- The paper's main contribution is a novel two-stage framework using wavelet-quantile transfer entropy for directional detection of financial contagion.

- It employs multi-method structural attribution to decompose contagion into Trade, Financial, Geopolitical, Behavioural, and Monetary Policy channels.

- Results reveal regime-specific channel dominance and robust identification of cross-market propagation during crises.

Mechanism Attribution in Cross-Border Financial Contagion: A Multi-Stage Identification Framework

Introduction

The paper "What Drives Contagion? Identifying and Attributing Cross-Border Transmission Mechanisms" (2604.26546) addresses a core limitation in the empirical contagion literature: the methodological gap between the detection of cross-border propagation of financial shocks and the attribution of such propagation to concrete, policy-actionable economic mechanisms. The prevailing detection approaches—correlation, connectedness, or information theory-based methods—are agnostic with respect to structural cause, leaving analysts with limited direction for intervention or risk allocation.

This work proposes and empirically implements a two-stage framework. The first stage employs wavelet-quantile transfer entropy (WQTE) for scale-, frequency-, and quantile-resolved directional detection of cross-market transmission, overcoming the aggregation bias of classical Granger-causality and variance-decomposition diagnostics. The second stage innovatively decomposes statistically significant propagation into five exclusive channels—Trade, Financial, Geopolitical, Behavioural, and Monetary Policy—using a suite of mutually disciplining identification strategies, including instrumented 2SLS, LASSO-based instrument selection, local projections at multiple horizons, heteroskedasticity-based inference, and sensitivity quantification.

Data and Channel Engineering

The analysis covers 18 G20 equity return series daily from January 2006 to March 2026, partitioned into eight distinct stress-regimes spanning the GFC, COVID-19, and regionalized crises. The composite design of the five transmission channels strictly enforces identification orthogonality through instrument construction and orthogonalisation procedures. Trade exposure is proxied by returns to the trade-weighted dollar index; the financial channel incorporates VIX, high-yield spreads, and the St. Louis Fed Financial Stress Index; the geopolitical/pandemic composite uses the Caldara-Iacoviello GPR and pandemic indices; the behavioural channel isolates sentiment proxies orthogonal to financial conditions; and monetary-policy is constructed via first-differenced rate composites, avoiding persistence- and co-integration-driven weak-instrument inflation.

Stage 1: Wavelet-Quantile Transfer Entropy Detection

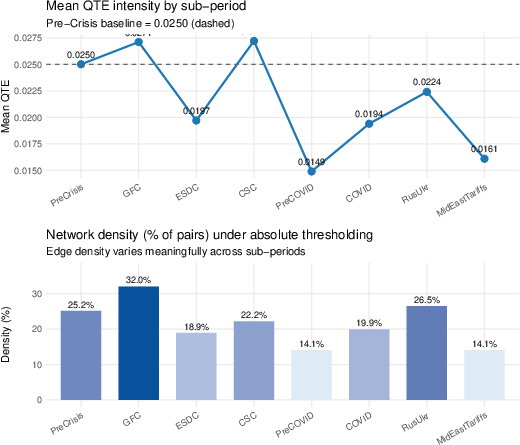

The WQTE detection architecture decomposes returns using the maximal-overlap discrete wavelet transform (MODWT) for translation invariance and cross-scale alignment. For each market pair, quantile-conditional transfer entropies (τ in {0.05,0.50,0.95}) are computed at each scale, detecting directional, tail-resolved propagation signals. An absolute threshold, calibrated on the Pre-Crisis baseline, selects significant transmission edges, guaranteeing comparability of detected network density across regimes.

Stage-1 results show marked temporal heterogeneity in contagion intensity and topology. Notably, network density peaks at 32% during the GFC and falls to 14% in more fragmented regimes, reflecting integration cycles in the cross-border system.

Figure 1: Stage-1 WQTE intensity and network density by sub-period, quantifying the regime-sensitive evolution of cross-border propagation structure.

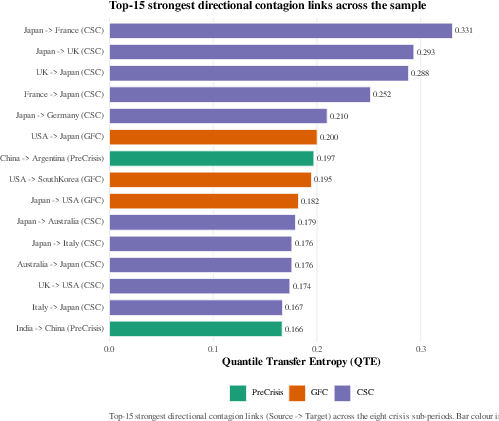

The strongest bilateral links are regime-specific, with the Japan→France connection during the Chinese Stock Crash reaching the largest WQTE magnitude.

Figure 2: Top-15 strongest bilateral contagion links by WQTE, highlighting temporal concentration of extreme cross-market transmission.

