- The paper presents a constructive method for identifying the viable state space as a linear transformation of the nonnegative orthant.

- It develops a multifactor Markovian approximation framework that guarantees simulation well-definedness via M-matrix conditions.

- The explicit domain characterization improves the setup of PDE methods and calibration techniques in rough volatility models.

State Spaces of Multifactor Approximations of Nonnegative Volterra Processes

Introduction and Motivation

Multifactor Markovian approximations have become an essential tool for approximating nonnegative Volterra processes, especially in the context of rough volatility models such as the rough Heston model. The critical issue in such approximations is a rigorous characterization of the viable state space—that is, determining the subset of RN in which the multifactor Markovian process remains, ensuring, for instance, the non-negativity of the aggregated volatility process. The explicit identification of this state space has multiple implications: it underpins well-defined simulation schemes, ensures the correctness of PDE methods for pricing, improves model calibration, and directly impacts the efficiency and reliability of numerical solvers.

Multifactor Markovian Approximation Framework

Consider a nonnegative stochastic Volterra process Yt of the form:

Yt=Y0+∫0tK(t−s)b(Ys)ds+∫0tK(t−s)σ(Ys)dWs,

where the kernel K is a positive weighted sum of exponentials (a Prony series),

K(t)=∑i=1Nwie−xit

with positive nodes x=(xi) and weights w=(wi). Functions b and σ satisfy nonnegativity-preserving boundary conditions at $0$.

The multifactor Markovian approximation rewrites Yt as the linear combination

Yt=∑i=1NwiYt(i)

where each Yt(i) evolves by

dYt(i)=−xi(Yt(i)−y0(i))dt+b(Yt)dt+σ(Yt)dWt,

yielding an N-dimensional SDE for Yt with coupled dissipative and nonlinear "CIR-type" dynamics.

The main technical question is: Given a set of initial values Y0, can it be characterized precisely when Yt remains in a subset D of RN ensuring the nonnegativity of the aggregate Yt?

Explicit Construction of the State Space

The paper proves that the viable state space D for the multifactor Markovian process can always be written as a linear transformation of the nonnegative orthant, i.e.,

D=Q−1R+N

where Q is an admissible matrix defined by:

- Invertibility.

- Q maps the N-th standard basis vector to the weights: eN⊤Q=w⊤.

- Q maps the vector of ones to a multiple of eN: Q1=weN.

- Off-diagonal entries of Qdiag(x)Q−1 are nonpositive, enforcing an "M-matrix" structure.

A crucial result (Theorem~2.2) provides a constructive method for such Q. In the special case N=2, the domain is

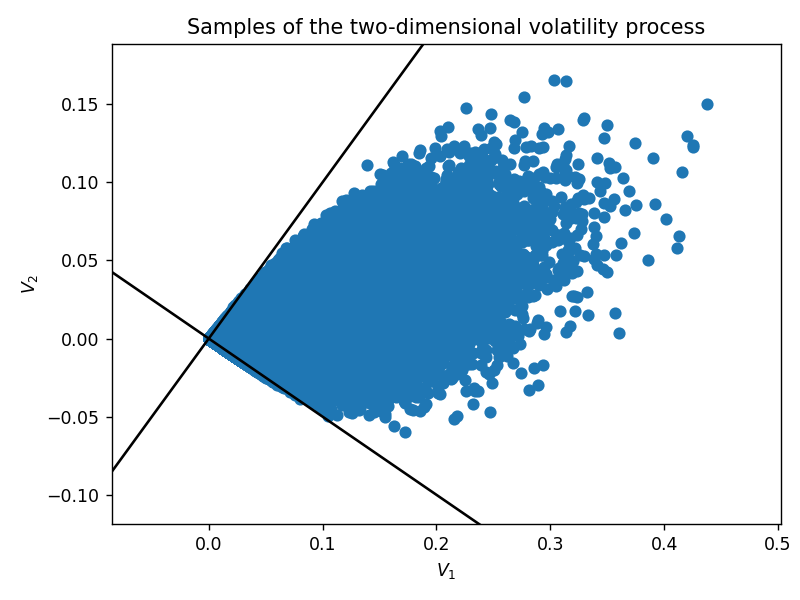

D={y∈R+2:w1y1+w2y2≥0, y1≥y2}

which is a cone intersecting the half-plane of nonnegative aggregate volatility.

