- The paper introduces novel Monte Carlo estimators, emphasizing variance reduction via indirect and control variate methods.

- It presents an empirical evaluation using Bauer’s models and an openIRM to demonstrate estimator convergence and efficiency.

- Findings highlight that optimal estimator selection is model-specific, reducing simulation costs under modern solvency regimes.

Estimation of Own Funds for Life Insurers: Direct, Indirect, and Control Variate Methods for Risk-Neutral Pricing

Introduction

The paper "On the Estimation of Own Funds for Life Insurers: A Study of Direct, Indirect, and Control Variate Methods in a Risk-Neutral Pricing Framework" (2511.04412) delivers a rigorous comparative analysis of Monte Carlo estimation methodologies for computing own funds of life insurers. Focusing on risk-neutral valuation, it scrutinizes direct, indirect, and control variate approaches for high-fidelity fair value assessment of insurance guarantees, providing both methodological innovation and empirical evaluation. The study is situated within the context of efficient capital requirement calculation under advanced European solvency regimes (Solvency II, IFRS 17), where computational efficiency and estimator precision are key.

Methodology Framework

The work conducts its analysis in the context of multi-period, stochastic models for participating life insurance contracts with profit-sharing and complex option-like features, specifically focusing on nested simulation environments. The direct approach computes expected discounted future profits (DFPs) under risk-neutral dynamics. The indirect approach leverages the link between the own funds and observable cash flows, such as policyholder distributions and shareholder outflows, to construct alternative (but unbiased) estimators. The control variate (CV) methods utilize auxiliary variables analytically or numerically correlated with the target payoff to achieve variance reduction.

The study formalizes all estimators and variance reduction schemes in a unified notation and provides theoretical variance and correlation diagnostics, showing under which model regimes the indirect or CV approaches yield substantial computational gains.

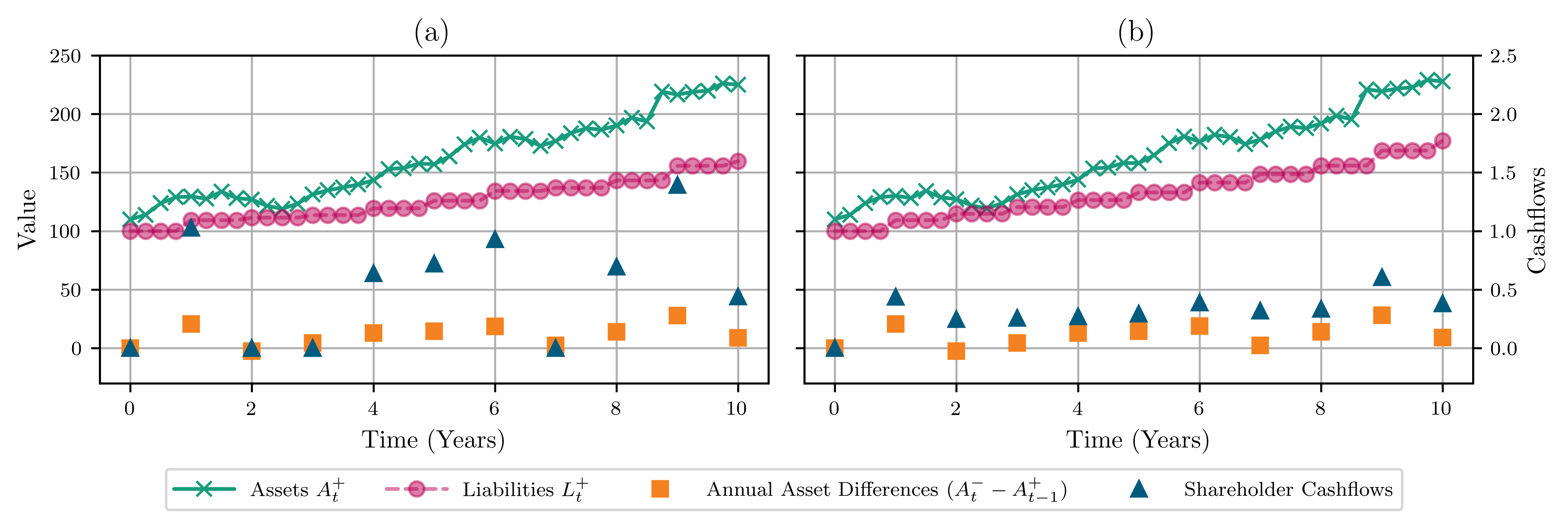

Figure 1: Bauer's model with (a) MUST and (b) IS case for a single representative simulation. Shareholder cash flow is plotted on the right y-axis, with all other quantities corresponding to the left y-axis.

