- The paper establishes that traditional founder credentials, including FAANG experience and top-tier education, explain less than 4% of funding variation.

- The paper employs rigorous regression analysis with temporal controls, revealing that each additional co-founder is associated with a 21% increase in total funding.

- The paper demonstrates that while business education and consulting/finance backgrounds show larger raw funding differences, only team size remains a robust predictor after accounting for batch year effects.

Founder Backgrounds and Startup Funding in Y Combinator: An Empirical Assessment

Overview and Motivation

This paper, "Founder Backgrounds and Startup Funding: Evidence from Y Combinator" (2512.13755), presents an empirical analysis of founder human capital and team composition predictive power for startup funding within the Y Combinator (YC) ecosystem, leveraging a newly merged dataset of 4,323 YC companies and S&P Global funding records spanning 2005–2024. The central critique addressed is whether, within the elite post-selection environment of YC, credentialed signals such as top-tier education, prior FAANG (Facebook/Meta, Apple, Amazon, Netflix, Google) experience, and team size contribute materially to capital acquisition outcomes, or whether other unobserved factors dominate. This inquiry is significant given the heavy reliance among investors and accelerator operators on founder pedigree for financing decisions and resource allocation.

Data Construction and Stylized Facts

The study undertakes comprehensive cross-sectional matching—achieving a 62.2% match rate—between YC company records (enriched using manual extraction and AI-assisted workflows) and funding transaction data from S&P Global, producing a well-structured regression sample of 2,113 companies with complete observability. The dataset enables quantification of technical and business education, prior company affiliations (including FAANG membership and prior YC startups), and fine-grained demographics (mean age, years since university, number of co-founders).

Substantial heterogeneity is observed in work experience (mean: 4.13 prior companies per founder), team composition (founders/company: mean 1.90, SD 0.80), and domain backgrounds (technical education: 38.2%, business education: 17.5%, consulting/finance: 9.9%). Funding outcomes are highly skewed (mean: \$23.36M, median: \$2.15M), with batch year and market conditions substantially influencing average amounts.

Figure 1: Mean funding by founders with versus without technical education shows minimal difference, suggesting technical education has limited predictive power for capital raised.

Figure 2: Mean funding by business education highlights a slightly higher capital acquisition for business-educated founders, though the effect size is minor.

Figure 3: Distribution of mean prior companies per founder indicates most YC founders possess moderate to substantial work histories—important for human capital theorizing.

Figure 4: Companies with at least one founder who worked at a prior YC company exhibit only marginally higher mean funding.

Figure 5: Companies with founders who have top tech experience (beyond FAANG) show only modest differences in mean funding, undermining universal transferability of “brand” signals.

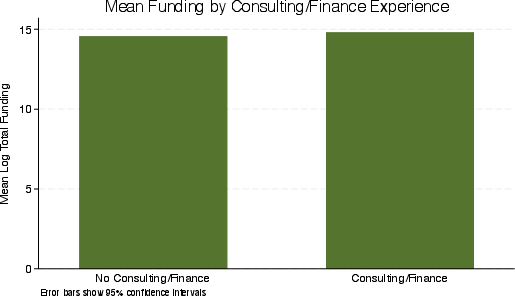

Figure 6: Consulting/finance experience is associated with a pronounced (27%) increase in mean funding, identifying these backgrounds as the strongest human capital signal in raw statistics.

Empirical Approach and Limitations

The regression design specifies log-transformed total funding as the dependent variable, regressing on FAANG experience, founder count, batch year FE, and top school attendance. Fixed effects control for temporal variance (driven by batch year and market cycles); limitations include lack of reliable industry categorization (preventing sector controls), high missingness in education data, and confounds due to non-random assignment of founder backgrounds. R-squared statistics (0.006 to 0.035) highlight the extremely low proportion of explained variance, indicating that observed credentials account for less than 4% of funding outcomes.

