Just-in-Time Resale in an Ahead-of-Time Auction: An Event Study

Abstract: We study Arbitrum's Timeboost mechanism following the adoption of Kairos by its main users -- Wintermute and Selini Capital -- to understand how the emergence of a just-in-time secondary market affects the dynamics of an ahead-of-time primary auction. We find that competition in the primary auction significantly declines and surplus shifts away from Arbitrum. After the transition, bids paid in the primary auction correspond to only 14.8\% of the highest bid (compared to nearly 62.7\% in the \textit{Pre-Kairos} era), and a lower share of searcher profit-and-loss (PnL), despite total PnL (gross of auction payments) remains of similar magnitude across regimes. This indicates that the primary auction effectively ceases to function as a meaningful surplus extraction mechanism. Although demand for time-boosting valuable CEX--DEX arbitrage transactions continues to increase with external price volatility, observed bids in the Timeboost auction no longer reflect this demand. While the exact distribution of the additional value between searchers and Kairos remains unclear, the evidence suggests that the secondary market captures a substantial share at the expense of the primary auctioneer. We conclude by outlining possible ways for Arbitrum to recapture this value, including modifying the auction design to reduce the gap between value and payments and adopting a dynamic reserve price.

Paper Prompts

Sign up for free to create and run prompts on this paper using GPT-5.

Top Community Prompts

Explain it Like I'm 14

What this paper is about

Imagine a theme park that sells a “fast pass” so your ride gets to skip the line. On Arbitrum (a popular blockchain that bundles and orders transactions), there’s something similar called Timeboost: every minute, there’s an auction to buy a tiny speed advantage (200 milliseconds) that lets your transactions go first for that minute.

This paper looks at what happened when another service, Kairos, started buying that one‑minute fast pass and then reselling super short “micro fast passes” just in time to different traders, per transaction. The authors ask: how did this new, just‑in‑time resale market change the original Timeboost auction and who ends up getting most of the money?

The big questions the authors asked

- If a reseller like Kairos buys the minute‑long fast pass and splits it into smaller, just‑in‑time slots, does that make the system more efficient or less competitive?

- Do the original bidders (two big trading firms named Wintermute and Selini) stop bidding hard in the main auction once they can buy from Kairos?

- Do the prices paid in the main auction still reflect demand (which tends to go up when crypto prices are jumpy)?

- Who captures most of the value: Arbitrum (running the auction), the traders, or the reseller (Kairos)?

- How could Arbitrum change the auction to recapture lost revenue?

How they studied it (in everyday terms)

The authors ran an “event study,” which is like watching what happens before and after a big change.

