- The paper's main contribution is demonstrating that systematic transaction scheduling reduces fee exposure by leveraging off-peak periods on Ethereum.

- It introduces an On-Chain Scheduling Matrix that classifies transactions by gas intensity and deferrability, yielding actionable regimes.

- Empirical analysis across industries indicates significant, but incomplete, fee reductions, emphasizing strategic cost management in blockchain operations.

On-Chain Peak Shaving: Transaction Scheduling as Operational Policy in the Ethereum Fee Market

Theoretical Framing: Extending TCE with Dynamic Execution Costs

"On-chain Peak Shaving" (2604.19956) advances a critical extension to Transaction Cost Economics (TCE) by explicitly integrating time-varying execution costs due to congestion externalities—specifically, Ethereum gas fees. Unlike classic execution costs such as settlement fees, which are assumed stationary in standard TCE formulations, on-chain execution costs fluctuate by over 100% intraday, driven by a surge pricing mechanism (EIP-1559) responsive to aggregate network demand. The paper further proposes a dual classification of gas fees, treating them as timing-dependent execution costs for the firm but as maladaptation costs in their origin, since they are imposed by extraneous network activity and are not contractually renegotiable.

This extension holds only when (i) the blockchain network employs endogenous, dynamic marginal-cost pricing, (ii) the focal firm is a price-taker with respect to network fees, and (iii) there is operational latitude for voluntary transaction deferral. These structural contingencies demarcate when standard TCE logic must be augmented to capture the strategic relevance of congestion-driven execution costs.

Mechanism, Propositions, and Methodological Architecture

The paper defines "on-chain peak shaving" as the systematic deferment of blockchain transactions to empirically off-peak, low-congestion periods to minimize fee exposure. Leveraging a novel transactional-speculative decomposition, the authors distinguish between necessity-driven transactional flows (low elasticity, predictable periodicity, identifiable actors) and speculative-arbitrage flows (high elasticity, cluster around price events, DEX/MEV participants per [daian2020flash]). They further introduce a structured On-Chain Scheduling Matrix taxonomy, partitioning firm populations by transaction deferrability and gas intensity, yielding four operational regimes—full peak shaving, selective peak shaving, cost provisioning, and accept-market-rate—with unambiguous strategic recommendations for each.

Empirical Identification: Cross-Industry On-Chain Scheduling

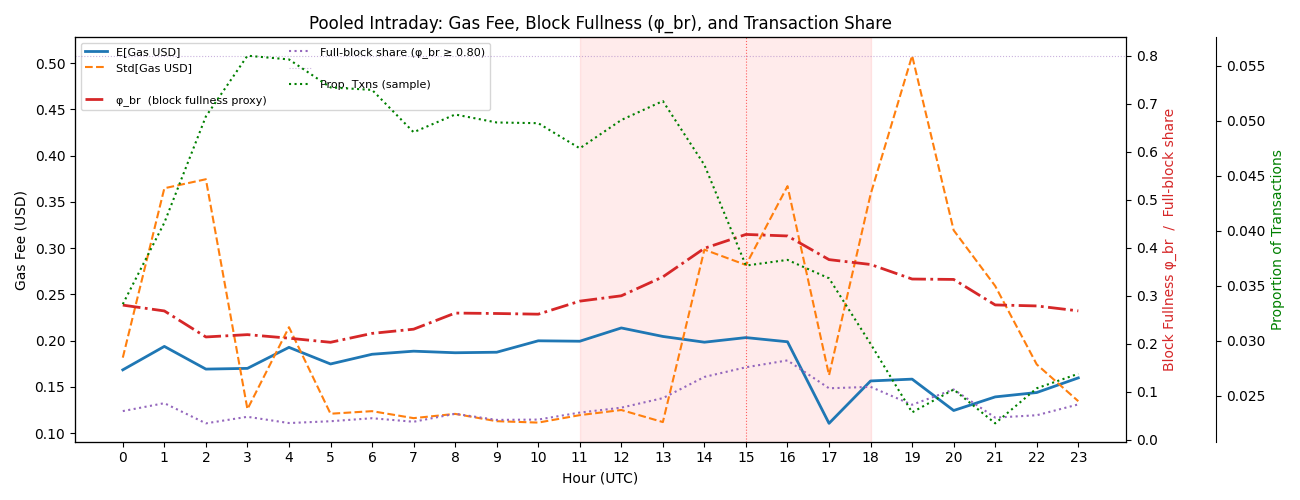

The study analyzes N=62,142 transactions submitted by seven firms in technology, finance, healthcare, supply chain, real estate, consumer goods, and administrative services, spanning January–March 2026. Hourly regressions (both pooled and firm-level) reveal robust intraday cost structure: base-fee premia peak at 10am ET (hour 15 UTC) with a statistically significant differential of \$0.220 over the overnight baseline$(t=12.33,\,p<0.001)$, and are primarily induced by speculative-arbitrage demand, not operational requirements.