Figure 1: Samples of the two-dimensional process Y=(Y(1),Y(2)) on a large time grid showing the support cone determined by explicit state space characterization.

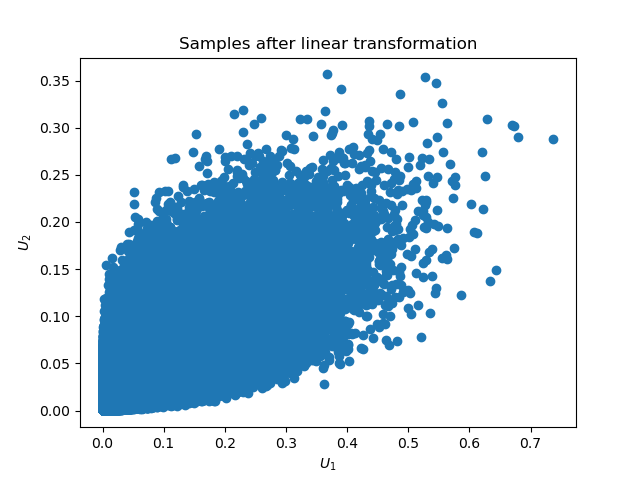

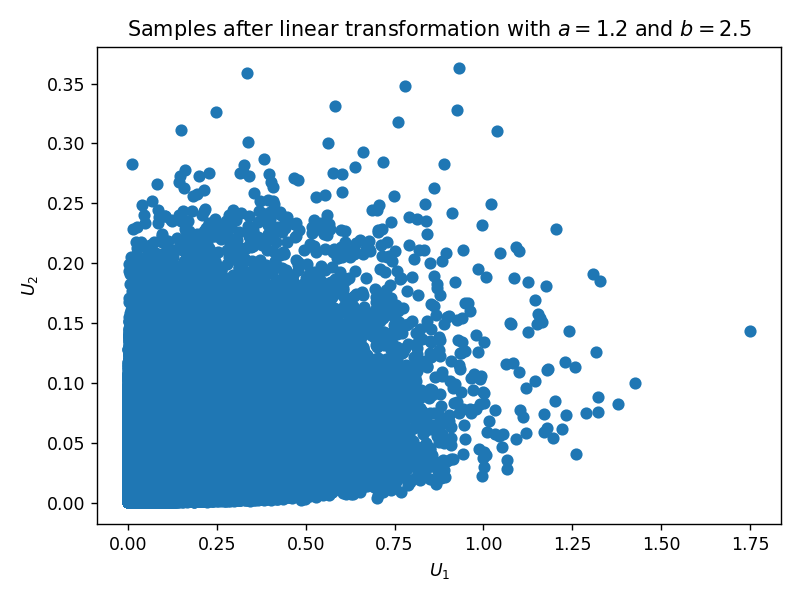

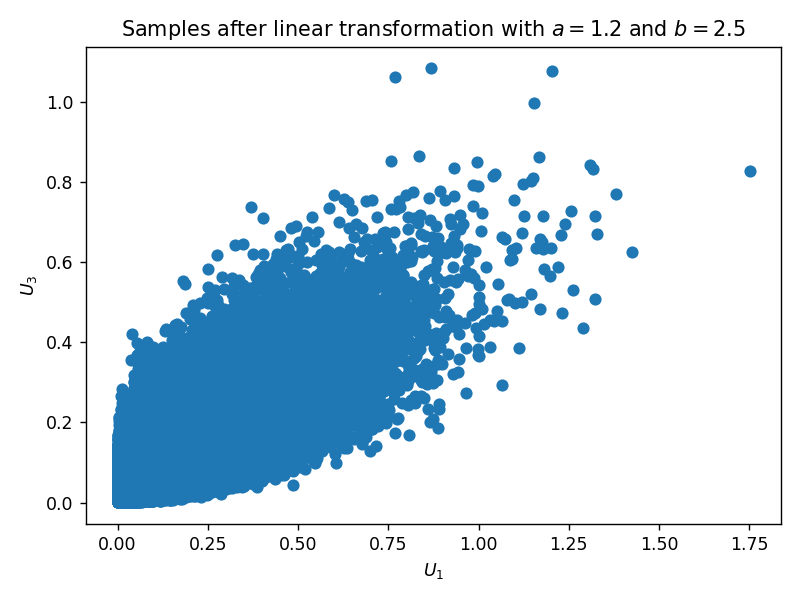

Figure 2: Visualization of the sample paths of the original multifactor process V2 (right) and of the process after applying the explicit Q transformation yielding an orthant (left), with black lines denoting the boundary hyperplanes.