Simulation Study and Estimator Distribution Analysis

A sequence of experiments is conducted on both stylized models adapted from the literature (Bauer's MUST and IS regimes) and a realistic open source internal risk model (openIRM). The study includes thorough statistical analysis across a sweep of model parameters, demonstrating estimator distributions, convergence properties, and sensitivity with respect to contract and market parameters.

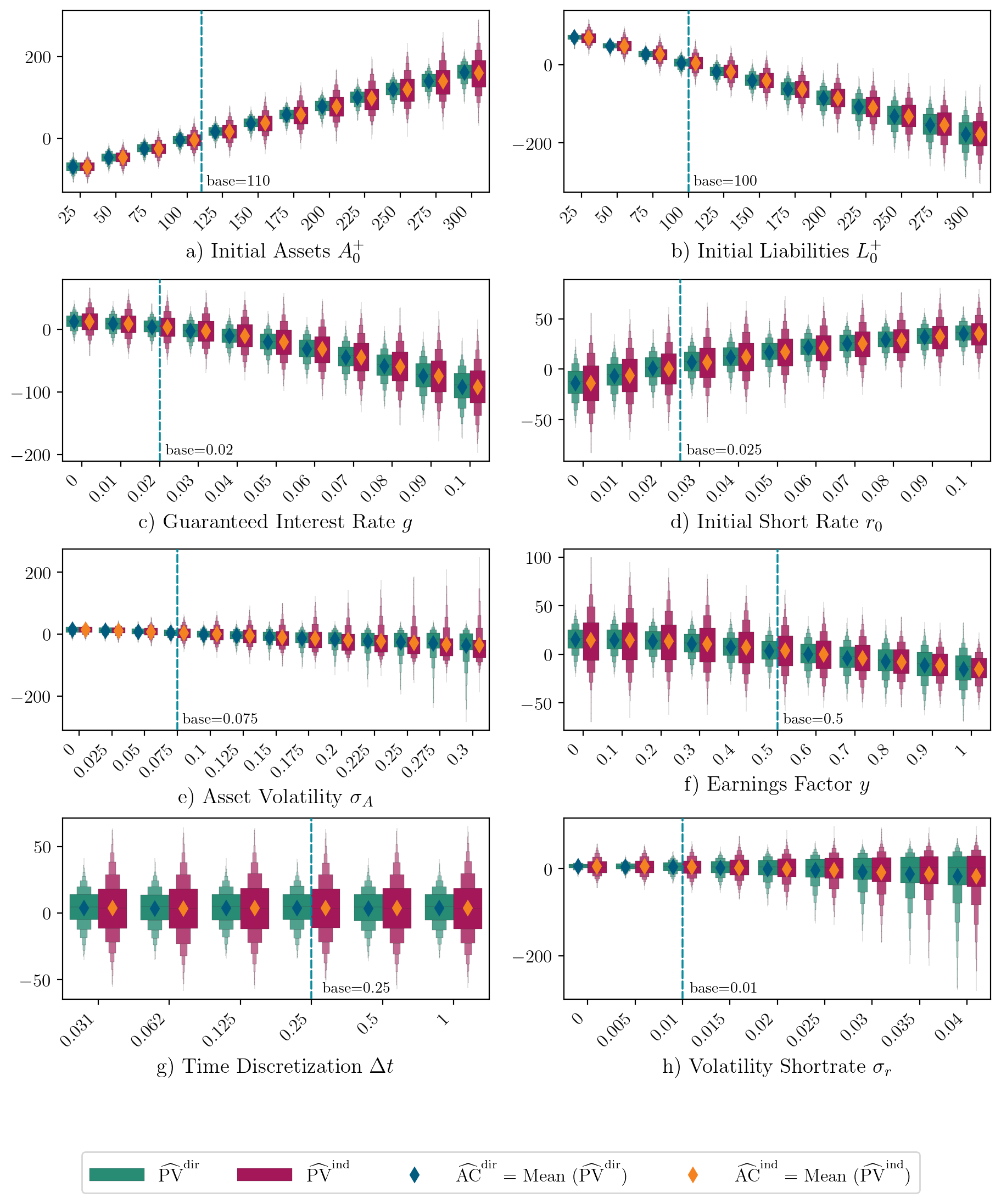

Figure 2: Distribution of direct and indirect estimators for varying parameters in Bauer's model, MUST case. The 100 outermost values on each side were removed for better visual clarity.

