- The paper demonstrates that order splitting and liquidity replenishment are jointly necessary to generate the square-root law of market impact.

- The agent-based model replicates key market microstructure stylized facts, revealing that disrupting either mechanism significantly alters the impact exponent.

- Controlled ablation experiments falsify single-mechanism theories, emphasizing that both splitting metaorders and rapid LOB liquidity recovery maintain realistic impact scaling.

Order Splitting and Liquidity Replenishment as Jointly Necessary Mechanisms for the Square-Root Law of Market Impact

Introduction

The square-root law (SRL) of market impact, stating that the normalized price impact I/σD of a metaorder scales as (Q/VD)δ with δ≈0.5, is an empirical regularity in equity markets. Despite extensive theoretical and empirical investigations, the mechanistic origins of this concave relationship remain unsettled. The study "Order Splitting and Liquidity Replenishment Are Jointly Necessary for the Square-Root Law of Market Impact: A Counterfactual Dissection" (2607.04280) systematically explores the causal mechanisms underlying the SRL using a minimal limit order book (LOB) agent-based model (ABM). It critically evaluates established theoretical frameworks and employs controlled counterfactual scenarios to identify which market microstructure features are necessary and sufficient for the emergence of the square-root impact scaling.

Model Design and Stylized Facts

The authors construct a continuous double auction LOB populated by four heterogeneous agent types: institutional (generating and splitting metaorders), high-frequency trading (HFT) market-makers (liquidity providers), retail agents (noise/background turnover), and news agents (exogenous volatility). The model operates without learning or adaptive intelligence—agents follow fixed behavioral protocols.

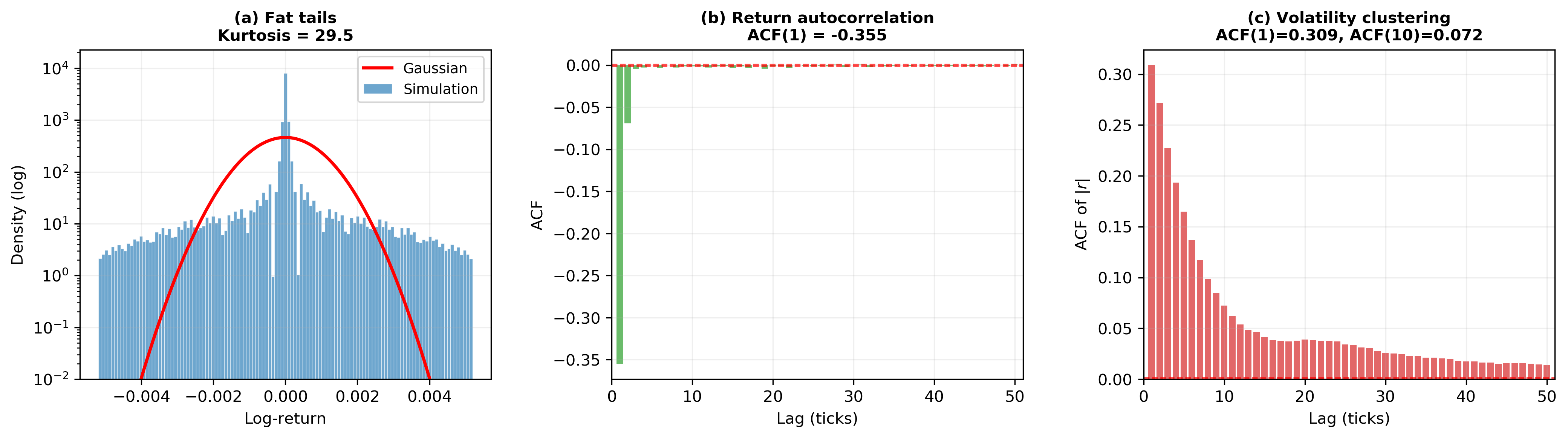

The simulation encompasses 2,000 stocks, each parameterized with heterogeneity in initial price, agent populations, and Pareto exponents of institutional metaorder size. Over 106 steps per stock, the dynamics generate price and return time series replicating canonical stylized facts of equity markets: random-walk-like prices, fat-tailed log-returns (κ=29.5 for one representative stock), bid–ask bounce (lag-1 return autocorrelation of -0.355), and volatility clustering.