The explicit invertibility and structure of Q guarantee that scheme and domain construction is feasible in any dimension (see also the N=3 extension and admissibility discussion).

Theoretical Implications

The construction of D as a linear (or in some cases affine) image of the nonnegative orthant links the support of the Markovian process to classical positivity requirements for affine SDEs with degenerate diffusions. The viability and invariance are certified by mapping the process to new coordinates where standard viability criteria for the orthant hold: at the boundary, the diffusion is tangential and the drift is inward-pointing.

A significant theoretical consequence is that this result subsumes and renders explicit previously only abstractly characterized domains, such as those involving resolvents of Volterra kernels [cf. "Markovian Representations of Fractional Processes and Affine Volterra Processes," Abi Jaber et al.]—the present result is notable for giving a constructive and dimensionally tractable description.

Consequences for Numerical Algorithms

Simulation Scheme Well-definedness

Accurate simulation schemes for multifactor square-root processes require that every step remains strictly inside D. The domain characterized here ensures that, at each time increment, simulation updates (including splitting and higher-order schemes) cannot produce states leading to undefined radicals or instability in the SDE integrators. The authors demonstrate this with the weak simulation scheme from [Bayer et al., 2023], showing that the transformation ensures nonnegativity (and thus well-definedness) globally.

PDE Methods on the Correct Domain

The precise identification of the domain allows the correct setup of parabolic PDEs for pricing contingent claims when the state variables are the components of Yt. Instead of ad hoc or infeasible rejection-based meshing, the method enables solving, e.g., Kolmogorov backward equations, by transforming to an orthant where standard techniques (finite elements, Dirichlet/Neumann boundary conditions) apply, and then reverting to the physical variables.

