- The paper introduces a structural econometric framework that uses transaction-level mempool data to recover the mapping from fee rate to confirmation delay.

- The paper employs a two-stage semiparametric estimation strategy combining random forests and isotonic regression to quantify the delay gradient and its impact on fees.

- The paper finds that dynamic congestion and VCG-like allocation drive fee levels, with practical implications for improving fee recommendation systems.

A Structural Model and Estimation Framework for Bitcoin Transaction Fees

Introduction and Theoretical Framing

This paper presents a structural econometric framework to model Bitcoin transaction fee formation, leveraging transaction-level mempool data and tools from mechanism design. The investigation is motivated by the declining relative importance of Bitcoin's protocol-level block subsidy, necessitating increased reliance on transaction fees as the primary security and liveness incentive for miners. Existing empirical work is hindered by the lack of direct observation of the relevant queueing environment at the time of fee selection, resulting in incomplete models of fee-setting behavior. This work addresses that gap by constructing a high-frequency panel using a self-hosted Bitcoin node, tracking fine-grained mempool and transaction state, and implementing market design theory to empirically recover the mapping from priority (as implemented via fee rate) to confirmation delay.

The theoretical backbone interprets the Bitcoin mempool as a decentralized implementation of a Vickrey-Clarke-Groves (VCG) allocation for priority service, enabling a direct link between observed fees and delay externality pricing. Transaction fees are posited to reflect the product of user impatience, the marginal reduction in confirmation delay per unit increase in fee-based priority, and transaction weight.

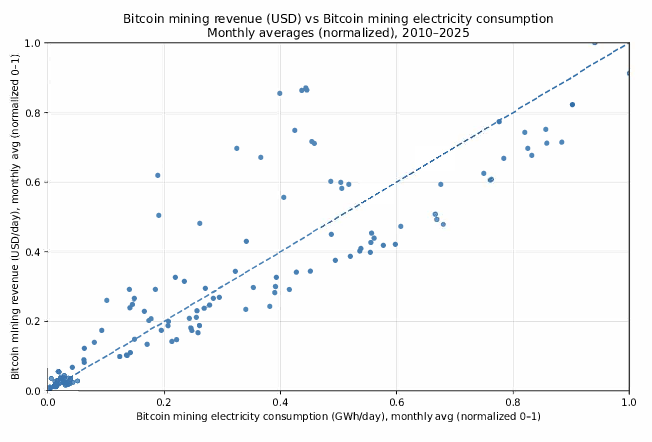

Figure 1: Empirical relationship between block reward value and aggregate electricity use, illustrating the economic incentives shaping Bitcoin mining and, by extension, transaction fee dynamics.

Data Construction and Measurement

A novel transaction-level mempool panel is assembled, capturing transaction arrival, exit, inclusion (block assignment), fee-bump events (both Replace-By-Fee and Child-Pays-For-Parent), and mempool congestion snapshots at 25-second frequency. The resulting dataset enables precise reconstruction of the queueing environment each transaction actually faced—a requirement for structurally identifying the fee-confirmation delay schedule.

Key variable engineering includes:

- blockspace utilization (fraction of a block occupied at transaction entry),

- mempool size and depth (bytes and transaction count),

- priority percentile (fee rate rank among contemporaneous pending transactions, with tie-aware sorting),

- CPFP package collapsing (grouping of parent–child transaction chains to compute effective package-level fee rates), and

- detailed transaction-type annotation.

Econometric Model and Estimation Strategy

The estimation strategy leverages a two-stage, semiparametric approach:

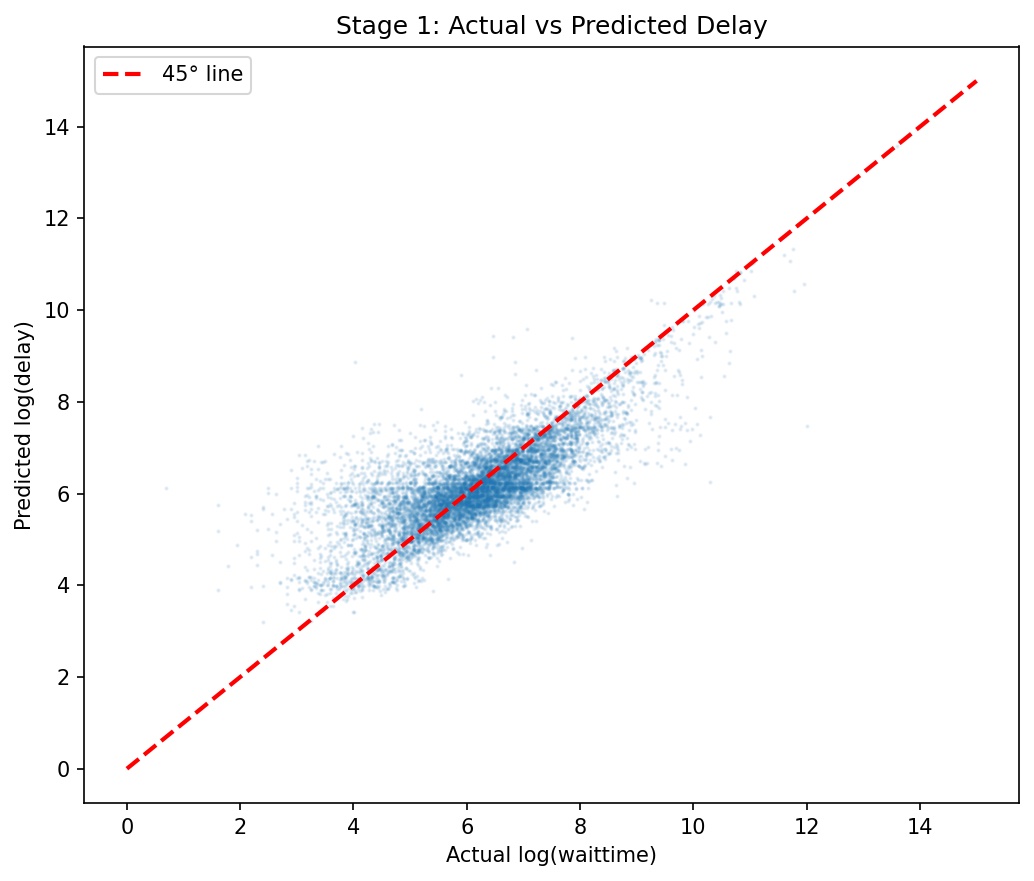

- Stage 1: The expected confirmation delay W(p,s) is flexibly estimated as a function of priority percentile p and network state s using random forest regressors. Monotonicity in priority is enforced post-hoc via isotonic regression on forest predictions, and the local slope of the delay schedule (∂W/∂p) is extracted using symmetric finite differences.

Figure 2: Actual vs. predicted log(waittime), demonstrating the accuracy of the random forest model for delay prediction.

