- The paper introduces a dynamic equilibrium model of limit order books using Student‑t noise to capture rare, large liquidity events.

- It demonstrates that heavy‑tailed liquidity shocks slow information aggregation, resulting in persistent bid‑ask spreads and flatter price impact curves.

- The study employs tail‑controlled existence proofs and Bayesian learning to explain state‑dependent price discovery under liquidity risk.

Liquidity Tail Risk, Market Impact, and Slowed Price Discovery in Limit Order Books

Overview and Core Model Innovations

This work presents a dynamic, equilibrium model of competitive limit order books (LOBs) in the presence of heavy-tailed, noise-driven liquidity demand, with asymmetric information. The authors extend standard LOB frameworks by specifying the aggregate, uninformed order flow as Student-t distributed with degrees of freedom parameter ν>2. This modeling choice systematically captures rare, large liquidity shocks with higher and tunable probability mass in the tails, thereby shifting the structural informational content of large trades.

Crucially, liquidity suppliers only observe aggregate order flow—not its decomposition into informed and noise demand. The statistical ambiguity arising from heavy-tailed noise means that even large trades cannot a priori be attributed to informed trading. This changes both the inference problems faced by liquidity suppliers and the mathematical properties of the equilibrium problem itself.

Mathematical Structure and Main Results

The model operates in discrete time with T periods and supports both finite and infinite horizons. In every period, risk-neutral, myopic informed traders (with number Nt) and noise traders submit marketable orders; liquidity suppliers post competitive limit orders. The fundamental value V is drawn once and revealed only at the end (if T<∞), while each period's noise demand Zt is drawn i.i.d. from a Tν(0,σ) distribution.

The limit-order book is priced via a "tail expectation": for buy (resp. sell) depth y>0 (y<0), the marginal price ν>20 is set to the conditional expectation of the fundamental value given the aggregate order flow exceeding (resp. falling below) ν>21. Informed demand is determined by a first-order condition linking the insider’s marginal value to the marginal execution cost, generating a fixed-point equation for the marginal-cost schedule ν>22.

Failure of Standard Monotonicity and Continuity

The introduction of Student-ν>23 noise fundamentally alters technical properties familiar from Gaussian equilibrium microstructure models. In the Gaussian case, monotonicity of the pricing operator and compactness of the candidate schedule class underpin existence theorems via standard fixed-point arguments. Here, however, the heavy tails of the Student-ν>24 distribution keep remote liquidity states pricing-relevant at polynomial (rather than exponential) order. The pricing operator is no longer globally monotone-preserving, nor continuous on broad classes of candidate schedules.

Existence and Tail-Controlled Construction

To overcome these issues, the authors construct existence results on a tail-controlled compact class, leveraging regular-variation properties. Under bounded support of ν>25, they establish (Theorem 1) fixed-point existence via conditions on the endpoint behavior of the posterior belief and the associated tail exponents. The selected branch exponents arise from a mixture of model primitives: the tail index ν>26 of noise trading, the number of insiders ν>27, and the posterior tail thickness of beliefs (equivalently, information aggregation progress).

Belief updating by liquidity suppliers proceeds through Bayes’ rule but treats order-flow outliers as possibly noise-driven—naturally slowing the rate at which posterior mass concentrates on the true fundamental. Using tools from Bayesian learning with dependent data, the authors demonstrate (Theorem 2) almost sure posterior consistency of liquidity suppliers’ beliefs, conditional on a compact parameter set and regularity of the inverse demand schedule.

Nevertheless, finite-horizon learning, spread compression, and adverse-selection premium decay all proceed more slowly under heavier liquidity tails. Empirically, this predicts a persistent residual bid-ask spread and market impact deep into the trading horizon under anomalous liquidity regimes.

Asymptotic Price Impact: Power Laws and Crossover Behavior

A central technical result is the characterization of large-order price impact. Asymptotically (with order size ν>28), the marginal cost schedule satisfies:

ν>29

with explicit exponent:

T0

(for suitable definitions of the tail expectations)—demonstrating regular variation of the impact curve at depth. The exponent is strictly controlled by the tail index T1 and the branch of learning realized, and does not reduce to the Gaussian case even as competition among insiders increases. Heavy-tailed noise trading permanently flattens the impact curve at depth.