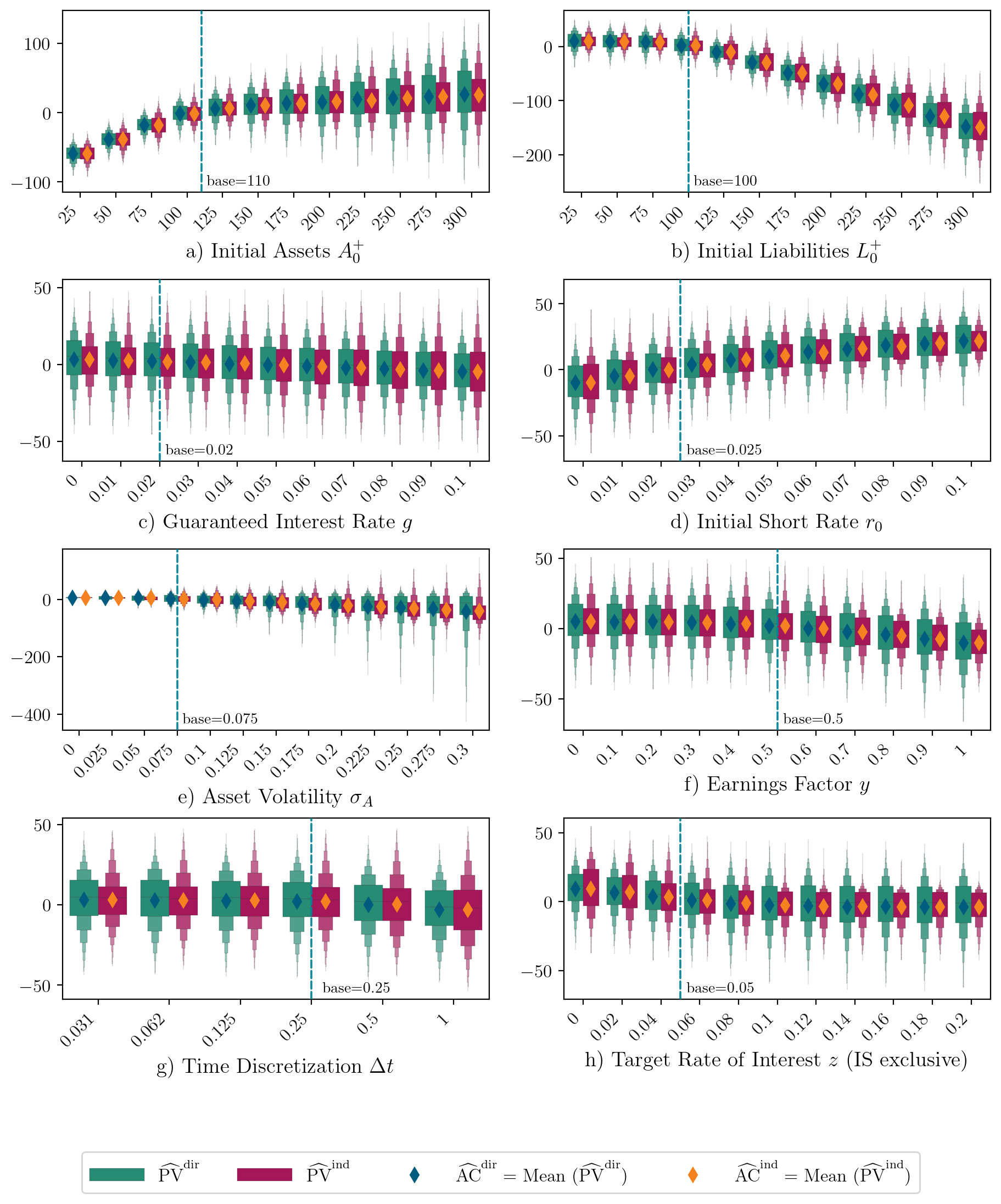

Figure 3: Distribution of direct and indirect estimators for varying parameters in Bauer's model, IS case. The 100 outermost values on each side were removed for better visual clarity.

