- The paper establishes a necessary and sufficient condition linking global stability to asymptotic contractivity and tight trajectories.

- It derives explicit exponential convergence rates in compact settings using the Bhattacharya metric to sharpen monotone mixing results.

- The framework is applied to economic models including wage dynamics, Bayesian learning, and income processes with heavy-tailed distributions.

Stationary Distributions in Monotone Markov Models: Theory and Applications

Overview and Main Theoretical Contributions

The paper "Stationary Distributions in Monotone Markov Models: Theory and Applications" (2604.03979) provides a unified framework for existence, uniqueness, and global stability of stationary distributions in monotone Markov processes, accommodating both compact and noncompact state spaces, discrete and continuous time models, and allowing for linear and nonlinear Markov operators. The key theoretical advance is a necessary and sufficient condition: a monotone Markov process is globally stable (in the sense of having a unique, globally attracting stationary distribution) if and only if it is asymptotically contractive and has a tight trajectory.

This is formalized in an abstract fixed point theorem: for any order-preserving semigroup on a complete preordered metric space with the diagonal property, global stability is equivalent to asymptotic contractivity plus existence of an order-bounded trajectory. The Bhattacharya metric on the space of probability measures is pivotal in verifying the diagonal property and closedness of stochastic dominance, tying tightness to order-boundedness and enabling generalization beyond prior compactness assumptions.

Advances over Existing Literature

Previous work, notably [hopenhayn1992stochastic], was built around the notion of monotone mixing and required compact state spaces with extremal elements, limiting the applicability to real economic settings featuring unbounded states and heavy-tailed stationary distributions, such as Pareto tails in income and wealth. Extensions using tightness and partial monotonicity (e.g., [kamihigashi2014stochastic], [foss2024compressibility]) were non-unified and included additional sufficiency conditions.

This paper supersedes those by (i) establishing a simple equivalence between global stability and asymptotic contractivity plus tightness, and (ii) elegantly covering discrete and continuous time, compact and noncompact spaces, and both linear (standard Markov operators) and nonlinear (aggregate-dependent) operators.

Explicit Exponential Stability in Compact Settings

Within compact state spaces, the paper recovers and sharpens the monotone mixing results of [hopenhayn1992stochastic], notably by producing explicit exponential convergence rates for distributions under the Markov semigroup. Theorem~2 establishes:

β(ϕPt,ϕ∗)≤Ce−αt

with rate constants dependent on model primitives, where β is the Bhattacharya metric and ϕ∗ the stationary distribution. In discrete time, monotone ergodicity for bounded increasing observables is also proved.

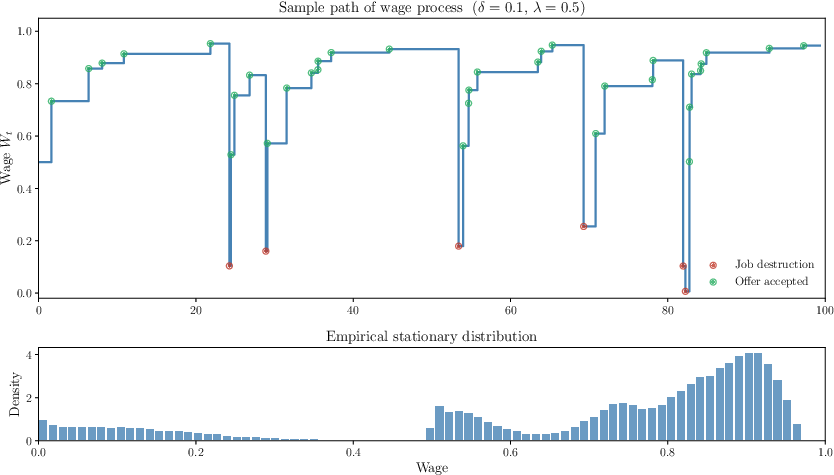

Figure 1: Stationary dynamics and convergence of the continuous-time job ladder wage model under state-dependent offers and monotone mixing.

Applications: Economic Models and Heavy-Tailed Stationarity

Wage Dynamics on a Job Ladder

Applying the theory, the authors generalize the continuous-time job ladder model with state-dependent wage offers and job destruction risk. Unlike standard models, stochastic kernels are allowed to be monotone but not homogeneous, and exponential stability of the wage distribution is guaranteed under minimal assumptions on the kernels, with verification via the monotone mixing condition. The simulated wage paths show empirical convergence to the stationary distribution, and the methodology allows handling of ergodicity without compactness constraints.

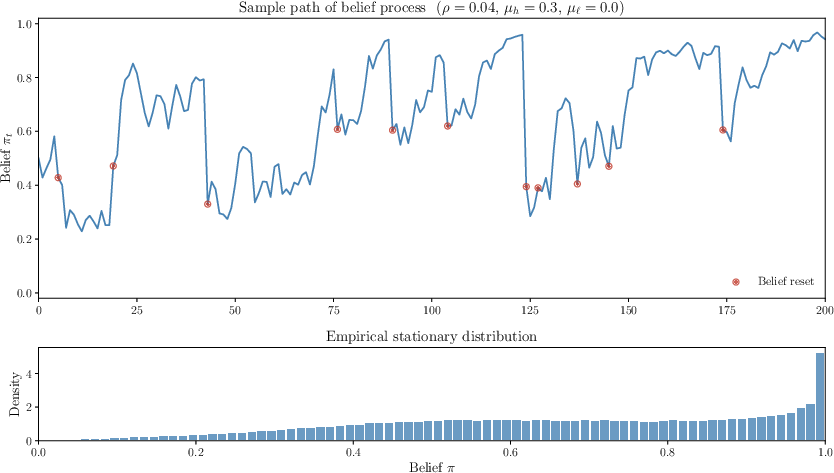

Bayesian Learning with Belief Shocks

For noncompact state spaces in discrete time, the framework applies to models of Bayesian learning subject to belief shocks, which reset the agent's posterior and introduce persistent heterogeneity, relevant in macro-financial settings (countercyclical uncertainty, inflation expectation drift). Under minimal moment and tightness conditions on the shocks, global stability and ergodicity of the belief distribution is ensured without Feller continuity or existence of an excessive/deficient distribution. The essential property is order-reversing: the possibility of randomly reversing any initial stochastic order.