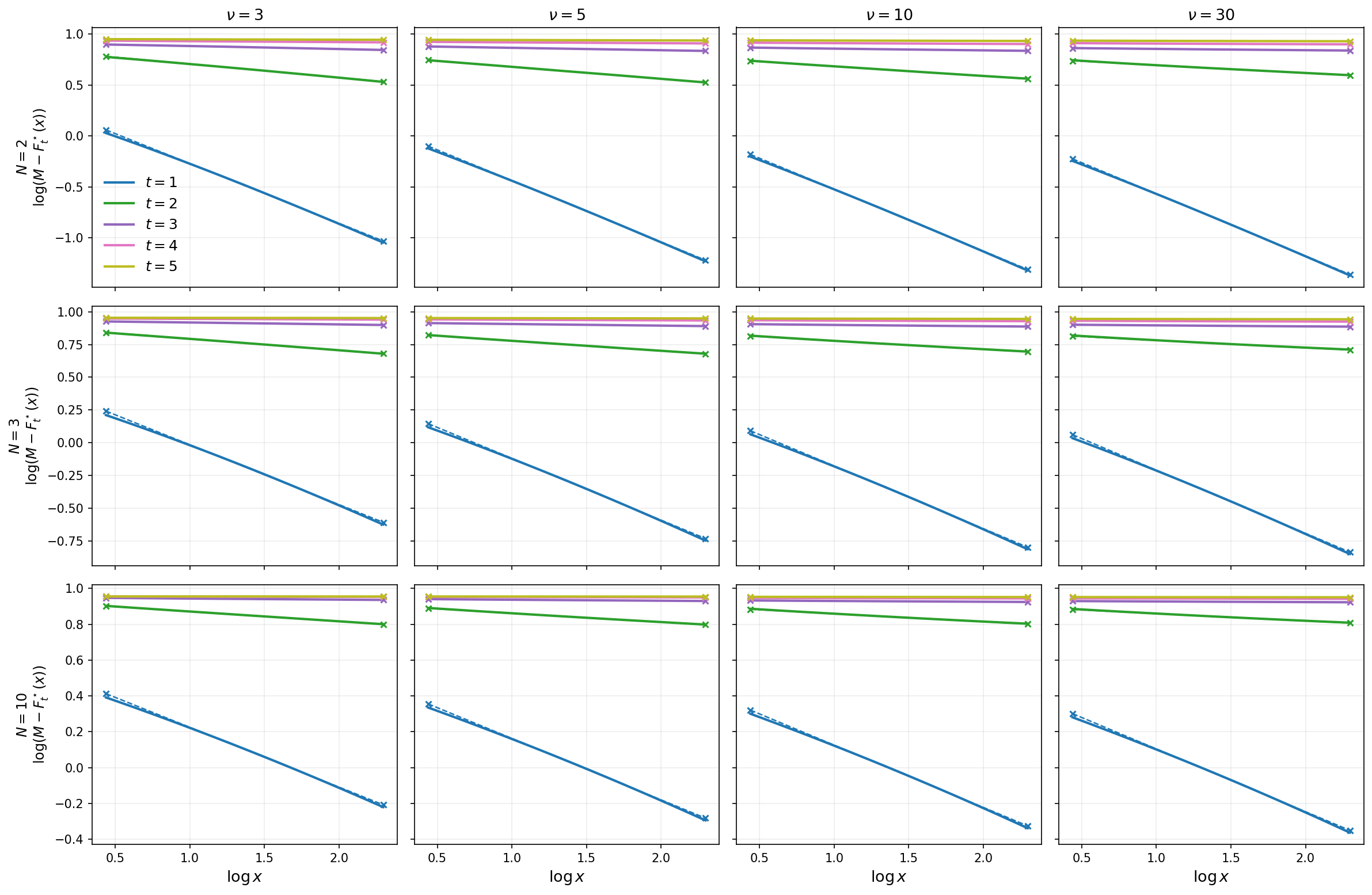

Figure 1: Log-log plot of logT2 against logT3 for the truncated Gaussian prior, showing power law scaling in price impact.

A corresponding result holds for aggregate order flow and informed demand distributions, with both aggregate quantities and cross-sectional sizes inheriting the tail structure from noise trading, only reverting to the posterior’s tail in ultradeep execution (i.e., the far tail is eventually dominated by informed demand).