Main Findings and Robustness

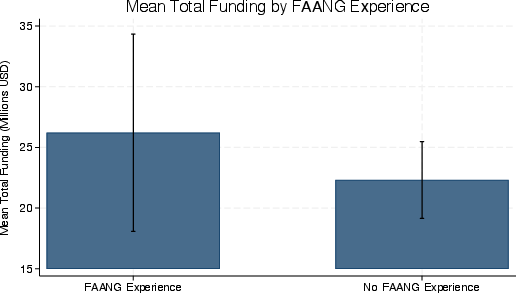

Contrary to popular belief and initial raw averages, FAANG experience is not a robust predictor of funding. In the primary specification (Model 2), the FAANG coefficient is negative (-0.251, p=0.057), suggesting 22% less funding for FAANG-experienced founders; however, robustness checks reveal sign flips and loss of significance when controlling for model specification, sample restrictions, and alternative dependent variables—raising concerns about substantial confounding and non-causal inference.

In contrast, founder team size is a reliable driver across specifications: each additional co-founder is associated with approximately 21% higher total funding (p<0.001), underscoring the importance of complementary skills and perceived execution capacity in VC evaluations.

Notably, business education and consulting/finance backgrounds yield the largest raw funding differentials, but their effects are not robust to multivariate controls. Temporal and market effects (batch year) are substantial, and controlling for these confounds is essential to prevent spurious founder background associations.

Figure 7: Funding as a function of years since university—founders with greater maturity display only a weak positive relationship with capital raised.

Figure 8: Normal distribution of years since university graduation, centering founder ages in the early 30s.

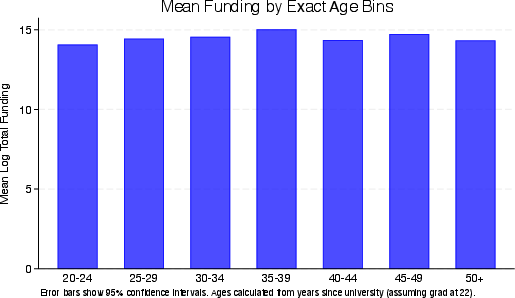

Figure 9: Funding by exact age bins—mid-30s founders raise the highest capital, with diminishing returns past 40.

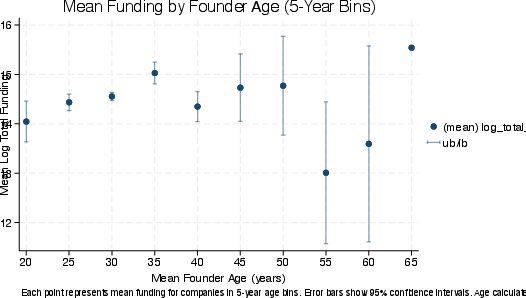

Figure 10: Funding by founder age in 5-year bins confirms that ages 35–39 mark the fundraising peak for YC alumni.

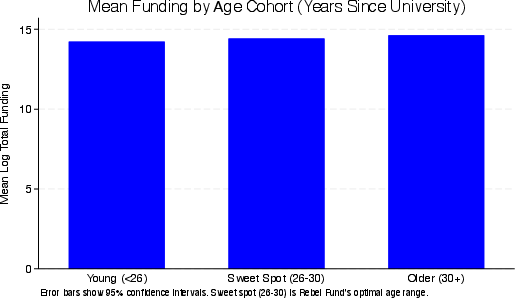

Figure 11: Funding by age cohort based on years since university—older founders show the highest mean funding in this sample.

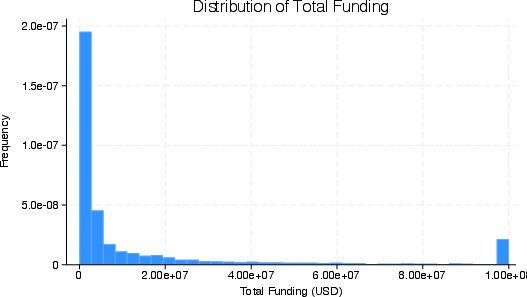

Figure 12: Distribution of total funding amounts is highly right-skewed, underscoring the power-law nature of VC outcomes.