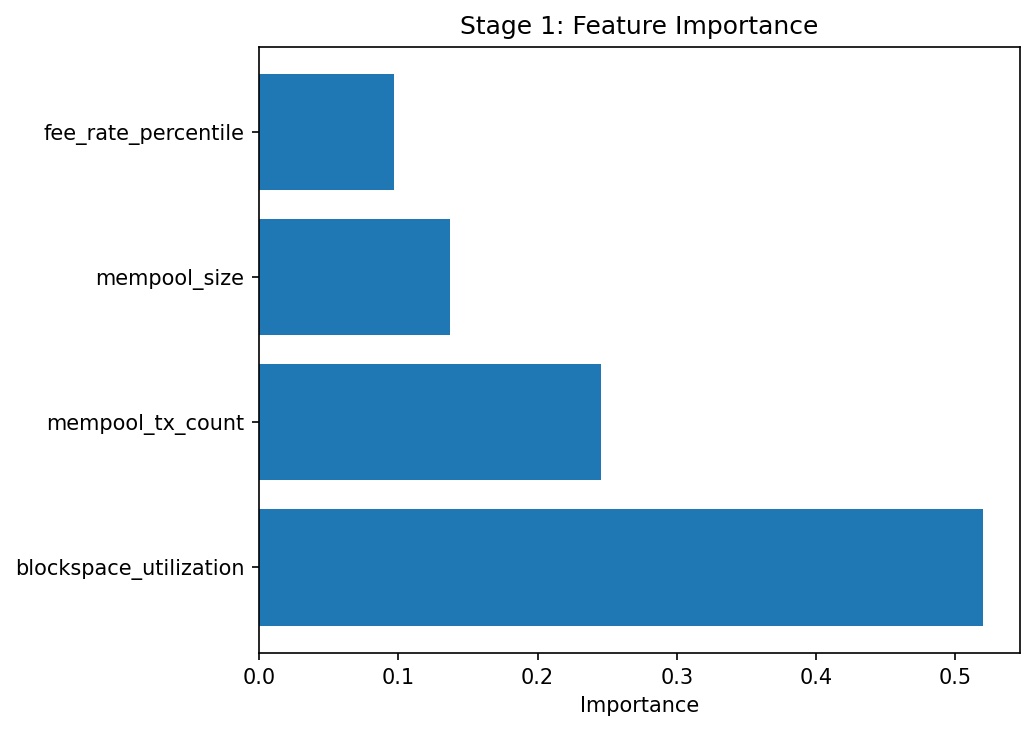

Figure 3: Feature importances from the Random Forest; blockspace utilization and mempool depth dominate confirmation delay.