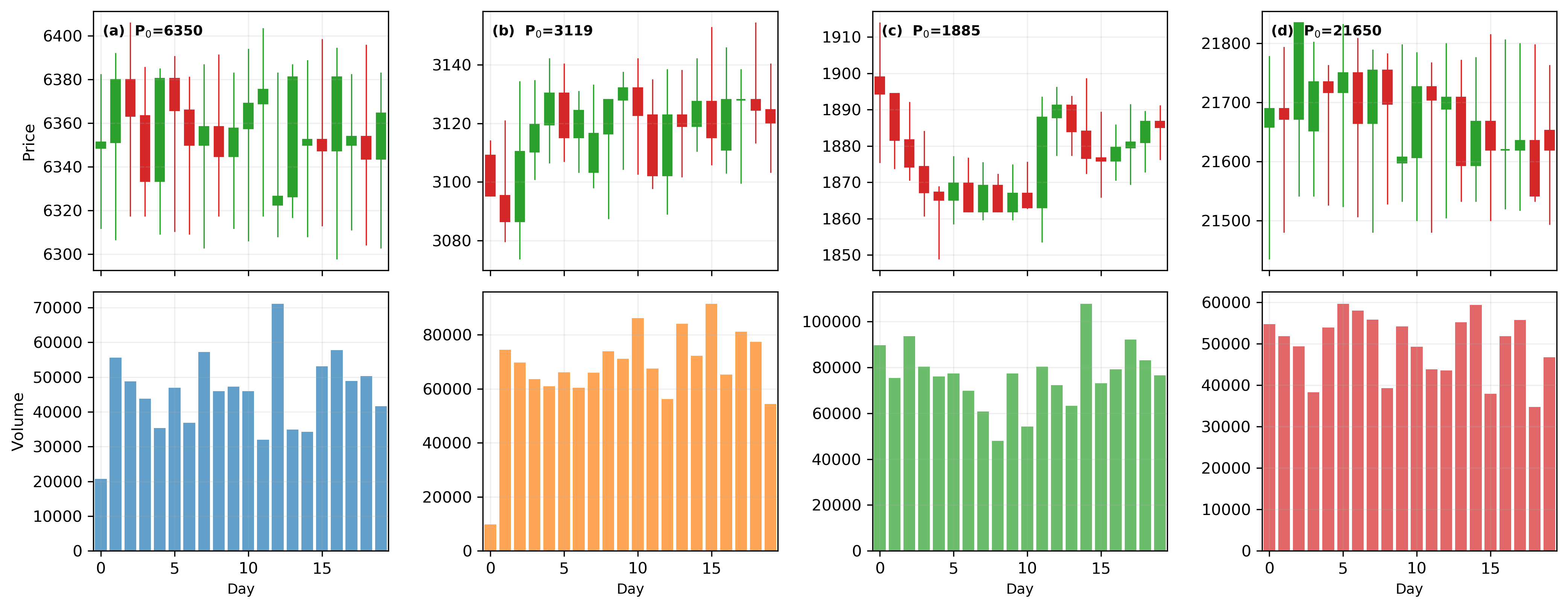

Figure 1: Daily candlestick charts and volume bars for representative stocks exhibit realistic volatility regimes and price paths.

Figure 2: Diagnostic plots confirm excess kurtosis in returns and negative first-lag autocorrelation, reproducing key market microstructure signatures.