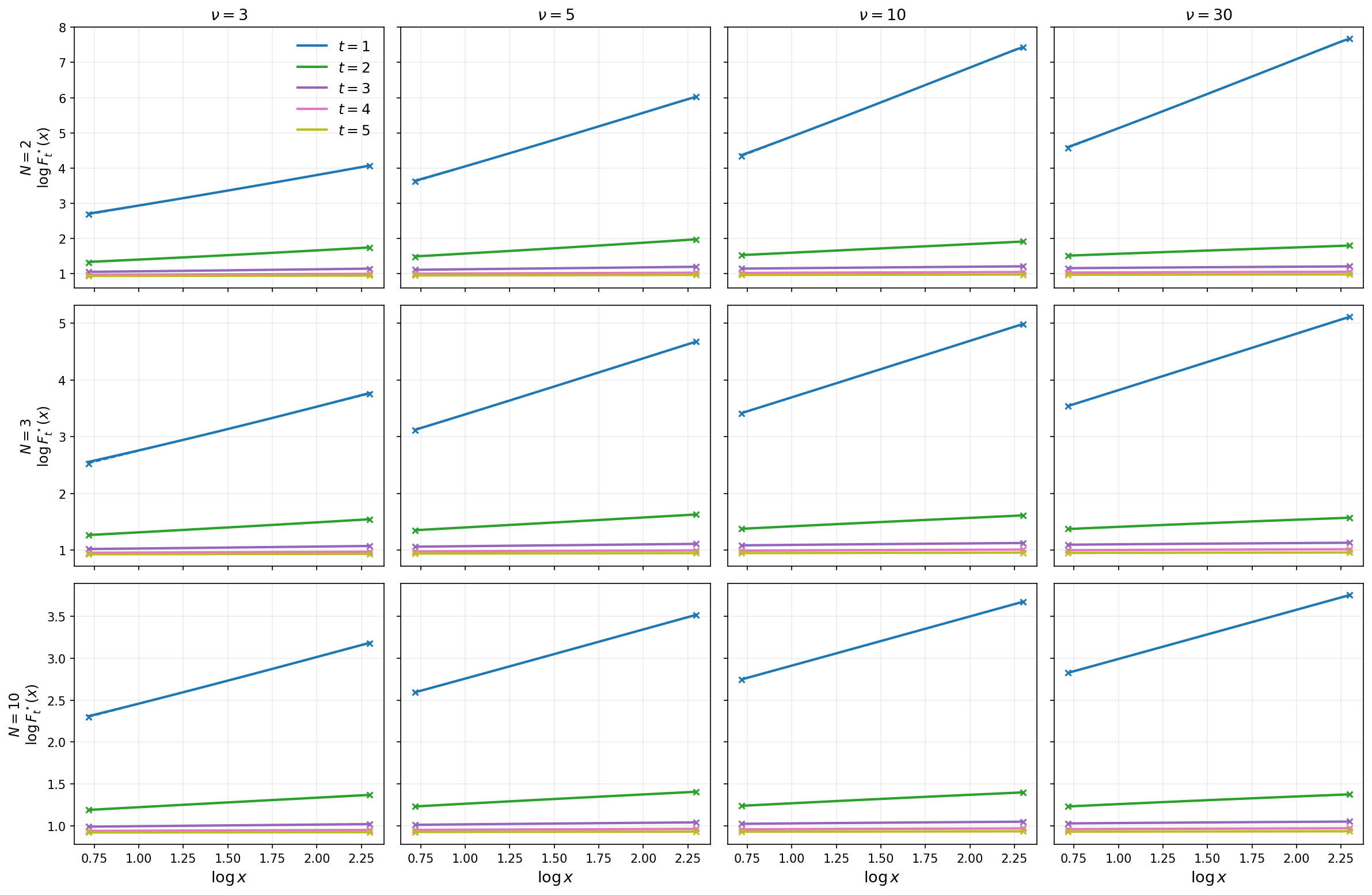

Figure 2: Log-log plot of logT4 against logT5 for the Pareto prior, highlighting the interplay of tail exponents in price impact for different noise regimes.

Numerical Results: Monotonicity, Uniqueness, and Empirical Diagnostics

Systematic numerical experiments across a range of prior distributions (uniform, beta, truncated Gaussian, Pareto) and insider counts (T6) confirm:

Secondary diagnostics include empirical convergence of posterior mean and variance, spread decay, and comparative statics in Nt1, all in tightly consistent qualitative alignment with the analytic theory.