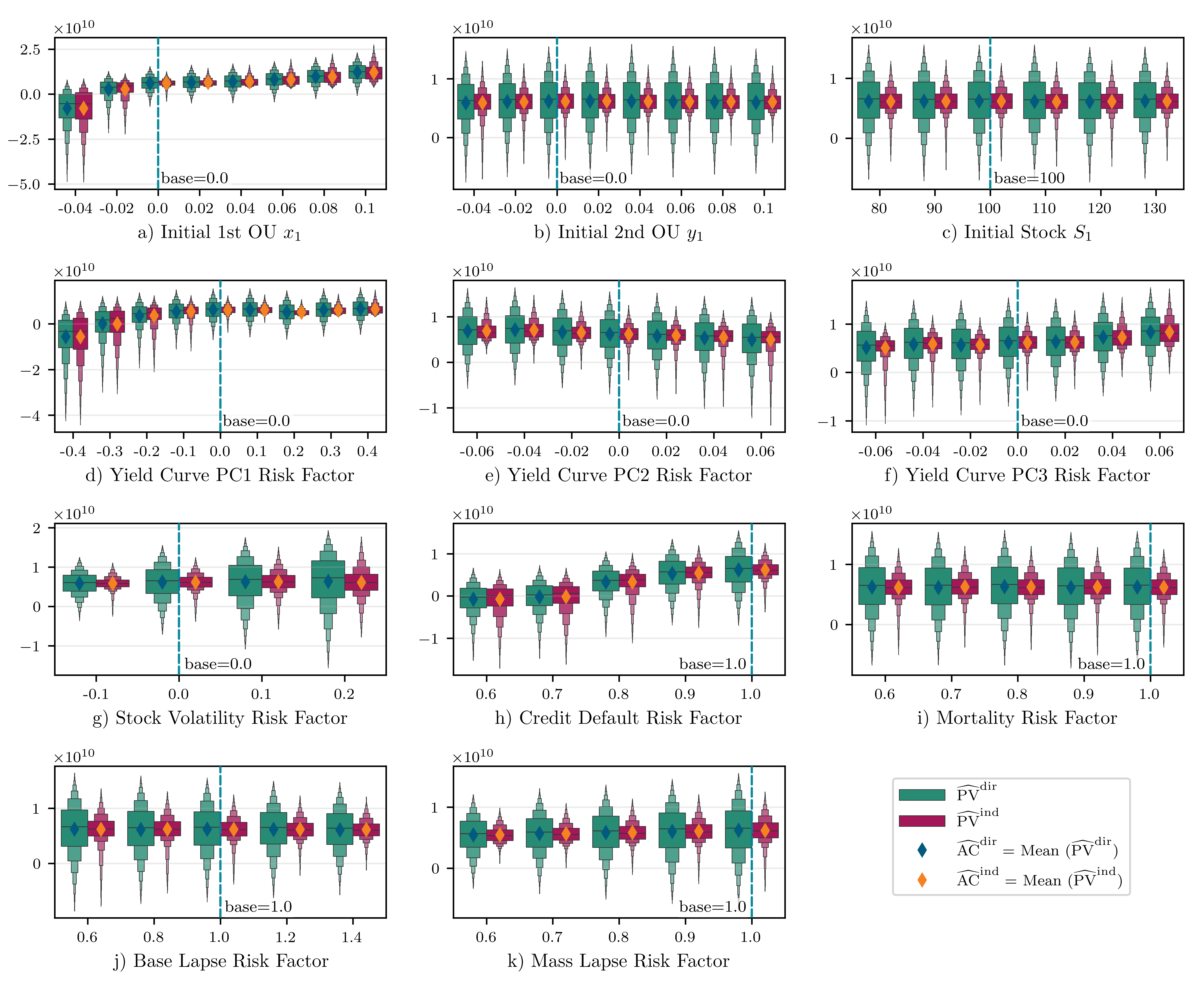

Figure 4: Distribution of direct and indirect estimators for varying parameters in openIRM. The 100 outermost values on each side were removed for better visual clarity.

The findings reveal that the indirect estimator, which relies primarily on cash flow projections rather than terminal value simulations, achieves significant variance reduction in certain contractual regimes (especially when profit-sharing dominates). The CV estimator further improves variance, with gains highly parameter-dependent.

