- The paper develops a high-frequency, OSINT-based GPR index from Telegram channels and applies a PC algorithm for robust causal discovery.

- It demonstrates that political and energy narratives causally precede conflict indicators, with conflict signals impacting energy sector ETF returns.

- The approach integrates multi-DAG analysis, bootstrap resampling, and SVAR tests to enhance real-time risk monitoring and market response insights.

CausalAlpha: Real-Time Geopolitical Risk Index Construction and Causal Analysis in Financial Markets

Framework Architecture and Index Construction

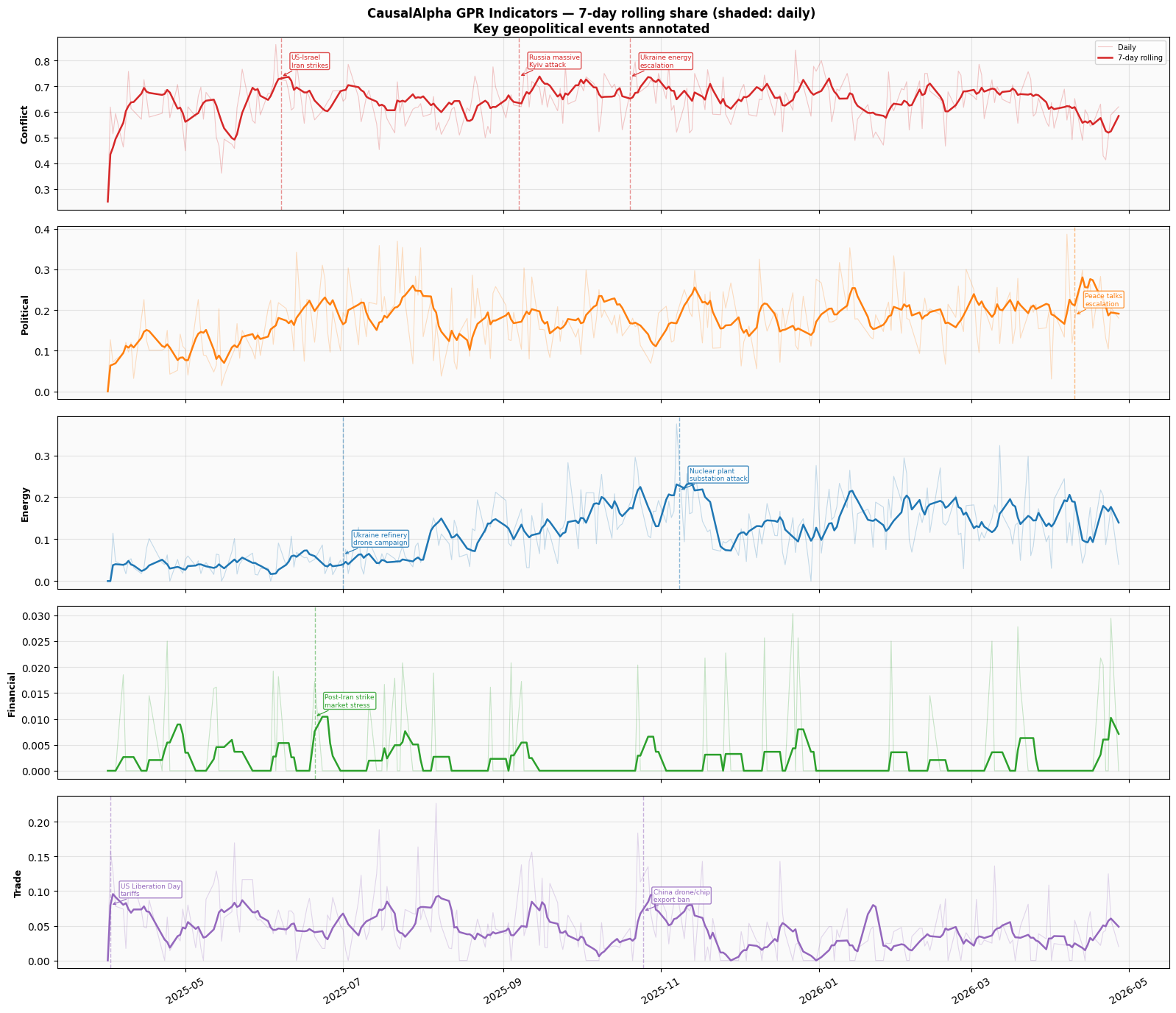

CausalAlpha presents an open-source pipeline for real-time construction of a high-frequency Geopolitical Risk (GPR) index from Telegram-based OSINT channels, emphasizing latency reduction in capturing geopolitical risk proxies. Six neutral and independent Telegram channels were curated to avoid bias and disinformation vectors, yielding a corpus tailored for conflict-intensive coverage, particularly the Russia–Ukraine war. The NLP pipeline operates daily, identifying five distinct GPR categories: Conflict, Political Instability, Energy Security, Trade Disruption, and Financial Stress, using keyword-driven message processing. Instead of aggregating these into a single GPR measure, CausalAlpha computes category-specific daily shares and applies a 7-day rolling average, mitigating noise but preserving event-driven spikes.

Figure 1: CausalAlpha GPR indicators showing both daily and 7-day rolling shares for five categories, highlighting structural breaks and spikes coinciding with major geopolitical events.

The resulting indicators reveal Conflict as the dominant signal, consistently comprising 55–70% of daily messages. Notably, the Energy indicator exhibits a structural break in July 2025, coinciding with drone strikes targeting Russian energy infrastructure, reflecting genuine shifts in the geopolitical news cycle rather than artifacts. Both Trade and Energy indicators display sharp event-driven surges, further validating the pipeline's capacity to distinguish episodic versus persistent geopolitical risks.

