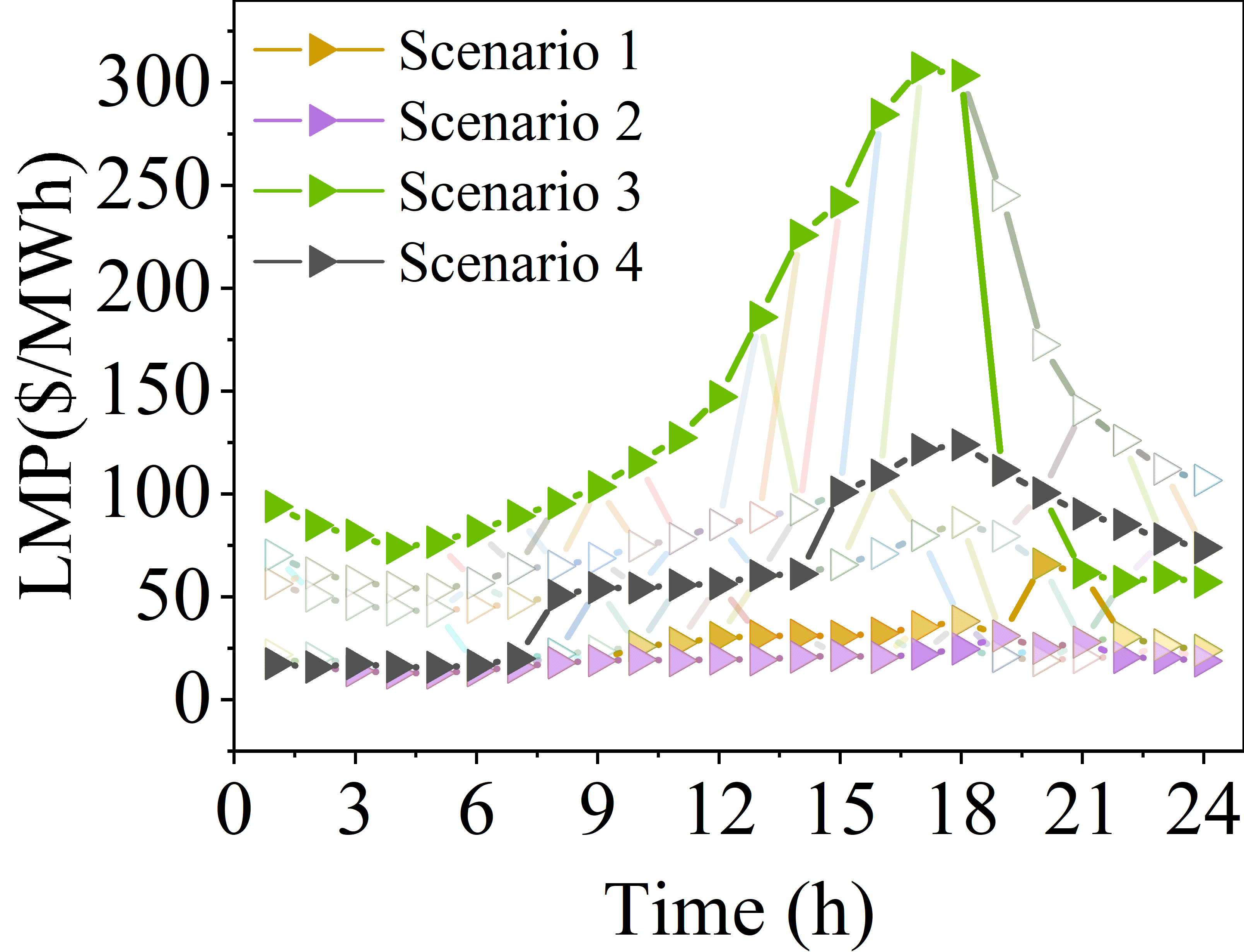

The model explicates VPP optimal offer formation as a function of price and risk budget (parameter Γ). Lower Γ yields less conservative, higher-volume offers and more aggressive arbitrage—buying during expected low-price intervals and selling at peaks.

Figure 5: Offering curves in the day-ahead market for time slots 1, 11, 12, and 22.

Storage and Dispatch Decisions

Scenario analysis shows that battery storage operates as a temporal arbitrageur, charging at low prices and discharging at high, synchronized with forecasted price trajectories. The dispatch aligns with operational and regulatory constraints.

Figure 6: Energy storage unit dispatch decisions within the VPP under six price scenarios.

Scalability

Empirically, solutions stabilize as the number of price scenarios exceeds 500, with coefficient of variation in the average profit dropping below 0.5%, demonstrating robustness with tractable scenario set sizes.

Figure 7: Evolution of the average profit with the number of sampled price scenarios.

Out-of-sample evaluation on historical data confirms that economic dispatch under proposed offer schedules satisfies commitments, avoids arbitrage between settlements (in accordance with market rules), and optimally arbitrages price dynamics through storage.

Figure 8: Economic dispatch decisions of VPP under three price scenarios (``RT'': the operational power).

Theoretical and Practical Impact

The work establishes that, for this class of VPP offering problems, robust two-stage stochastic optimization can be exactly reduced to a scalable stochastic LP without model loss. The structured algorithm (PSM-PAVA) exploits problem decomposability, obviating the need for cut accumulation or MILP-based recourse reformulations. Practically, this enables high-fidelity, scenario-rich offer optimization for large DER aggregations in hours rather than days—facilitating broader VPP market participation and integration of renewables.

On the theoretical front, the separation of adversarial renewables from stochastic price processes and the greedy reduction for piecewise-linear cumulative-constrained resources generalizes to other market-coupled energy resource scheduling regimes and robust SP/ARO settings.

Conclusion

This paper presents a significant advancement in VPP day-ahead bidding optimization by reformulating the challenging two-stage stochastic ARO as a tractable stochastic LP and introducing an efficient projected subgradient algorithm with a custom greedy recourse oracle. Theoretical guarantees and extensive computational studies confirm that the proposed methodology attains strong solution quality with substantial computational savings. This approach is well-positioned to support large-scale, uncertainty-aware DER aggregation in competitive electricity markets and opens the door to further advances in robust, scalable stochastic energy market participation models. Future research may examine extensions to networked VPPs, dynamic offering rules, and integration of additional DER types.