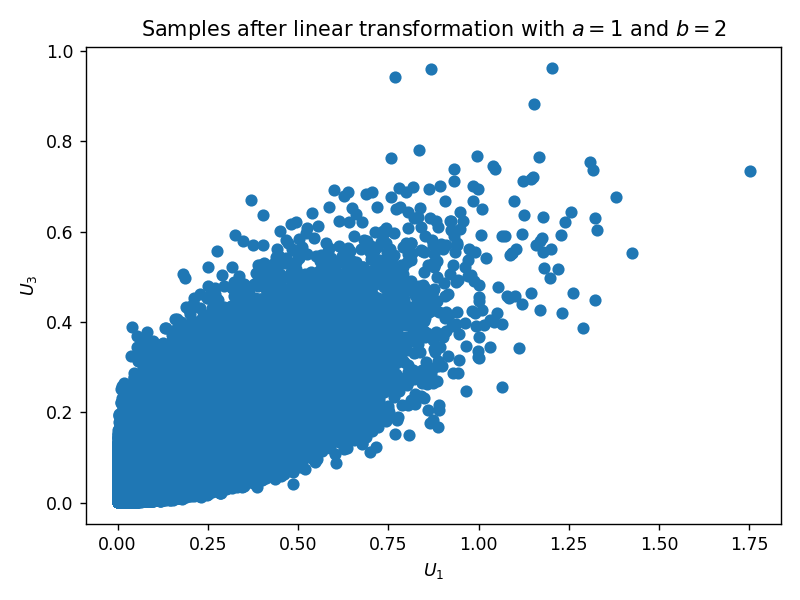

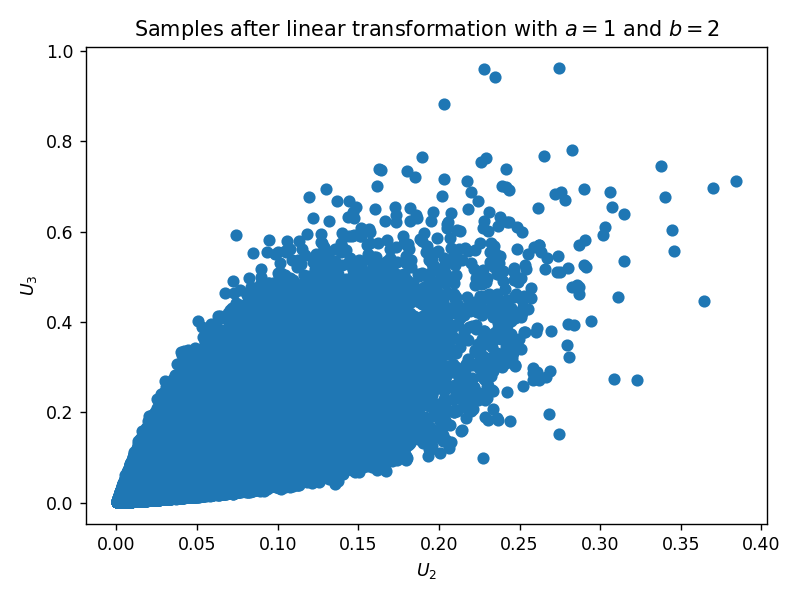

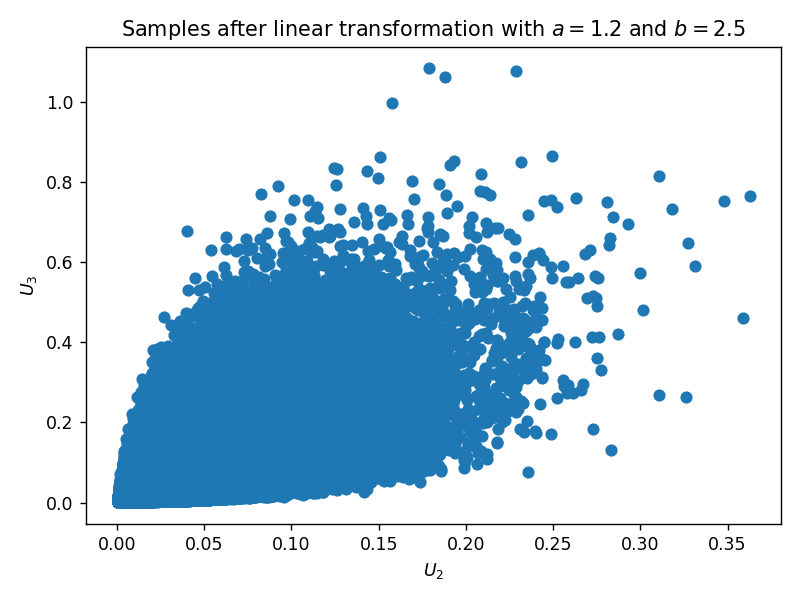

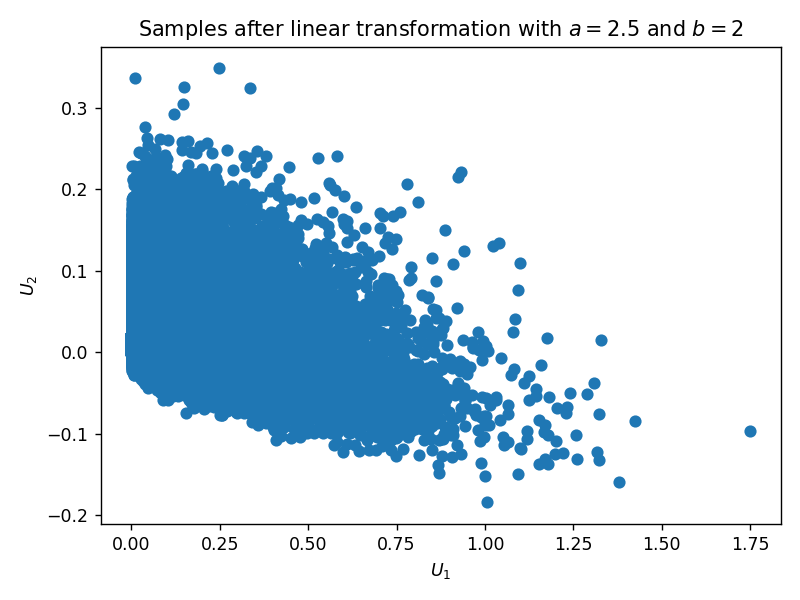

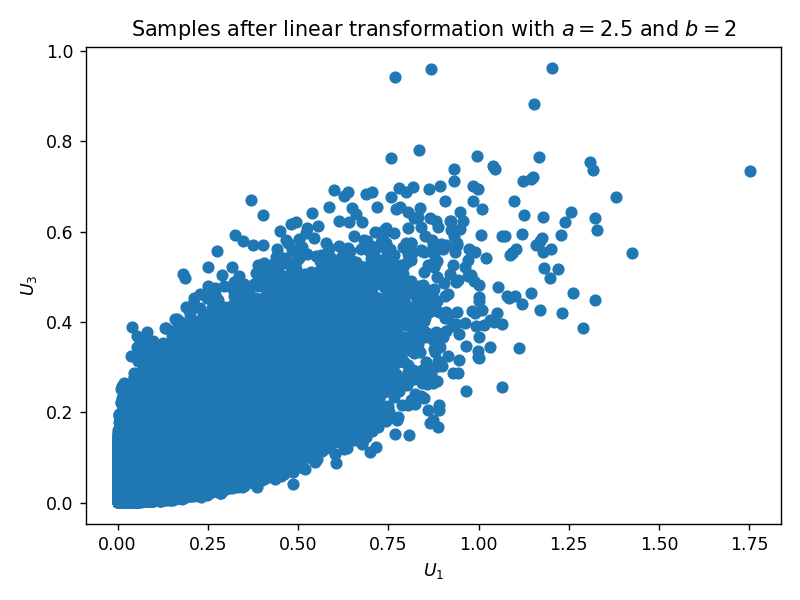

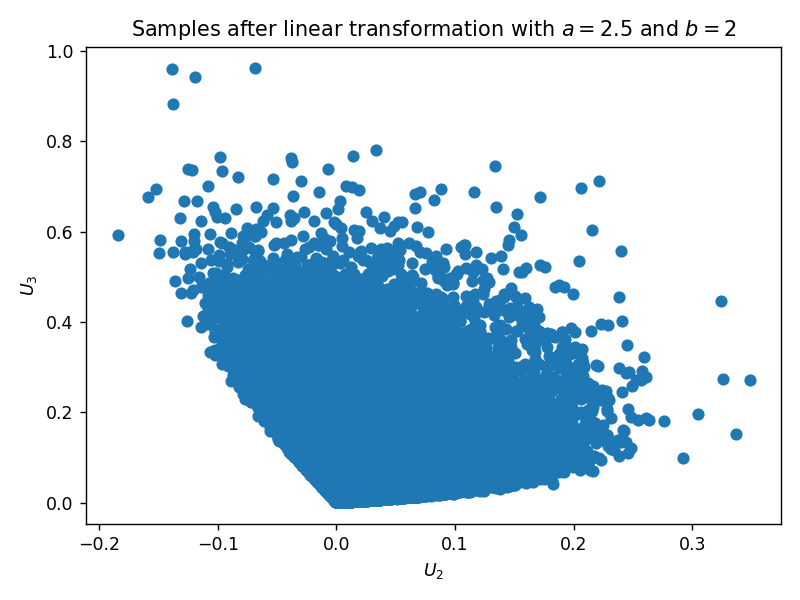

Figure 3: Projections of simulated samples of the transformed state vector U for N=3, demonstrating tight adherence to the positive orthant in all lower-dimensional subspaces, confirming correct domain characterization.

The paper provides explicit error reductions when the domain is chosen as prescribed, with significant error explosion when the domain is even slightly misspecified, demonstrating the practical necessity of the explicit state space in PDE numerics.

Broader Implications and Future Directions

- Calibration and Model Fitting: The ability to enforce or calibrate initial conditions Y0 to market fits is greatly improved when the exact state space is tractable.

- High-dimensional Applications: The method scales naturally with N due to the explicit matrix structure, enabling multifactor approximations of rough volatility with many exponentials.

- Connections to M-matrix Theory: The admissible transformations Q draw connections between stochastic viability and classical results in linear algebra, opening routes to further structural results and possibly more refined spectral analysis of Markovianized Volterra equations.

- Extensions to Nonlinear Volterra and Non-exponential Kernels: The explicit tractability found here for exponential-indexed kernels suggests a path for more general kernel approximation architectures.

Conclusion

The paper provides a rigorous, explicit, and scalable characterization of the viable state space for multifactor Markovian approximations of nonnegative Volterra processes by unveiling a correspondence to linear transforms of the nonnegative orthant. This result precisely pins down the geometry required for both theoretical pathwise positivity and practical spectral and finite difference/finite element numerical algorithms. The domain characterization directly enables provably correct and efficient simulation and PDE solution schemes in stochastic modeling of rough volatility and related areas.

For researchers working in stochastic analysis, mathematical finance, or numerical methods for SDEs with memory, this work provides an indispensable methodological tool for constructing and analyzing Markovian representations of nonnegative Volterra-type processes.