- The paper establishes that AMM token prices follow a structural CEV process with volatility inversely related to price, demonstrating a systematic leverage effect.

- It reveals that Black–Scholes underprices out-of-the-money options by ~6% compared to the CEV model, with discrepancies scaling as pool depth decreases.

- Empirical tests across 90 Bittensor subnets show a median variance elasticity of -0.86, confirming the CEV model's predictions for real-world DeFi environments.

Option Pricing for Automated Market Maker Tokens: A Structural CEV Approach

Structural Derivation of AMM Token Dynamics

This paper rigorously derives the price process for tokens whose price is exclusively determined by a constant-product AMM, notably as implemented in the Bittensor dTAO protocol. Employing a diffusion model for net staking flow, it is demonstrated that the AMM token price follows a Constant Elasticity of Variance (CEV) stochastic differential equation with exponent β=w, where w is the numeraire token weight in the pool. For the standard constant-product AMM (w=1/2), volatility is inversely proportional to the square root of price, structurally generating a leverage effect.

Empirical confirmation emerges from realized variance regressions across 90 Bittensor subnets, revealing a median variance elasticity of −0.86, decisively rejecting the Geometric Brownian Motion null hypothesis, and aligning with the CEV prediction. The closed-form European option pricing formula is obtained, leveraging the non-central chi-squared distribution. Liquidity-adjusted Greeks are defined, including a novel liquidity Greek Λ=∂C/∂k and an emission Greek E=∂C/∂e, capturing sensitivities to pool depth and token emissions respectively.

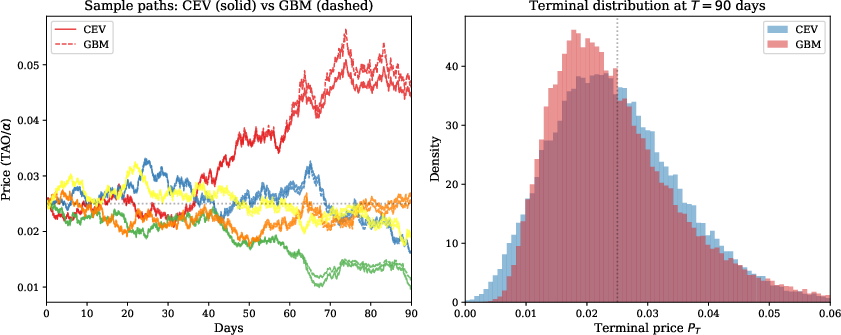

Figure 1: Simulated price paths under CEV (solid) and GBM (dashed) for identical Brownian increments, illustrating divergence in volatility structure.

Comparative Statics and Analytical Pricing Corrections

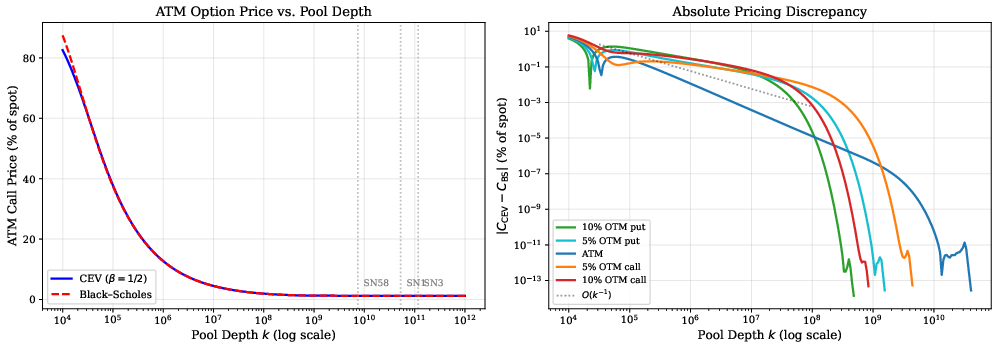

An explicit comparison of CEV and Black--Scholes pricing reveals that Black--Scholes emerges as the limiting case for large pool depth (infinite liquidity). The efficacy of Black--Scholes is quantified: CEV and BS ATM call prices are visually indistinguishable, but discrepancies for out-of-the-money (OTM) puts are persistent, with Black--Scholes underpricing OTM puts by approximately 6% in implied volatility at every pool depth. This normalized implied volatility skew is shown to depend only on the AMM pool weight parameter β, not on the volatility scale or depth, fundamentally refuting prior empirical parameterizations.