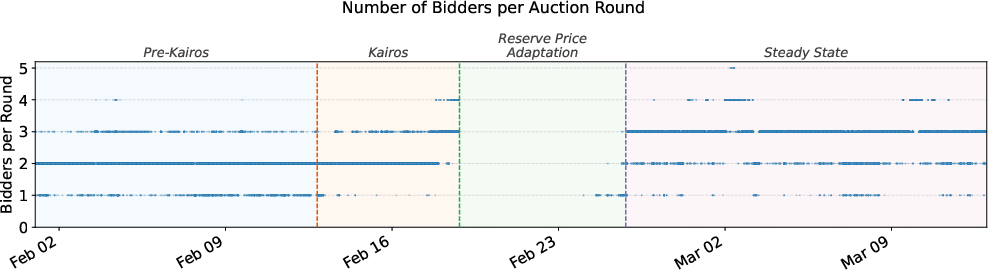

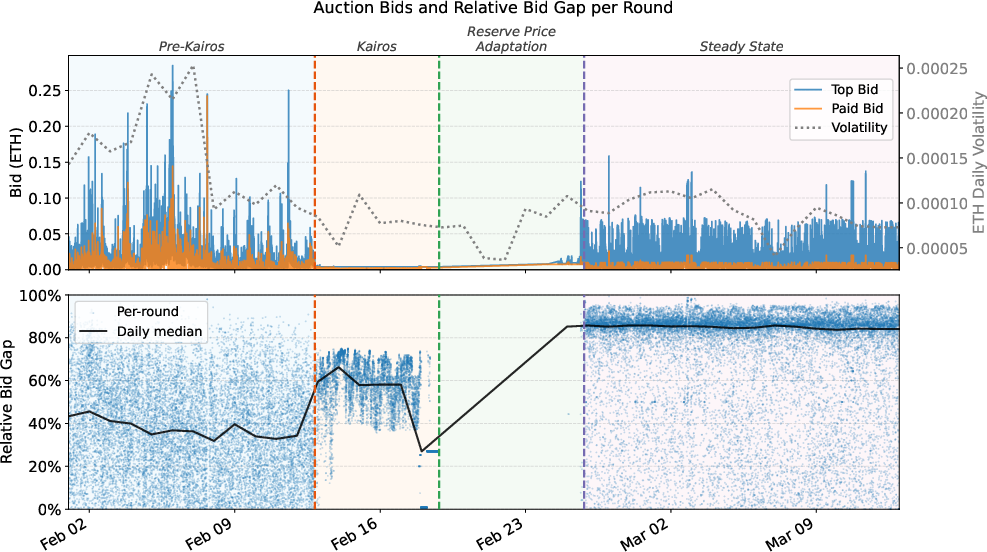

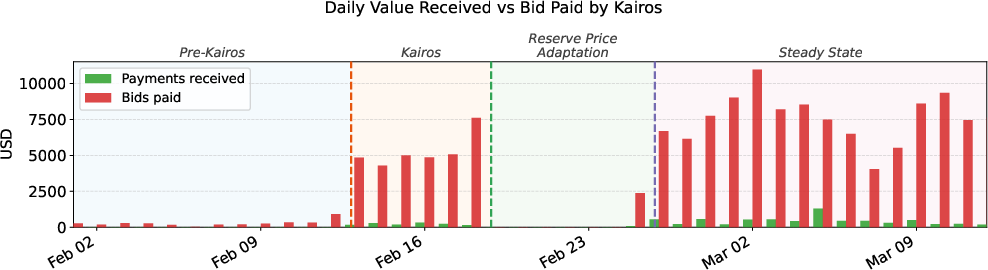

- The “fast pass” auction: Every minute, there’s a second‑price auction with a reserve price (a minimum price). In a second‑price auction, the top bidder wins but pays the second‑highest bid.

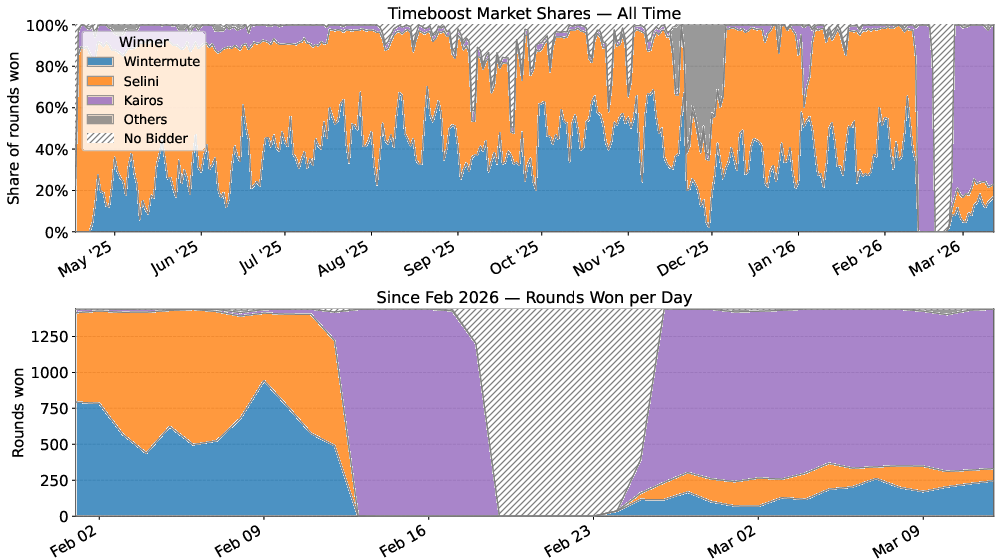

- The change: In mid‑February 2026, Wintermute and Selini mostly stopped bidding hard in the main auction and started using Kairos’s resale market. Kairos began winning most rounds.

- The data:

- 47,000+ auctions from Feb 1 to Mar 12, 2026.

- 7.3 million “time‑boosted” transactions (transactions that used the fast lane).

- Focus on CEX–DEX arbitrage, which is like buying on one market (a centralized exchange, CEX) and selling on another (a decentralized exchange, DEX) when there’s a price difference. Think “buy low on one store, sell high on another.”