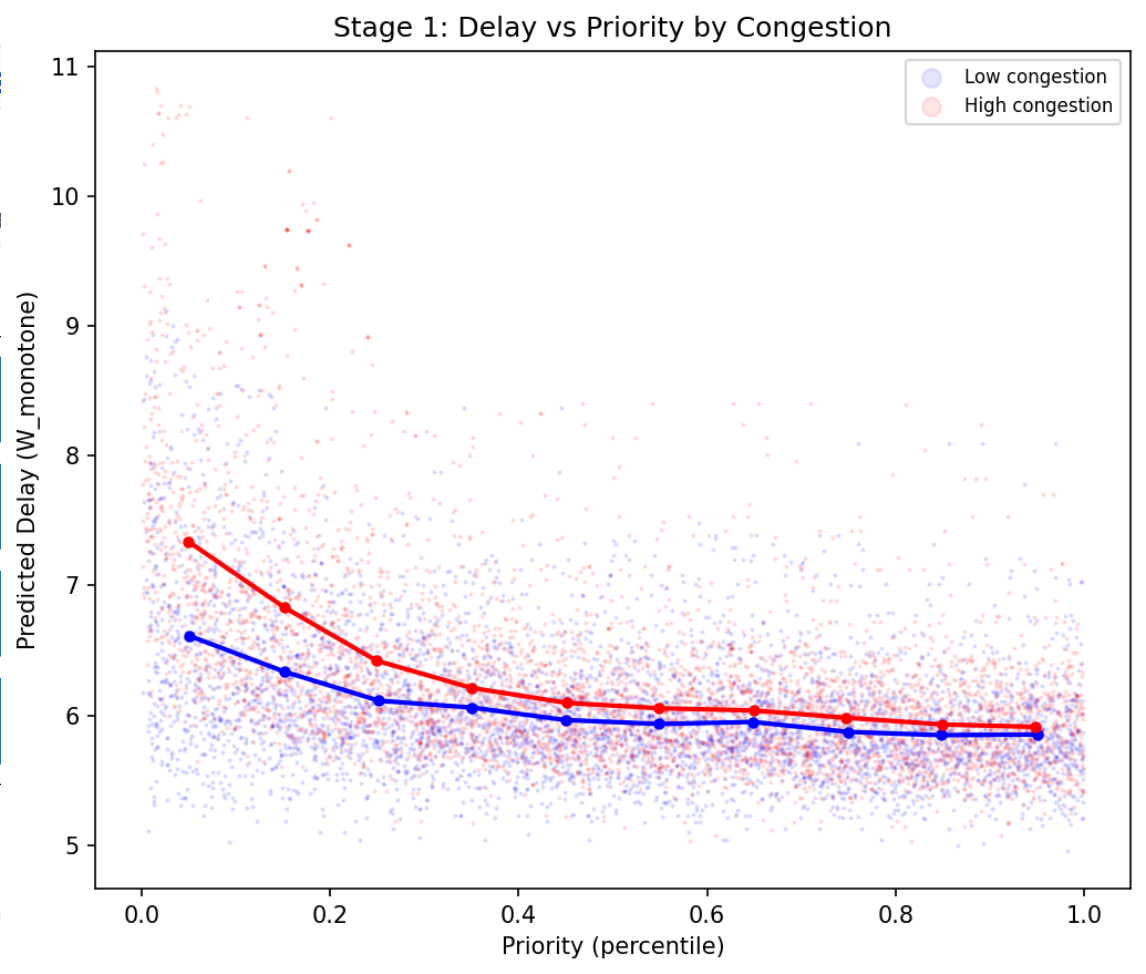

Figure 4: Delay–priority relationship across congestion regimes; delay gradient is actively steep only under congestion.