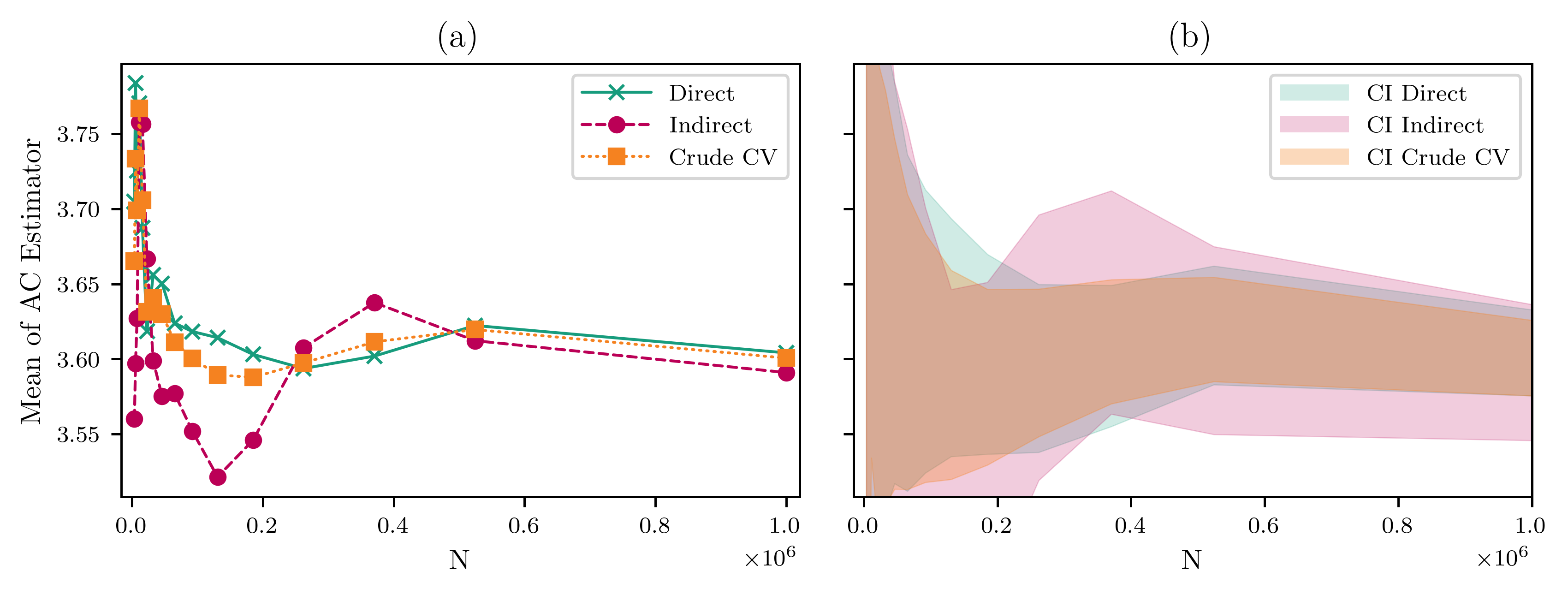

Figure 5: Comparison of direct, indirect, and crude control variate estimator for Bauer's model MUST case for varying number of observations N. (a) The estimated value given by the mean. (b) Approximate 95\% confidence intervals for estimators.

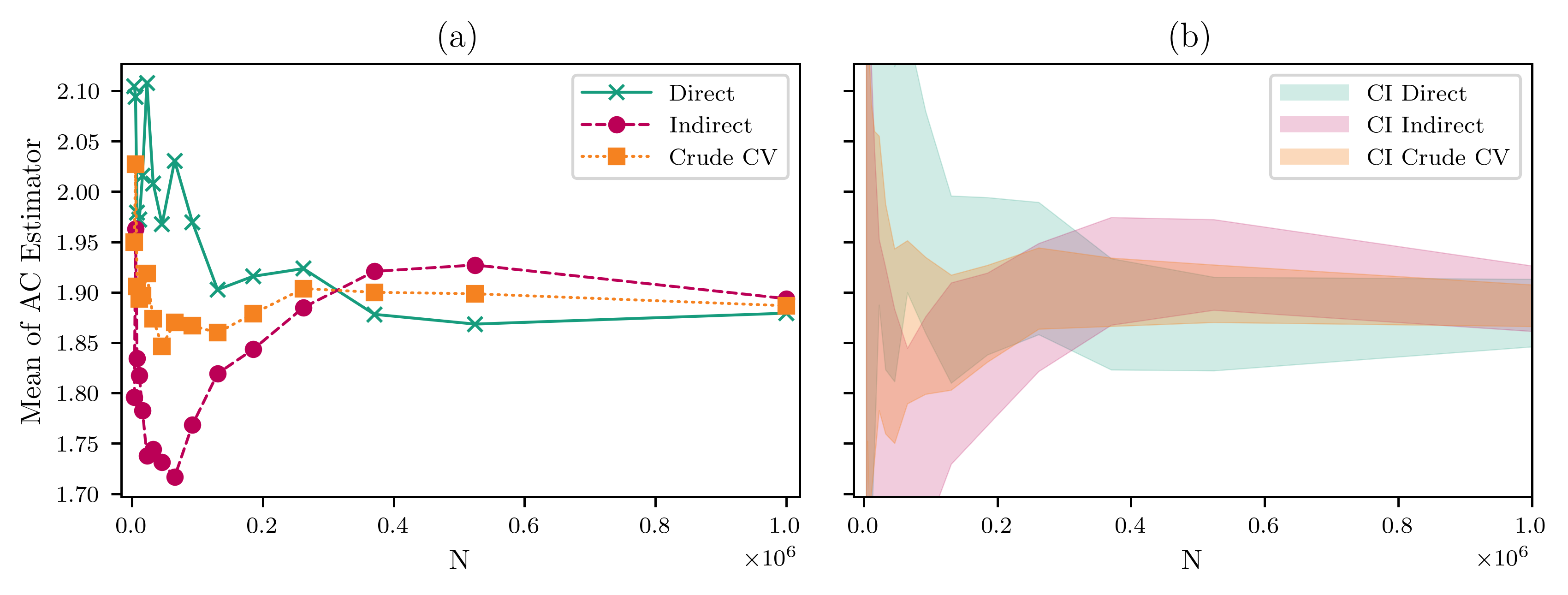

Figure 6: Comparison of direct, indirect, and crude control variate estimator for Bauer's model IS case for varying number of observations N. The crude control variate estimator estimates the coefficient b only with the available subset of N observations. (a) The estimated value given by the mean. (b) Approximate 95\% confidence intervals for estimators.