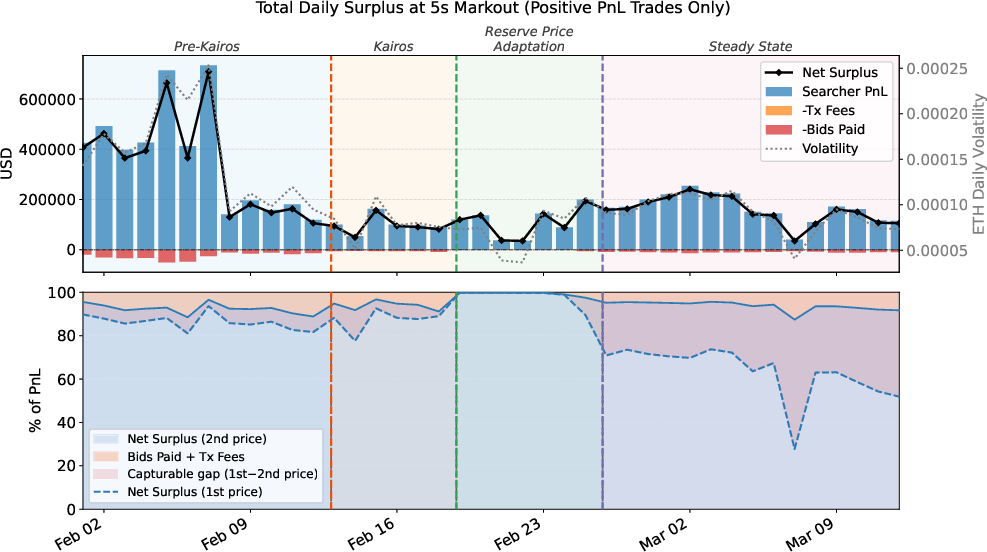

- They estimated profits (PnL = profit and loss) by checking prices a few seconds after trades to see if a trade likely made money. They used exchange price data and a simple 5‑second “markout” to estimate profit shortly after the trade.

- They tracked how bids and profits change with volatility—how “jumpy” crypto prices are. More jumpiness usually means more chances for arbitrage, so demand for the fast lane should rise.

Key terms in simple language:

- Second‑price auction: You bid what you want, but if you win, you pay what the second‑highest person bid.

- Reserve price: The minimum allowed price.

- Volatility: How much prices wiggle up and down quickly.

- Just‑in‑time resale: Buying a big block of speed and reselling tiny slices exactly when needed.

What they found and why it matters

Big picture: After Kairos started reselling the fast pass, competition in the main auction fell sharply, and Arbitrum collected much less money from the auction—even though traders’ overall profits stayed about the same.

Here are the main points:

- Who won the auction changed:

- Before Kairos took over, Wintermute and Selini were the main winners and bid against each other.

- After mid‑February 2026, Kairos started winning most rounds (about 75–80% in the new “steady” period), while Wintermute and Selini mostly stopped aggressive bidding and bought access from Kairos instead.

- The auction stopped tracking demand:

- Before, both the top bid and the price paid moved up when markets got jumpy (more volatility = more demand).

- After, the paid price often sat near the minimum, even when volatility (and likely demand) was high. The top bid stayed high sometimes, but the price actually paid fell way behind.

- The “gap” exploded:

- In a second‑price auction, the winner pays the second‑highest bid. Before Kairos, the paid price was close to the top bid (about 62.7% of it). After, it dropped to about 14.8% of the top bid. That means the auctioneer (Arbitrum) captured much less of the value.

- Traders’ profits didn’t shrink:

- Wintermute and Selini kept making similar total profits overall, especially when markets were more volatile.

- They just got fast‑lane access through Kairos almost all the time, rather than winning it themselves.

- Who got the money instead?

- Arbitrum’s auction revenue fell. Kairos likely captured some value by reselling access, and Wintermute/Selini likely kept more profit.

- On‑chain payments to Kairos were small compared to what Kairos paid in the main auction, which suggests many payments were done off‑chain via subscriptions (so it’s hard to see exactly how the money is split between Kairos and the traders).

- Why it matters:

- The primary auction “stopped working” as a revenue tool. It no longer made bidders pay close to what the fast lane was worth to them.

- The just‑in‑time resale market changed incentives: instead of competing in the main auction, big traders could coordinate by buying from a reseller, lowering competitive pressure.

What this could mean going forward

The authors suggest simple changes to help Arbitrum recapture value:

- Switch to a first‑price auction: The winner pays what they bid. That can make it harder to keep the paid price far below the winner’s true value and can reduce the huge gap observed in the second‑price setup.

- Use a dynamic reserve price: Raise the minimum price when markets are jumpy and opportunities are plentiful, and lower it when things are calm. In other words, tie the minimum to recent price volatility so the auction captures more demand.

Bigger picture:

- Ahead‑of‑time auctions (selling access before it’s used) can be undermined by just‑in‑time resale markets. That can shift revenue away from the protocol and toward intermediaries and traders.

- Careful auction design matters. Small tweaks can change who benefits—whether it’s the network, the middlemen, or the traders.

- If more searchers join the resale market and bring new strategies, the “unbundling” (splitting a minute into many tiny slots) could improve efficiency. But right now, the main effect seems to be reduced competition in the primary auction, not a big increase in overall value.

