- The paper presents a novel approach using Wiener chaos expansions to construct and calibrate arbitrage-free martingale models.

- It leverages explicit conditional expectations and advanced Monte Carlo techniques to achieve mean absolute errors as low as 7.23 bp in calibration.

- The method bypasses traditional parameterization, enabling rapid, flexible pricing of both plain vanilla and exotic options.

Framework and Methodological Innovations

The paper introduces a novel, highly flexible approach to financial model calibration grounded in the martingale representation theorem and Wiener chaos expansions. The authors construct a class of martingale models for the risk-neutral asset price by representing the terminal asset value as a truncated Wiener chaos expansion in Hermite polynomial basis, and then recover intermediate dynamics via explicit conditional expectations. By treating expansion coefficients as trainable parameters, the model achieves universality among square-integrable martingales driven by Brownian motion.

A significant methodological distinction is the direct calibration of chaos coefficients to observed option prices, bypassing the necessity for interpretable dynamical parameters as in traditional parametric models. The approach is theoretically justified by a universality result guaranteeing that, for sufficiently rich truncation, the model can approximate any Brownian-driven price process in MT2 up to arbitrary precision.

Chaos Expansion and Conditional Expectation Computation

The asset price terminal value ST is written as:

ST=∑n≥0∑∣a∣=ndaΦa,

where Φa denotes multivariate Hermite polynomial evaluations of stochastic integrals against Brownian paths, indexed over an orthonormal basis (piecewise-constant and Legendre polynomials are instantiated). The asset price process is then St=E[ST∣Ft], preserving the martingale property.

Computationally, piecewise-constant basis functions admit efficient and explicit expressions for conditional expectations, enabling scalable calibration. For general orthonormal bases, Malliavin calculus and the Dyson formula facilitate analytic evaluation of conditional expectations, allowing broader functional flexibility. The scalability and tractability of the approach are demonstrated for both basis types.

Calibration Procedure and Numerical Techniques

Calibration targets the European option surface by minimizing the Vega-weighted mean squared error between model and market prices, using gradient-based optimization (AdamW). Expectations required for model prices are estimated via Monte Carlo, with variance controls employing both polynomial-degree control variates and, where possible, quadrature methods for short maturities.

Monte Carlo estimator variance is further reduced by analytic calculation of second moments in the piecewise-constant case, providing two-dimensional control variates for higher accuracy and computational stability.

Empirical Validation and Robustness

The model is extensively validated via calibration to synthetic data from classical Heston and rough Heston models, as well as to real SPX market data. Both synthetic and real calibration experiments are performed under varying basis expansions and truncation levels.

