- The paper presents a nonparametric jump-diffusion model, Edgeworth++, that couples stochastic volatility with deterministic volatility displacement to accurately price ultra-short-term SPX options.

- It achieves superior pricing accuracy with over 60% reduction in RMSE compared to rough volatility models and operates 28–67× faster for single-tenor quotes.

- The approach offers a real-time, closed-form solution for capturing sharp ATM IV oscillations, enabling effective risk management in high-frequency trading scenarios.

Ultra-short-term Volatility Surfaces: Nonparametric Pricing of SPX Options with Edgeworth++

Motivation: Market Microstructure and Volatility Surface Puzzles

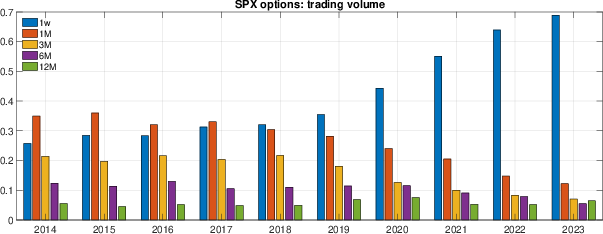

The proliferation of ultra-short-term SPX options (tenors ≤ 7 days) is the most consequential shift in recent listed derivatives markets. From 2018, the fraction of overall SPX option volume attributed to contracts expiring within a week has risen dramatically, reaching nearly 70% by 2023.

Figure 1: Fractional SPX option volumes by tenor, establishing the rapid rise in ultra-short-term contract trading.

This liquidity shift has been paralleled by an increase in the market relevance of 0DTE contracts and daily-expiring options, particularly after the extension of CBOE’s expiry structure in 2022. As a result, modeling and pricing demands have shifted toward “ultra-short” strikes, where the traditional SPX volatility surface exhibits strikingly pronounced oscillations and departures from the regularity seen at longer tenors.