Causal Discovery Methodology

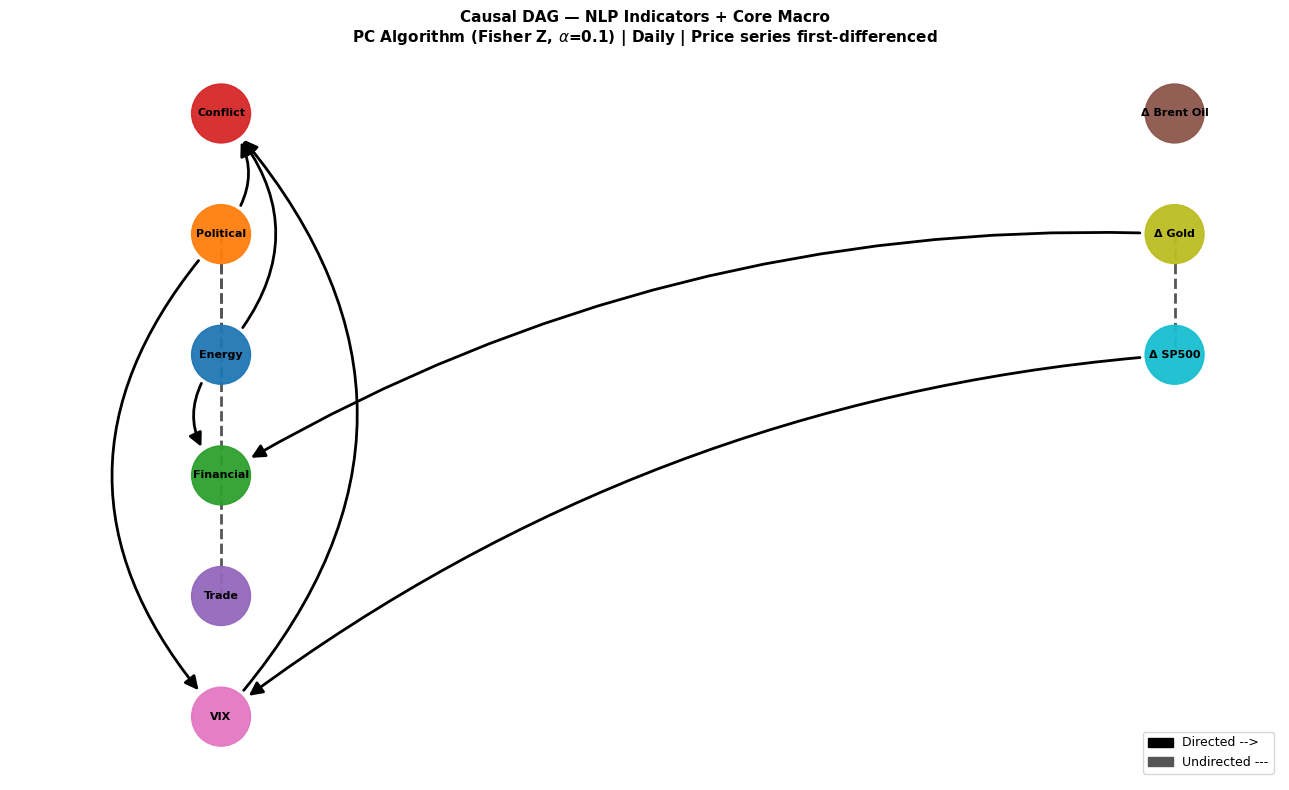

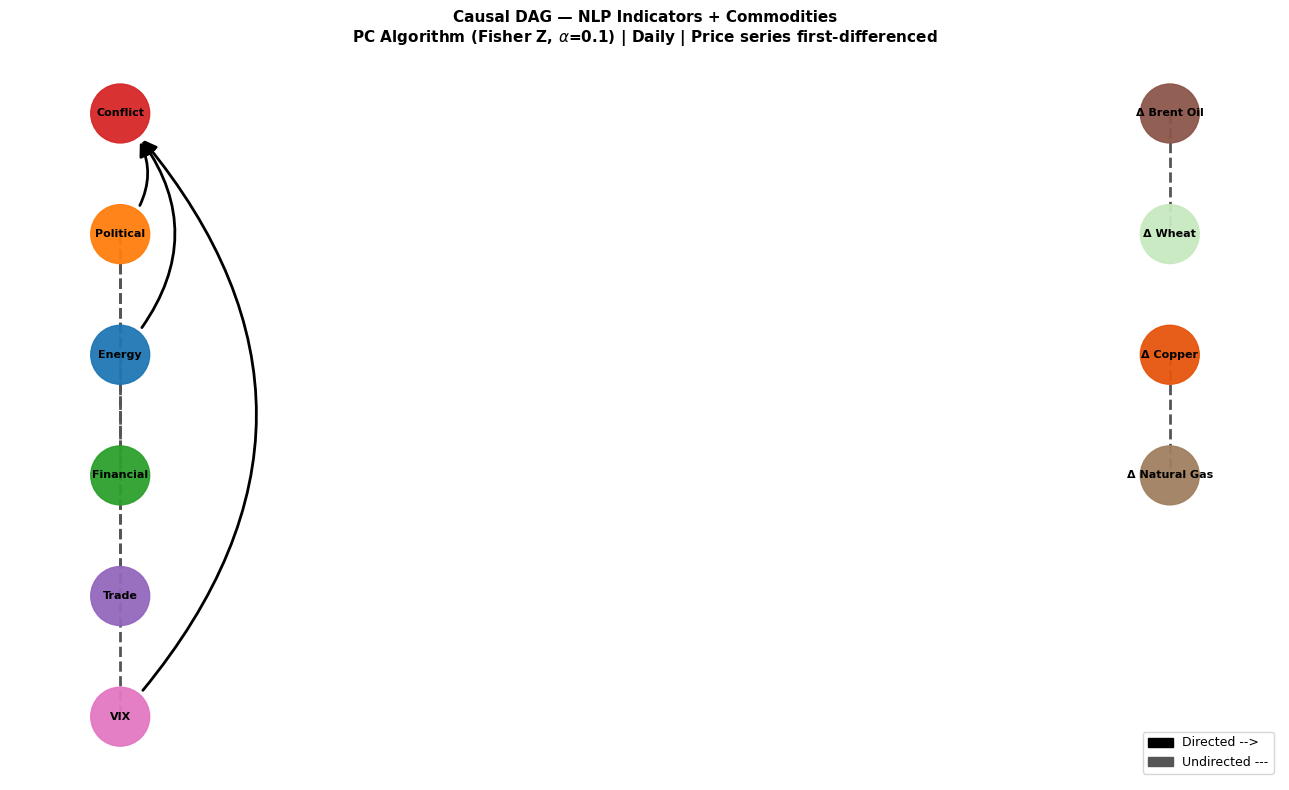

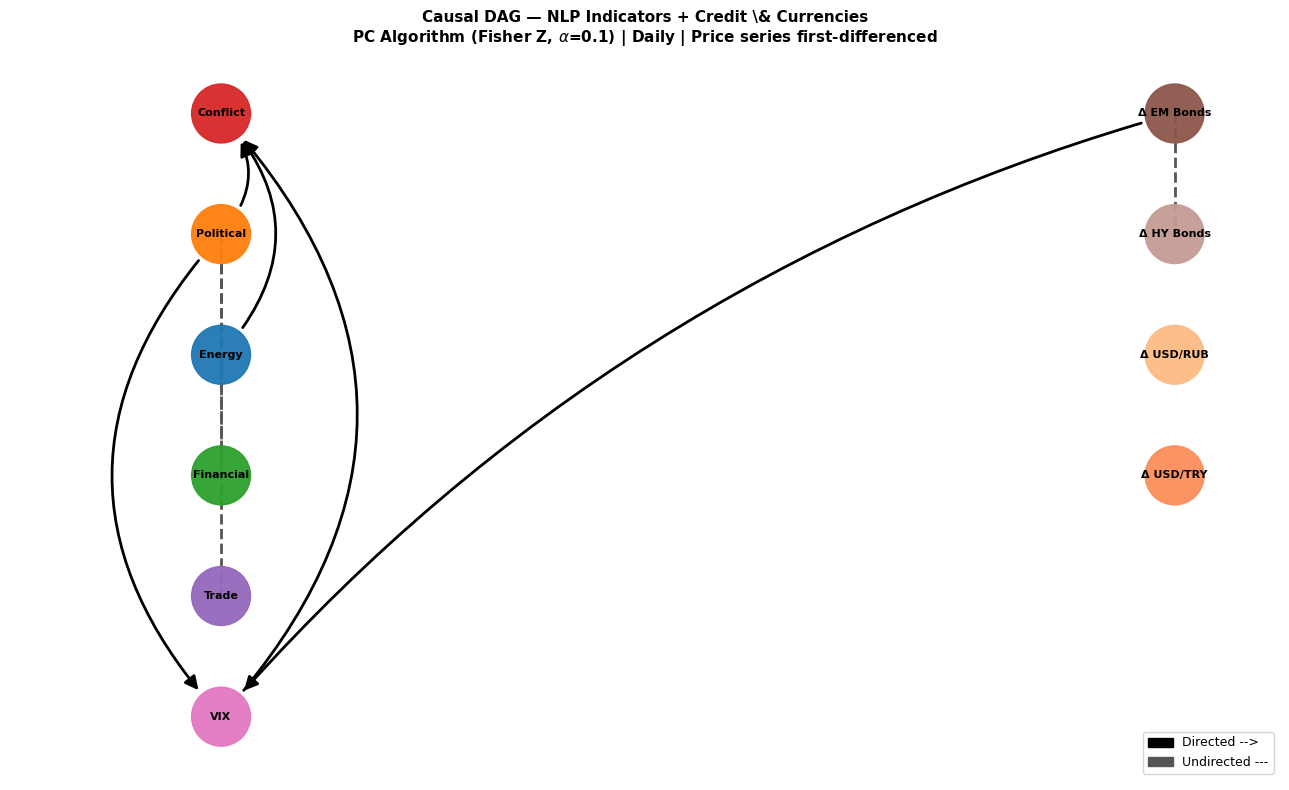

CausalAlpha integrates the PC algorithm—a constraint-based causal discovery method—across four DAG specifications and three alpha levels (0.05, 0.10, 0.15) with 500 block-bootstrap resamples for edge stability quantification. The PC algorithm avoids omitted variable bias by conditioning independence tests on the full variable set, overcoming limitations of standard pairwise Granger causality.