Figure 4: Posterior mean and standard deviation convergence, confirming Bayesian learning for all prior/noise settings.

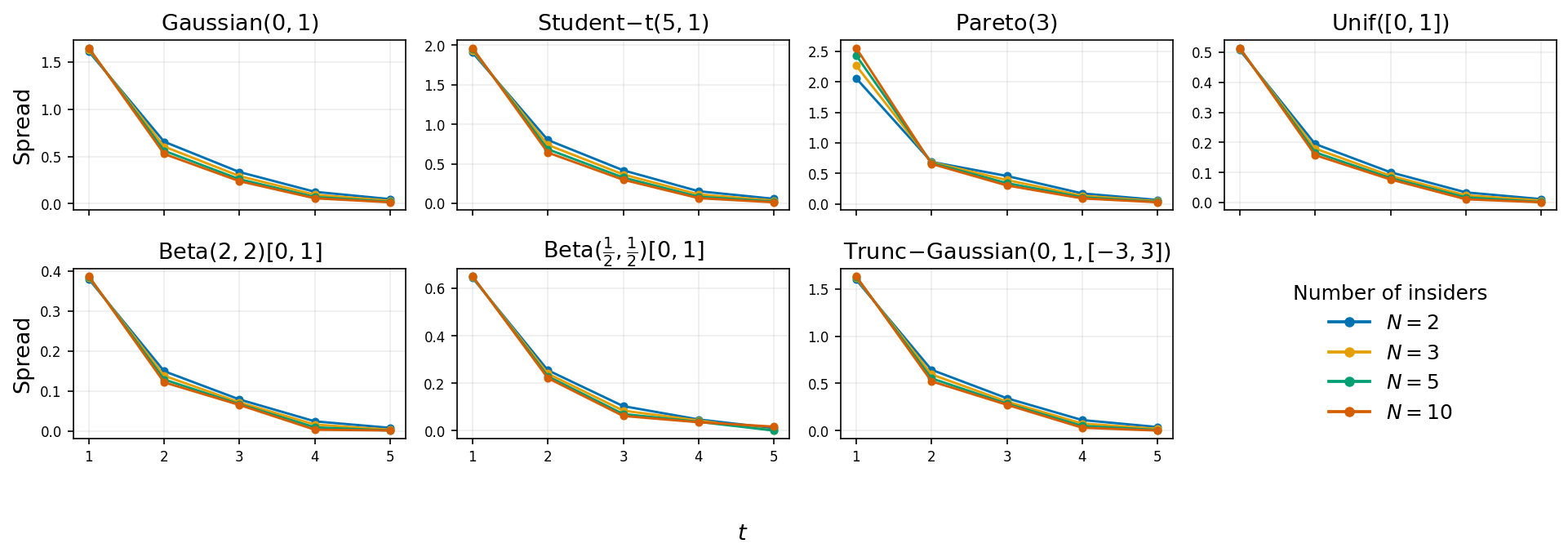

Figure 5: Bid-ask spread evolution Nt2, illustrating slowed spread compression for low Nt3.

Theoretical and Practical Implications

Pricing and Inference: State-Dependent Information Content

The key implication is that large trades are not always news: their informativeness is a state variable, determined by the tail thickness of liquidity demand. Heavier-tailed regimes obscure the distinction between informed and liquidity-driven trades, flatten price impact, and elongate the range of ambiguous order flow. This fundamentally changes trade-surveillance heuristics and time scales in which market makers manage adverse selection risk.

Market Impact and Robustness of Power-Law Tails

The results provide an equilibrium microstructure mechanism connecting empirically observed market impact nonlinearities and power-law tails in trading volume with endogenous learning. They indicate that liquidity tail risk sets lower bounds on impact concavity and slows information aggregation, regardless of competition among insiders.

Directions for Extensions

Empirical calibration of the model via tail index estimation and its deployment in market quality diagnostics are immediate practical directions. Theoretically, the separation of fixed-point existence and monotonicity in the Student-Nt4 regime invites further analysis—whether the observed global monotonicity is generic or contingent. Additional features such as liquidity provision frictions, multi-asset extensions, and endogenous order splitting can now be rigorously grounded in a framework where liquidity tail risk is a first-order structural parameter.