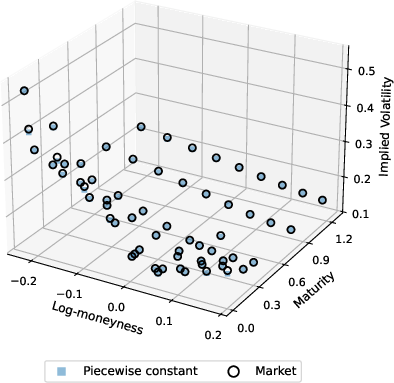

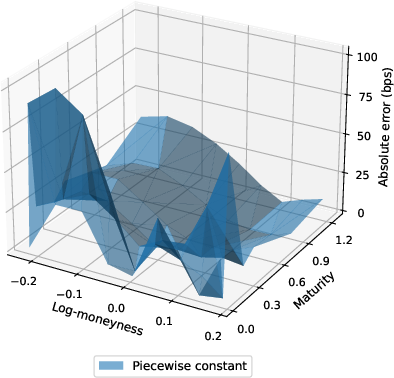

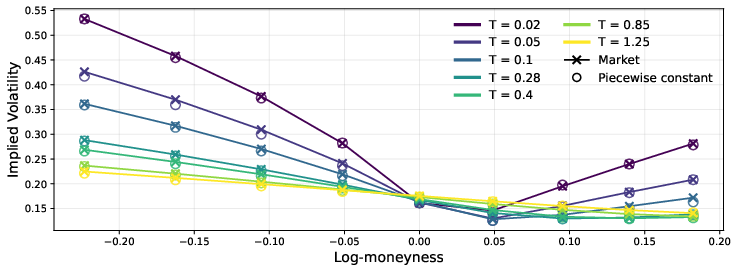

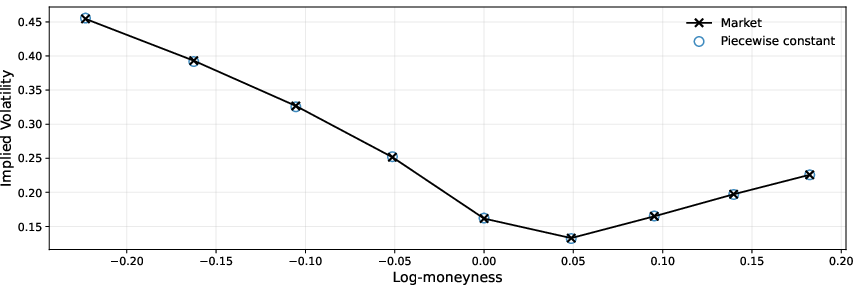

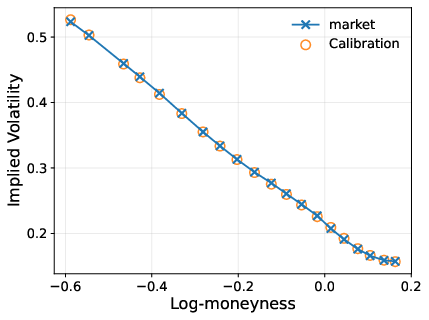

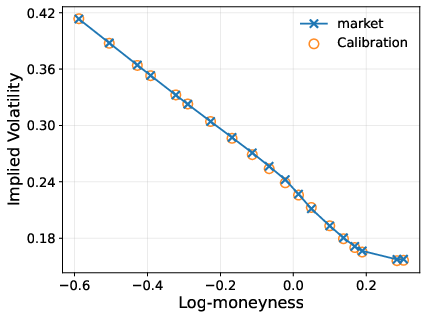

Figure 1: Implied-volatility surfaces at the calibrated maturities for the Heston model (top left) and corresponding absolute-error surfaces for piecewise-constant and Legendre bases; bottom panel shows implied-volatility smiles.

Results highlight that the model achieves strong accuracy in fitting implied-volatility surfaces for calibrated maturities, with mean absolute errors as low as 7.23 bp for the piecewise-constant basis and 8.80 bp for the Legendre basis. Calibration time is approximately $60$--$120$ seconds, demonstrating computational practicality.

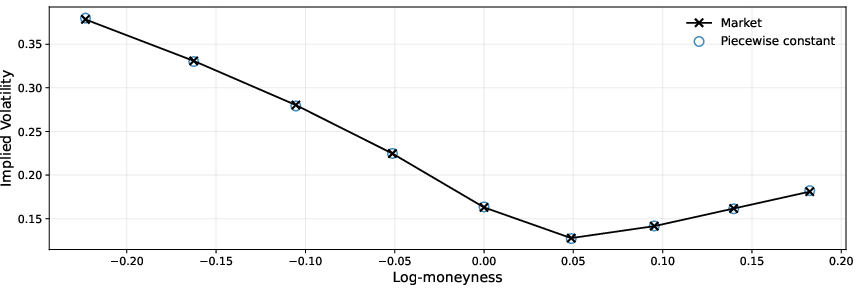

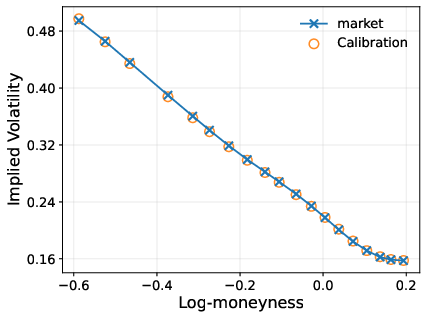

Figure 2: Implied-volatility surfaces at the non-calibrated maturities for the Heston model and corresponding absolute-error surfaces; MAE increases but remains competitive (16.62 bp for piecewise-constant, 34.95 bp for Legendre).

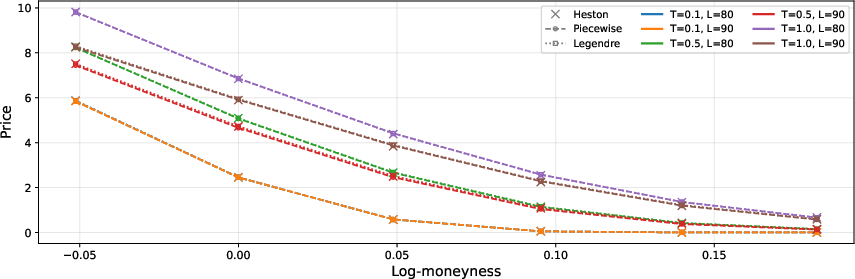

To probe robustness and economic plausibility, the model's ability to interpolate across maturities is examined, confirming stability and consistency with arbitrage-free dynamics. Out-of-sample testing is extended to the pricing of exotic, path-dependent contracts (forward-starting calls, down-and-out calls, and floating-strike lookbacks), with prices closely matching those from the underlying Heston dynamics for both base choices.