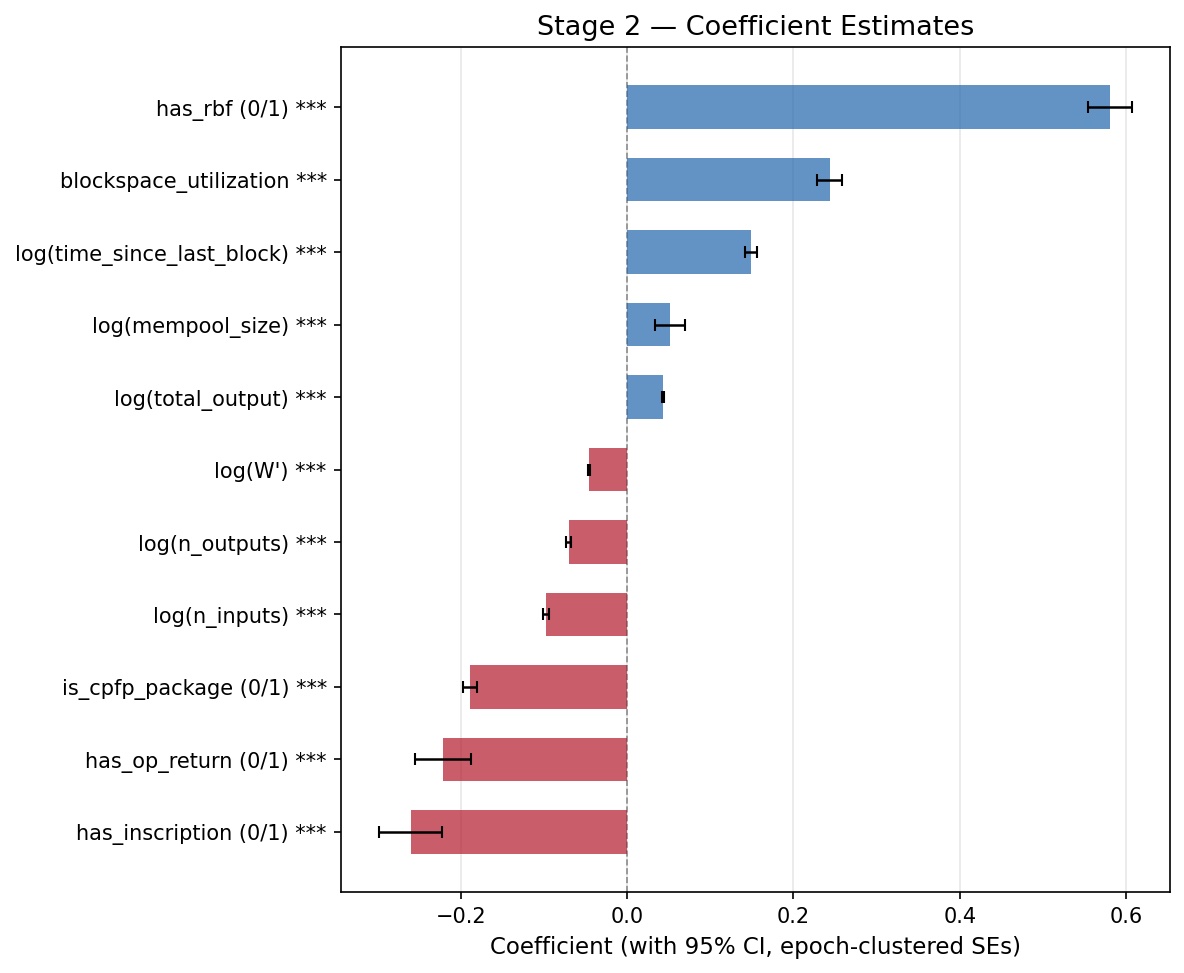

- Stage 2: The log fee rate is regressed on the log delay gradient, transaction controls (including RBF, CPFP, transaction structure), and high-frequency blockstate covariates, with epoch fixed effects to absorb persistent aggregate congestion. User impatience, proxied by future re-spend intervals, is modeled as a monotone spline component but does not drive results.

Key Empirical Results

The model identifies that congestion, as measured by blockspace utilization and mempool volume, is the primary determinant of confirmation delay, and consequently of transaction fees. The delay schedule is steep in high congestion, so marginal increases in priority provide substantial expected delay reductions, and users rationally pay higher fees during such episodes.

Among the strong empirical findings:

Control for user impatience yields a small, directionally consistent but economically minor positive effect on fees, suggesting that observable urgency proxies are weak in explaining cross-sectional fee variation once the delay gradient is accounted for.

Model diagnostics confirm:

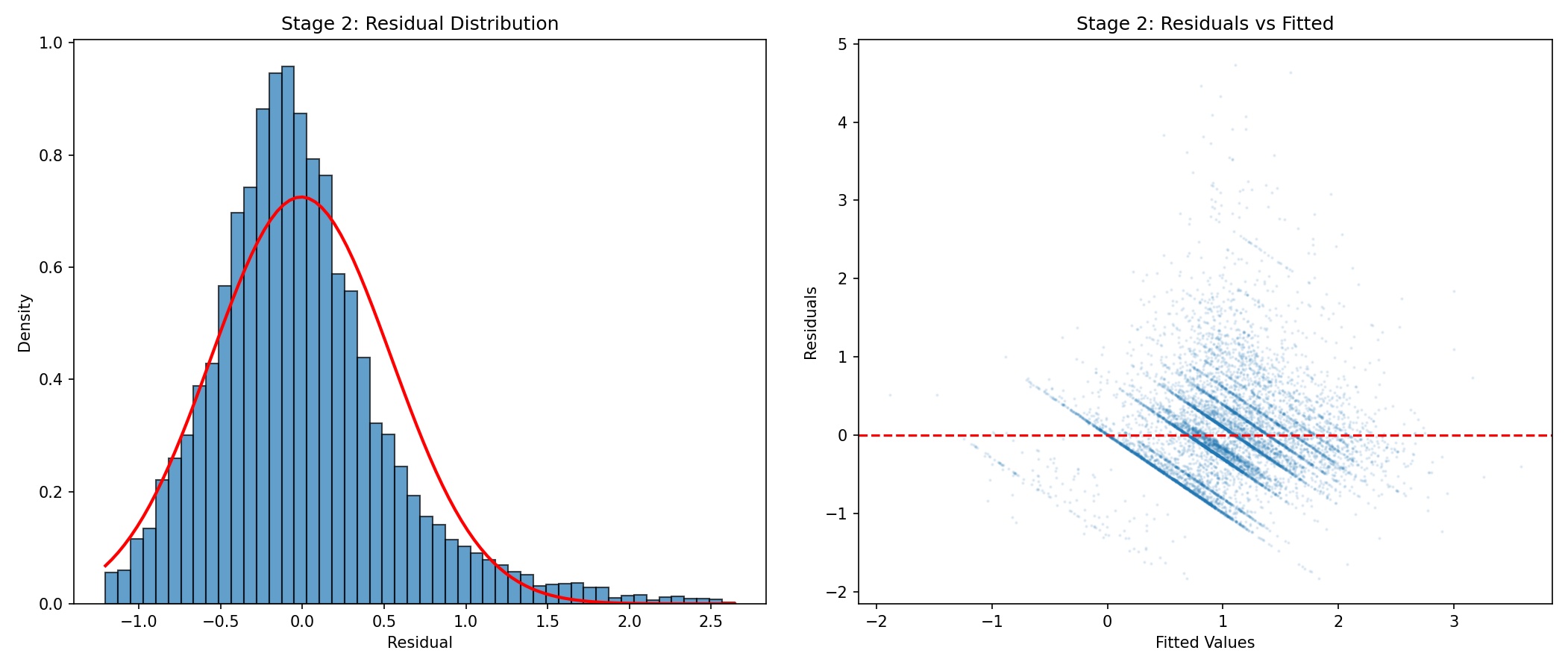

- Strong model fit throughout the transaction fee distribution, with underprediction biases only in the extreme right tail (largest fees).

- Clustered standard errors at the epoch level, correcting for substantial within-epoch correlation.

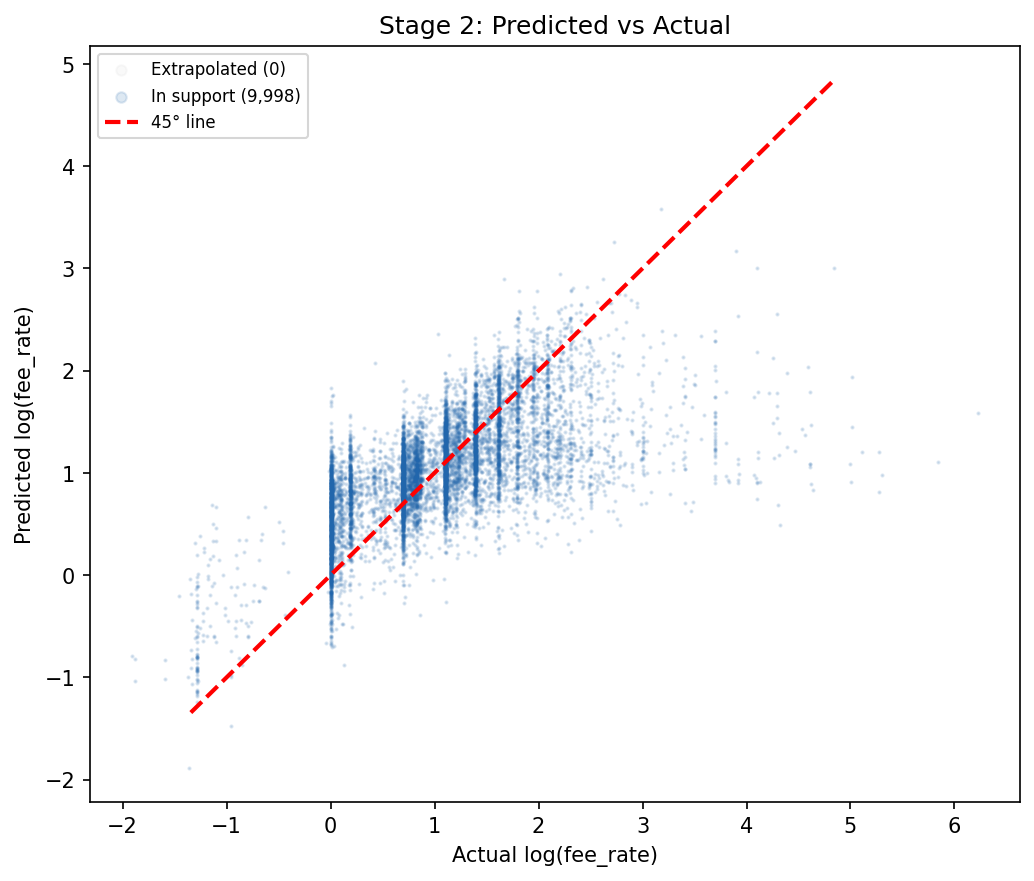

Figure 6: Actual vs. predicted log fee rates, confirming strong model fit (10,000 transactions sampled).

Figure 7: Residual analysis; left: density with normal overlay, right: residuals vs. fitted values.