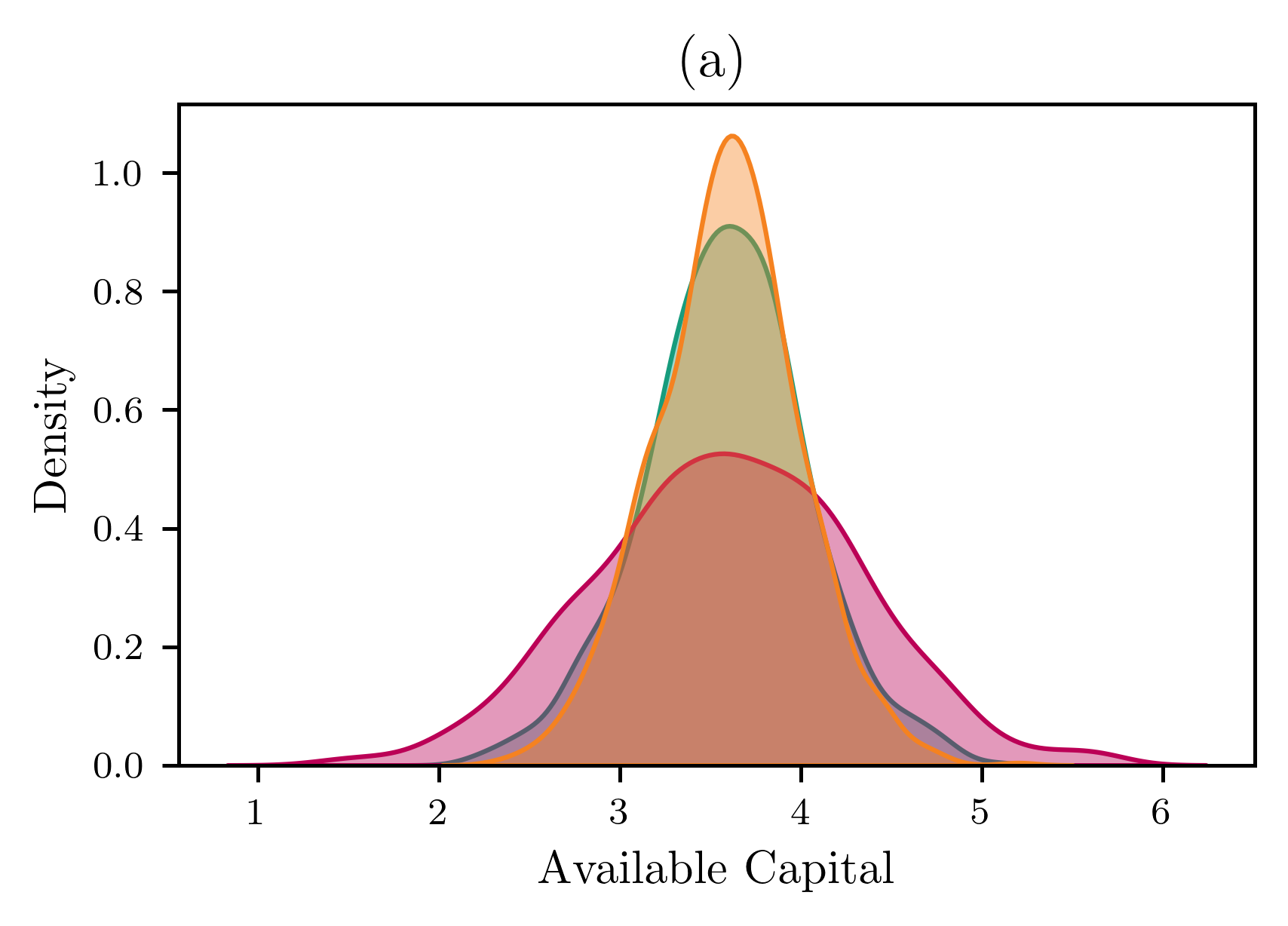

Figure 7: Comparison of direct, indirect, and crude control variate estimator's distribution (approximated with a Kernel Density Estimation) in Bauer's model (a) MUST and (b) IS case for 1,000 different estimations using 1,000 simulations each.

