- The paper introduces a novel deep neural network with a Monodense layer that enforces economic monotonicity for robust price elasticity estimation.

- It leverages cross-joined lead-lag transaction data and feature embeddings to capture complex relationships between price and demand.

- Results demonstrate lower WMAPE and MAE compared to LightGBM and DML, ensuring operational feasibility and economic consistency in pricing applications.

Monodense Deep Neural Model for Determining Item Price Elasticity: An Expert Analysis

Introduction

This paper presents a novel framework for item-level price elasticity estimation in retail, with a focus on scalability, economic consistency, and operational feasibility. The proposed approach circumvents the need for treatment-control experimentation by leveraging massive transactional datasets from retail operations, introducing a new neural architecture, Monodense-DLM, that explicitly encodes monotonicity between price and demand. The authors systematically compare their method with established alternatives such as LightGBM and double machine learning (DML) models, demonstrating superior predictive and elasticity estimation performance.

Limitations of Traditional and ML-Based Approaches

Classical econometric approaches for elasticity estimation, such as Linear Expenditure Systems and AIDS, impose strong parametric assumptions and struggle to capture nonlinear dependencies or scale to the high-dimensional feature spaces encountered in modern retail. These methods are further constrained by the impracticality of universal control-treatment designs in large product assortments.

Conventional machine learning models—including gradient boosting and deep learning architectures—address nonlinearity and high-dimensionality but can fail to enforce the fundamental economic property that demand must decrease as price increases, often permitting spurious positive elasticities. Attempts to rectify this via data curation or post hoc filtering are methodologically unsatisfying, particularly when feature interactions and real-world supply-chain effects (stockouts, seasonality, competitor pricing) further complicate the demand structure.

Proposed Framework and Monodense-DLM Architecture

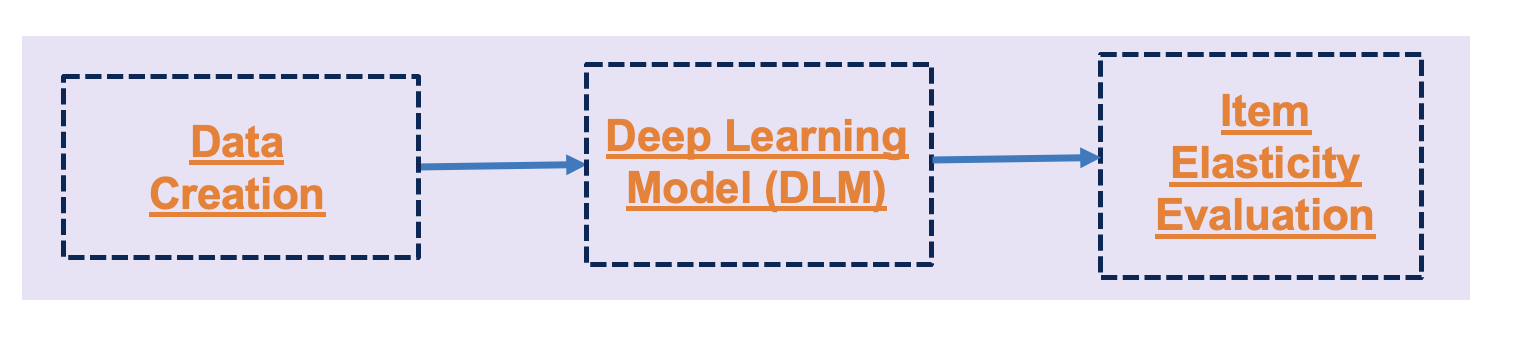

The framework starts with the systematic construction of a lead-lag dataset, performing a cross join of monthly transaction records to construct pairs reflecting all plausible lead and lag relationships for each item under the constraint that the lag-lead difference is between 1 and 12 months. Extensive features are incorporated: inventory, promotions, competitor data, seasonality, substitute availability, and others are included to accurately capture context dependencies.

Figure 1: Overview of the full pipeline, from cross join data construction to embedding-enriched neural modeling and elasticity inference.