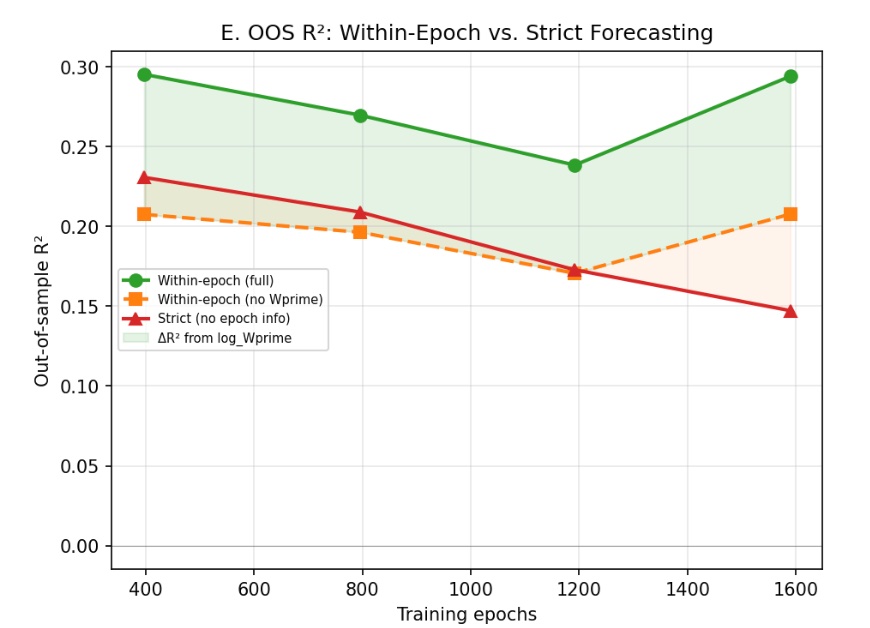

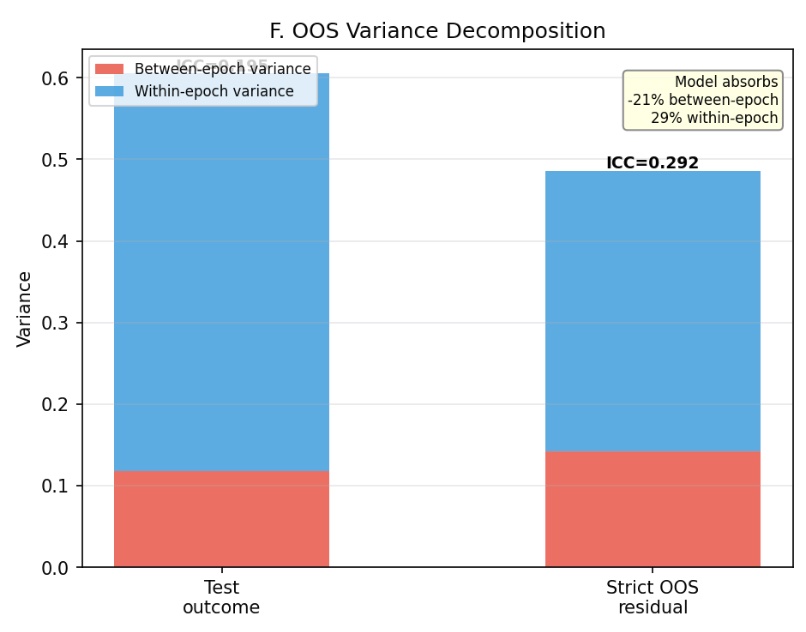

The model's within-epoch, cross-sectional explanatory power is strong and robust across time windows and out-of-sample splits. The delay-gradient channel consistently adds 7–9 percentage points of R2 within epochs even in strict OOS prediction. However, the model does not explain epoch-level fee regime shifts; aggregate fee level variation across time periods remains largely absorbed by fixed effects, not observable congestion or blockstate features.

Figure 8: Out-of-sample R2 learning curves under multiple evaluation protocols; the shadowed wedge quantifies the explanatory contribution of the delay gradient term.