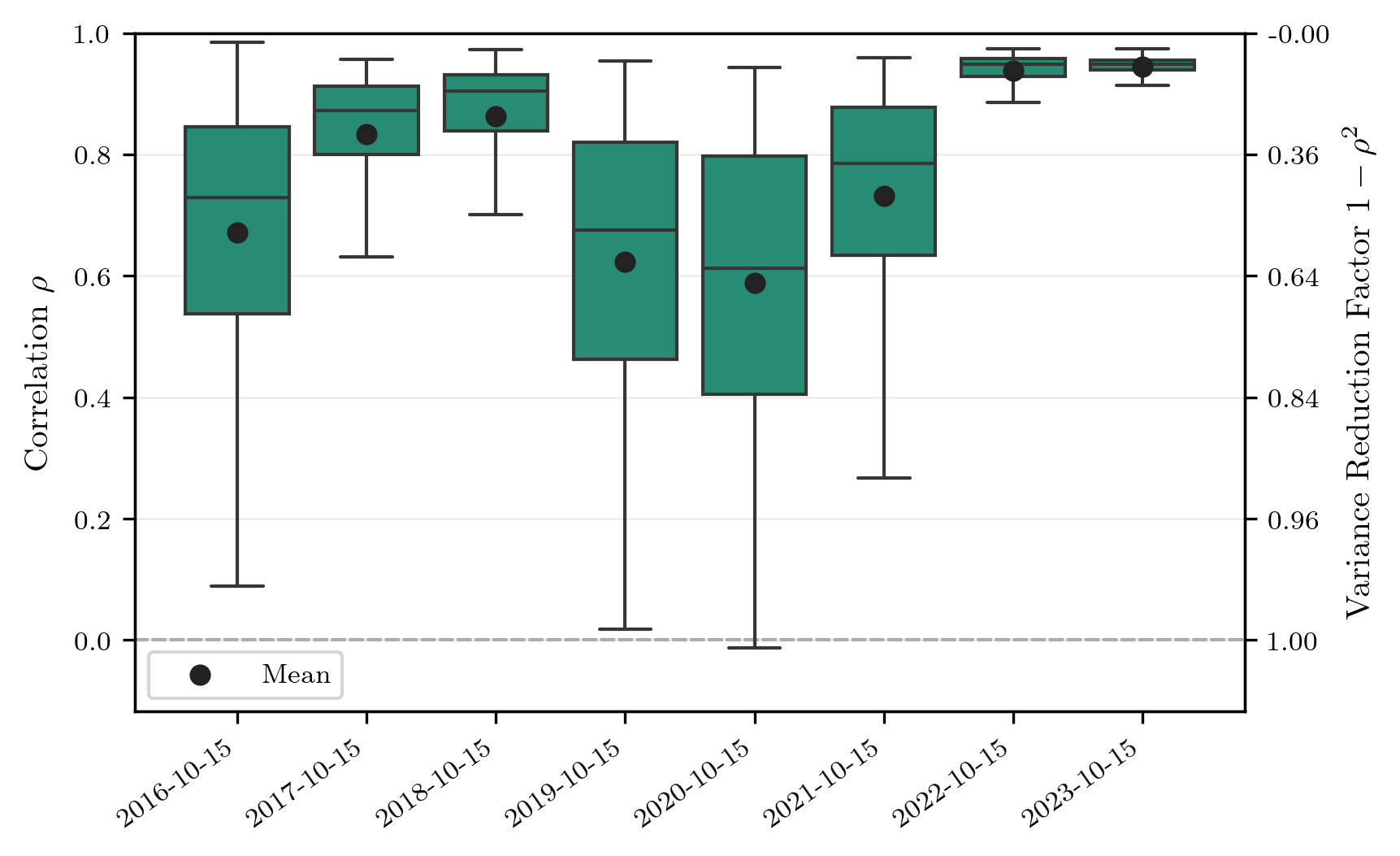

Variance Reduction and Correlation Behavior

The correlation structure between candidate control variates and the desired estimator is systematically analyzed. The variance reduction factor, a key efficiency indicator, is empirically quantified as 1−ρ2 for correlation coefficient ρ.

Figure 8: Correlation ρ and variance reduction factor 1−ρ2 of indirect and direct estimators for 1,000 estimations in openIRM across years.

The analysis documents that the indirect estimator often closely tracks the direct estimator, especially for cases with high policyholder profit-sharing or in mature portfolios, supporting aggressive variance reduction through control variates. However, structural breaks due to profit-sharing regime shifts or differences in shareholder payouts can restrict effectiveness, highlighting the requirement for model-specific estimator design.

