- The paper proposes a deterministic model capturing multi-asset dynamics and heterogeneous investor behavior to identify stability conditions and bifurcation thresholds.

- It utilizes coupled ODEs and Jacobian analysis to demonstrate how momentum parameters trigger Hopf bifurcations and price oscillations in oil and gas markets.

- Numerical simulations validate model predictions by illustrating wealth redistribution and limit cycle dynamics for value versus momentum investor groups.

Multi-Asset Market Dynamics with Heterogeneous Investor Groups: A Technical Analysis

Model Structure and Microeconomic Foundations

The paper "A Microeconomic Finance Model with a Multi-Asset Market and a Multi-Investor Heterogeneous Groups" (2604.15220) develops a deterministic dynamical systems model for financial markets comprising m assets and n investor groups, generalizing prior two-asset, single-group frameworks. Each asset market is closed (fixed cash and shares), and investor groups are characterized by distinct behavioral strategies: value-based (valuation relative to fundamental price), trend-based (momentum), or mixed. Notably, buying decisions for each asset depend on the prices of other assets, whereas selling remains asset-specific, reflecting asymmetric cross-asset interaction.

Investor preferences are encapsulated by sentiment variables: trend sentiment ζ1,j(i) and value sentiment ζ2,j(i), governed by coupled first-order ODEs. Transaction rates (kj(i) for buying, k~j(i) for selling) are defined as bounded nonlinear functions of these sentiments, incorporating group-specific time-scales and sensitivities. The market price for asset i evolves according to excess demand, and wealth fractions for each investor group are tracked. The approach ensures asset price coupling both via investor strategy and explicit cross-asset dependence in purchasing rates.

Analytical Stability and Bifurcation Results

The equilibrium analysis identifies explicit fixed points where all asset prices are at their respective fundamental values (P(i)=Pa(i)), and all sentiment variables vanish. The transition rates at equilibrium are functions of zero sentiment, with market clearing enforced via calibration. Linear stability is characterized via the full Jacobian matrix—m+2mn dimensional with block structure—that couples the price and sentiment dynamics.

Theorem 1 establishes stability for homogeneous value investors: under zero momentum sensitivity (q1,j(i)=0), positive responsiveness to value sentiment, and negligible cross-asset coupling, the fundamental equilibrium is locally asymptotically stable. Diagonal dominance and negative real parts of all eigenvalues follow analytically via Gershgorin circle theorem and characteristic polynomial criteria.

Theorem 2 extends this result to mixed strategy populations (value and trend investors): stability is retained if trend-following sensitivity (n0) and sentiment adjustment rates (n1) are sufficiently small, and cross-group/asset couplings remain weak. If momentum parameters surpass explicit thresholds, instability manifests via a Hopf bifurcation—deterministically generating limit cycles of growing amplitude and endogenous price oscillations independent of external shocks.

Numerical Simulations: Multi-Asset Oil and Gas Markets

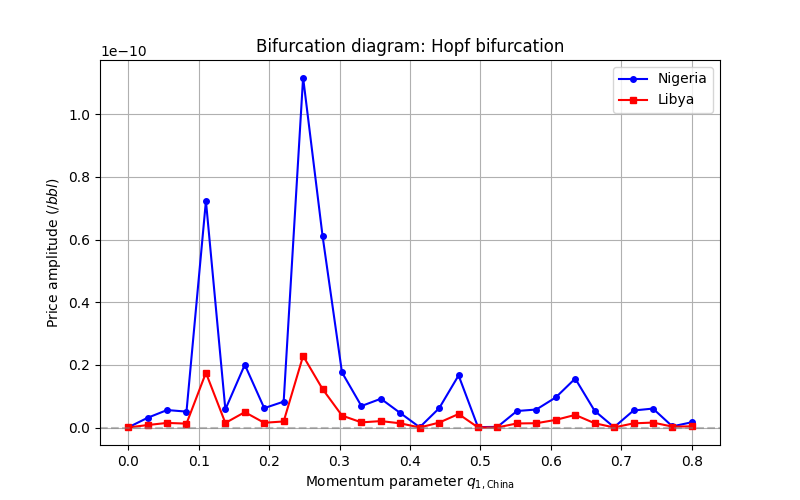

The model’s practical implications are demonstrated through two-asset (Nigeria, Libya) simulations with USA (value investor) and China (momentum trader) as investor groups. The bifurcation diagram (Figure 1) explicates the critical threshold for China’s momentum parameter n2: below n3, the system converges to fundamental prices; above, price amplitude grows continuously via supercritical Hopf bifurcation.