Figure 1: Hourly average and standard deviation of gas fees, with transaction proportions by hour highlighting cost concentration during US/European business periods.

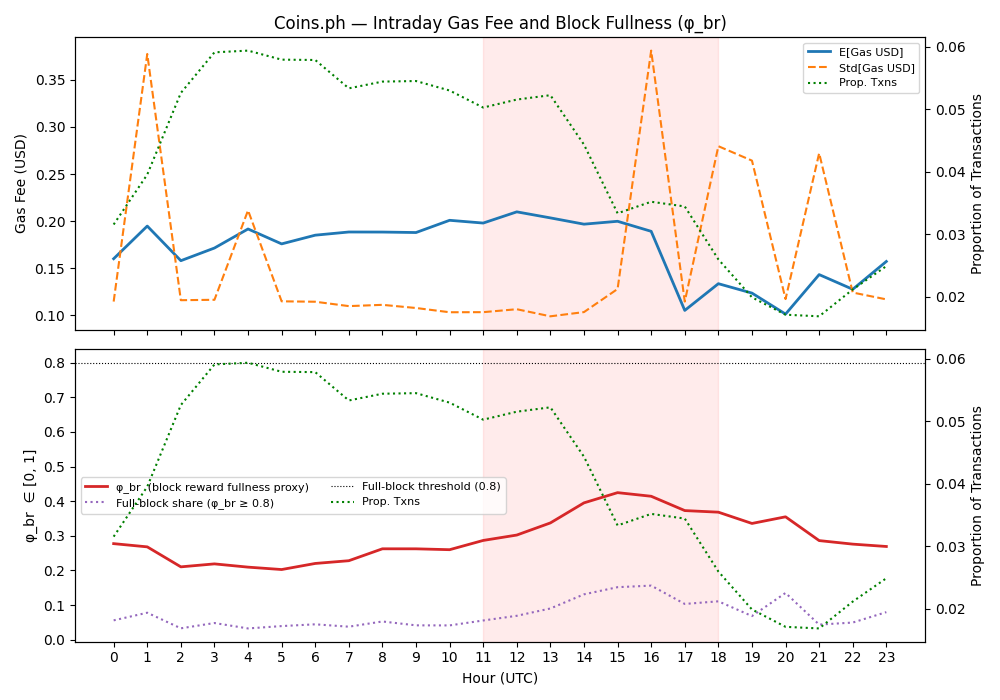

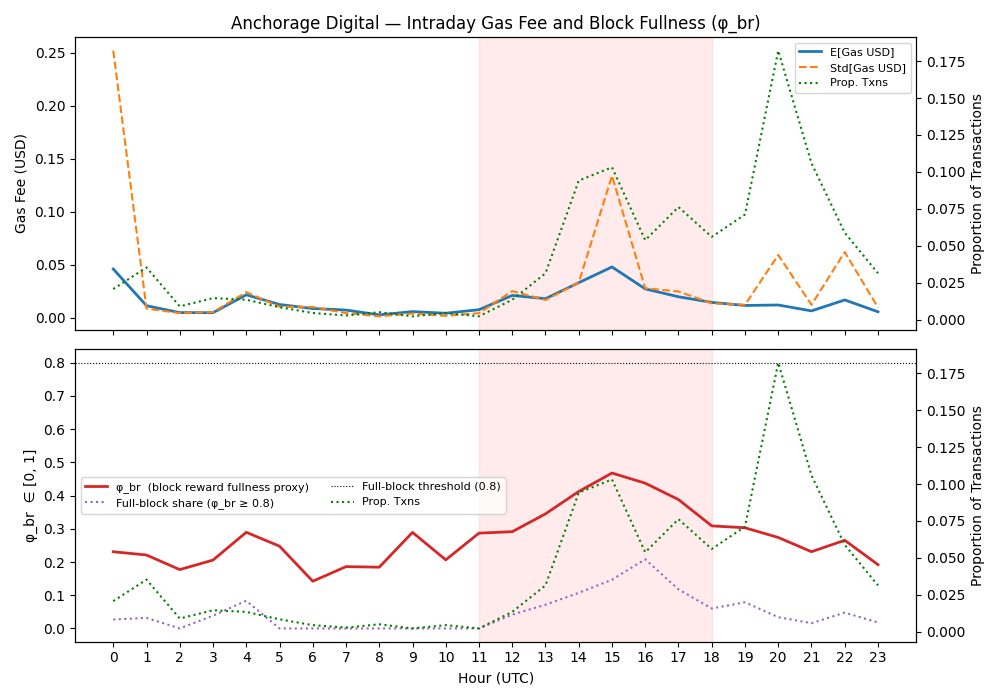

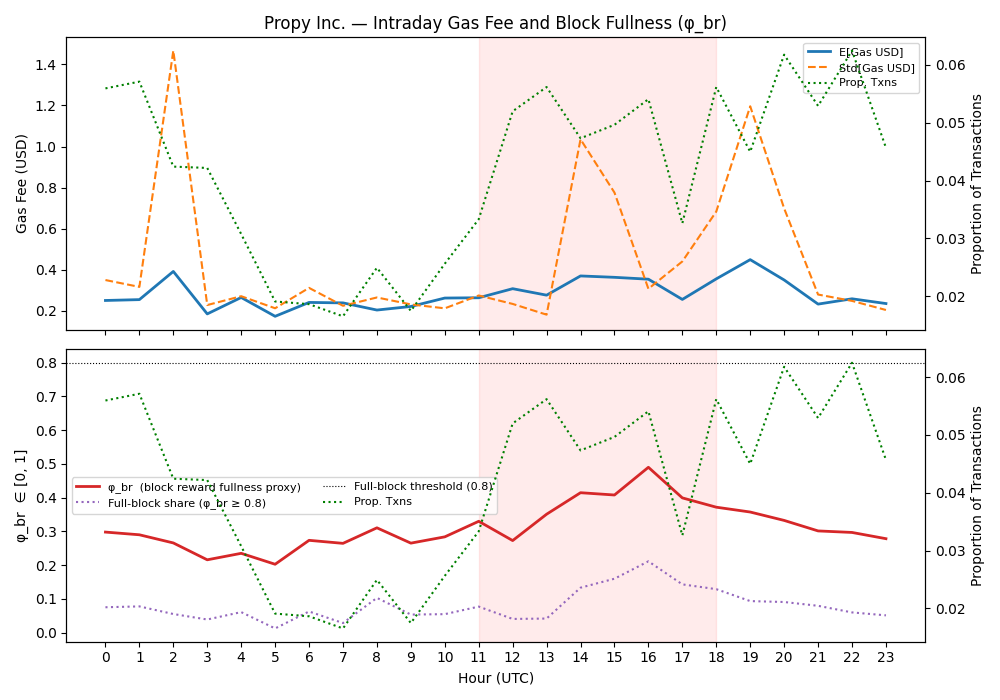

Critically, avoidance behavior is heterogeneous. Firms such as Coins.ph (remittance, high frequency/deferrability), Solve.Care (healthcare, operational flexibility), and Nike/Ondo (tokenized equity, event-driven but low volume) effectuate pronounced off-peak concentration (positive Peak Shaving Scores, PSS). By contrast, Propy (real estate closures), Anchorage Digital (institutional settlement, regulatory T+1 adherence), BrainTrust, and Morpheus.Network operate under substantial external timing constraints and obtain only marginal schedule-driven fee mitigation.

Figure 2: Coins.ph demonstrates strong off-peak scheduling discipline, aligning low transaction costs with hours of peak transaction activity.

Figure 3: Anchorage Digital exhibits higher costs and transaction clustering in peak hours due to regulatory/settlement-driven timing rigidity.

Figure 4: Propy, as a real estate platform, faces episodic high-gas transactions tightly coupled to operational deadlines, with moderate capacity for peak avoidance.