Empirical Verification of the Square-Root Law

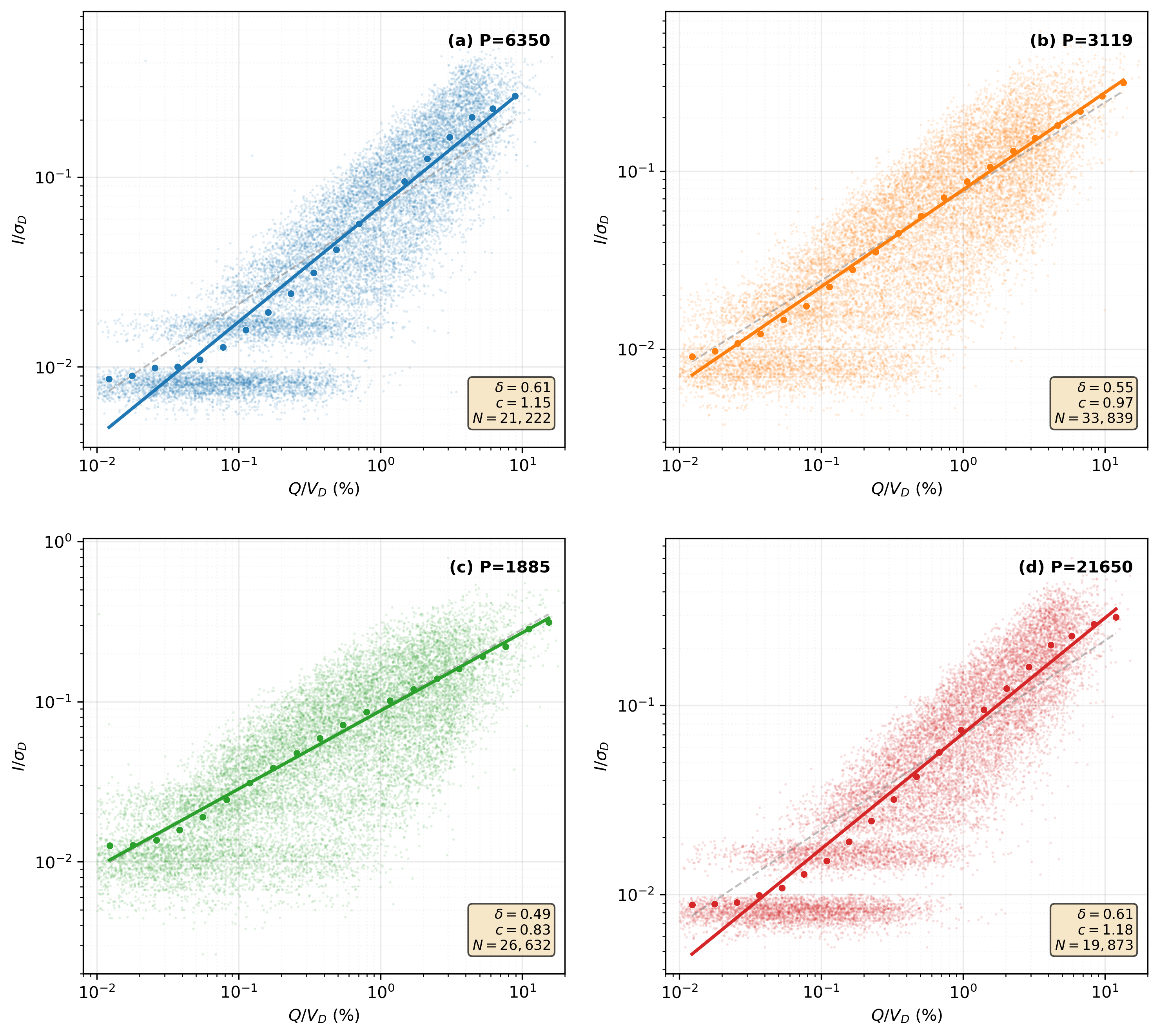

The model robustly produces concave impact curves at the stock level, with δ values clustering tightly around 0.54 (⟨δ⟩=0.539±0.048), closely matching the Tokyo Stock Exchange empirical mean (⟨δ⟩=0.489).

Figure 3: Per-stock impact curves across heterogeneous stocks confirm the square-root law with exponents near $1/2$.