Figure 9: Variance decomposition demonstrates the model's strength is in cross-sectional (within-epoch) explanation rather than prediction of epoch-level mean fees.

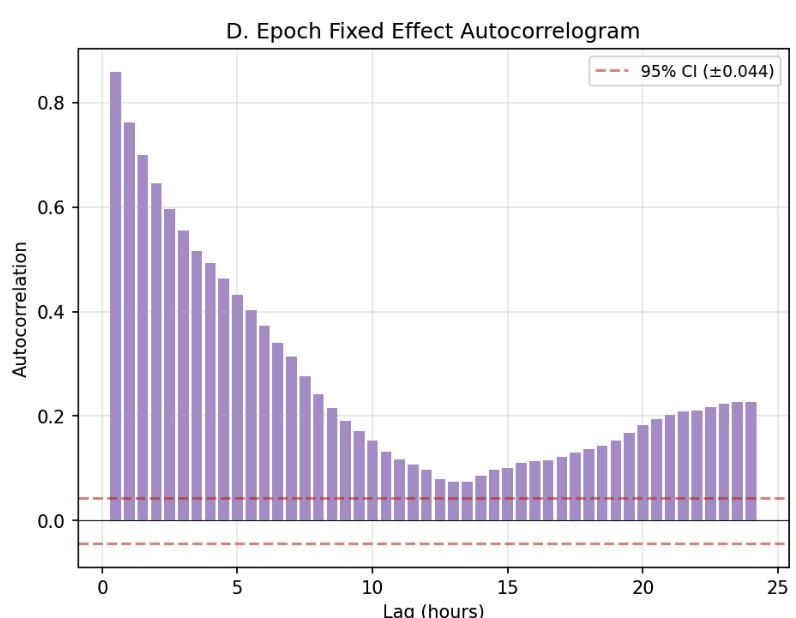

Figure 10: Autocorrelation in epoch fixed effects indicates slow reversion of aggregate congestion.

Theoretical and Practical Implications

This work provides empirical validation of mechanism design theory as applied to Bitcoin mempool economics: the decentralized, fee-based, miner-prioritized mempool closely implements a VCG-like allocation and payment mechanism. The most direct implication is that fee-setting can best be understood as the pricing of priority under state-dependent congestion, not merely as a function of aggregate demand, arbitrary willingness-to-pay, or “fee estimation” heuristics.

On a practical level, fee estimation algorithms can be improved by:

- Focusing on local delay gradients extracted from mempool data,

- Incorporating institutional transaction details (such as CPFP and RBF flags),

- Conditioning predictions on contemporaneous blockspace utilization and mempool depth.

This framework enables disciplined counterfactuals under hypothetical congestion states, potentially informing both wallet fee recommendation logic and future protocol design for blockspace pricing and allocation.

On the theoretical side, the finding that impatience, as measured by future output re-spend, is weakly connected to fee variation (contradicting earlier studies on pre-2015 data), points to substantial evolution in user- and application-level behavior and/or in the structure of fee estimation tools over time.

Limitations and Directions for Future Research

The primary empirical limitation is the data window—nine weeks—with little variation in truly extreme congestion regimes. This restricts the potential to identify temporal dynamics or parameter drift in the delay gradient's effect on pricing, and limits extrapolation to future fee-market regimes (e.g., under further subsidy halvings or protocol changes). Continued extension of the transaction-level mempool panel will support more robust time series inference and regime-switching analyses.

A further avenue opened by the approach is structural modeling of block assembler (miner) behavior, including testing for strategic mining (e.g., delayed inclusion, soft-collusion, side-channel fee negotiation), which would appear as systematic violations of the priority-to-delay mapping.

Conclusion

This paper presents a structural estimation of Bitcoin transaction fee formation grounded rigorously in mechanism design and operationalized via a novel high-frequency panel of the mempool state. It demonstrates that dynamic congestion, not static willingness-to-pay, is the principal determinant of fees; that VCG logic is empirically operative; and that institutional design features such as RBF, CPFP, and blockspace metrics meaningfully modulate fee schedules. The approach provides both practical insight for fee estimation strategies and theoretical grounding for understanding blockspace as a congested, priced digital resource.