In short: A reseller stepped in, split the fast lane into tiny slices, and changed the game. The main auction stopped reflecting real demand, the protocol earned less, and most of the value shifted to traders and the reseller. Design changes like first‑price auctions and smarter minimum prices could help balance things back.

Knowledge Gaps

Unresolved knowledge gaps, limitations, and open questions

Below is a single, consolidated list of what remains missing, uncertain, or unexplored in the paper, phrased to be concrete and actionable for follow-up research:

- Surplus split opaque due to off-chain billing: the exact revenue sharing between Kairos and searchers is unknown because subscription payments are off-chain; quantify this by accessing Kairos billing data, scraping merchant-provider settlement rails, or inferring fees via controlled experiments with instrumented client orders.

- Attribution of value within Kairos “sub-auctions”: the pricing and allocation rules for Kairos’s ~100 ms batches are not observable; obtain per-batch bid/ask/clearing data to assess how much surplus the reseller captures versus searchers.

- Collusion vs. efficiency ambiguity: the paper infers coordinated bidding from patterns but lacks statistical tests for tacit collusion; develop and apply collusion screens (e.g., rotation tests, bid variance collapse, Granger causality around reserve changes) and structural models to distinguish coordination from benign unbundling.

- Causal identification missing: effects are correlational and confounded by contemporaneous reserve-price changes; use quasi-experimental designs (e.g., difference-in-differences with matched L2s, event studies with placebo windows) to isolate Kairos’s impact from policy shocks.

- Short observation window: the study runs Feb 1–Mar 12, 2026; extend to pre-2026 and multi-month post-periods to test stability, seasonality, and long-run equilibria (entry/exit, fee convergence).

- Two-searcher dominance limits generalizability: results hinge on Wintermute/Selini behavior; examine periods with more active searchers and other strategies (atomic arbitrage, liquidation arbitrage) to assess external validity.

- Incomplete detection of CEX–DEX arbitrage: heuristics miss multi-hop, long-tail tokens, cross-chain legs, and OTC legs; augment with path reconstruction, cross-chain logs, and heuristics for non-canonical venues to improve recall.

- PnL measurement bias: markouts at 5s with mid-prices ignore slippage, hedging paths, inventory risk, and execution costs; run robustness with multiple horizons, bid–ask adjusted prices, and alternative inventories unwind models.

- Positive-PnL-only selection: excluding loss-making trades inflates net value and captured shares; re-estimate with all trades (including failed/reverted) and separate opportunity-selection errors from execution outcomes.

- Failed/reverted transactions not analyzed: the cost of failed attempts (gas, missed opportunities) and their correlation with lanes/volatility are unmeasured; include failure rates and costs to avoid survivorship bias.

- Mapping transactions to auction rounds may be noisy: matching by minute windows can misattribute inclusion; validate with sequencer timestamps or fast-lane identifiers to reduce misclassification.

- Latency advantage not empirically verified: assumed 100–200 ms edge is not measured at the client–sequencer path; instrument end-to-end latency to quantify realized advantage and its variance.

- Demand elasticity unestimated: the paper shows correlations with volatility but does not estimate the demand curve for time-boost; fit structural or reduced-form models linking willingness-to-pay to volatility, spreads, and contention.

- First-price counterfactual unrealistic without shading: revenue comparisons use observed second-price max bids; simulate equilibrium with bid shading (e.g., using IPV/affiliated-values models) to bound realistic first-price revenue.

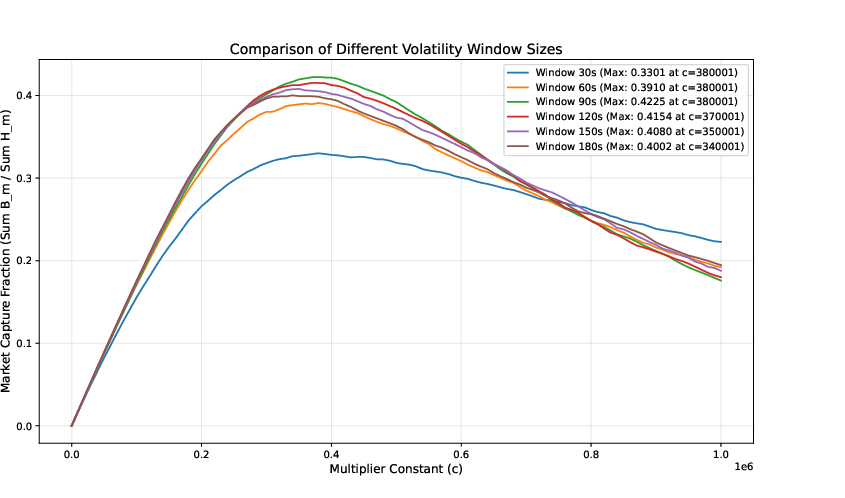

- Dynamic reserve price proposal unvalidated: the σ²-based rule is tuned in-sample, lacks out-of-sample tests, and is potentially manipulable; evaluate across holdout periods, alternative volatility estimators, latency of feeds, and adversarial robustness (volatility spoofing).