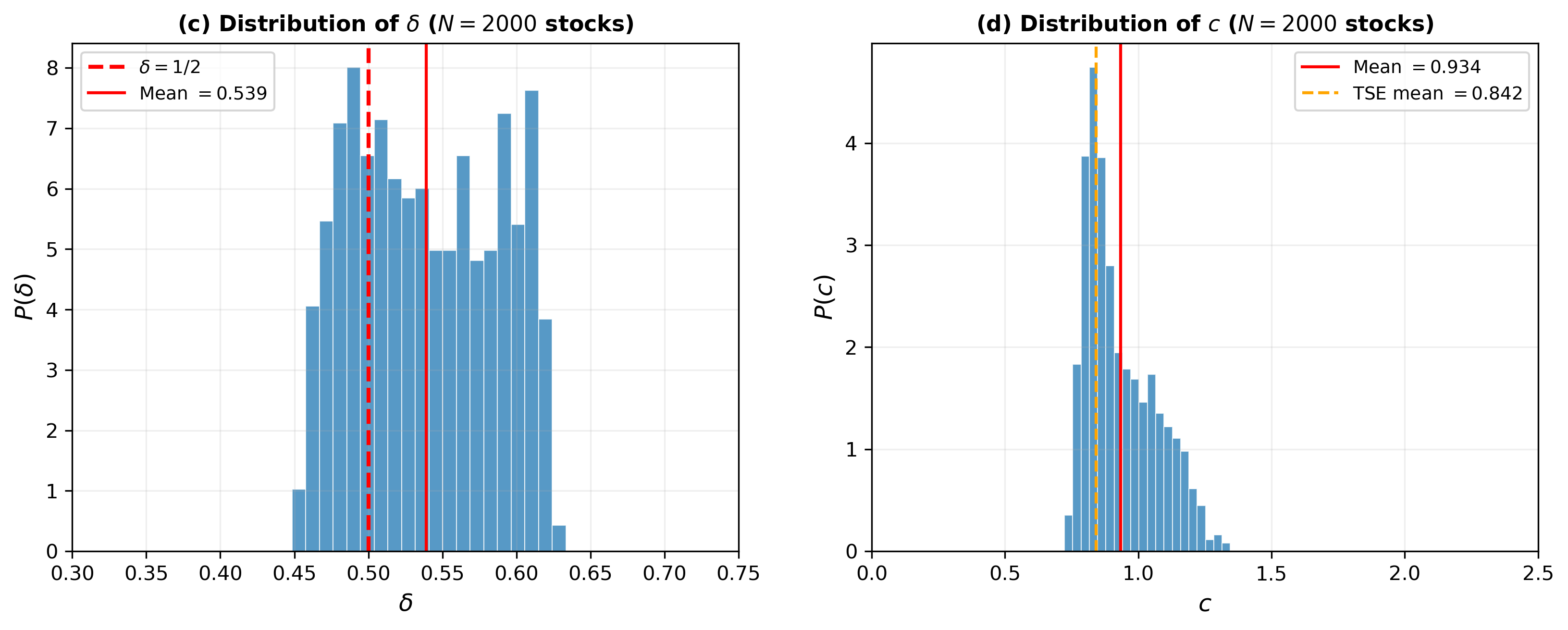

Pooling across all simulations yields (δ,c)=(0.549,0.982). The distribution of (Q/VD)δ0 is narrow, indicating that the SRL is robust to microstructure variation in the model.

Figure 4: Histogram of fitted (Q/VD)δ1 and (Q/VD)δ2 across 2,000 simulated stocks; (Q/VD)δ3 is symmetric and centered on 0.54.

Stress Testing Theoretical Explanations

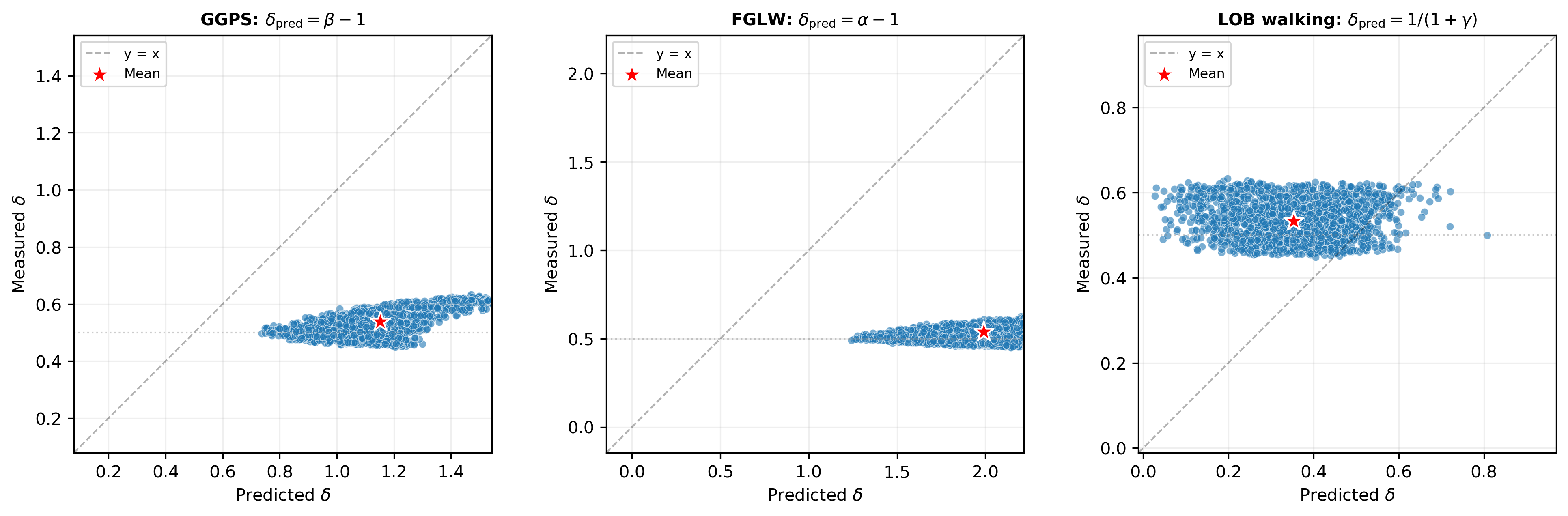

The study provides a direct computational stress test for three standard theoretical predictions of (Q/VD)δ4:

- GGPS ((Q/VD)δ5): Relates impact exponent to the Pareto tail of metaorder size.

- FGLW ((Q/VD)δ6): Connects (Q/VD)δ7 to the fat tail in the child-order count per metaorder.

- LOB walking ((Q/VD)δ8): Derives (Q/VD)δ9 from the cumulative depth exponent of the static LOB.

Empirically measured exponents for 2,000 stocks reveal that GGPS and FGLW both over-predict δ≈0.50 (values often exceeding one), while the LOB walking model under-predicts (typically δ≈0.51), with none matching simulated δ≈0.52 on the same data.

Figure 5: Predicted vs. measured impact exponents—a clear systematic mismatch for all mechanistic single-factor theories tested.

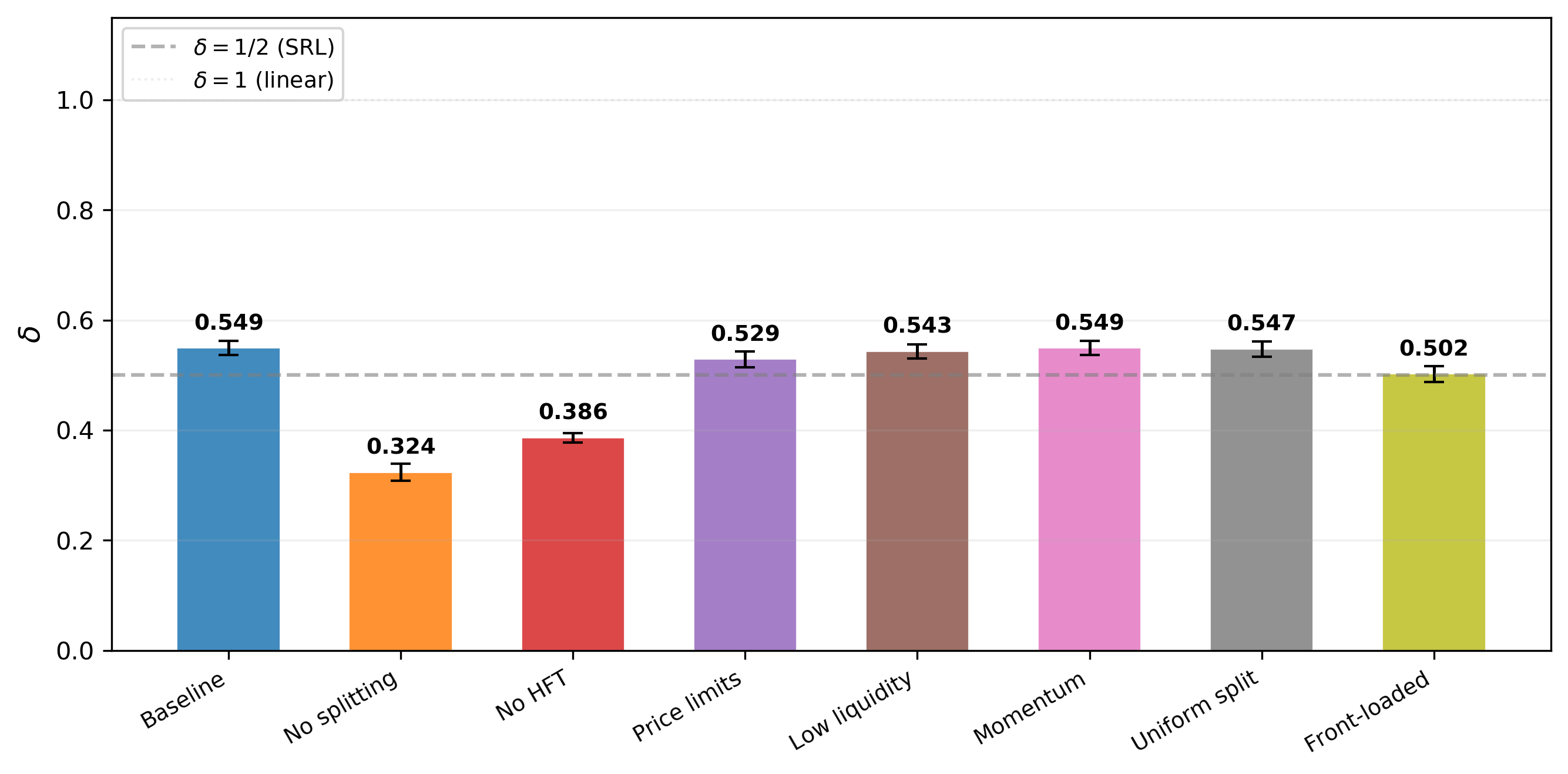

Counterfactual Ablation and Causal Identification

The central methodological innovation is controlled ablation: the authors suppress one microstructural feature at a time and measure the effect on δ≈0.53. The most salient ablations are:

- No Order Splitting: Collapses δ≈0.54 from 0.549 to 0.324.

- No HFT Liquidity Replenishment: δ≈0.55 drops to 0.386.

- Other Perturbations (e.g., price limits, momentum, uniform splitting rule, lower liquidity): δ≈0.56 remains within 10% of baseline, between 0.49 and 0.53.