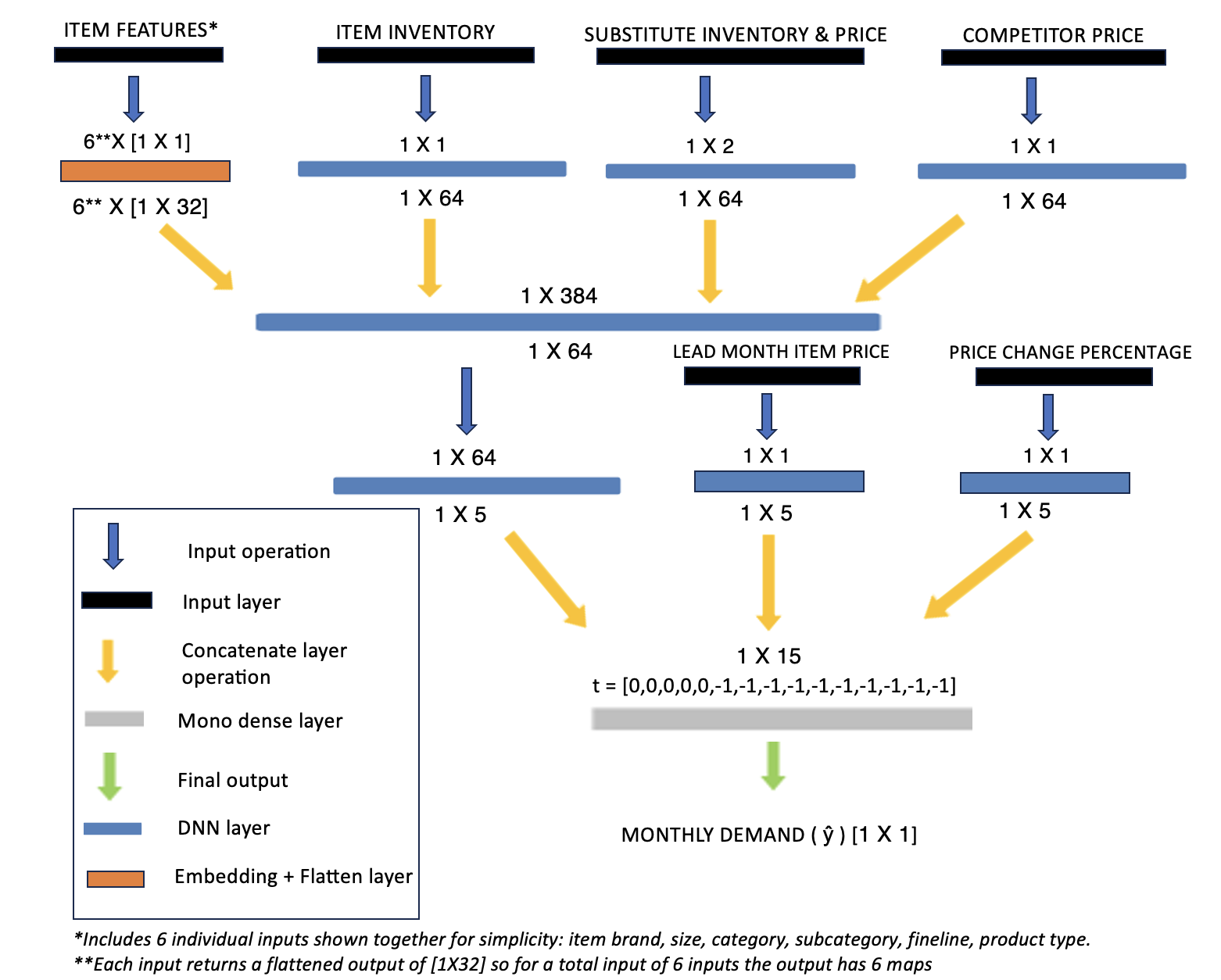

The neural network design begins with embeddings for categorical and continuous features, which are concatenated into higher-order dense representations. A critical architectural innovation is the Monodense layer, where monotonicity is enforced via sign constraints on weights, as informed by an indicator vector. For features signaled as monotonically decreasing (notably, item price), weights are explicitly constrained non-positively, thereby ensuring that a rise in price does not predict an increase in demand. The Monodense layer utilizes piecewise convex, concave, and bounded activations to flexibly fit complicated but economically consistent demand curves.