The four market panels are:

- Core macro: VIX, ΔBrent, ΔGold, ΔSP500

- Commodities: VIX, ΔBrent, ΔWheat, ΔCopper, ΔNatural Gas

- Credit/FX: VIX, ΔEM Bonds, ΔHY Bonds, ΔUSD/RUB, Δ0USD/TRY

- Equity sector ETFs: VIX, Δ1SP500, Δ2XLE, Δ3ITA, Δ4XLF

This multi-specification DAG approach probes the cross-domain robustness of detected causal edges, a critical design for generalizability across asset classes.

Empirical Causal Structure

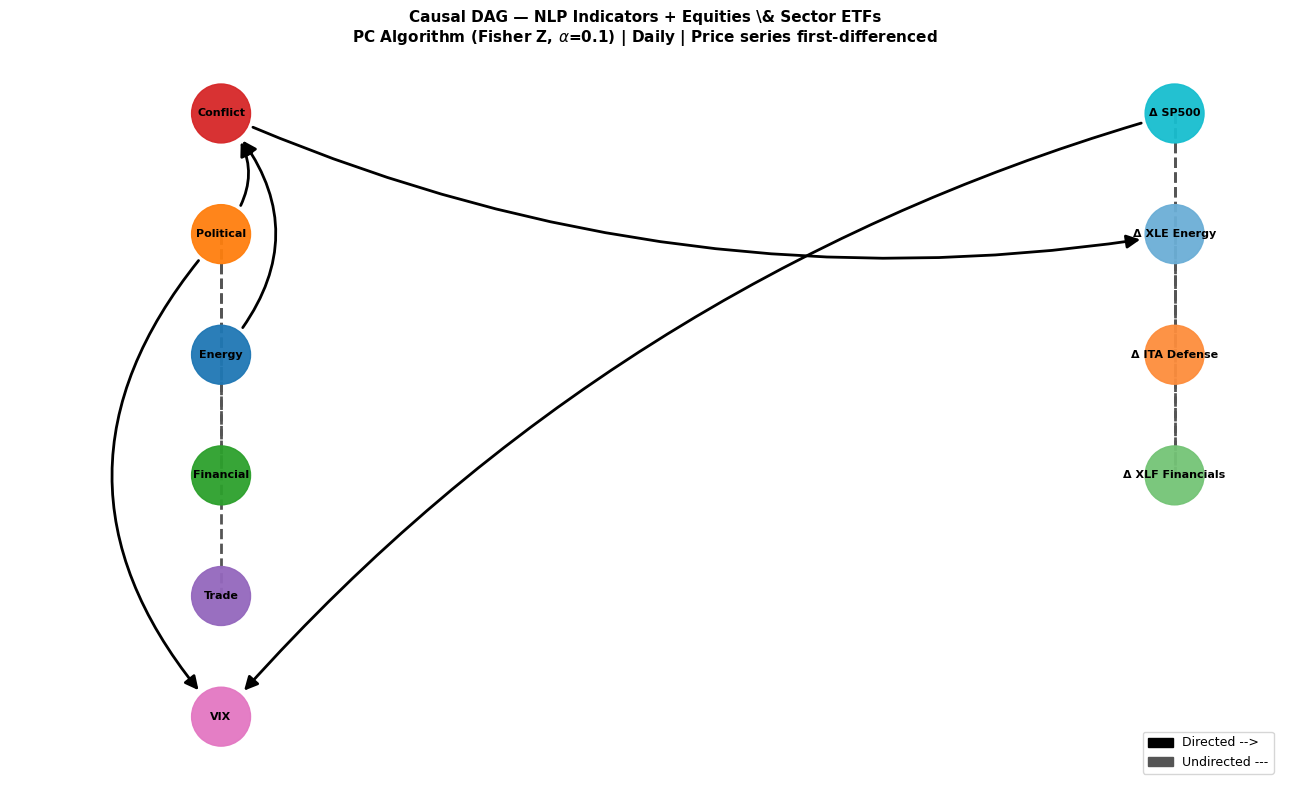

Robust causal discovery yields two primary findings. Across all DAGs and at Δ5, Political Instability and Energy Security media coverage independently and causally precede Conflict coverage, establishing Conflict as the principal causal sink in OSINT-driven geopolitical narrative escalation. At the strictest threshold (Δ6), Conflict coverage causally precedes energy sector equity returns (Δ7XLE), indicating direct transmission from geopolitical escalation to financial markets—specifically the energy sector ETF, which is a principal traded entity for U.S. energy equities.