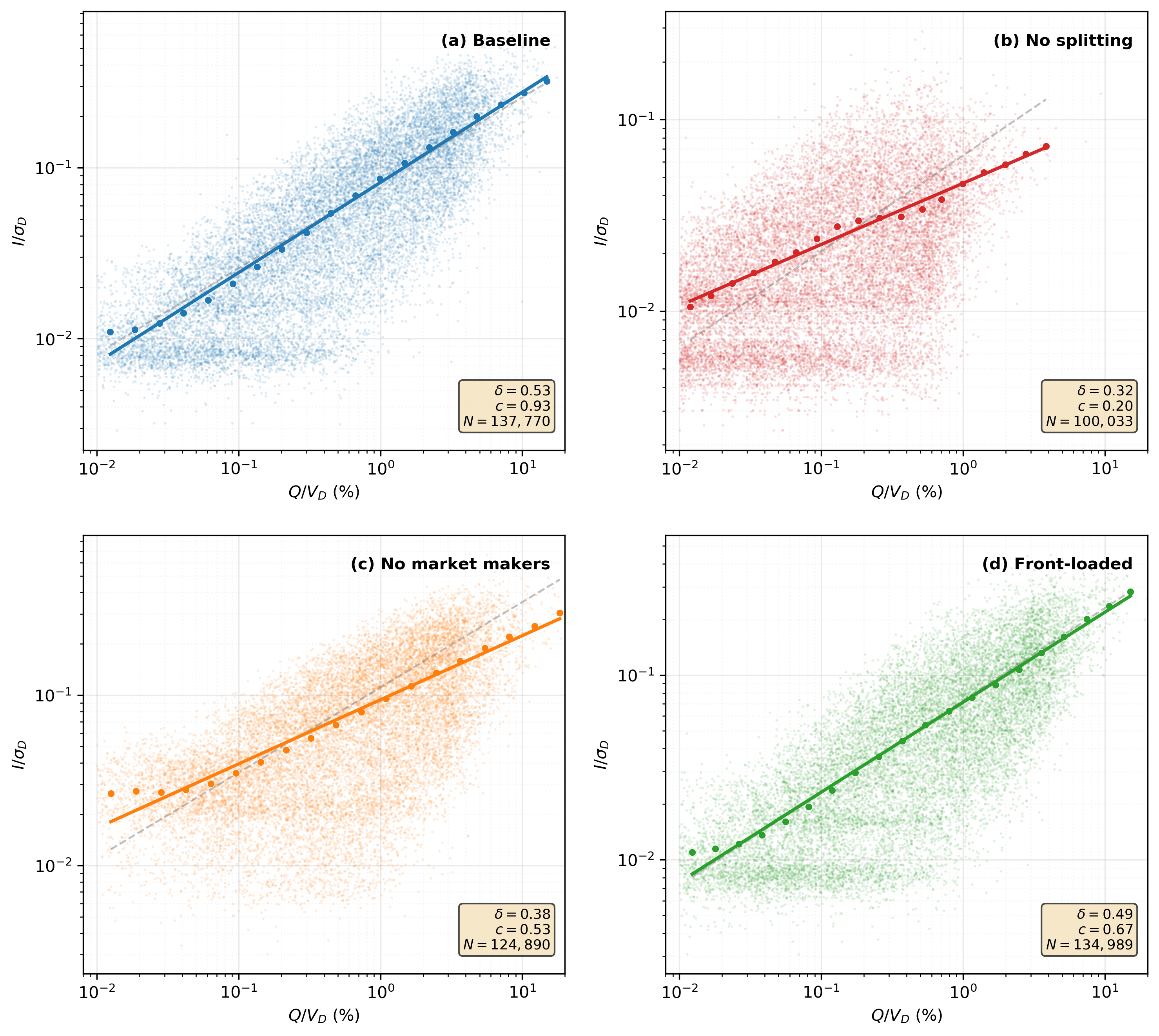

The flattening of the impact curve when splitting is suppressed and the increased steepness when liquidity replenishment is disabled are evident in scenario-specific impact curves.

Figure 6: Impact curves for baseline, no-splitting, no-HFT, and front-loaded splitting scenarios.

Figure 7: Summary of fitted δ≈0.57 for all counterfactual scenarios, highlighting collapse only when splitting or liquidity replenishment is removed.

These results establish that both order splitting and rapid LOB liquidity replenishment are jointly necessary for the square-root law in this ABM framework—a claim that directly contradicts theoretical models postulating that SRL arises from a single distributional or geometric feature.

Mechanistic Interpretation

