- The paper demonstrates that visible TWAP orders significantly lower execution costs, reducing temporary impact by about 9 basis points compared to hidden metaorders.

- It leverages granular on-chain data to contrast execution dynamics, revealing distinct impact trajectories and scheduling between TWAP and statistical metaorders.

- The study shows that sunshine trading mitigates adverse selection and elicits robust liquidity provision responses, validating key microstructure models.

Market Impact, Adverse Selection, and Sunshine Trading on Hyperliquid

Introduction and Motivation

This paper provides a comprehensive empirical study of market impact, adverse selection, and the economic mechanisms arising from pre-trade transparency (“sunshine trading”) on Hyperliquid’s on-chain central limit order book (CLOB). The unique architecture of Hyperliquid, with protocol-native TWAP mechanisms and granular, address-level data, enables a direct comparison between visibly-announced order trajectories and statistically inferred latent metaorders—a setting regularly theorized but rarely observed in traditional markets.

Data and Institutional Setting

Hyperliquid offers spot and perpetual futures trading on a fully on-chain CLOB. Crucially, the platform implements protocol-native, public TWAP orders, splitting metaorders into child trades at fixed intervals, with all parameters visible to market participants from submission. The analysis reconstructs over 4 million statistical metaorders (hidden, ex-post inferred using child order clustering) and 465,000 natively visible TWAP metaorders, comparing execution costs, impact profiles, and dynamic footprint. The dataset, comprising USD 1.93 trillion cross 641 million fills, enables robust cross-sectional and conditional inference.

Stylized Facts and Empirical Characterization

Metaorder style—rather than raw size—is the primary driver of differences. Native TWAPs are executed with markedly lower participation rates, spread over longer volume-time durations, and are substantially larger in the right tail but more finely sliced (higher child order count). In contrast, statistical metaorders are more aggressive within shorter time frames, concentrate market impact, and display execution strategies more consistent with optimal transient-impact theory.