- Oracle/market-data dependence risk: volatility from Binance may lag, be unavailable, or diverge from on-chain prices; compare multiple feeds (DEX TWAPs, cross-CEX composites) and quantify sensitivity.

- Strategic responses to new mechanisms unmodeled: searcher and reseller reactions to first-price auctions or dynamic reserves are not analyzed; build game-theoretic or agent-based simulations to forecast entry, shading, and bypass behavior.

- Alternative designs unexplored: multi-winner auctions, per-transaction protocol-native time boosts, randomized priority, or lotteries could mitigate hub-and-spoke coordination; evaluate revenue and welfare under these mechanisms.

- Entry barriers and market concentration: why do other searchers not compete via Kairos or the primary auction? Survey access prerequisites, fees, technical requirements, and exclusivity to assess barriers and policy levers.

- US-market-hours effect only partially characterized: the increase in Kairos losses around NYSE hours is noted but not decomposed; quantify how liquidity, spreads, and cross-venue latencies drive time-of-day bidding shifts.

- Ecosystem welfare unquantified: user/LP outcomes (price impact, LP impermanent loss, failed swaps, delays) are not measured; estimate externalities of JIT resale on non-arbitrage participants.

- Sequencer operations and fairness not assessed: impacts on inclusion fairness, censorship risk, and operational load from frequent JIT batches are unknown; collect sequencer-level metrics to evaluate.

- Fee accounting scope unclear: which fees are counted as “transaction fees” and how priority fees/MEV tips interact with Timeboost is not detailed; reconcile fee components to avoid under/over-attribution to Arbitrum.

- Robustness to stablecoin depegs and stress: assuming USDT=USDC=USD may break under stress; re-run PnL under depeg scenarios to bound error.

- Cross-chain spillovers unstudied: whether Kairos-like resale shifts MEV and liquidity across rollups/L1s is unknown; analyze correlated changes on other chains around the event.

- Endogeneity between volatility and gas/queueing: both bids and fees respond to common shocks; use instruments or control variables (gas prices, mempool congestion) to disentangle channels.

- Identification of “unbundling” benefits limited: increased fast-lane usage is shown but not linked to higher total value; test whether total PnL increases net of fees when more searchers transact via JIT resale.

- Market power of a single reseller: centralization and resilience risks (downtime, policy changes) from Kairos dominance are not quantified; perform counterfactual stress tests on availability and failover.

- Transparency and governance questions: off-chain payments reduce auditability; analyze governance/monitoring mechanisms needed if resale markets mediate protocol revenue.

- Parameter stability over regimes: relationships among volatility, PnL, and bids may be regime-dependent; estimate regime-switching models to detect structural breaks.

- Confounding contemporaneous events: other protocol updates or exogenous shocks (listings, liquidity migrations) could influence bidding and PnL; control for these events in augmented regressions.

- Data coverage limits: reliance on Dune and identified contracts may miss protocols/addresses; cross-validate with raw node traces and alternative indexers to quantify missingness.

- Mechanism manipulation risks: dynamic reserves based on recent prices may invite volatility/gas manipulation; formally analyze attack surfaces and design countermeasures (e.g., robust volatility estimators, guardrails).

- Legal/compliance implications of off-chain resale: the paper does not discuss regulatory or policy constraints that could affect feasibility or data access; map these constraints to research design (e.g., data-sharing MOUs).

- Path to measuring “true” opportunity value: the gap between top bid and economic value is not estimated; construct benchmarks using realized arbitrage spreads across venues to bound private values.

Practical Applications

Immediate Applications

Below are actionable, sector-linked use cases that can be deployed with today’s infrastructure and tooling.

- Finance/blockchain protocols (L2s, sequencers)

- Implement a first-price Timeboost auction to shrink the first–second price gap and discourage tacit coordination.

- Tools/workflows: upgrade auction contract and client; educate bidders on bid shading; dry-run in testnets and canary minutes.

- Assumptions/dependencies: DAO approval; bidders adapt to first-price equilibria; minimal impact on latency/settlement.

- Deploy a dynamic reserve price tied to real-time volatility, e.g., R_t = c·σ_t² (σ from WETH 1s log-returns over a short window).

- Tools/products: “Dynamic Reserve Oracle” (robust volatility oracle with circuit breakers), backtesting module to calibrate c; governance-controlled parameters.

- Assumptions/dependencies: reliable and manipulation-resistant data feed; observed positive volatility–demand relationship persists; guarded launch to prevent overblocking during spikes.