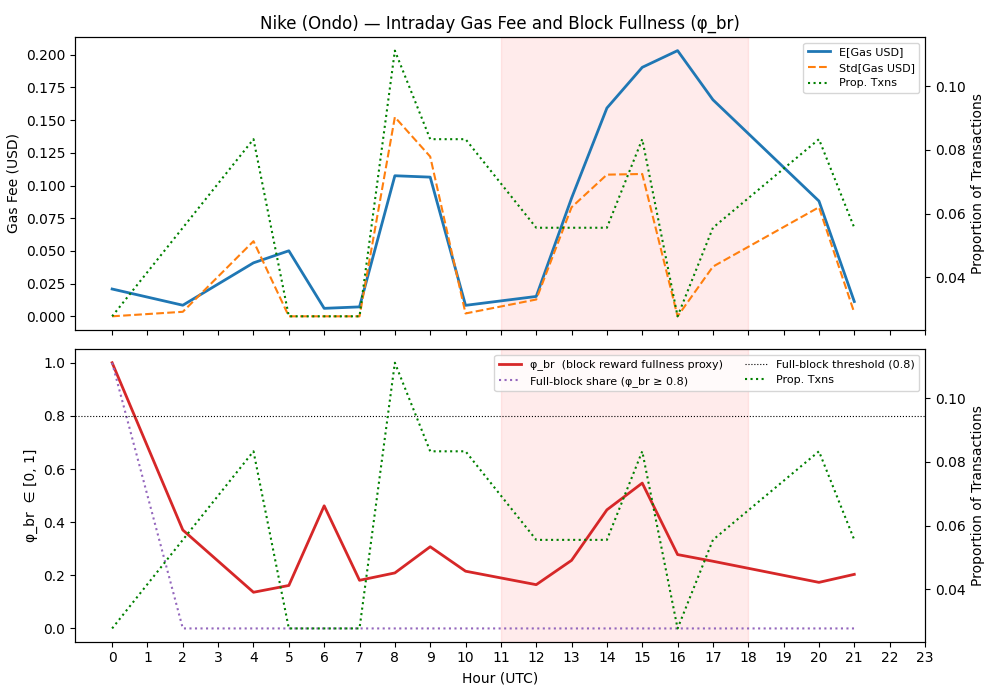

Figure 5: Nike (Ondo), a tokenized instrument, is primarily event-driven with unconstrained timing, resulting in low volume and high residual cost floor.

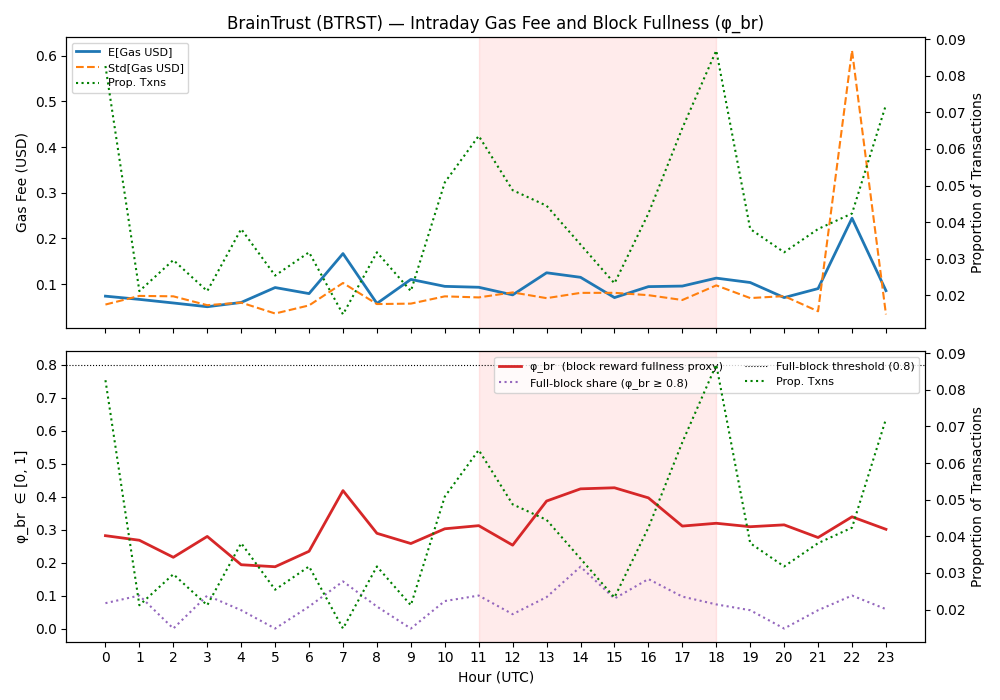

Figure 6: BrainTrust is governed by governance/payroll cycles, resulting in counter-cyclical scheduling with significant peak-hour cost exposure.