Aggregate Market Impact and the Decomposition of Execution Costs

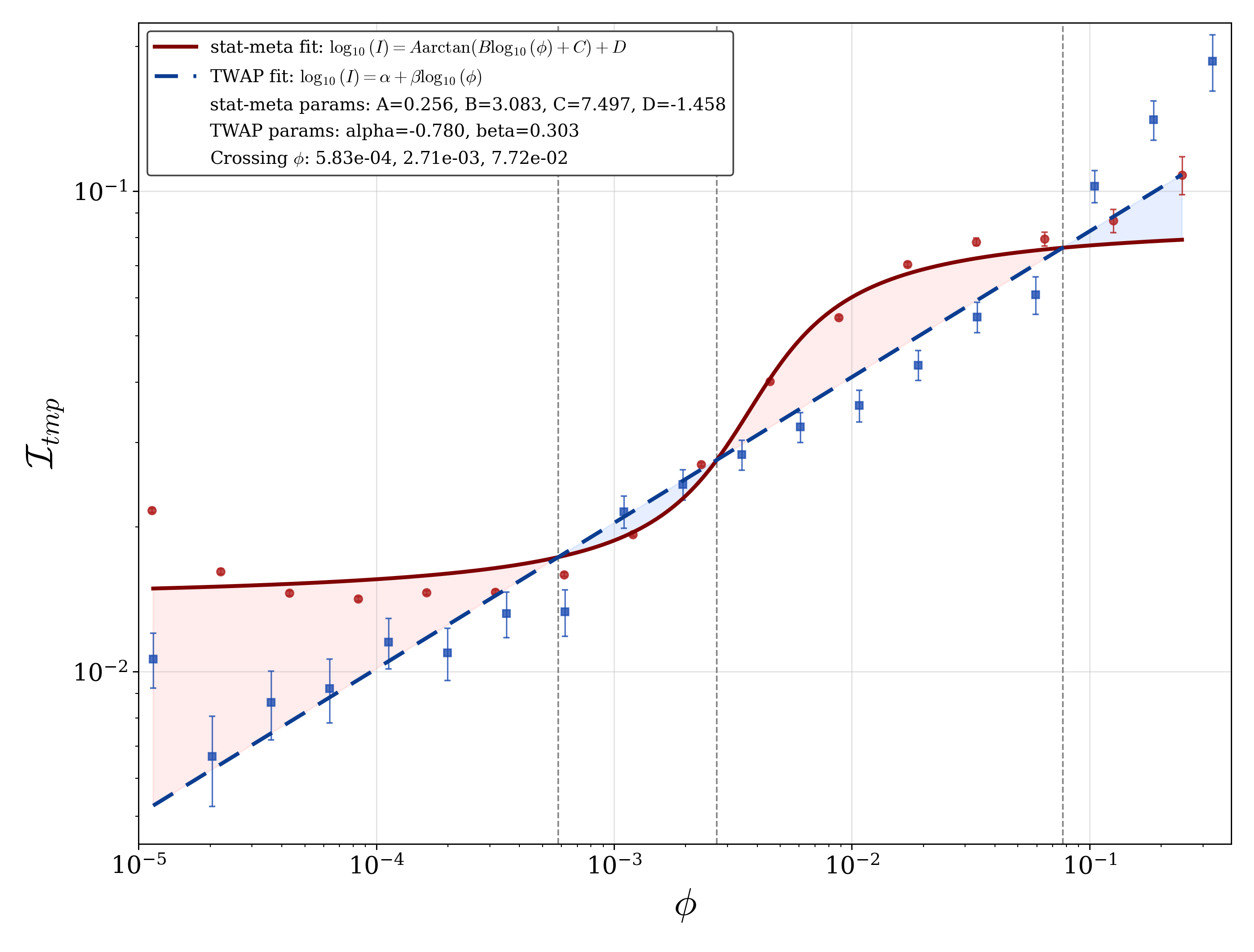

The study confirms—and strongly nuances—the classic “square-root law” of market impact: for native TWAPs, the volatility-normalized temporary market impact scales as Itmp∝ϕ0.30, with ϕ being the traded fraction, exhibiting a sublinear, near power-law dependence (Figure 1).

Figure 1: Temporary market impact Itmp as a function of traded fraction ϕ, showing sharply lower impact and distinct functional form for visible TWAPs versus statistical metaorders.

Statistical metaorders, however, exhibit strongly nonlinear, saturating impact curves—impact grows steeply at intermediate ϕ and flattens at extremes. Conditioning on execution duration and participation reveals that impact is much more sensitive to execution duration than to participation rate, directly contradicting the universality of the one-dimensional square-root law.

