- The paper introduces a novel variational framework that unifies entropic OT, Brenier–Strassen, and Bass problems through weak transport principles.

- It reformulates the Schrödinger–Bass problem as a semimartingale control model with an explicit dynamic-to-static equivalence via a specialized weak OT cost.

- A Sinkhorn-type algorithm is developed with rigorous convergence proofs, and asymptotic analysis recovers classical optimal transport limits.

A Weak Transport Approach to the Schrödinger–Bass Bridge

Introduction and Context

The paper "A weak transport approach to the Schrödinger-Bass bridge" (2604.02312) develops a comprehensive variational framework connecting several fundamental optimal transport (OT) paradigms via a parameterized family of semimartingale transport problems. These interpolate between classical entropic OT (the Schrödinger bridge), the static Brenier–Strassen problem, and, upon rescaling, the martingale Benamou–Brenier (Bass) problem. The analysis is set within the modern weak optimal transport (WOT) formalism, yielding both new structural insights and practical computational tools.

This approach is motivated by the need for a unified treatment of dynamical and static couplings between probability measures, especially in contexts where martingale constraints or additional process randomness are present. The authors emphasize an equivalence between the dynamic, process-level formulations and explicit static WOT forms. They further propose a Sinkhorn-type algorithm for computational solution, with rigorous asymptotic analysis for the connection between the limiting regimes.

The central object is the Schrödinger–Bass problem, a one-parameter family (β>0) of stochastic optimal transport problems. It seeks to minimize the action of paths (Xt)t∈[0,1] governed by Itô SDEs

dXt=atdt+btdBt,X0∼μ, X1∼ν,

where (at) is a drift and (bt) is a stochastic volatility process, B is a standard Brownian motion, and the objective functional is

E[∫0121∣at∣2+2β∣bt−I∣HS2dt].

This cost interpolates between the Schrödinger bridge (β→∞, volatility fixed), the Brenier–Strassen problem (β→0 without rescaling), and, after a proper rescaling, the martingale Benamou–Brenier (Bass) problem (β→0 with scaling).

Importantly, the authors provide an explicit equivalence between this dynamic problem and a static weak OT formulation:

(Xt)t∈[0,1]0

where (Xt)t∈[0,1]1 is an explicit WOT cost constructed via infimal convolution and deconvolution of Schrödinger and Wasserstein terms.

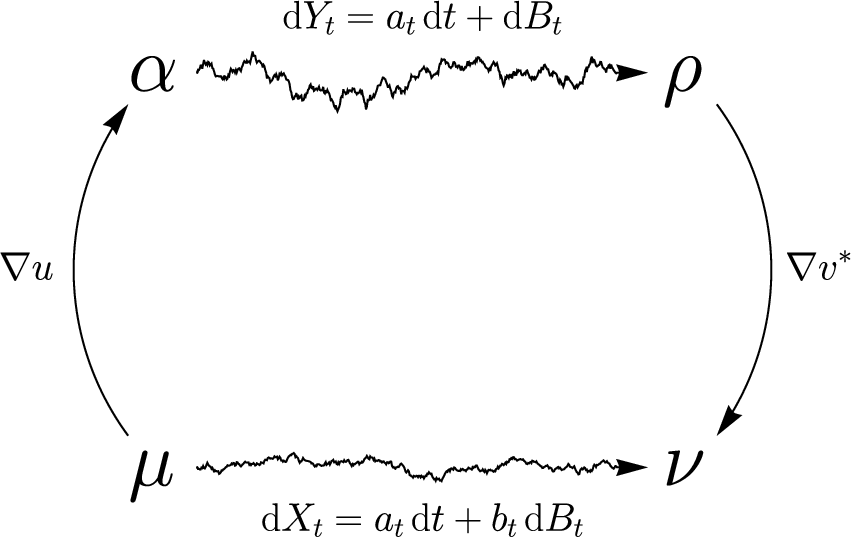

Figure 1: Schematic illustration of the relationships characterizing the Schrödinger–Bass system, parameterized by the dual potentials and mapping functions linked to the drift and volatility control in the semimartingale representation.