- Add auction health monitors and controls: auto-pausing under no-bid regimes; per-minute caps; laddered reserve floors during high volatility.

- Tools/products: “Primary Auction Monitor” dashboard tracking bid gap, participation, correlation with volatility; alerting and automated parameter adjustments.

- Assumptions/dependencies: accurate live telemetry; operator playbooks; safe automation limits.

- MEV intermediaries and searchers

- Productize just-in-time (JIT) resale lanes with transparent APIs and SLAs (e.g., 100 ms batching, latency/ordering guarantees).

- Tools/products: “Fast-Lane Broker API,” SDKs, latency attestation, per-transaction receipts; optional on-chain settlement path for auditability.

- Assumptions/dependencies: proximity hosting near sequencer; stable peering; fair queuing and anti-frontrun controls.

- Introduce hybrid payment models: on-chain fees for non-CEX clients; off-chain subscriptions for CEX–DEX arb with periodic on-chain attestations.

- Tools/products: payment hubs, signed invoices, Merkle-ized receipts; exporter for protocol-facing audits.

- Assumptions/dependencies: trust in off-chain settlement; dispute resolution mechanism; minimal latency overhead.

- Protocol governance and policy (DAOs, foundations)

- Establish transparency and oversight for secondary resale: require periodic reporting of resale volumes, effective prices, and access policies from JIT brokers.

- Tools/products: “MEV Surplus Dashboard” that decomposes searcher PnL, fees, and auction revenue; reseller self-reported metrics with cryptographic attestations.

- Assumptions/dependencies: cooperation by intermediaries; standard formats; privacy-preserving aggregation.

- Parameter stewardship workflows: routine reviews of reserve pricing, auction format, and participation trends; crisis playbooks for mass withdrawal or collusion signals.

- Tools/workflows: governance proposals templated with KPIs (bid gap, captured-PnL share, participation concentration).

- Data/analytics providers and researchers

- Adopt the paper’s event-study pipeline to measure auction competitiveness and surplus flows (bid-gap tracking, PnL markouts, volatility linkage).

- Tools/products: reusable Dune queries; “Markout PnL Analyzer” with 5s markouts; bidder/round joiners; public notebooks.

- Assumptions/dependencies: data coverage on DEXs and traces; markout simplifications (e.g., immediate CEX unwind) are acceptable for relative comparisons.

- Real-time collusion/tacit coordination indicators: monitor winner share, bid dispersion, and first–second price spread over time.

- Tools/workflows: anomaly detection on auction metrics; public scorecards for market health.

- Wallets, order flow aggregators, and UX providers

- Offer “priority routing” via reseller APIs for retail and pro users needing faster inclusion, with explicit pricing and success probabilities.

- Tools/products: fee estimator tied to minute-level fast-lane availability; opt-in toggle for urgent transactions.

- Assumptions/dependencies: user consent for extra fees; truthful SLA from resellers; avoidance of adverse selection.

- Exchange operations and HFT-style trading desks

- Integrate volatility-aware execution and bidding: scale fast-lane usage with σ; shift spend from primary auction to JIT resale when advantageous.

- Tools/workflows: strategy modules that map realized volatility to fast-lane budgets; post-trade markout audits to validate spend.

- Assumptions/dependencies: stable σ–profit link; predictable reseller access; low variance in per-trade returns.

Long-Term Applications

The following opportunities require additional research, protocol changes, standardization, or scaling.

- Mechanism design for priority markets across chains

- Protocol-native per-transaction priority auctions (continuous or micro-batched), internalizing the JIT resale function at the sequencer.

- Tools/products: “Continuous Priority Auction” module; secure micro-batch scheduler; fairness policies; robust anti-manipulation.

- Assumptions/dependencies: sequencer re-architecture; latency-safety; strong commitments to ordering rules; community consensus.

- Revenue-sharing with secondary markets: protocol fees on reseller-controlled fast-lane usage; rebates tied to measured delivered priority.

- Tools/workflows: attribution framework; on-chain metering of priority consumption.

- Assumptions/dependencies: measurable priority units; agreement on fair splits; auditability.

- Advanced, volatility-aware auction design

- Mechanisms that endogenize demand signals: predictive reserves from multi-asset volatility, liquidity, and mempool pressure; bandit-style reserve learning.

- Tools/products: “Adaptive Reserve Engine” using rolling windows, robust stats, and adversarial defenses; simulator for bidder response.

- Assumptions/dependencies: bidder adaptation to non-stationary reserves; oracle integrity; defense against price/volatility manipulation.

- Auction formats that degrade collusion incentives: randomization, commitment devices, cryptographic commitments, or periodic first-price/second-price mixing.

- Tools/workflows: formal mechanism analysis; experiments on testnets with real bidders.