Impact Trajectories, Schedules, and Execution Dynamics

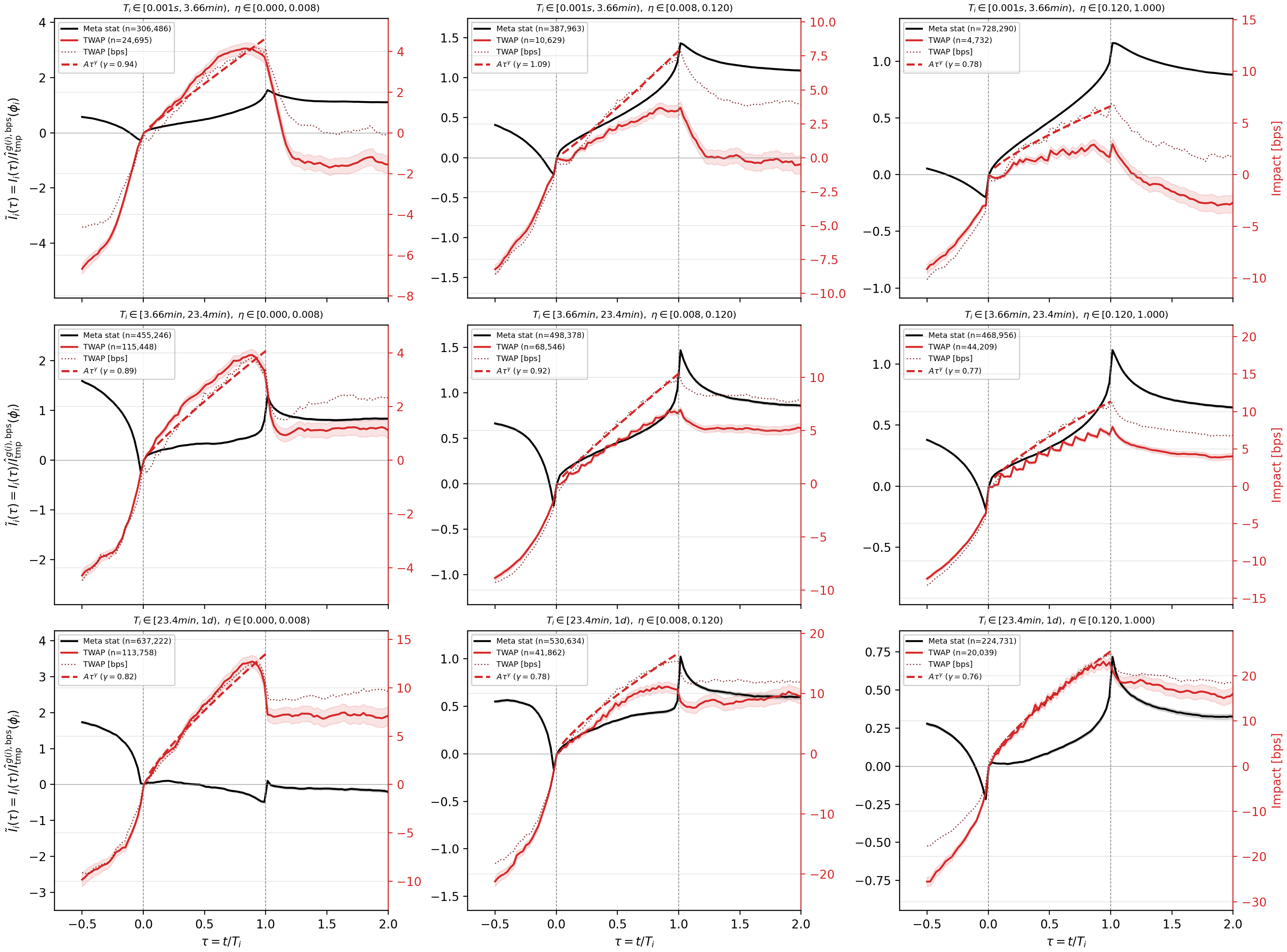

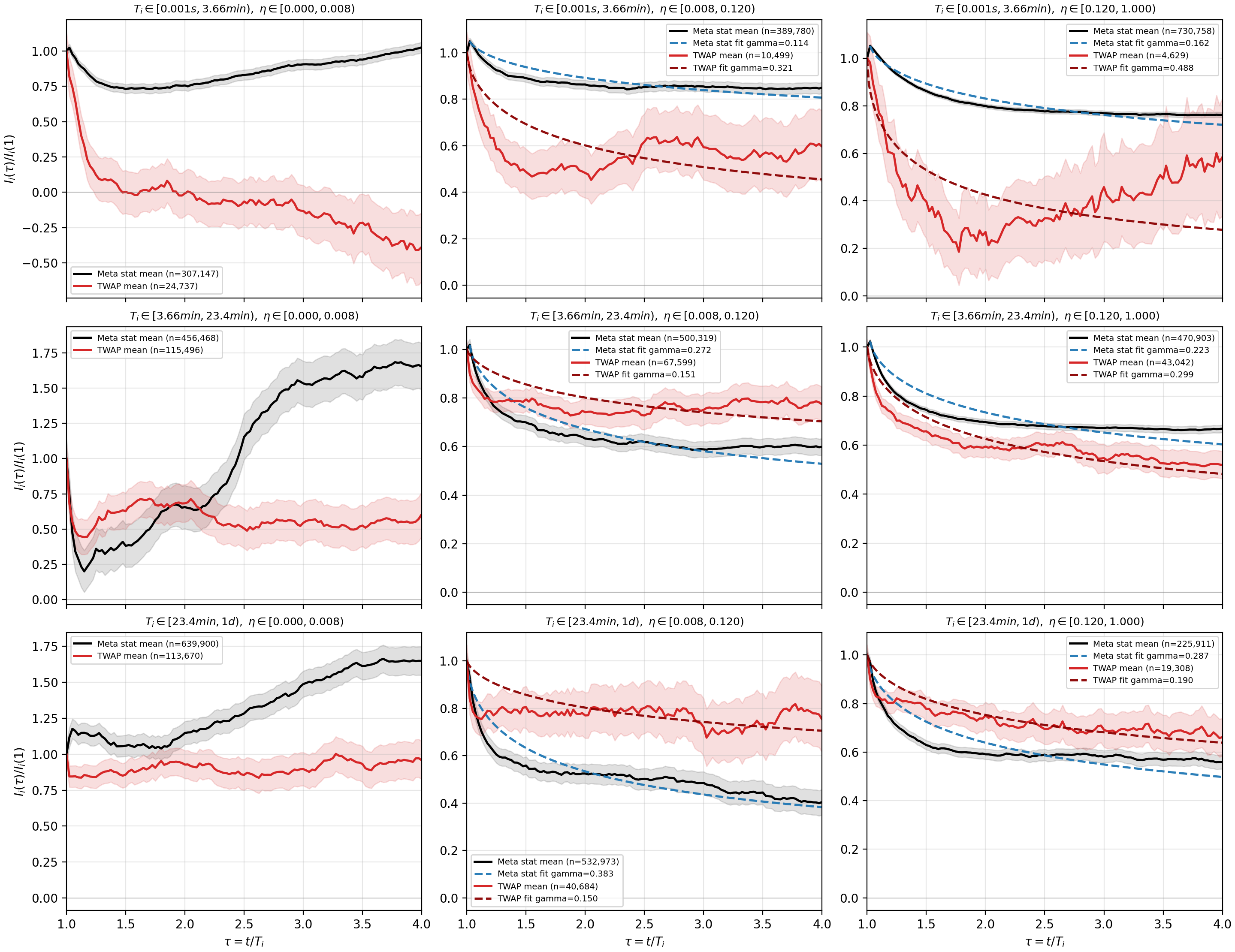

TWAPs yield strictly concave, smooth price trajectories throughout the execution interval, consistent with constant-rate trading and propagator-theoretic expectations (concave, power-law temporal buildup). By contrast, statistical metaorders exhibit S-shaped, double-inflection trajectories, with sharp peaks upon completion and stronger post-trade decay—dynamics consistent with risk-averse, optimal transient-impact schedules.