Figure 2: ATM call price vs. pool depth; CEV and Black--Scholes coincide at the money, but OTM discrepancies scale ∼ k−1.

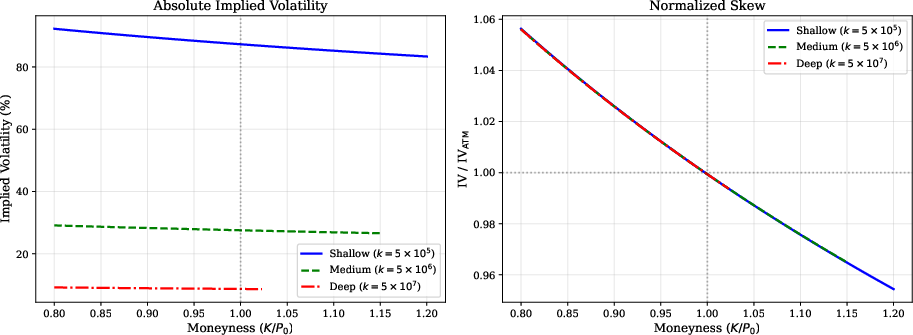

Figure 3: Implied volatility normalized by ATM level, confirming universal skew dependence on β alone.

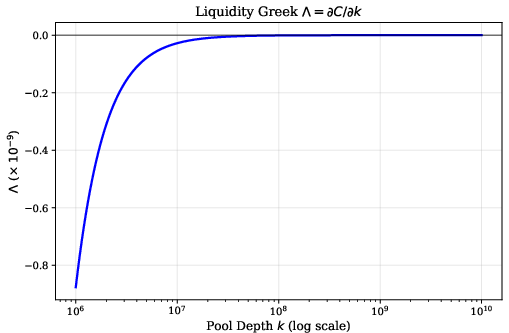

The liquidity Greek w0 quantifies option value sensitivity to pool depth; it is strongly negative for shallow pools and negligible for w1. This aligns with the practical observation that option values collapse as AMM pools deepen.

Figure 4: Liquidity Greek w2 as a function of pool depth, highlighting substantial sensitivity in shallow pools.

Emissions and Dynamic Liquidity Adjustments

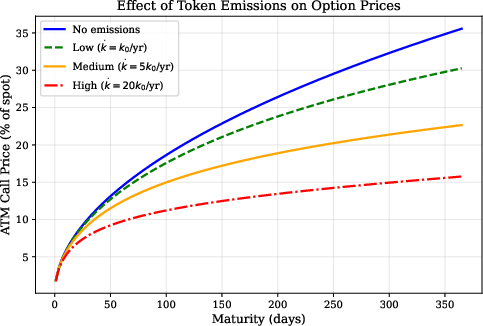

Token emissions, prevalent in Bittensor's protocol, introduce deterministic deepening of pool liquidity, dynamically compressing volatility. The integrated variance correction for time-dependent pool depth is formalized, with option prices decreasing as emission rates increase. The emission Greek provides direct quantification of sensitivity, and the analytic framework maps emissions to an effective dividend yield for variance adjustment.

Figure 5: ATM call prices vs. maturity under varying emission rates, emphasizing pronounced volatility compression in shallow pools.

