- The paper finds that prediction market prices consistently exceed Binance-implied risk-neutral benchmarks by about 5–6 percentage points.

- The methodology uses hourly-aligned time series and Black–Scholes inversion to isolate genuine cross-market pricing discrepancies with a mean-reverting AR(1) half-life of roughly 4 hours.

- The arbitrage analysis, including tests on Deribit and Ethereum, highlights digital market frictions, segmented capital mobility, and potential exploitability of observed pricing gaps.

Cross-Venue Pricing Divergence in Digital Markets: Binance Options Versus Polymarket Prediction Contracts

Empirical Framework and Data Alignment

This paper rigorously examines whether centralized crypto-option exchanges and blockchain-based prediction markets price identical binary payoffs equivalently, focusing on Bitcoin threshold contracts. The methodology is predicated on a direct contract mapping: each Polymarket Yes share, denoting a positive outcome for Bitcoin exceeding a fixed threshold, is matched hour-by-hour against a Binance vanilla call with precisely the same underlying, strike, and maturity. The price discrepancy Dt=Ppoly,t−Pfair,t is the central metric, where Pfair,t is the option-implied risk-neutral value under Black–Scholes, extracted via mid-price-based implied volatility inversion.

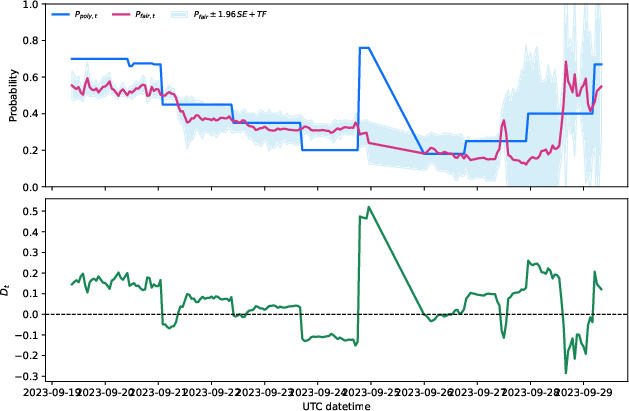

Figure 1: Main-market time series for BTC \$27,000 September contract, illustrating Polymarket Yes price, Binance risk-neutral benchmark, and discrepancy process.

Hourly-aligned time series ensure that observed pricing gaps are not artifacts of contract ambiguity or misaligned maturity, thus isolating genuine cross-market inefficiencies. The sample spans three matched Bitcoin threshold contracts in mid-2023, yielding 287 hourly observations in the pooled panel. Efficient, friction-adjusted comparison bands account conservatively for bid–ask spreads and fee structures native to each venue.

Statistical Characterization of Pricing Gaps

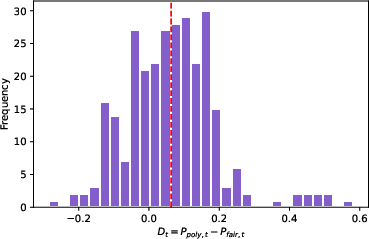

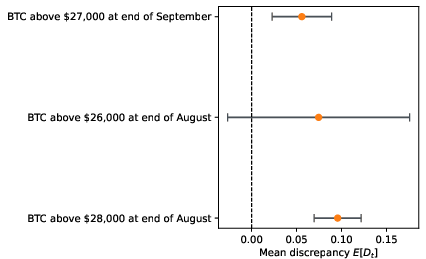

The primary finding is a statistically robust, economically significant positive wedge: Polymarket prices consistently exceed Binance-implied risk-neutral benchmarks. For the main September 2023 Bitcoin market (BTC \$27,000), the mean gap is 5.6 percentage points (t=6.46,$p<10<sup>{-9}$) across 214 observations. The pooled panel aggregates to a mean gap of 6.3 percentage points ($p<10<sup>{-14}$). This discrepancy is persistent (AR(1) half-life ≈ 4 hours), mean-reverting, and not explained by transient microstructure noise or stale quotes.

Figure 2: Pooled discrepancy distribution, demonstrating systematic positive deviation in Polymarket pricing.

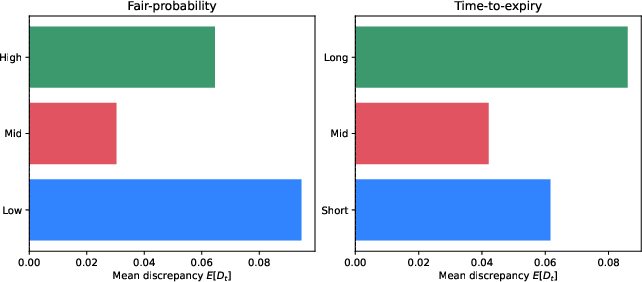

Figure 3: Mean gap across option-implied probability terciles, revealing concentration of discrepancy at low-probability regimes.