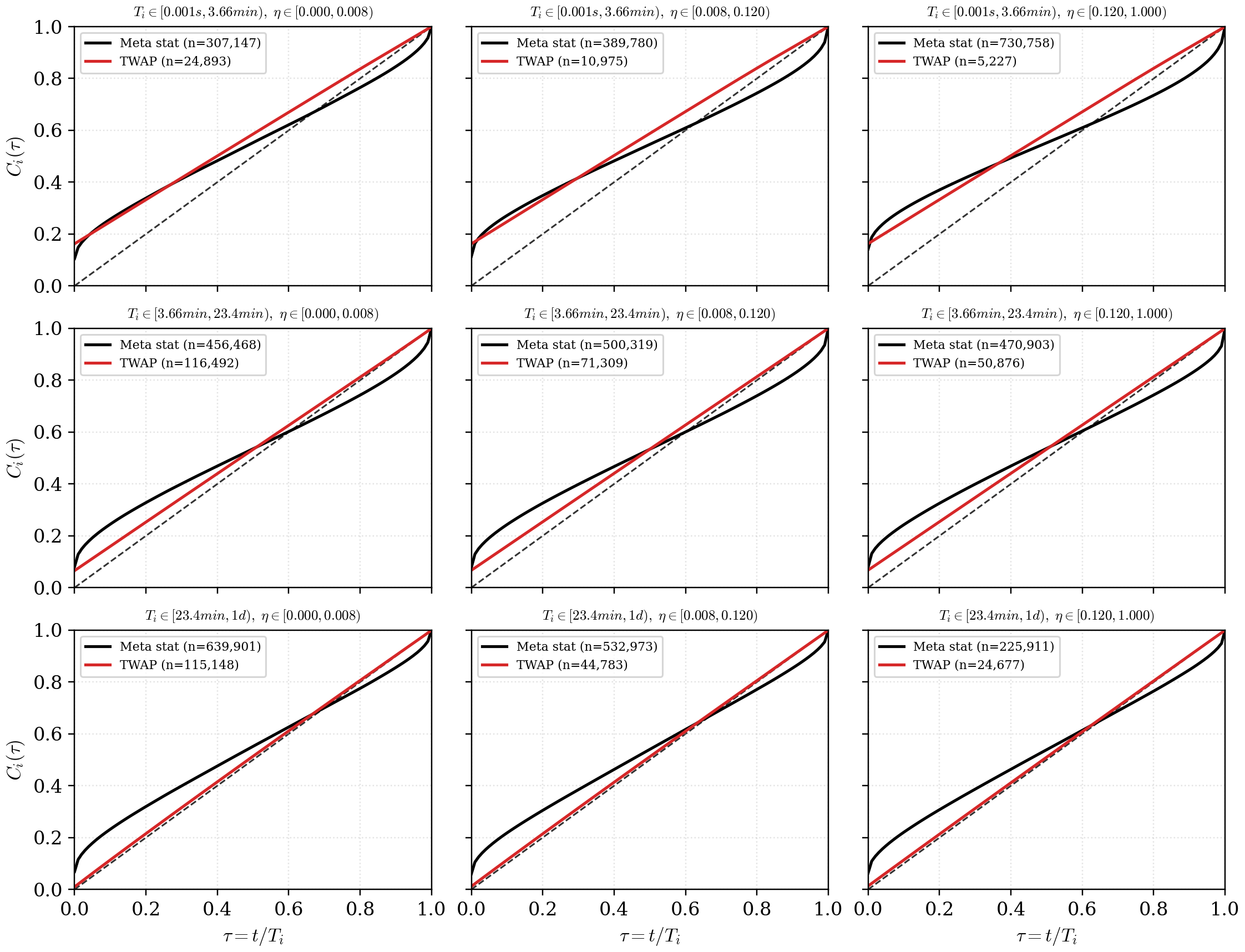

The execution schedules further elucidate this distinction: TWAP programs result in nearly linear cumulative execution, whereas statistical metaorders show classic U-shaped scheduling, front-loading and end-loading trading velocity (Figures 3 & 4).

Figure 2: Average signed impact trajectories, conditional on both order duration and participation; TWAP and statistical styles diverge sharply.

Figure 3: Average normalized execution schedules. Statistical metaorders display a U-shaped schedule, while TWAPs exhibit uniform execution.

Sunshine Trading: Mechanism Tests and Empirical Validity

The core of the paper operationalizes the Admati and Pfleiderer framework for sunshine trading via four empirical tests using the privileged Hyperliquid microstructure.