Empirical Validation and Hedging Robustness

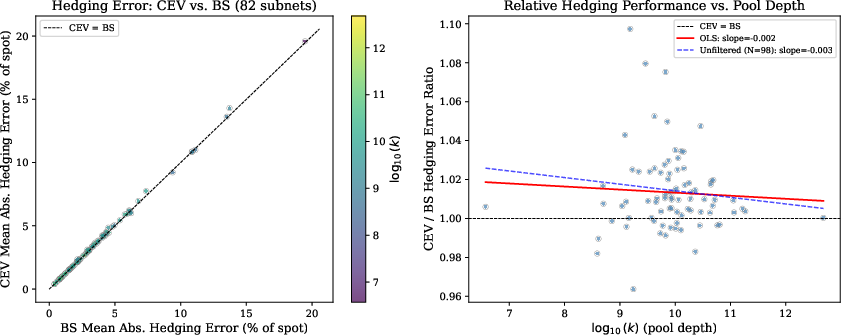

A cross-sectional delta-hedged backtest of ATM calls demonstrates that hedging errors under both CEV and Black--Scholes are nearly identical across pool depths, confirming theoretical predictions that divergences are confined to the wings (OTM strikes). The replication premium induced by AMM slippage is w3, vastly subdominant to the w4 magnitude of CEV–Black--Scholes pricing discrepancy for practical pool sizes encountered in Bittensor.

Figure 6: Mean absolute hedging error for delta-hedged ATM calls across Bittensor subnets: CEV and Black--Scholes exhibit indistinguishable performance.

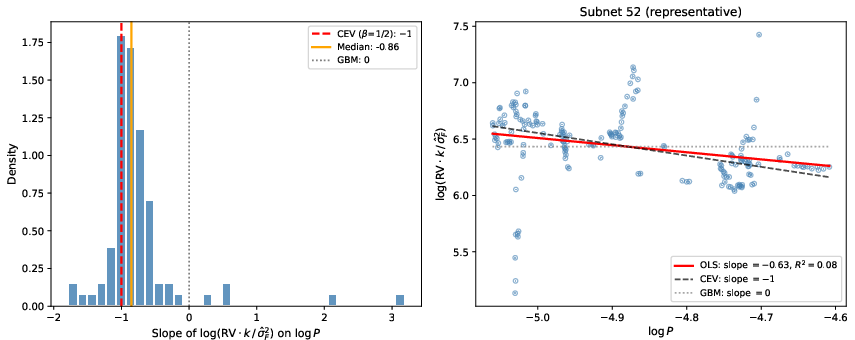

Variance elasticity tests on realized returns provide decisive evidence that volatility scales as w5, in accordance with the CEV structural prediction for w6. The median elasticity of w7 (IQR: w8) is statistically different from zero (GBM) and closely matches the theoretical model.

Figure 7: Distribution of empirical variance elasticity slopes across Bittensor subnets, decisively rejecting the GBM null.

Implications and Extensions

The structural CEV characterization of AMM token prices provides a foundational quantitative framework for derivatives pricing and risk management in AMM-dominated DeFi ecosystems. Practically, OTM put protection is systematically underpriced by models that assume lognormality, regardless of pool depth, posing ramifications for risk-neutral hedging and protocol treasury management. Theoretical implications include a direct mapping from AMM microstructure to volatility dynamics, obviating the need for empirical calibration.

Extensions include concentrated liquidity AMMs, basket options across correlated subnets, and jump-diffusion generalizations to account for heavy-tailed staking flows. Option manipulation risks in shallow pools are analytically bounded by the structural price impact relation.

Conclusion

This paper establishes that AMM-native token prices follow a CEV process, with the volatility exponent deterministically set by AMM design. Black--Scholes is valid only in infinite-liquidity asymptotics; for real-world DeFi pools, structural leverage effects and universal volatility skew are intrinsic. Empirical testing validates the diffusion approximation and the CEV variance-price relationship. The resulting derivations facilitate accurate pricing, hedging, and risk management for AMM token options, and inform optimal AMM protocol design in decentralized AI and finance applications.