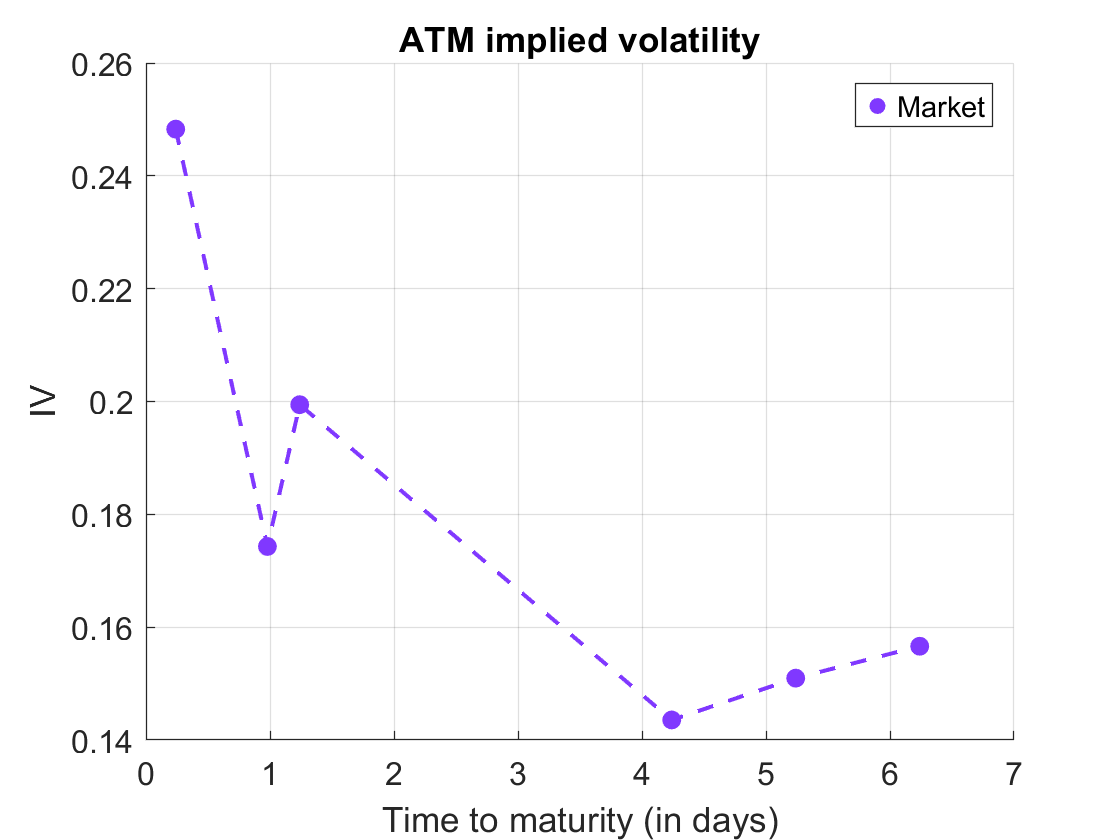

The empirical implied volatility (IV) term structures in this short-end sector can exhibit sharp non-monotonic slope changes, in contrast to the smoother behavior at longer maturities, as evident for Aug 18, 2022.

Figure 2: ATM IV term structure for six consecutive maturities, illustrating characteristic slope oscillations for ultra-short-term SPX options.

This irregular behavior persists even after controlling for known features such as weekly expiry cycles, institutional flows, and retail dominance. Quantitative summaries validate that both the first and second derivatives of ATM IV term structures are much larger and more variable for the 0-7d sector versus the 8-30d sector.

Modeling Solution: The Edgeworth++ Nonparametric Jump-Diffusion Surface

Standard models (affine stochastic volatility/rough volatility, even with multiple factors) are structurally unable to reproduce these empirical IV term structure oscillations across very short maturities. Theoretical constraints in Heston-like models (forward variance monotonicity, limited flexibility in skew/convexity, and lack of sufficient moneyness adaptivity when price jumps are absent) impair their fit and forecasting.

The authors introduce the Edgeworth++ model, a continuous-time jump-diffusion specification with two key sources of flexibility:

- Nonparametric stochastic volatility component: Allows arbitrary volatility dynamic adjustment (including time-varying leverage and volatility of volatility), thus capturing the local IV smile across strikes for each tenor.

- Deterministic shift extension (volatility displacement): A piecewise-constant mapping acting on volatility, not variance, enabling direct fit of the ATM IV term structure oscillations across short tenors.

This construction is operationalized by a local-in-tenor expansion of the process characteristic function. The expansion is performed up to O((τ)3/2) terms in the square root of the option’s maturity τ, leading to efficiently computable, essentially closed-form, option prices via Fourier inversion.

Data: Ultra-short-term SPX Option Surfaces

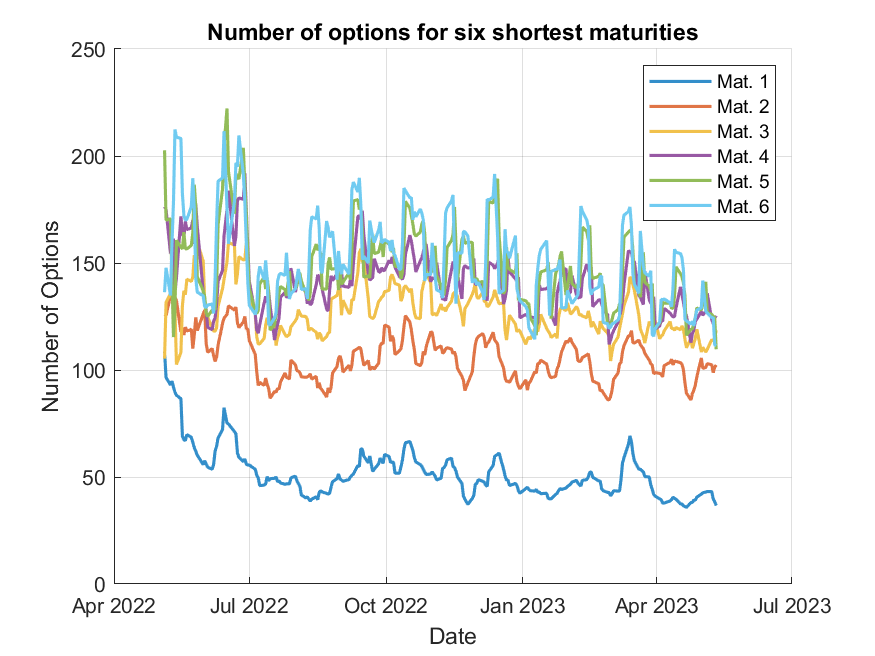

The empirical basis is a full year of intra-day CBOE SPX options data (May 6, 2022 - May 11, 2023) sampled at 10:30AM each day. For each surface, the six shortest expiries (post CBOE extension) are analyzed, supporting both typical and boundary-case surface realizations.