1. Trading Costs for Announcers

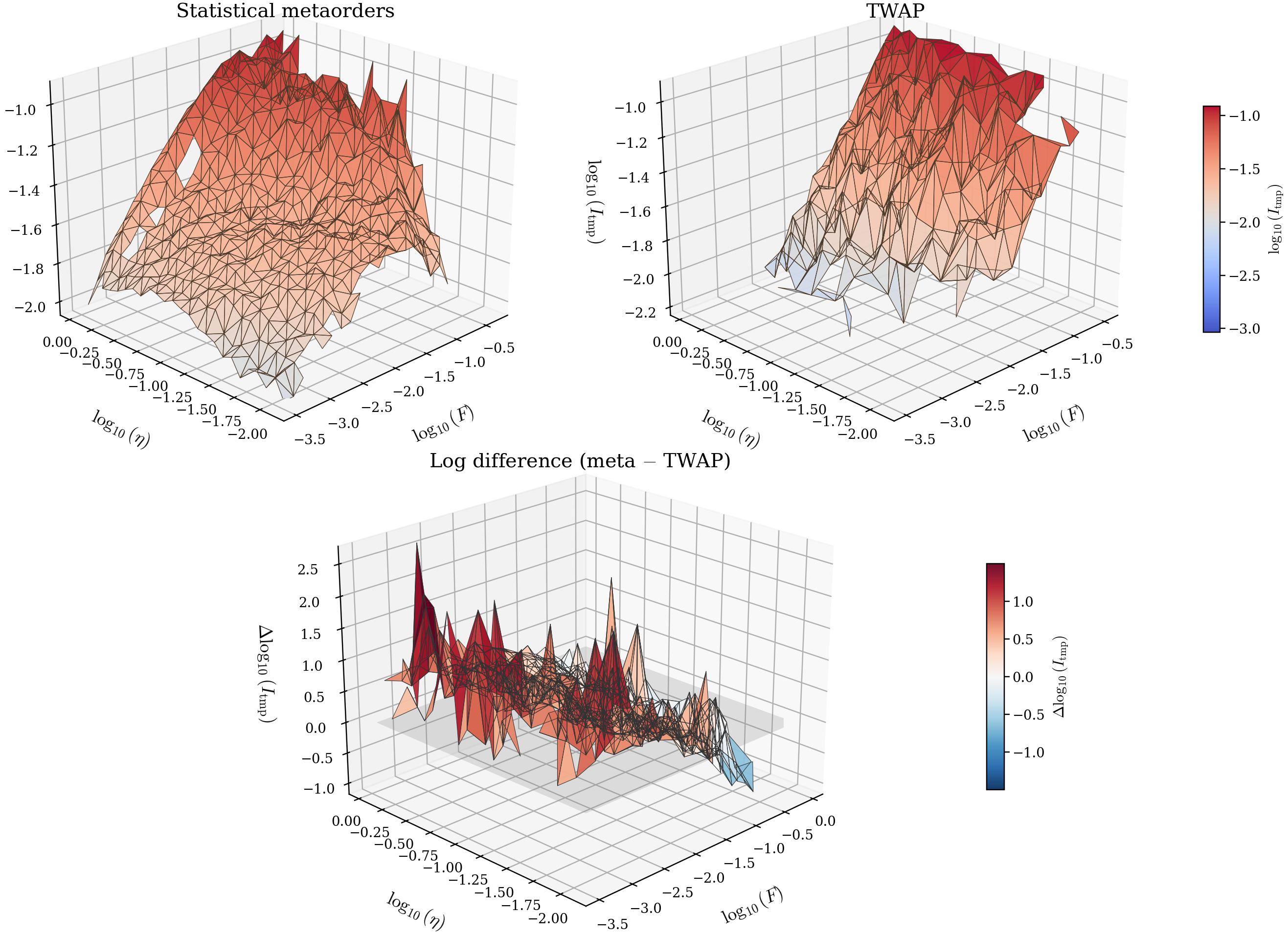

Conditional on execution parameters, visible TWAPs consistently incur lower temporary market impact than statistical metaorders—by a median of 9 basis points at median volatility, with an average impact ratio favoring TWAPs by a factor of approximately 2.3 over common-support bins (Figure 4). This effect persists after controlling for order characteristics and market volatility.