Weak Optimal Transport Structure and Duality

By mapping the dynamic stochastic control problem into the WOT setting, one can handle costs that are convex in the conditional law (generalizing classical Monge-Kantorovich OT). The cost (Xt)t∈[0,1]2 is shown to retain favorable continuity, convexity, and growth properties. This enables a dual formulation:

(Xt)t∈[0,1]3

where (Xt)t∈[0,1]4, (Xt)t∈[0,1]5 denotes infimal convolution, and (Xt)t∈[0,1]6 with (Xt)t∈[0,1]7 the standard Gaussian.

The dual potentials yield explicit formulae for the optimal drift and diffusion processes in the original stochastic problem.

Algorithmic Implications: The Schrödinger–Bass Sinkhorn Algorithm

The authors propose and analyze a Sinkhorn-type algorithm for numerically solving the static WOT problem, with monotonic improvement in the dual value and, under mild conditions, convergence to the unique optimizer. The iteration follows the system schematic (Figure 1), alternating between updates of convex potentials and marginal pushforwards.

Core Properties:

- Each step either strictly increases the dual value or remains constant only when convergence is reached.

- The iterates can be normalized, and by epi-convergence arguments and tightness estimates, convergence to the unique dual optimizer is established.

Asymptotic Analysis: Limiting Regimes

A central aspect is the analysis of the limiting behaviors as (Xt)t∈[0,1]8 and (Xt)t∈[0,1]9:

- Schrödinger Bridge Limit (dXt=atdt+btdBt,X0∼μ, X1∼ν,0): dXt=atdt+btdBt,X0∼μ, X1∼ν,1, recovering entropic OT.

- Brenier–Strassen Limit (dXt=atdt+btdBt,X0∼μ, X1∼ν,2 without rescaling): dXt=atdt+btdBt,X0∼μ, X1∼ν,3, the barycentric cost.

- Martingale Benamou–Brenier/Bass Limit (dXt=atdt+btdBt,X0∼μ, X1∼ν,4 with scaling): dXt=atdt+btdBt,X0∼μ, X1∼ν,5, characterizing the stretched Brownian martingale coupling.

In each limiting regime, primal and dual optimizers converge to those associated with the corresponding classical problems.

Structural and Theoretical Implications

Existence, Uniqueness, and Characterization

- The static WOT problem with cost dXt=atdt+btdBt,X0∼μ, X1∼ν,6 possesses unique primal and dual optimizers.

- The unique dual optimizer determines a semimartingale process which is optimal in law.

- The static and dynamic problems are equivalent: static couplings correspond to the marginal laws of dynamic optimal processes and vice versa.

Generalization

The use of infimal convolution on the WOT cost level formalizes how mixtures of transport and entropy/variance regularizations can be analyzed rigorously. The preservation of continuity and coercivity properties through infimal convolution extends the toolkit for handling more general regularized transport problems and their martingale extensions.

Algorithmic Convergence

The Sinkhorn-type algorithm can be interpreted as an alternating maximization for the dual potentials, guaranteeing convergence under integrability of the marginals. This provides a computationally tractable method for the semimartingale OT interpolating family.

Conclusion

This work establishes a rigorous bridge between major classes of optimal transport and martingale transport problems by parameterizing a family of stochastic control problems whose weak transport cost structure is made explicit and tractable. Key theoretical advances include strong duality, unique attainment, precise description of limiting regimes, and practical algorithms for computation. These findings deepen the understanding of the geometry and analysis of transport in both classical and stochastic or martingale-constrained settings, with future ramifications in areas such as stochastic control, quantitative finance, and the theory of regularized OT.

References

- "A weak transport approach to the Schrödinger-Bass bridge" (2604.02312)