Figure 3: Daily option counts for each maturity, confirming robust and broad cross-sectional coverage for ultra-short tenors.

Data preprocessing includes elimination of illiquid contracts, standard moneyness banding, and the exclusion of FOMC announcement days.

Empirical Evaluation: Benchmarks, Pricing Accuracy, and Computation

Benchmark Model Failure

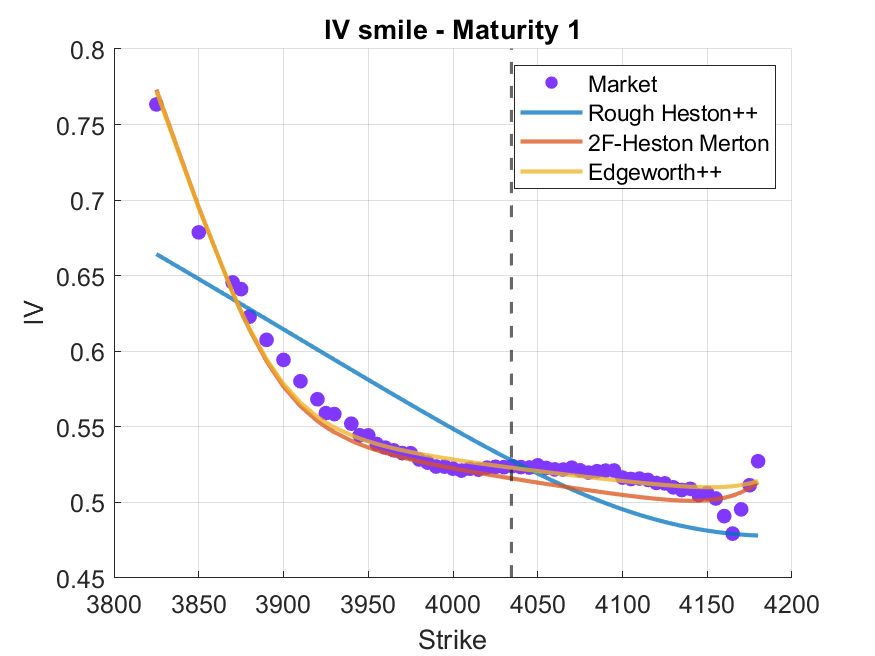

Edgeworth++ is contrasted with two class-leading specifications:

- Rough Heston++: An affine, univariate, rough volatility model with a deterministic displacement.

- 2F Heston Merton: Two-factor affine volatility plus jumps in price and volatility (self-exciting).