- Market integrity and competition policy in Web3

- Frameworks to detect and deter hub-and-spoke tacit coordination in priority markets; disclosure standards for brokers (access criteria, fees, latency).

- Tools/products: standardized “Priority Market Disclosures”; third-party audits; public health metrics.

- Assumptions/dependencies: community norms; enforcement hooks (e.g., listing/allowlisting privileges); privacy vs transparency trade-offs.

- Cross-chain and cross-domain priority marketplaces

- Interoperable fast-lane brokers spanning several L2s/L3s with unified SLAs and cross-domain arbitration; portability of subscriptions.

- Tools/products: “Multi-Rollup Priority Router”; cross-chain receipts; escrow-based dispute settlement.

- Assumptions/dependencies: heterogeneous sequencer stacks; cross-domain messaging latency; regulatory considerations.

- Standardized telemetry and verification for off-chain payments

- Attested off-chain settlements with verifiable usage (e.g., signed per-batch statements, privacy-preserving proofs of fees paid).

- Tools/products: zk/commitment-based receipts aggregated per epoch; on-chain anchors for audits.

- Assumptions/dependencies: proof systems overhead; acceptance by parties; balancing data confidentiality with verifiability.

- Enhanced measurement science for MEV and surplus flows

- Richer PnL attribution models beyond 5s markouts: partial hedging, multi-venue liquidations, inventory risk, and cross-asset legs.

- Tools/workflows: data partnerships with CEXes/OTC; synthetic execution models; wider DEX protocol coverage.

- Assumptions/dependencies: data-sharing agreements; model identifiability; privacy constraints.

- Education and ecosystem capacity-building

- Curricula and case studies on ahead-of-time vs JIT auctions, surplus extraction, and collusion dynamics for market design and crypto-econ programs.

- Tools/products: open courses, simulators, reproducible datasets from the paper’s pipeline.

- Assumptions/dependencies: sustained data availability; collaborative teaching resources.

- Risk management products for participants

- Volatility-driven budgets and insurance for fast-lane spend; SLAs-backed coverage for failed priority delivery or delays.

- Tools/products: parametric covers keyed to latency/priority KPIs; spend caps that auto-adjust with σ regimes.

- Assumptions/dependencies: reliable measurement; enforceable SLAs; actuarial modeling for new risks.

- Governance playbooks and standards bodies

- Repeatable “auction crisis response” guidelines (e.g., sudden monopsony or mass bidder exit), and cross-protocol best-practices groups.

- Tools/workflows: formal KPIs (bid-gap thresholds, captured-PnL share bands) that trigger parameter changes; inter-chain working groups.

- Assumptions/dependencies: coordination across DAOs; willingness to align on norms; divergence in protocol objectives.

Notes on feasibility and dependencies common to multiple applications:

- The paper’s observed σ–demand linkage underpins reserve-pricing ideas; future market structure changes could weaken this relationship.

- Off-chain payment opacity complicates surplus accounting; adoption of attestations or partial on-chain settlement improves measurability.

- Mechanism changes (e.g., first-price, per-tx auctions) alter bidder strategies; careful simulation and phased deployment are essential.

- Latency-sensitive systems depend on low-jitter infra near sequencers and precise batching/ordering enforcement.

Glossary

- Ahead-of-time primary auction: An auction held before the actual execution window, selling rights (e.g., to priority ordering) in advance. "how the emergence of a just-in-time secondary market affects the dynamics of an ahead-of-time primary auction."

- Arbitrum rollup: A Layer-2 blockchain scaling solution that batches transactions off-chain and posts proofs on Ethereum. "Timeboost has been deployed on the Arbitrum rollup since April 17, 2025."

- Blockspace: The scarce capacity within a block to include transactions, which can be allocated or resold. "Similar dynamics are familiar from Layer-1 block-building auctions~\cite{flashbots_mevboost}, where builders resell blockspace to many different searchers."

- CEX--DEX arbitrage: Trading strategy that exploits price differences between centralized exchanges (CEX) and decentralized exchanges (DEX). "we classify a transaction as CEX--DEX arbitrage if it targets these contracts, emits only one swap-related event, and trades a known liquid pair involving WETH, WBTC, ARB, USDC, or USDT."

- Counterfactual: A hypothetical alternative scenario used to analyze what would have happened under different rules. "we consider a counterfactual in which the winning bidder pays the first price rather than the second price."

- Dynamic reserve price: A reserve price that adjusts with market conditions (e.g., volatility) rather than remaining fixed. "implement a dynamic reserve price that better responds to market conditions."