Figure 4: Common-support temporary-impact surfaces illustrating statistically lower costs for visible TWAPs compared to hidden statistical metaorders.

2. Information Content and Permanent Impact

Announced TWAPs exhibit significantly lower permanent price displacement after execution—about 5 basis points less than hidden metaorders, conditional on order profile and market conditions (Figure 5). Post-trade decay analysis confirms that TWAP-induced price moves revert more rapidly, indicating these are perceived as less informative/liquidity-driven versus the more information-impacted metaorders.

Figure 5: Decay profiles of post-execution impact, highlighting faster dissipation and lower permanent impact for TWAPs.

3. Adverse Selection: Cost for Non-announcers

Hidden statistical metaorders executed alongside same-direction visible TWAP activity incur higher permanent impact: a 10% increase in same-direction (already observable) TWAP flow elevates latent metaorder costs by 0.8–0.9 basis points. This adverse selection effect is persistent, not explained by mechanical price pressure, and aligns sharply with the sorting mechanism predicted in theoretical sunshine-trading equilibria.

4. Liquidity Provision Response

Active TWAP windows prompt substantial liquidity-provision responses in the order book: displayed depth increases, the book tilts to the absorbing side, and sweep costs fall relative to baseline. Notably, these effects scale with announced order size and are not the result of favorable pre-trends or market selection (Figure 6). However, the best quote spread widens during large, visible executions—liquidity suppliers supply depth discretely away from the touch, demanding compensation for inventory risk.

(Figure 6)

Figure 6: Order-book liquidity metrics during TWAP execution: visible orders tilt book imbalance, increase depth, and lower sweep costs on the absorbing side.

Theoretical Consistency and Model Implications

These empirical findings are congruent with equilibrium models of sunshine trading: visible, non-informative flow receives lower marginal pricing, and market-makers (or automated liquidity suppliers in DeFi) respond by supplying more depth selectively during visible program windows, in line with the informational separation and liquidity-supply coordination of Admati and Pfleiderer.