Figure 3: Schematic for the Monodense-DLM model, highlighting the embedding, concatenation, and monotonicity-enforcing layers.

To avoid the loss of sensitivity to price often observed in generic deep architectures (which tend to dilute price information in high-level encodings), the model introduces price as a direct input in these lower layers, ensuring robust responsiveness.

Experimental Setup and Training

The dataset consists of over a billion transactional records, encompassing a comprehensive assortment of retail SKUs. Data is split into training and validation (two years) and a three-month out-of-time test set. All models (Monodense-DLM, LightGBM, and DML) are trained under the same data and operational constraints, with Monodense-DLM trained using MSE loss, the Adam optimizer (learning rate 0.01, batch size 128), and batch data standardization.

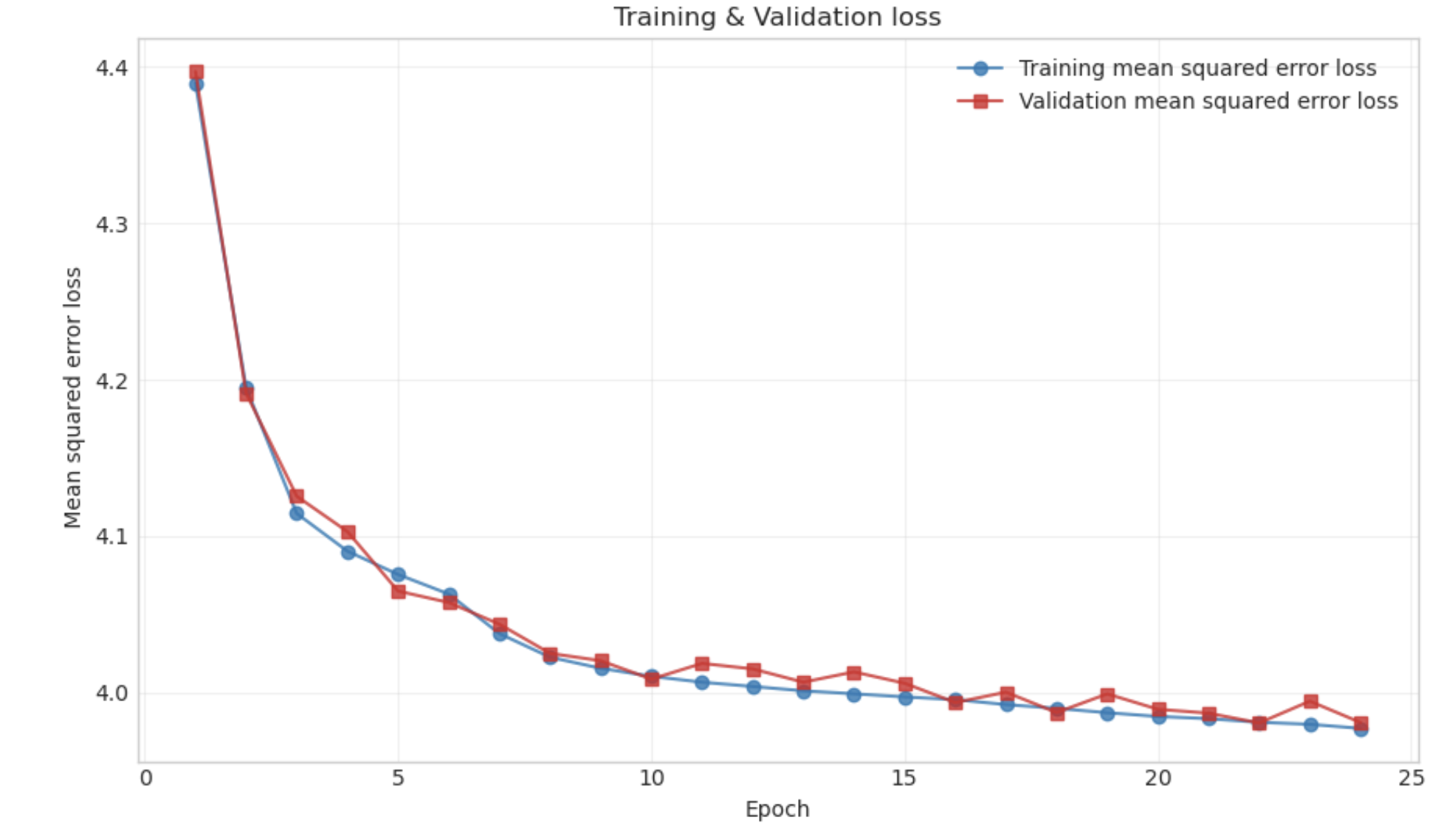

The training process is monitored using training and validation losses, ensuring overfitting is controlled via L2 regularization and early stopping.

Figure 2: Convergence of training and validation loss illustrating stable optimization and generalization.

Method for Elasticity Estimation

Elasticity at any price point is evaluated by comparing predicted (counterfactual) demands at perturbed price levels, applying the standard elasticity formula:

EΔp=y^(p)y^(p+Δp)−y^(p)×Δpp

By deploying the neural network in an inference context on the most recent data rows with price variates, the framework estimates elasticity for arbitrary price shocks without requiring explicit experimental group splits.

Numerical Evaluation and Comparative Analysis

The Monodense-DLM is benchmarked against LightGBM (with monotonicity constraints activated) and DML regression. Performance is assessed on two critical metrics:

- WMAPE (Weighted Mean Absolute Percentage Error) on demand prediction

- MAE (Mean Absolute Error) on elasticity estimation, referencing items with known ground-truth elasticities

Empirical results demonstrate that Monodense-DLM achieves WMAPE of 30.9%, outperforming LightGBM (35.9%) and DML (36.1%), as well as lowest MAE in elasticity estimation (0.36 vs. LightGBM 0.42 and DML 0.43). These results indicate both predictive and interpretability gains. Notably, due to the architectural constraints, the Monodense-DLM never produces positive (economically inconsistent) elasticities, effectively eliminating a significant failure mode observed in traditional ML models.