Figure 2: Evolution and stationary law of Bayesian beliefs under random belief shocks; note skewness from learning dynamics and shocks.

Income Processes with Pareto Tails

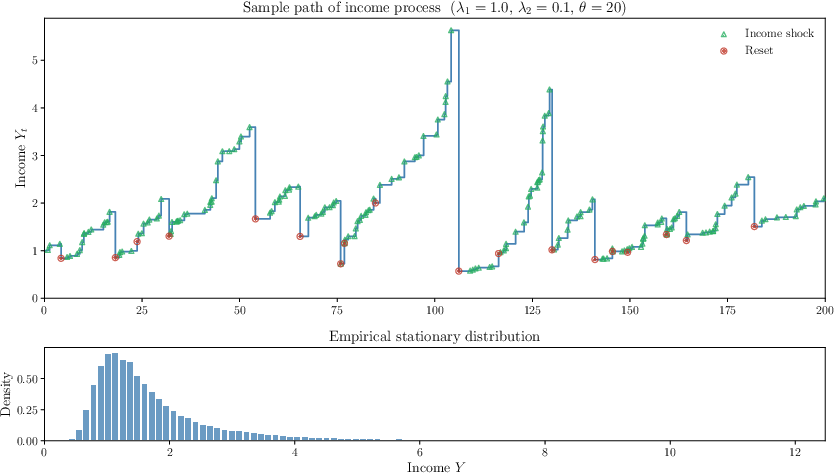

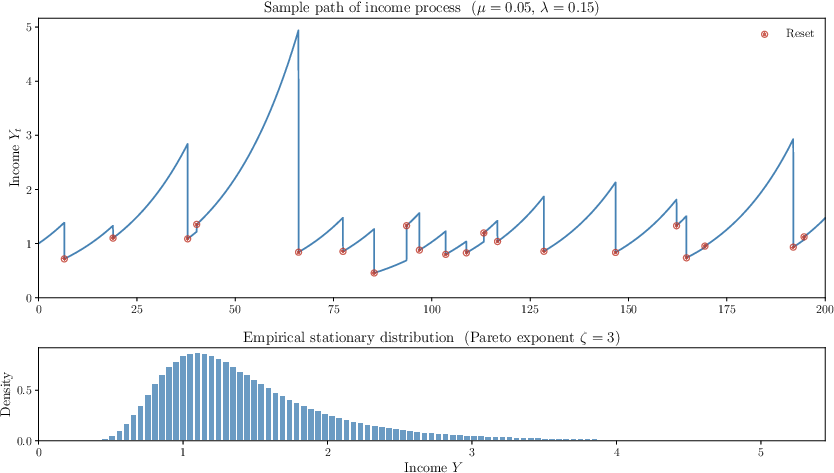

Continuous-time PDMPs (piecewise deterministic Markov processes) provide a flexible and analytically tractable framework for modeling individual income processes, with pure jump and drift+reset models treated in detail. For both, the framework yields necessary and sufficient conditions for stationarity and shows existence of Pareto tails analytically in certain settings. The coupling and monotonicity conditions replace the need for irreducibility/positivity, and the influence of model parameters on the Pareto tail exponent is made explicit.

Figure 3: Pure jump income model exhibiting heavy-tailed stationary distributions; resets and income shocks jointly determine the tail behavior.

Figure 4: Income model with deterministic drift and random resets; stationary distribution demonstrates Pareto law shaped by growth and reset intensity.

Implications and Technical Significance

The primary implication is methodological: criteria for stationarity in high-dimensional and/or noncompact monotone Markov models reduce to two verifiable properties, sidestepping case-by-case arguments and specialized irreducibility. This paves the way for analysis of heterogeneous-agent models with aggregate-dependent updating, models with endogenous entry/exit, and dynamic contracts under monotone transformations.

For practical modeling in economics and applied probability, the paradigm provides explicit, easily checked stability criteria, supports simulation-based estimation, and handles models generating empirical distributions with realistic heavy tails.

Theoretical implications extend to operator theory (fixed point theorems on preordered metric spaces), stochastic process theory (Markov semigroups beyond Feller/irreducible settings), and ergodic theory on noncompact spaces.

Future Directions

Potential avenues for extension include weakening mixing requirements (e.g., non-uniform jump intensities in PDMPs), extending order-boundedness methods to non-monotone or partially monotone systems, and further characterizing the robustness of Pareto tail exponents to perturbations in transition mechanisms. The techniques introduced around the tightness-order boundedness correspondence could prove useful in diverse settings with monotone stochastic recursions.

Conclusion

This work supplies a definitive, general criterion for global stability and uniqueness of stationary distributions in monotone Markov models, unifying and extending decades of research. The synthesis of contractivity and tightness, deployed in both theoretical form and in complex applications (wage, belief, income dynamics), makes the results broadly applicable and simplifies economic and probabilistic analyses using monotone Markovian frameworks.