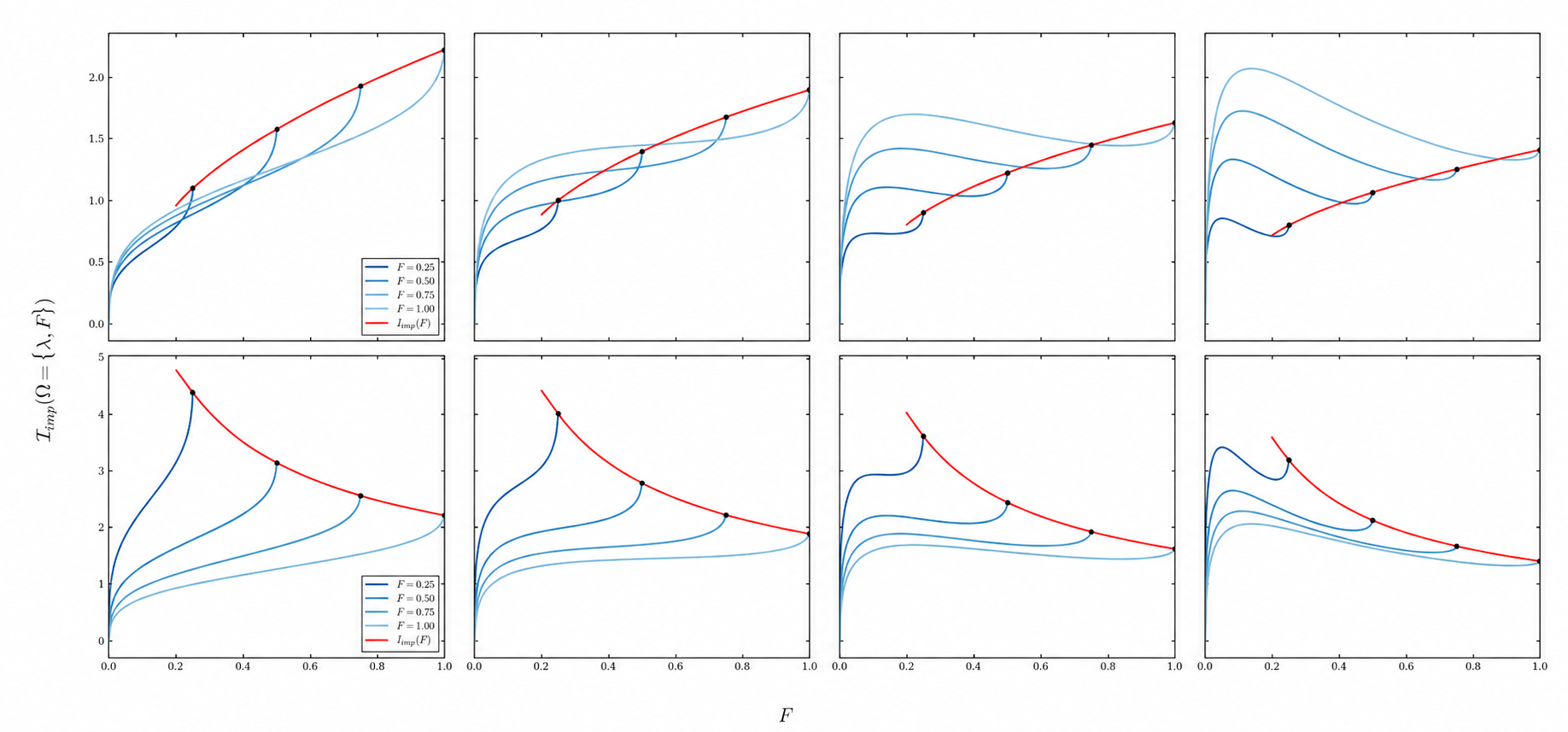

A propagator model (Figure 7) demonstrates that the observed distinct trajectory shapes—concave power-law for uniform execution, S-shaped with terminal peaks for transient-impact optimized trading—can be explained parsimoniously by varying the risk aversion parameter in mean-variance scheduling.

Figure 7: Propagator model impact trajectories illustrate transition from linear (TWAP) to S-shaped (strategic) impact under varying risk aversion.

Limitations

Interpretation must recognize several caveats:

- The regime comparison is observational and entwined with trader identity: most participants specialize exclusively in either hidden or visible execution.

- Latent metaorders are only partially hidden—address-level clustering enables gradual inference, so the true difference is between explicit preannouncement and statistical detectability, not full anonymity.

- Results are environment-specific: the ready observability and protocol-native TWAPs on Hyperliquid do not fully generalize to traditional or AMM-based trading venues.

Conclusion

The paper provides unambiguous, large-scale evidence that on-chain, protocol-mediated preannouncement (sunshine trading) via visible TWAPs reduces execution costs, diminishes adverse selection, and elicits substantial liquidity provision on the observable limit order book on Hyperliquid. The observable mechanisms closely track the theoretical channels of pre-trade transparency, confirming that sunshine trading selects for less informative flow, offloads adverse selection to non-announcers, and supports coordinated liquidity supply. These data-rich DeFi venues offer a unique lab to interrogate longstanding microstructure theory and highlight both opportunities and risks in designing transparent trading protocols. Future work could leverage cross-market variation, analyze identity effects, or extrapolate to environments with batch auctions or MEV-resistant execution.