Conclusion

This paper advances the theoretical underpinnings of market microstructure under heavy-tailed noise by rigorously characterizing the equilibrium, learning, and price impact properties in limit order books where rare liquidity events remain economically meaningful through polynomial tail decay. Liquidity tail risk is elevated from a residual feature to a state variable fundamentally determining the informativeness of order flow, resilience of the spread, and the asymptotics of market impact, with persistent consequences for both equilibrium learning and high-frequency trading behavior. The mathematical innovations in the existence theory under heavy tails are substantial and set a template for further work on tail-sensitive equilibrium dynamics.

Key Figures Referenced:

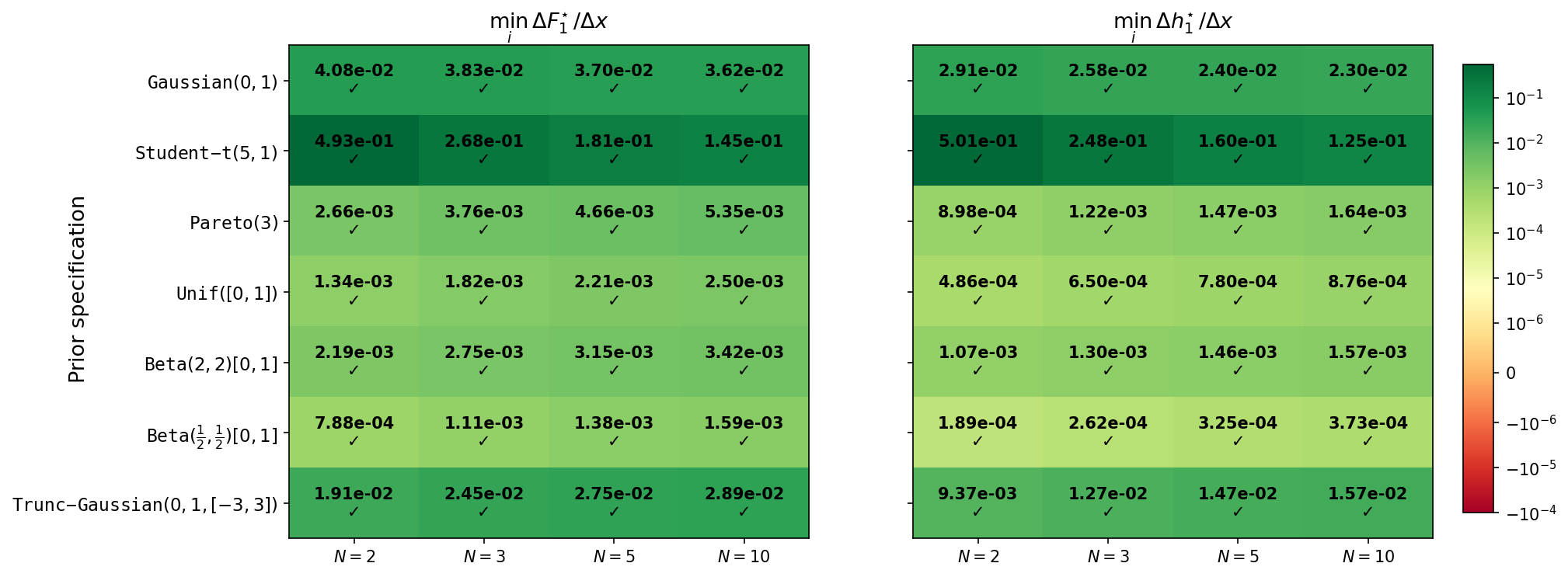

Figure 3: Minimum finite-difference slope of the Nt5 (Left panel) and Nt6 (Right panel), across seven prior distributions and four choices for the number of insider traders.

*Figure 5: Bid-ask spread

Nt7 across trading periods

Nt8, for the considered seven prior distributions and

Nt9. *

*Figure 1: Log-log plot of log

V0 against log

V1 for the

V2. *

*Figure 2: Log-log plot of log

V3 against log

V4 for the

V5. *

*Figure 4: Posterior mean and standard deviation across trading periods under constant signal noise. Each column corresponds to a different value of

V6. The solid line denotes the posterior mean averaged across runs, and the shaded region represents one standard deviation. The dashed line indicates the true value

V7. *

References