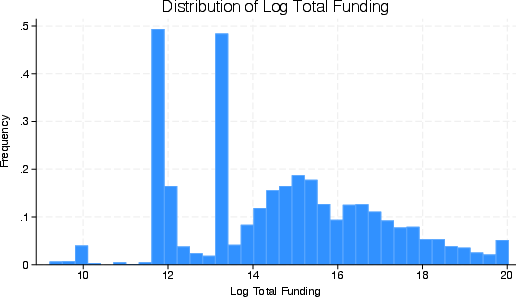

Figure 13: Log-transformed funding distribution is approximately normal, justifying log-linear regression approaches.

Figure 14: Mean total funding by FAANG experience visualizes the raw difference but with overlapping confidence intervals, indicating statistical insignificance after controls.

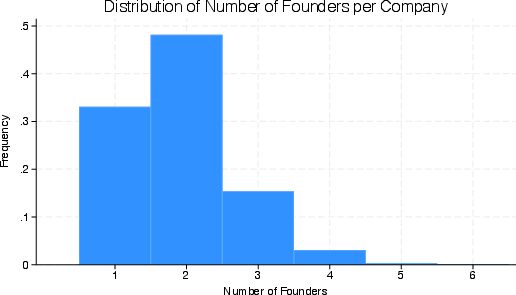

Figure 15: Distribution of founder count per company—most YC startups are founded by small teams (1–2 founders).

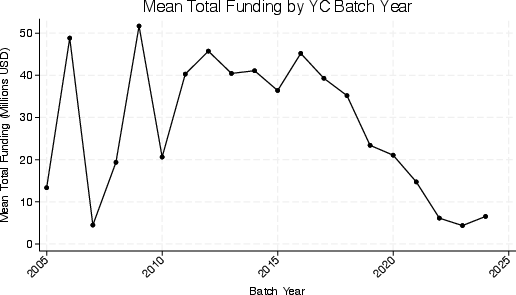

Figure 16: Temporal patterns in mean funding by YC batch year reflect market and accelerator selection fluctuations.

Theoretical and Practical Implications

The empirical evidence from YC startups suggests that observable founder credentials (education, FAANG, top tech, consulting/finance) have only marginal and inconsistent explanatory power for eventual capital raised, once batch year and temporal effects are taken into account. Team composition, specifically the number of founding members, emerges as the sole robust predictor among measured characteristics. This points to a context where accelerator “branding” (YC certification) may supersede individual credential signaling, consistent with quality certification theories in entrepreneurial finance.

For accelerator operators and VCs, this shifts focus from founder pedigree to collective team attributes (depth, diversity, complementary skills) and underscores the dominance of other, unobserved factors—likely product-market fit, industry waves, and dynamic market conditions. From a theoretical standpoint, the findings question human capital-centric investing narratives and highlight the necessity for methodological rigor when exploring founder effects in pre-selected, prestigious populations.

Limitations and Directions for Future Research

Key limitations include selection bias (partial dataset matching), endogeneity in team formation, missing education and industry data, absence of transaction-level temporal granularity, and inability to control for product or geographic effects. The low explanatory power of models calls for expanded, panelized datasets with instrumented or exogenous founder background shocks to parse causal mechanisms. Inclusion of comprehensive product and market variables, as well as sector-specific fixed effects, is advisable for future work. Panel data tracking fundraising milestones beyond Series A (timing, size, investor composition) will provide more granular evidence on founder influence over venture trajectories.

Conclusion

Within the Y Combinator ecosystem, the predictive power of founder credentials for startup funding outcomes post-acceptance is demonstrably weak, with less than 4% of funding variation explained. Team size is the only robust, positive predictor of capital raised. FAANG experience and educational pedigree do not consistently correlate with higher funding when controlling for batch year and compositional effects, pointing to the preeminence of unobserved factors such as industry, product quality, and timing in venture outcomes. These findings recalibrate practical and scholarly perceptions of founder signals as investment drivers and spotlight the need for methodologically robust, sector-contextualized research.