Practical and Theoretical Implications

Practically, the proposed method enables elasticity estimation at catalog and transaction scale without experimental intervention. This increases the feasibility of demand response modeling for both national chains and single-location retailers. By encoding monotonicity directly into the network weights, economic consistency is maintained, which is crucial for robust deployment in pricing and revenue optimization.

Theoretically, the integration of monotonicity constraints into deep models for structural economic relationships is a significant contribution, applicable beyond price elasticity to other contexts where monotonicity is a domain requirement (e.g., credit scoring, risk assessment).

Prospects for Future Work

Further gains are anticipated from deeper architectural exploration and advanced monotonic activations. The framework is readily generalizable to other elasticity dimensions (e.g., cross-price elasticity, supply-side shocks) and can be adapted for multivariate temporal modeling. The computational pipeline scales efficiently to extreme data volumes, opening opportunities for near-real-time repricing strategies, automated promotion optimization, and broader applications in e-commerce and omnichannel retail environments.

Conclusion

This paper establishes that it is feasible and operationally effective to directly estimate item-level price elasticity using deep neural networks with monotonicity constraints (the Monodense-DLM), obviating the need for experimental group construction or data curation to ensure economic consistency. The architecture robustly outperforms both traditional econometric and standard ML alternatives in large-scale real-world settings, delivering superior demand forecasts and elasticity estimates. The approach represents a practical advance for algorithmic pricing, revenue management, and data-driven decision environments, while providing methodological advances with applicability to a broad class of economic machine learning problems.