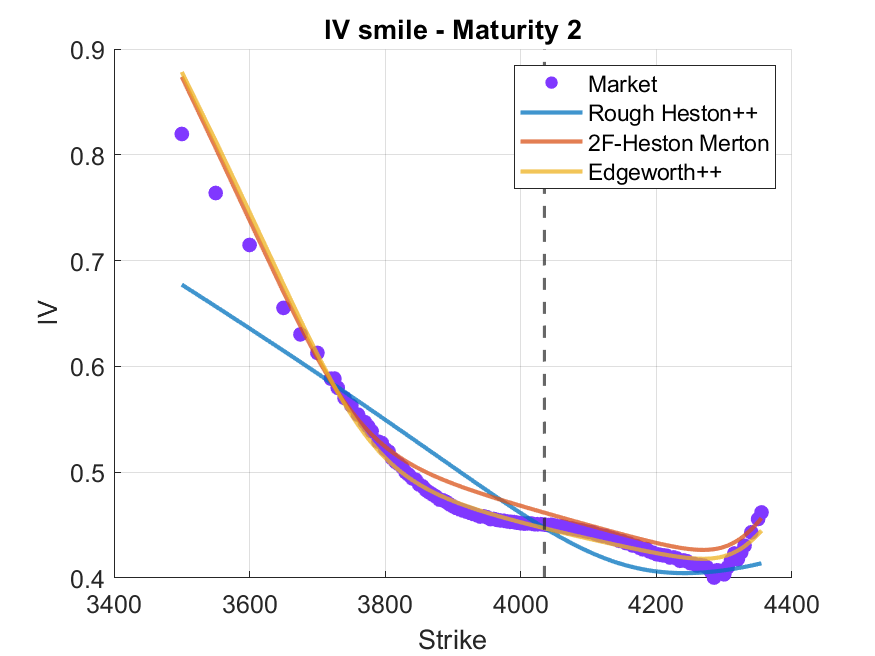

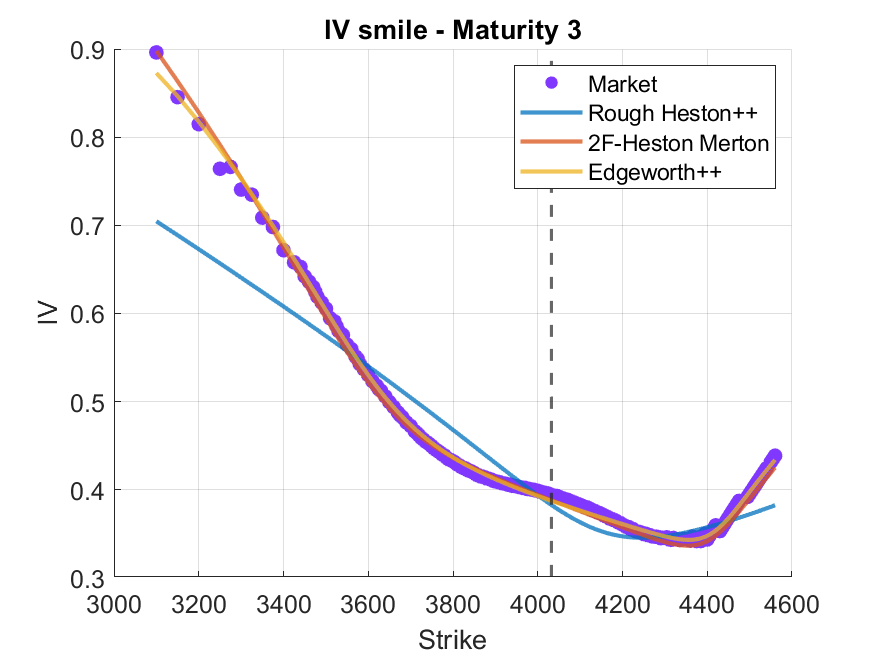

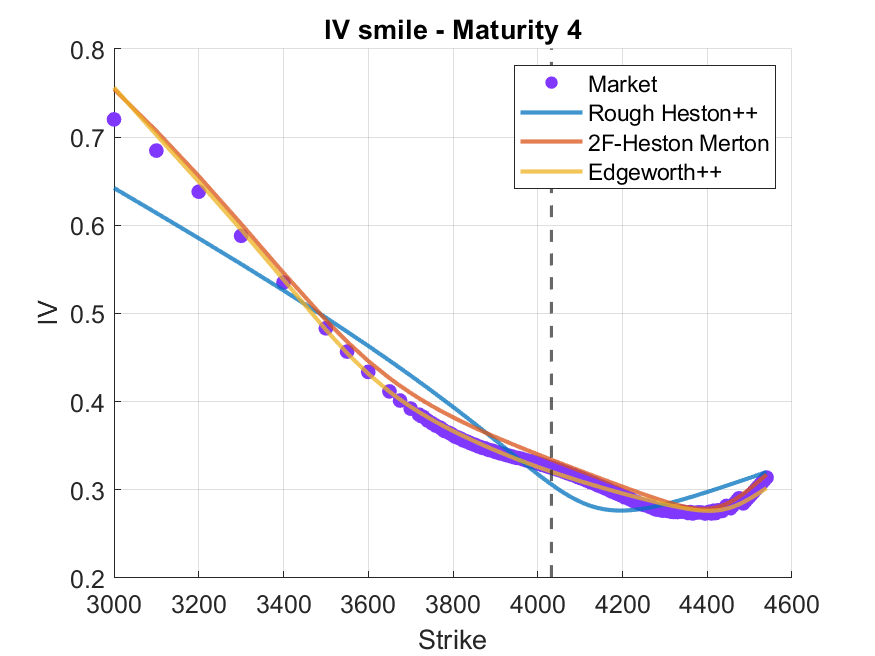

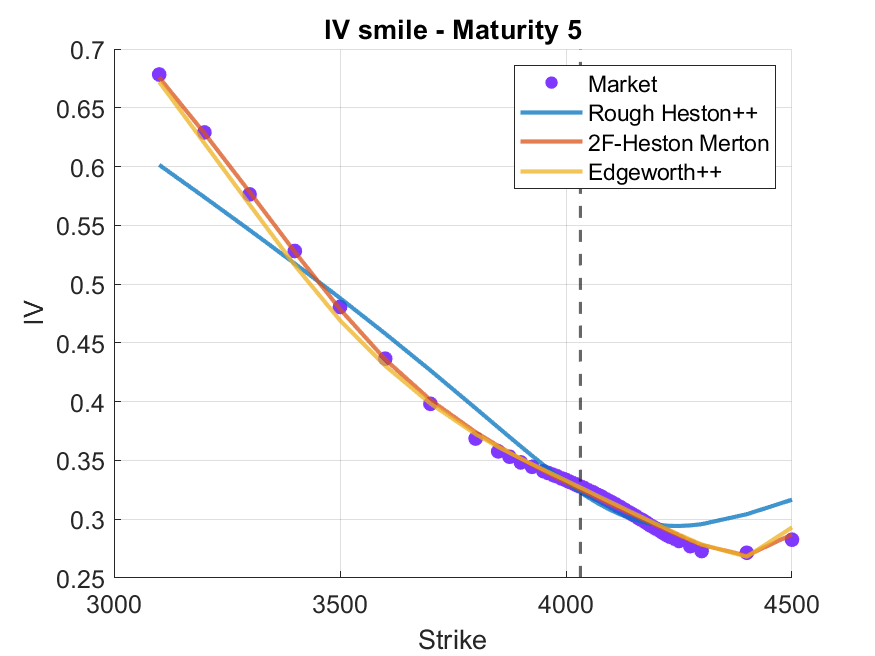

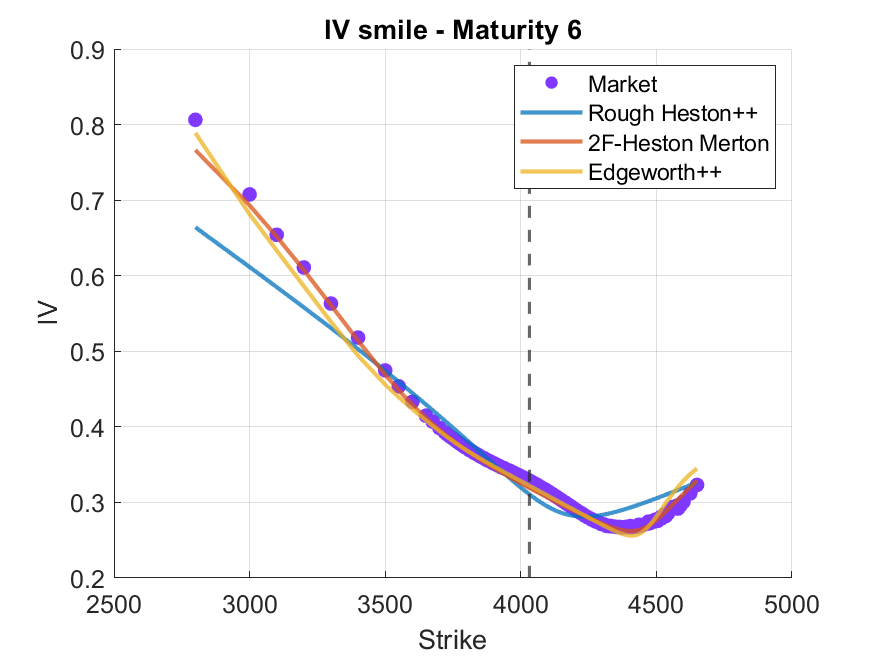

Neither achieves satisfactory joint fit—Rough Heston++ fails to calibrate the IV smile for fixed tenor (parsimonious structure, no jumps), while 2F Heston Merton delivers an ATM IV term structure that is overly smooth, unable to capture empirically observed oscillations.

The model is estimated daily, minimizing cross-sectional pricing RMSE (across maturities and log-moneyness). When restricted to single-tenor (0DTE) prices, Edgeworth++ yields lowest error, outperforming even parameter-rich affine competitors. For full-surface pricing (all six short tenors), mean RMSE is approximately 1 volatility point—over 60% lower than rough volatility alternatives (Rough Heston++), and over 40% lower than non-rough 2F Heston Merton. These numbers represent order-of-magnitude improvement in high-frequency pricing, with Edgeworth++ prices falling within quoted bid-ask spreads far more frequently.