Figures reporting domain-specific causal DAGs further elucidate directed and undirected associations:

Figure 2: Causal DAG showing directed edges from Political and Energy indicators to Conflict and equity/macroeconomic variables.

Figure 3: Causal DAG highlighting commodity and NLP indicator relationships, reinforcing contemporaneous dynamics and co-movement across Wheat and Brent.

Figure 4: Causal DAG focusing on credit and currency markets, with statistically robust Δ8EM Bonds Δ9 VIX edge.

Figure 5: Causal DAG for sector ETFs displaying Conflict Δ0 Δ1XLE Energy as the preferred orientation at Δ2.

The Conflict-to-energy ETF edge is notable not only for its statistical strength (bootstrap probability 0.528) but also for its causal ordering, aligning with empirical literature on anticipatory market behavior to conflict onsets [chadefaux2017market], and complementing studies using high-frequency VARs for oil price shocks [VerduzcoZanetti2026].

Short-Run Price Transmission Analysis

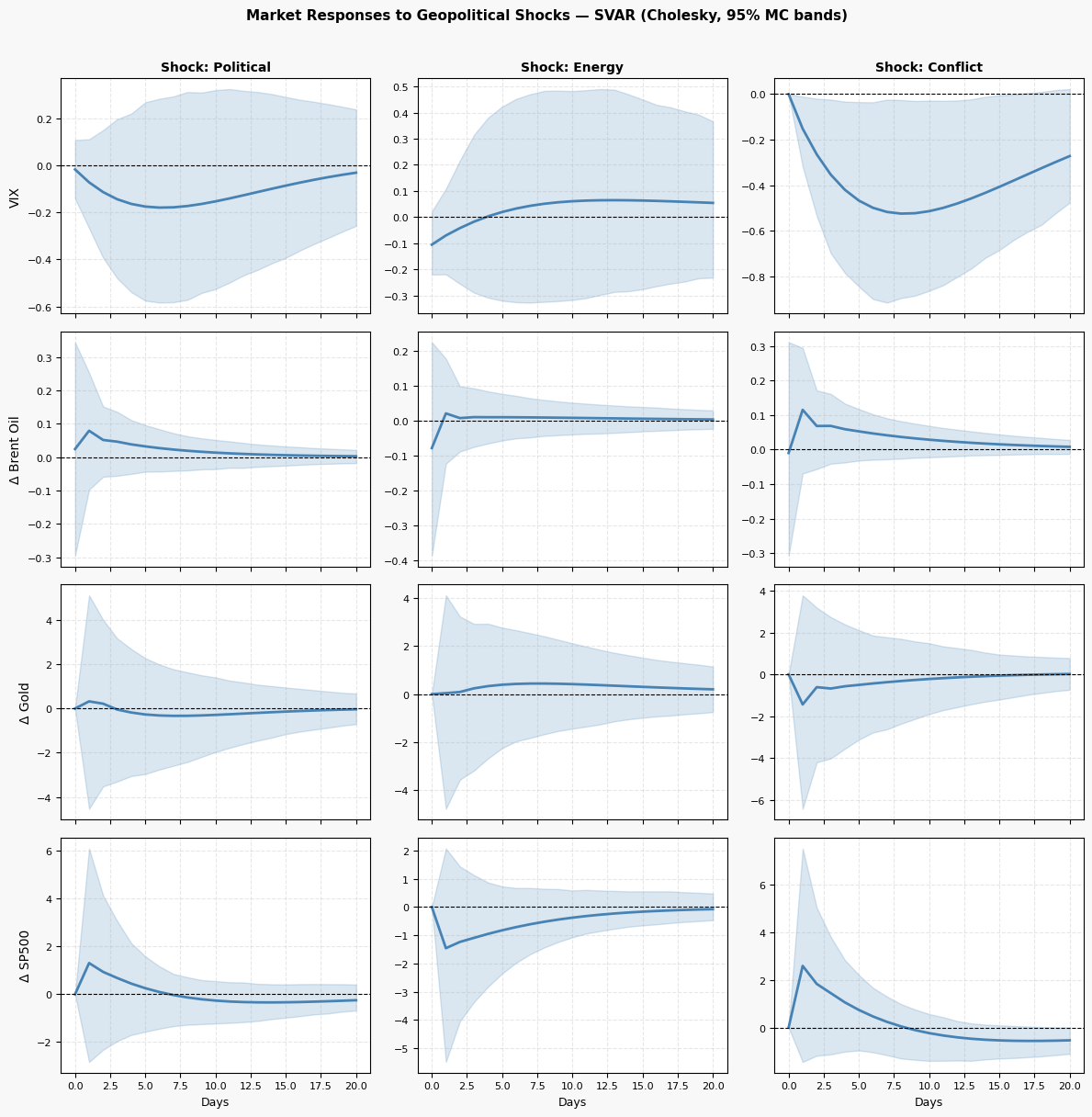

CausalAlpha estimates an SVAR on the core macro panel to test dynamic shock propagation from GPR indicators to financial market prices. The Cholesky ordering, rooted in the directed edges from the PC algorithm, supports topologically informed impulse response estimation.

Figure 6: SVAR impulse response functions for shocks to Political, Energy, and Conflict NLP indicators, showing weak transmission to VIX, Brent, Gold, and SP500 variables at daily frequency.

Responses reveal that transmission from NLP geopolitical signals to asset prices is statistically weak—confidence bands mostly include zero at all horizons—underscoring the rapid information incorporation by markets relative to news cycles. Exceptionally, the Conflict Δ3 VIX response is negative but marginal in significance.

Forecast error variance decomposition corroborates this finding:

Figure 7: FEVD analysis highlighting dominance of own-variance in market variables, with GPR indicators explaining minimal forecast variance.

These results suggest the functional role of OSINT signals as narrative drivers within the media system rather than as direct generators of price moves at the daily horizon.

Prediction Market Extension