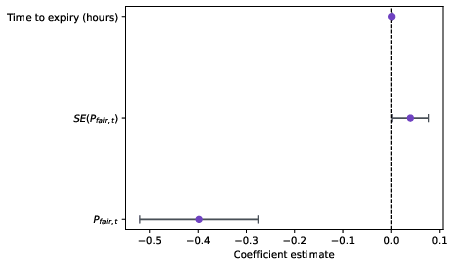

Cross-sectional regressions indicate that the wedge is maximized at low option-implied probabilities and long maturities, aligning with speculative demand for "longshot" contracts—an analogue to parimutuel favourite–longshot bias. Robustness checks (median, trimmed means, sign tests) confirm internal consistency and rule out outlier-driven inference.

Arbitrage Analysis and Economic Exploitability

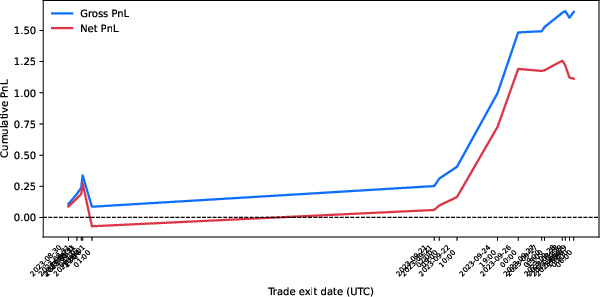

A backtest of a delta-hedged arbitrage proxy—constructing offsetting positions in Polymarket contracts, Binance calls, and spot Bitcoin—demonstrates net profitability after conservative transaction costs, though statistical precision is near threshold (p=0.053 for pooled net alpha of 0.067). Trades are initiated when observed discrepancies materially exceed estimated frictions and uncertainty, and are typically held for 3.5 hours until mean reversion or expiry.

Figure 4: Cumulative gross and net PnL across arbitrage-style trade exits, indicating positive net returns relative to deployed notional.

The presence of persistent arbitrage opportunities, though limited in frequency and scale, signals frictions and segmentation in cross-market capital mobility.

Benchmark Extensions: Deribit and Ethereum Markets

The same methodology applied to Deribit options yields larger discrepancies (~11 percentage points mean gap), indicating cross-exchange heterogeneity but confirming the qualitative directionality. A smaller Ethereum exercise delivers mixed results: three February markets are roughly aligned or slightly negative, but a March contract shows pronounced positive wedge. These results underscore the conservative nature of the Black–Scholes benchmark and highlight the role of market structure and asset-specific dynamics.

Theoretical and Practical Implications

The empirical evidence demonstrates that digital fragmentation—in both technological and institutional terms—imposes limits on cross-market price equalization, even for economically identical contingent claims. The persistent wedge observed between Polymarket and option-implied benchmarks is theoretically consistent with models of slow-moving capital, segmented participation, and demand-driven overpricing, as articulated in the literature on arbitrage limits and parimutuel biases.

The practical implication is that prediction-market probability aggregates may systematically overstate true risk-neutral expectations, particularly in low-probability, speculative contexts. Researchers and practitioners should interpret digital prediction-market signals with explicit adjustment for demand-side bias and cross-venue frictions. This has direct bearing on the use of prediction markets as probabilistic forecasting tools in both economics and finance.

Future Research Directions

Open questions include structural modeling of heterogeneous preferences, dynamic arbitrage constraints, and the scalability of cross-market arbitrage strategies across digital venues. Deeper exploration of settlement risks, liquidity heterogeneity, and microstructure features in decentralized versus centralized platforms would refine these results. Extending the analysis to broader asset classes and maturities, with stochastic-volatility corrections, promises to yield more comprehensive characterization of digital fragmentation in state-contingent pricing.

Conclusion

The paper establishes, via a precise option-theoretic benchmark, that blockchain-based prediction markets and centralized crypto-option exchanges exhibit systematic, persistent pricing wedges for identical Bitcoin threshold payoffs. The magnitude and structure of these discrepancies point toward speculative demand as a key mechanism, challenging the na\"ive interpretation of prediction-market prices as unbiased probabilities. This evidence advances the literature on information aggregation, market segmentation, and digital financial inclusion, and sets the stage for further investigation into structural frictions and cross-venue integration in digital financial ecosystems (2606.19517).