Figure 4: Market and fitted implied volatility smiles for six consecutive tenors (Aug 18, 2022), with Edgeworth++ demonstrating high fidelity both ATM and OTM.

Moreover, in terms of computational cost, Edgeworth++ is fundamentally superior due to its analytic characteristic function expansion: it is 28–67× faster for single-tenor quotes and up to 12× faster for joint multi-tenor pricing compared to competitors.

Failure Modes of Competing Specifications

Rough Heston++ can, via displacement, approach the observed ATM IV term structure oscillations, but its lack of jumps and its enforced V-shaped smile limits its fit to the full smile, and the model trades off OTM and ATM accuracy. 2F Heston Merton, due to the inherent smoothness of its affine volatility formulation, cannot generate the high-frequency term structure variability observed in SPX data.

Empirical IV smiles (for both “typical” and “unusually smooth” days) show consistently superior Edgeworth++ fit to the cross-section for all strikes and maturities.

Figure 5: Implied volatility smiles for a day with regularly decreasing term structure (May 10, 2022); Edgeworth++ achieves almost-perfect fit.

Structural Enhancements and Robustness

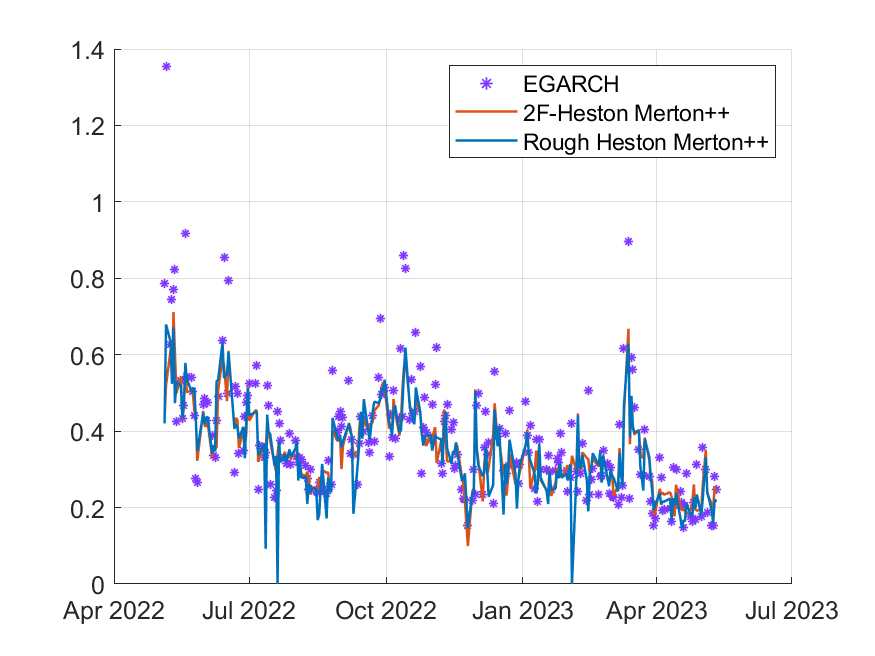

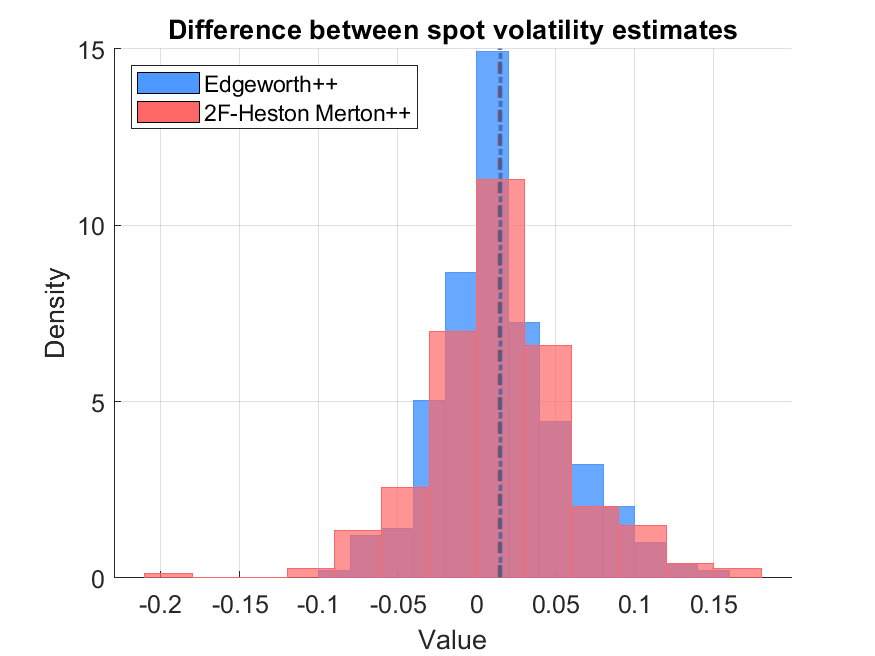

The authors consider “enhanced” versions of both benchmarks—adding jumps to rough volatility and a displacement to 2F Heston Merton—yielding material improvements particularly for OTM pricing and spot volatility estimation. However, Edgeworth++ remains dominantly more efficient and accurate (both in-sample fit and estimated spot volatility).