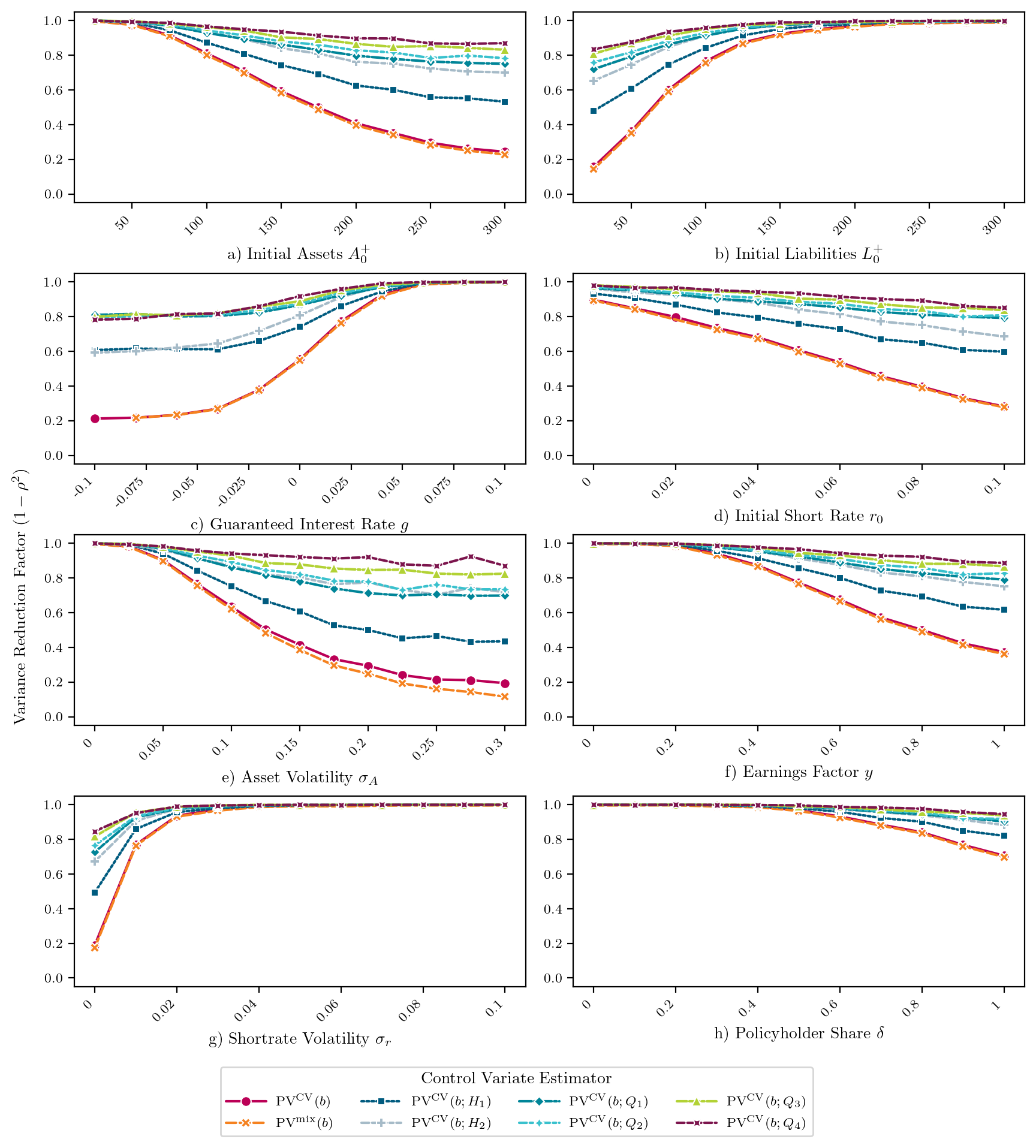

Figure 9: Variance reduction factor for various mixed control variate estimators for varying parameters in Bauer's model, MUST case. Mixed controls used: different temporal partitions. The indirect method consistently achieves superior variance reduction in single control settings.

Practical and Theoretical Implications

The principal practical implication is the reduction of simulation cost for life insurer's own fund and liability computations under modern valuation regimes. In regimes with appropriately selected cash-flow-based control variates, the computational budget can be reduced by orders of magnitude for fixed estimator variance—a critical improvement for real-world regulatory applications merging complex multi-period asset-liability dynamics.

Theoretically, the study demonstrates that the structural design of insurance contracts (profit-sharing rules, guarantee structure) dictates the optimal estimator family and the magnitude of achievable variance reduction. This provides a decision framework for actuaries and financial engineers to select estimator configurations tailored to the contract and risk landscape, especially in nested or multi-regime environments.

Conclusion

This work establishes a comprehensive statistical and practical foundation for the selection and deployment of advanced Monte Carlo estimation strategies—direct, indirect, and control variate—in the context of own funds calculation for life insurers. It quantifies estimator behavior across a spectrum of realistic parameter settings, offers a blueprint for model-specific estimator choice, and demonstrates strong variance reduction when indirect and control variate approaches are judiciously applied. Ultimately, the findings enable high-precision, low-cost regulatory capital and fair value computation under contemporary solvency regimes, with substantial prospects for further optimization in actuarial risk analytics and financial engineering for insurance liabilities.