- FCFS (First-come, First-Served): A transaction ordering policy in which earlier arrivals are processed first. "First-come, First-Served (FCFS) transaction ordering policy"

- First-price auction: An auction format where the winner pays their own bid, often inducing bid shading. "switching to a first-price auction format could make anti-competitive bidding harder"

- Hub-and-spoke bidding coordination: A collusive structure where a central party (hub) coordinates with others (spokes) to reduce competition. "Kairos might effectively (although not necessarily deliberately) operate as a hub in a hub-and-spoke bidding coordination"

- i.i.d. random variables: Independent and identically distributed variables, a standard assumption in probability/statistics. "the mean of i.i.d. random variables is smaller than the expected maximum of these variables"

- Just-in-time secondary market: A resale market that allocates priority rights at the last moment, closer to execution time. "how the emergence of a just-in-time secondary market affects the dynamics of an ahead-of-time primary auction."

- Latency: The time delay in communication or processing that affects transaction priority and success. "The exact advantage depends on the latency between Kairos servers and the sequencer."

- Layer-1 block-building auctions: Auctions at the base blockchain layer that allocate the right to assemble blocks. "Similar dynamics are familiar from Layer-1 block-building auctions"

- Log returns: The logarithmic change in price between two time points, commonly used in volatility measurement. "We compute volatility as the standard deviation of log returns computed from consecutive one-second ETH/USDT mid-price observations."

- Markout: A method to estimate realized PnL by revaluing a position after a fixed time horizon. "we measure arbitrage returns using markouts."

- Mid-price: The average of the best bid and ask prices, used as a reference price. "We compute markouts using the mid-price."

- Net surplus: Total value generated minus payments/fees captured by the platform or auctioneer. "We define net surplus as"

- Non-atomic arbitrage: Arbitrage that does not execute in a single atomic transaction, often involving off-chain legs or latency risk. "specialized in non-atomic arbitrage"

- Off-chain payments: Payments settled outside the blockchain, often for speed or privacy reasons. "operates via a subscription model with off-chain payments."

- On-chain payments: Payments recorded directly on the blockchain as part of transactions. "Payments to Kairos are typically made on-chain as explicit ETH transfers"

- OTC markets: Over-the-counter venues where trades occur bilaterally outside centralized exchanges. "as well as OTC markets or markets on other chains serving as complementary venues"

- Parallel lane: A specialized fast-lane variant (in Kairos) dedicated to certain users/flows, operating separately from the main lane. "Kairos's parallel lane"

- Private value auction: An auction where each bidder’s valuation is known only to themselves and independent of others’ values. "consider a pure private value auction"

- Relative bid gap: The proportional difference between the highest (top) bid and the paid (second) bid. "relative bid gap between the top bid and the paid bid"

- Reserve price: The minimum acceptable price set by the seller in an auction. "via a second-price auction with a reserve price."

- Second-price auction: An auction where the highest bidder wins but pays the second-highest bid. "via a second-price auction with a reserve price."

- Searcher: A specialized actor that identifies and executes profitable on-chain strategies (e.g., arbitrage). "two searchers (Wintermute and Selini Capital)---specialized in non-atomic arbitrage---who have won the vast majority of auction rounds"

- Sequencer: The designated party ordering and including transactions in a rollup, enforcing priority rules. "the sequencer, which executes regular transactions with a 200\,ms delay"

- Sub auctions: Short, rapid auctions run within a larger allocation window to distribute priority on a finer timescale. "Kairos organizes fast-lane ``sub auctions'' with bidding phases of 100\,ms."

- Tacit coordination: Implicit, non-explicit collusion among bidders that reduces competition. "makes the market vulnerable to tacit coordination or collusion of bidders."

- Time advantage: A guaranteed priority window that allows faster execution relative to standard ordering. "The time advantage is 200\,ms and lasts 1 minute for the auction winner."

- Time-boosted transactions: Transactions submitted via the fast-lane that receive priority execution. "In total, we identify 7{,}299{,}376 time-boosted transactions executed during our study period."

- Timeboost (auction): Arbitrum’s mechanism selling fast-lane access via an ahead-of-time auction for priority ordering. "The Timeboost auction in Arbitrum~\cite{arbitrum_timeboost_gentle_intro} is the only major example to date of an ahead-of-time ``arbitrage auction'' for transaction ordering."

- Unbundling: Splitting a bundled right (e.g., a full minute of priority) into smaller units (e.g., per-transaction) to improve allocation efficiency. "Unbundling: The Timeboost auction whole-sells a 200\,ms time-advantage for an entire minute."

- Volatility: The magnitude of price fluctuations, often proxied by the standard deviation of returns. "continues to increase with external price volatility"

- WETH: Wrapped ETH, an ERC-20 representation of Ether used for interoperability with token-based protocols. "the most traded asset, namely WETH."

Collections

Sign up for free to add this paper to one or more collections.