Figure 1: Bifurcation diagram for the two-asset oil market, showing price oscillation amplitude as a function of the momentum parameter n4.

Detailed time series (Figure 2) confirm stable limit cycle dynamics for n5: prices oscillate around n6 with n75amplitude,andwealthfractionsareperiodicallyredistributed.Valuesentimentstabilizesfundamentalequilibrium;trendsentimentdrivesphase−correlatedpricefluctuations.<imgsrc="https://emergentmind−storage−cdn−c7atfsgud9cecchk.z01.azurefd.net/paper−images/2604−15220/nigerialibya2.png"alt="Figure2"title=""class="markdown−image"loading="lazy"><pclass="figure−caption">Figure2:Oilpricetimeevolution,valuesentiment,andinvestorwealthfractions,illustratingperiodiclimitcyclesinducedbymomentumtrading.</p></p><p>Furtheranalysis(Figure3,Figure4,Figure5)revealsthatinstableregimes,wealthfractionsarestationary,whereasinoscillatoryregimes,distributionsexhibitperiodicstructure—confirmingendogenouswealthtransferasadirectoutcomeoftrend−followinginstability.<imgsrc="https://emergentmind−storage−cdn−c7atfsgud9cecchk.z01.azurefd.net/paper−images/2604−15220/wealthfractionchinausa.png"alt="Figure3"title=""class="markdown−image"loading="lazy"><pclass="figure−caption">Figure3:TimeevolutionofwealthfractionsforUSAandChinainthegasmarketsimulation,convergingtoastablesteadystate.</p><imgsrc="https://emergentmind−storage−cdn−c7atfsgud9cecchk.z01.azurefd.net/paper−images/2604−15220/usawealthniglyb.png"alt="Figure4"title=""class="markdown−image"loading="lazy"><pclass="figure−caption">Figure4:WealthdistributionofUSA(valueinvestor)intheNigeria−Libyaoilmarketwithn8,showingequilibriumfractionandnear−zerovariance.</p><imgsrc="https://emergentmind−storage−cdn−c7atfsgud9cecchk.z01.azurefd.net/paper−images/2604−15220/wealthchinaniglyb.png"alt="Figure5"title=""class="markdown−image"loading="lazy"><pclass="figure−caption">Figure5:WealthdistributionofChina(momentumtrader)intheNigeria−Libyaoilmarketwithn$9, confirming stable wealth fraction distribution.

Implications for Market Stability and Future Directions

The deterministic multi-asset, multi-group modeling provides a rigorous framework for endogenous price oscillations, periodic wealth transfer, and parameter-regulated bifurcations absent in classical stochastic models. The structure allows explicit identification of instability regimes—where momentum traders dominate—offering technical insight for market regulation (e.g., policies restricting trend-following to mitigate destabilization).

Practically, the model enables simulation and prediction of regime shifts, volatility clustering, and synchronized asset dynamics. Theoretical implications include the ability to generalize bifurcation analysis across arbitrary asset and investor dimensions, supporting robust mathematical exploration of contagion, persistence, and cyclical behavior.

Limitations include static asset and cash allocation, fixed strategic preferences, and constant fundamental values. Integration of adaptive strategy selection, time-varying fundamentals, and stochastic perturbations constitute critical extensions. Empirical calibration and application to high-frequency or real-world multi-asset markets would further validate and refine the model’s predictive capabilities.

Conclusion

The paper synthesizes prior asset flow and heterogeneous agent models into a comprehensive deterministic framework capable of capturing complex market dynamics. Strong analytical results demonstrate conditions for stability and critical bifurcation thresholds. Numerical simulations validate key predictions regarding price cycles and wealth distribution, emphasizing the practical and theoretical relevance for understanding and managing multi-asset financial markets. Future research should focus on adaptive strategies, empirical calibration, and integration of stochastic dynamics to enhance realism and applicability.