The model shows that splitting a large metaorder into smaller slices, executed over time, allows the LOB to recover via market-maker replenishment after each child order. The cumulative impact thus reflects the sum of many minor displacements, each partially counteracted by new liquidity. Without order splitting, large unsplit market orders traverse the book in a single pass, encountering superlinear depth growth and leading to much more concave, sublinear impact. Eliminating liquidity replenishment by HFTs thins the book, causing each slice to produce disproportionately higher incremental impact—even with order splitting intact.

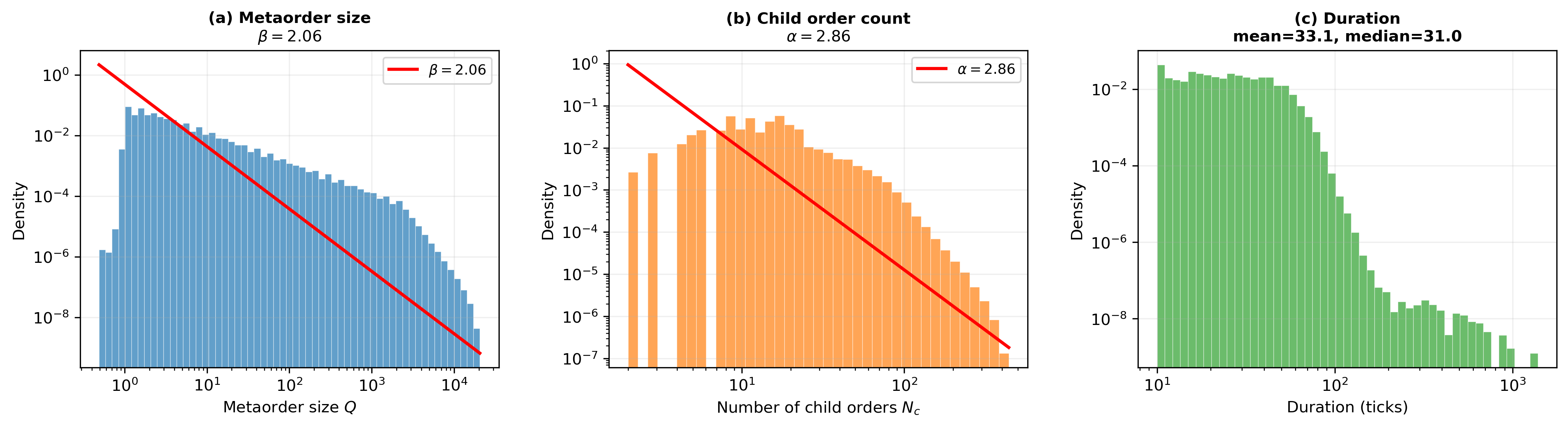

Metaorder and execution statistics further confirm that neither the metaorder size distribution (δ≈0.58) nor the child count (δ≈0.59) or LOB depth exponent (1060) alone are predictive of the observed 1061 in simulation.