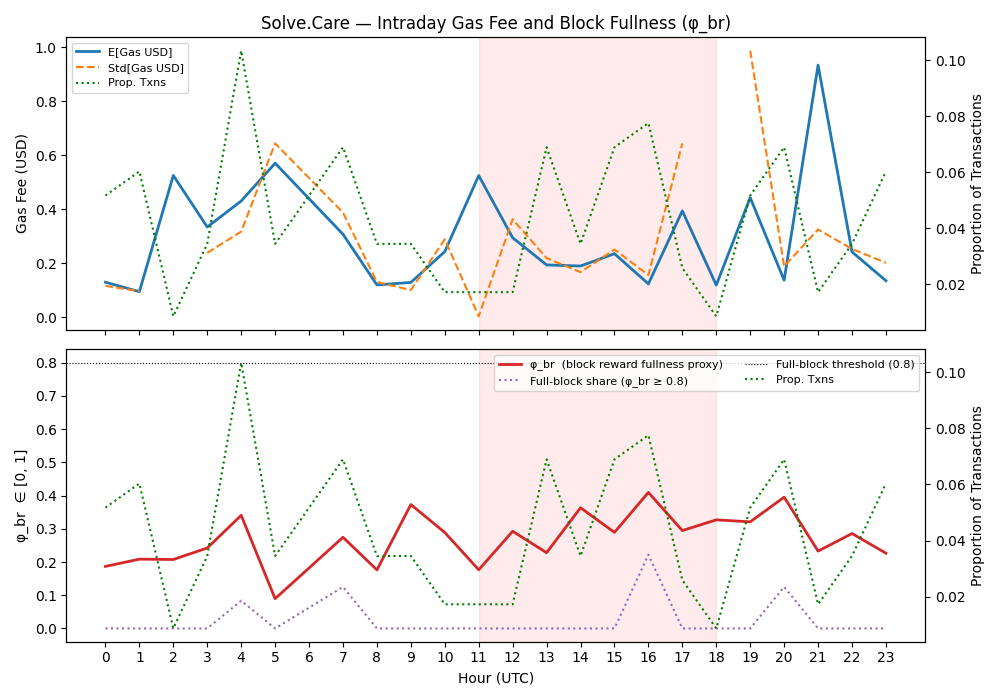

Figure 7: Solve.Care, a healthcare platform, shows peak-shaving behavior with scheduling flexibility that minimizes fee exposure.