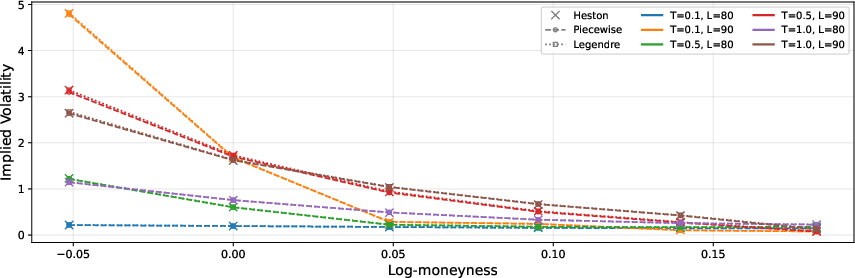

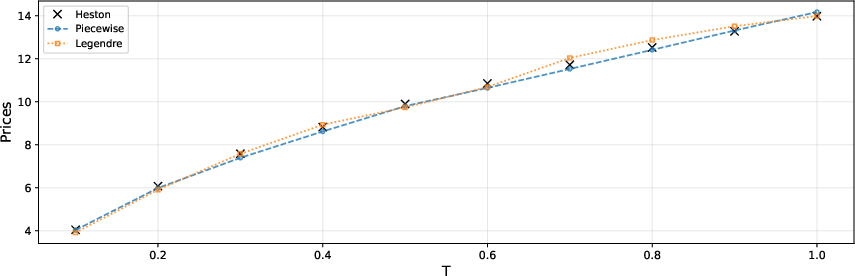

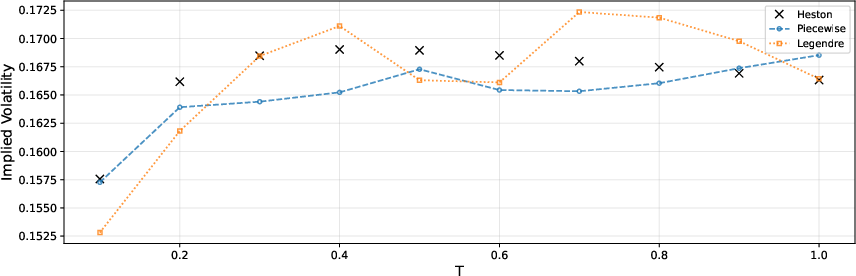

Figure 3: Forward starting call option comparison, showing alignment between price and implied volatility curves for chaos model versus Heston dynamics.

Figure 4: Down-and-Out call option comparison, indicating strong agreement in path-dependent pricing.

Figure 5: Floating strike lookback call options comparison; the chaos-based model captures the term-structure and implied-volatility curvature.

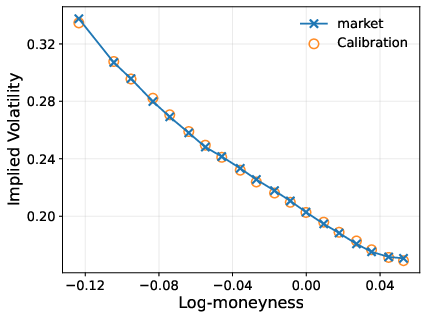

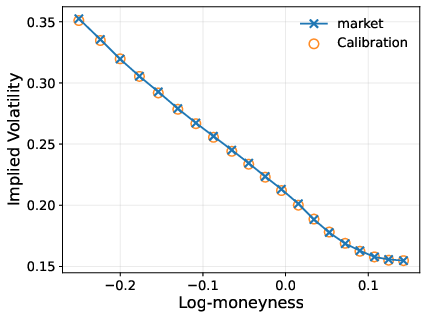

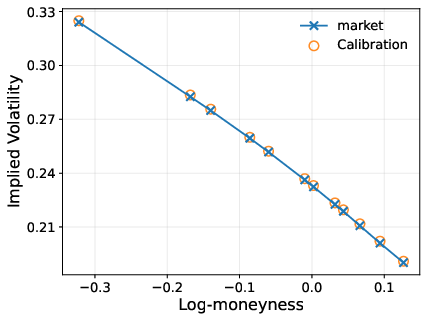

In the rough Heston example (with pronounced short-maturity skew), chaos-based calibration achieves MAE of 6.75 bp on calibrated maturities and 23.35 bp for non-calibrated maturities (piecewise-constant basis).