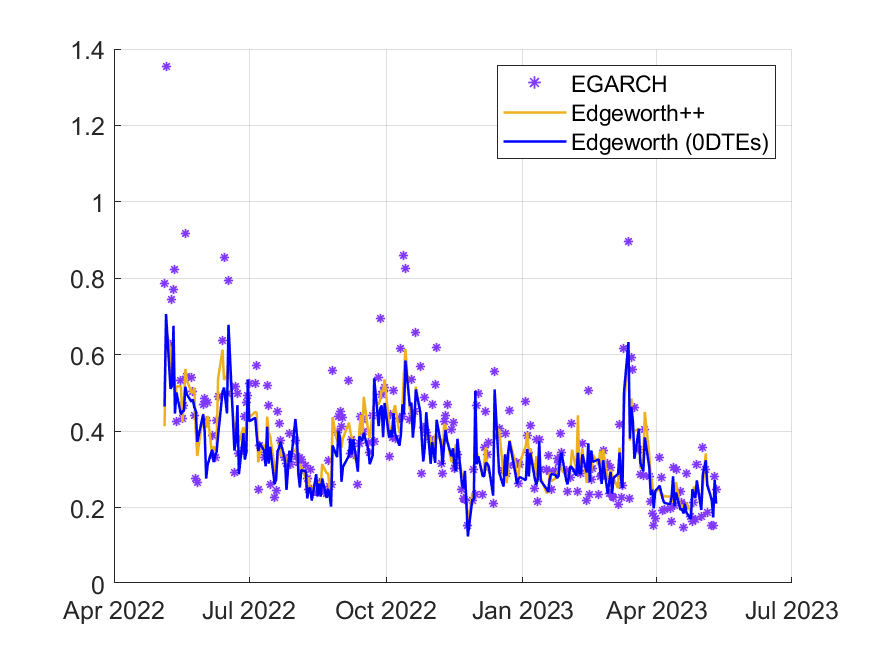

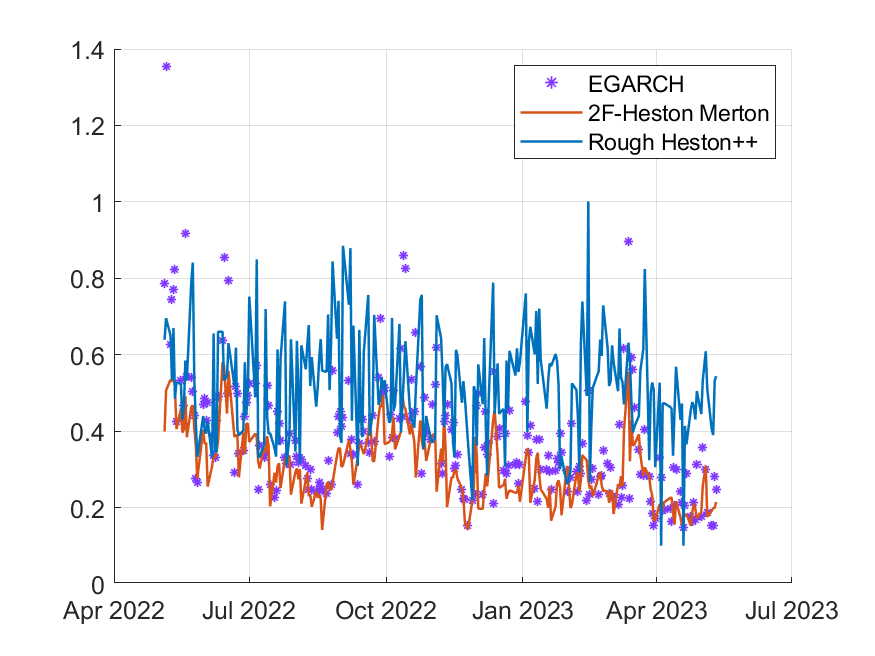

Figure 6: Spot volatility estimates across the full sample, comparing historical (EGARCH), Edgeworth (0DTE-only), Edgeworth++ (full surface), and both standard and enhanced benchmarks.

Histogram analysis of estimation errors confirms the statistical efficiency of Edgeworth++.

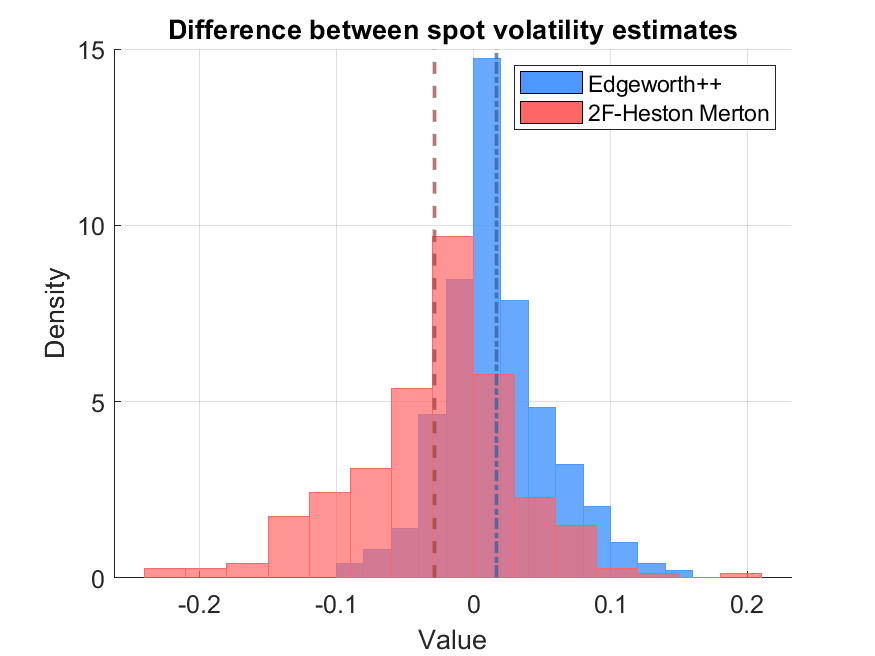

Figure 7: Absolute spot volatility estimation error distributions, contrasting Edgeworth++ and enhanced 2F Heston Merton variants.

Theoretical and Practical Implications

The study demonstrates that for ultra-short-term options, deterministic volatility displacements and jump components are strictly necessary to fit observed market surface behavior. While affine and rough volatility models have a prominent place in mainstream pricing (and have historically deliberately excluded jumps), the empirical findings here necessitate reintroducing jump-diffusions and nonparametric volatility evolutions—particularly if accurate risk management, hedging, and estimation are to be achieved at the sub-weekly horizon.

Practically, the tractability of Edgeworth++ (analytic expansions, closed-form pricing, parsimony in parameters) enables real-time fit, parameter inference, and efficient calibration even for orderbook-level streaming data, supporting industrial trading and risk platforms.

Conclusion

The empirical structure of SPX ultra-short-term volatility surfaces is inconsistent with the predictions of standard affine or rough volatility models, regardless of parameterization. The Edgeworth++ model architecture—a nonparametric stochastic volatility factor with deterministic piecewise volatility displacement and time-inhomogeneous jumps—enables precise fit of both IV smiles and ATM term structure oscillations, at a speed and parsimony suitable for market applications. This approach represents a foundational shift in the modeling of short-end volatility and will likely influence future high-frequency derivatives research and practice.

Reference: "Ultra-short-term volatility surfaces" (2603.29430)