CausalAlpha proposes the integration of prediction market data (e.g., Polymarket) as a third information layer, capturing forward-looking probability series mapped to geopolitical risk contracts. Preliminary evidence indicates prediction markets may react faster than OSINT and traditional media, with financially incentivized traders preempting event coverage. This raises the hypothesis of a three-layered causal ordering: OSINT NLP indicators Δ4 prediction market probabilities Δ5 asset prices.

Implications, Robustness, and Future Directions

The study formalizes OSINT channels as a valuable risk monitoring source, constructing category-specific, event-sensitive GPR measures. The causal system recovered through PC algorithm demonstrates the primacy of conflict escalation as a media sink, with political and energy narratives acting as upstream triggers. The transmission to financial markets is largely indirect and more pronounced for sector-specific ETFs (e.g., energy), consistent with the notion of markets as anticipatory agents.

Practical implications include improved early-warning capability for sovereign risk monitoring, suggesting that systematic real-time tracking of political and energy narratives can signal pending conflict escalation, possibly preceding both traditional risk indices and price responses. Theoretical implications extend to the modeling of information diffusion and market reaction time, underlining the media–market temporal asymmetry.

Future development should focus on:

- Extending aggregation to weekly/monthly data to capture lower-frequency transmission.

- Enhancing OSINT coverage beyond conflict-centric channels for broader generalizability.

- More granular inclusion of commodity-specific and financial reporting OSINT sources.

- Rigorous integration of prediction market probabilities as dynamic information intermediaries.

- Applying alternative independence tests robust to non-Gaussianity for sparse NLP indicators.

Conclusion

CausalAlpha operationalizes real-time, category-specific GPR measurement and causal analysis, uncovering a robust narrative structure in OSINT channels and limited direct transmission to daily asset price dynamics. The primary causal sinks and upstream triggers are consistent across multiple asset classes and significance levels, providing empirical support for the differentiated roles of political, energy, and conflict narratives in shaping both media and financial systems. The methodological advances, including multi-DAG, bootstrap validation, and SVAR cross-verification, lay the groundwork for increasingly precise macrofinancial risk monitoring leveraging OSINT and prediction market data.

(2606.07049)