Figure 6: Implied volatility surfaces at the calibrated maturities for the rough Heston model; chaos model fits the full surface with low error.

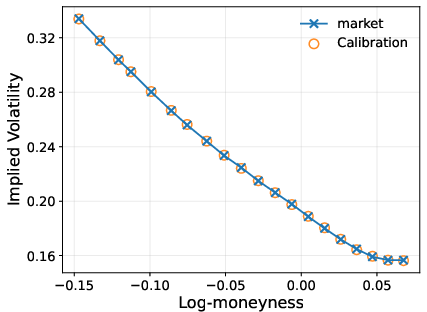

Figure 7: Implied volatility surfaces at the non-calibrated maturities for rough Heston; high-fidelity interpolation.

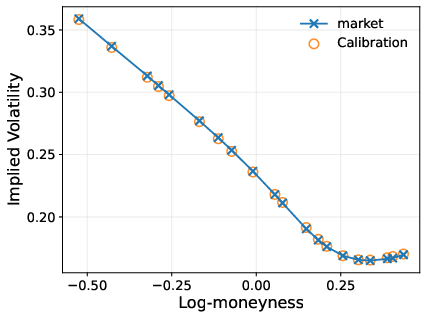

Short-maturity smile shapes (especially under rough volatility) are matched nearly perfectly, even for deep out-of-the-money strikes.

Figure 8: Implied volatility fits to short maturities in the rough Heston model, demonstrating precision for both synthetic and real moneyness.

Application to Real Market Data

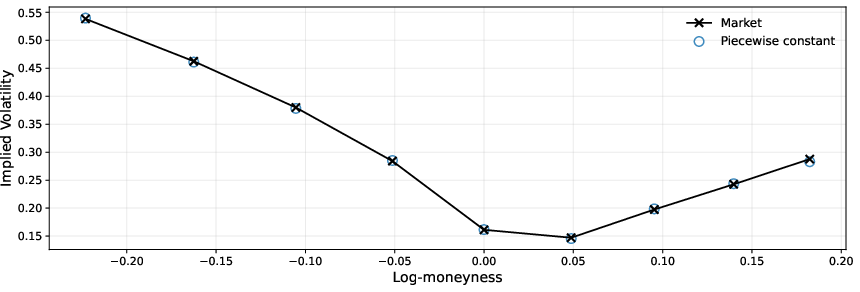

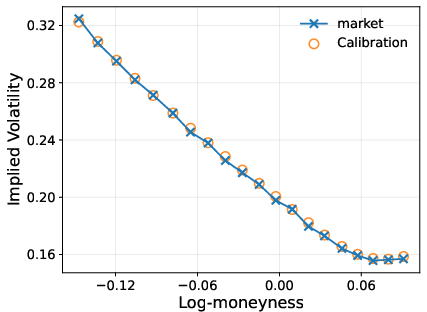

The model is calibrated to SPX options (nine maturities, broad moneyness range), reaching an MAE of 11.32 bp and fitting the volatility surface with high precision.

Figure 9: Calibrated implied volatility smiles from SPX data; observed (blue) and fitted (orange) volatilities show near-perfect overlap across maturities.

These results underscore the model's ability to generalize to real market data, offering practical utility for dynamic calibration, risk management, and exotic derivative pricing.

Implications and Outlook

The Wiener chaos martingale model defines an over-parameterized, universal class of risk-neutral price processes, capable of reproducing arbitrary Brownian-driven dynamics. This expresses flexibility exceeding traditional parametric models and aligns with contemporary signature and neural SDE approaches, while preserving analytic tractability and arbitrage-free consistency.

By decoupling model specification from explicit interpretability of dynamic parameters, applications extend to rapid recalibration, real-time risk management, and the accurate pricing of illiquid, path-dependent derivatives. Theoretically, the universality property provides a foundation for statistical studies of market model adequacy, model risk, and dynamic hedging strategies.

Future developments may include extension to Lévy-driven chaos, integration with neural network architectures for further expressivity, and real-time deployment in electronic markets. Deeper investigation into pathwise regularity and the behavior across stochastic volatility regimes remains warranted for both theoretical and practical enhancement.

Conclusion

The presented Wiener chaos martingale modelling framework offers a theoretically rigorous and empirically validated approach to implied-volatility calibration and asset price modelling. It combines universality, computational efficiency, and arbitrage-free dynamics, enabling both routine and advanced applications in quantitative finance. Numerical evidence demonstrates competitive or superior accuracy compared to established models for both plain vanilla and exotic options. The approach promises significant future impact in robust calibration and derivative pricing.