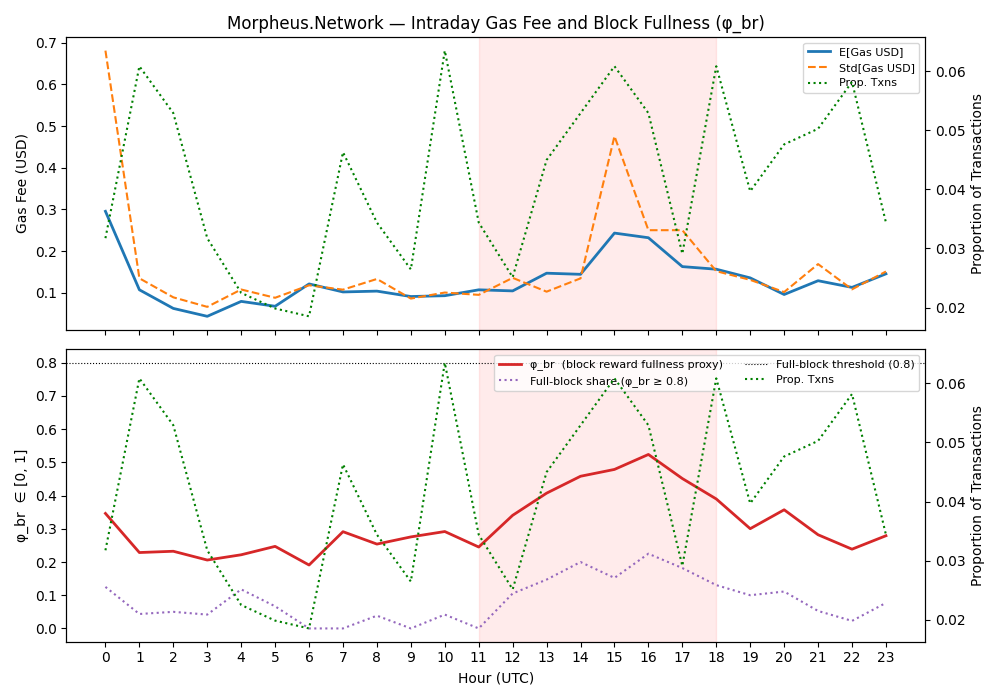

Figure 8: Morpheus.Network, a supply-chain solution, sits in the high-gas, partially deferrable quadrant, achieving moderate fee reduction through partial scheduling control.

Quantitative Findings: Fee Dynamics, Residual Cost Floors, and Scheduling Matrix Implications

The empirical findings are quantitatively robust:

- Peak-hour premium is persistent and driven by externalities generated by speculative actors, with the 10am ET window carrying the dominant tail risk for gas expenditure.

- Firm-level scheduling responses are sharply heterogeneous. Peak Shaving Scores (PSS) are positive only for three out of seven firms, aligning with high-deferrability and/or flexible operational footprints. The other four exhibit counter-cyclical or peak-constrained timing, due variously to regulatory/timeline requirements or governance cycles.

- Residual cost floors are large and ineliminable through schedule optimization alone. Even optimally disciplined firms retain residual cost burdens ranging from 40.7% to 92.5% of actual expenditure, as block fullness from speculative demand persists during all hours.

- Pass-through coefficients for congestion are tightly correlated with asset specificity: transactions featuring high asset specificity (e.g., real-estate contracts) absorb a greater share of block-level congestion premiums, while low-specificity, commoditized flows (e.g., ETH transfers) are partially insulated.

- Peak-shaving discipline cannot fully arbitrage out execution cost floors; network externalities are non-contractible, and order flow sparseness (episodic, deadline-constrained) precludes perfect off-peak submission.

These dimensions are synthesized in the On-Chain Scheduling Matrix, with clear operational regimes prescribed depending on gas intensity (git) and deferrability (dit):

|

High Gas Intensity (git>gˉ) |

Low Gas Intensity (git≤gˉ) |

| High Deferrability (dit=1) |

I. Full peak shaving: schedule to cheapest windows |

II. Selective peak shaving: economics-driven scheduling |

| Low Deferrability (dit=0) |

III. Cost provisioning: forecast/hedge cost spike |

IV. Accept market rate: focus on ex-ante optimization |

Practical and Theoretical Implications

Operationally, the paper reconceptualizes blockchain cost management: rather than static, externally imposed friction, gas fees become a forecastable, potentially hedgeable input cost, akin to real-time electricity procurement or FX risk management. This requires deployment of systematic timing, potentially automated or batched scheduling, and explicit cost provisioning for non-deferrable flows. The evidence refutes the notion that blockchain eliminates operational friction post-adoption; rather, it shifts the cost boundary to the execution phase, with substantial cross-industry heterogeneity.

Theoretically, the dual-classification of gas fees maps a novel cost category (timing execution/maladaptation origin) onto TCE, warranting a new analytic lens distinct from both deterministic IT cost reduction and classic asset-specific bilateral maladaptation. This analytic refinement can generalize to other public digital infrastructures exhibiting endogenous, price-responsive congestion costs (Layer-2 solutions, cross-chain bridges, etc.), and also calls for integration with behavioral OM research on managerial cognition under uncertainty in algorithmic markets.

Future research should examine the potential for Layer-2 diffusion to compress the intraday peak, the effect of market structure evolution on speculative demand persistence, and managerial adaptations (including automated scheduling agents). Environmental externalities (e.g., per-transaction energy/cost coupling), and microstructure effects in high-frequency vs. episodic order flow environments, also warrant priority study.

Conclusion

"On-chain Peak Shaving" (2604.19956) establishes that systematic transaction scheduling can quantifiably reduce (but not eliminate) fee exposure in public blockchain systems. The operational and theoretical advancements—an extended TCE cost taxonomy, explicit scheduling matrix, and robust cross-industry measurement of avoidance behavior and residual floors—position gas-fee management as a core OM concern for blockchain adoption, on par with energy and FX cost governance. The findings decisively shift the blockchain operations discourse from deterministic cost reduction to dynamic, strategically moderatable cost management.