Figure 8: Empirical distributions for metaorder size and child order count confirm heavy tails, but these are not causally predictive for 1062.

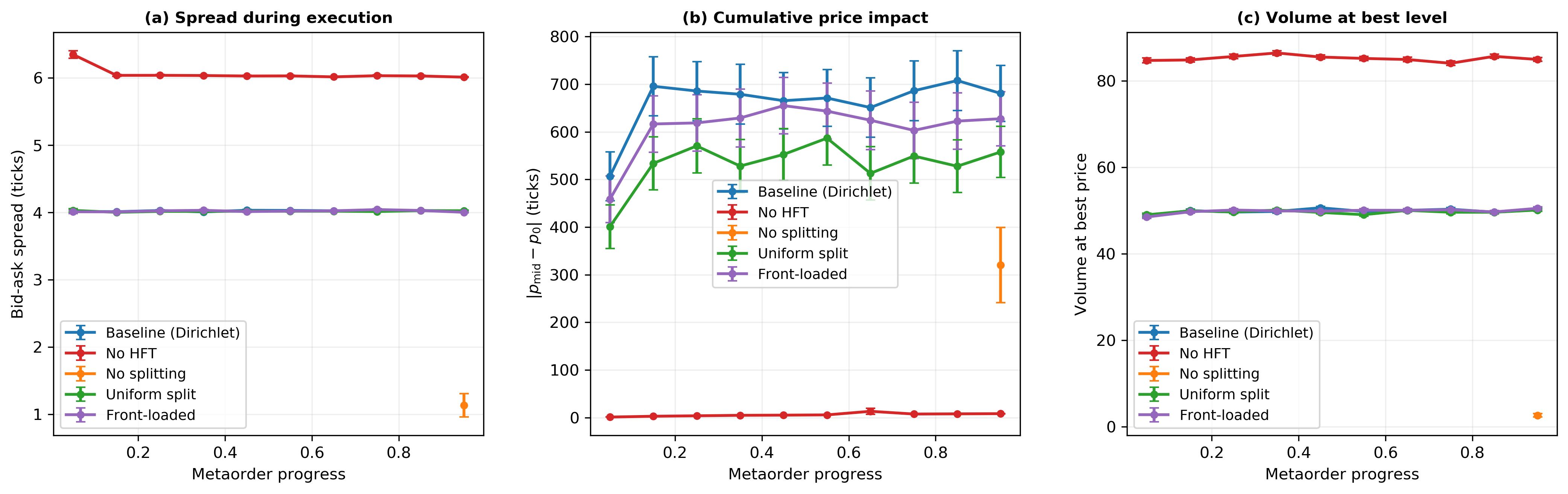

LOB evolution analysis shows how the book is replenished during metaorder execution in the baseline and how the lack of splitting or HFT causes dramatically different LOB states and price trajectories.

Figure 9: Evolution of bid-ask spread, cumulative impact, and best-price volume during execution under varied scenarios illustrates the mechanisms driving SRL.

Theoretical and Practical Implications

The results convincingly falsify distributional (GGPS, FGLW) and static LOB-based (LOB walking) explanations for the SRL within the boundaries of their ABM. The empirical reproduction of SRL is exclusively robust to order splitting and LOB replenishment. The latent liquidity framework, in which hidden depth is revealed gradually over the course of execution, is consistent with these findings, but this study advances the literature by performing agent-level causal ablation.

The methodology represents a pathway to isolating necessary and sufficient conditions for other empirical laws in market microstructure. In real markets, these findings suggest that regulatory or technological interventions that alter splitting practices or impede rapid liquidity recovery could fundamentally change the observed price impact scaling. While the ABM omits strategic adaptation, cross-asset effects, and more sophisticated order flow dynamics, its clarity in mechanism isolation provides foundational insight for future empirical and modeling studies.

Conclusion

This work provides robust computational evidence that the coexistence of order splitting and liquidity replenishment by market makers is jointly necessary for the square-root law of market impact within a large-scale ABM. Neither the metaorder size distribution, the distribution of order counts, nor the static geometry of the LOB alone suffices to explain concave market impact. The implications extend both theoretically—in critiquing widely-used single-mechanism models—and practically—in highlighting which market design and trading practices are essential to maintain observed impact regularities. This framework offers a rigorous template for mechanistic identification in agent-based models of market microstructure.