Stage 2: Multi-Method Structural Channel Attribution

The attribution stage operationalizes a sequence of identification strategies for each detected link:

- IV/2SLS with channel-specific lagged instruments and cross-channel cross-lags,

- LASSO-based sparse instrument selection to mitigate the many-instruments bias and allow for high-dimensional external-variation settings,

- Local projection (LP) impulse responses at h=1,5,22-day horizons for model-free dynamic effect estimation,

- Rigobon-style heteroskedasticity identification in Sargan-rejected windows,

- Cinelli-Hazlett robustness values to quantify sensitivity to omitted variable bias.

Bootstrap aggregation over significant links yields period-channel attribution shares and posterior uncertainty intervals.

Empirical Results

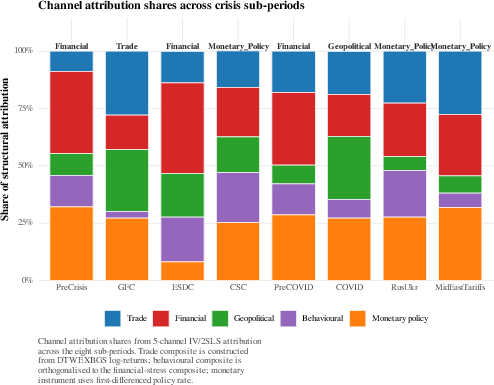

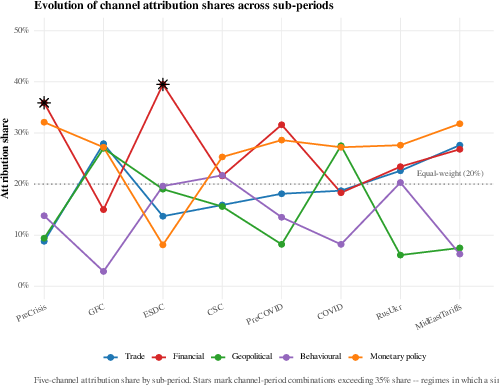

IV/2SLS attribution reveals that the dominant channel varies sharply across crises:

Identification robustness is assessed through cross-method comparison:

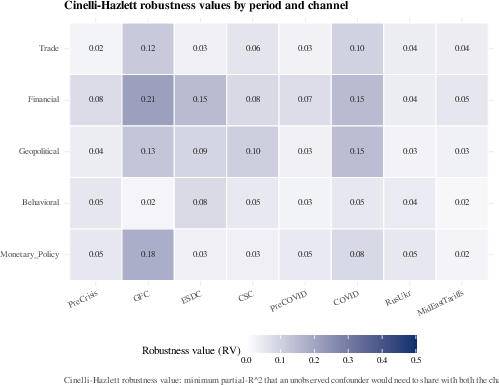

Rigorous sensitivity analysis using Cinelli-Hazlett ρ∗ shows high robustness for attribution shares in Financial during robust sub-periods and diminished robustness (lower ρ∗) in method-sensitive windows.

Figure 5: Cinelli-Hazlett robustness value ρ∗ per channel and sub-period; higher values denote greater immunity to unobserved confounding in mechanism attribution.

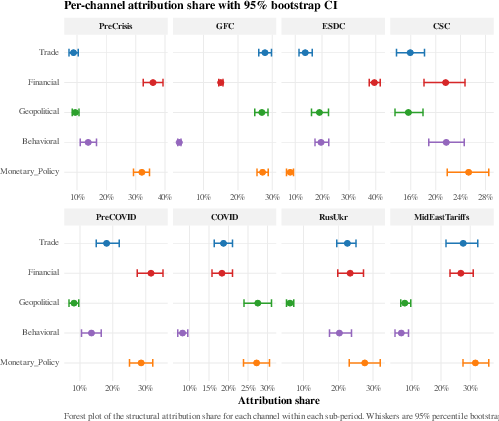

Bootstrap confidence intervals highlight the variance in identification precision across episodes and mechanisms.

Figure 6: Bootstrap 95% confidence intervals on channel-attribution shares by sub-period, quantifying statistical uncertainty in mechanism identification.

Network Role Decomposition

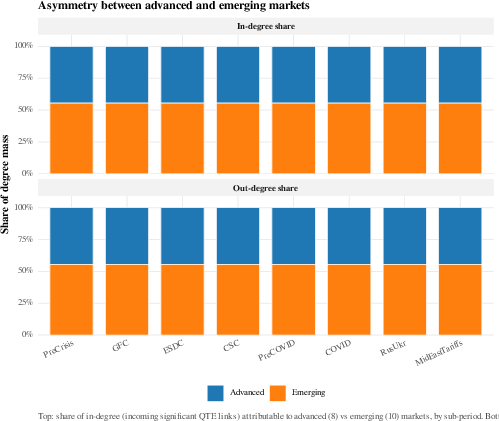

The role of advanced versus emerging markets is nontrivial and regime-dependent. During GFC and ESDC, developed markets account for a disproportionate share of origin (out-degree) in shock propagation; in the Chinese Stock Crash, Russia-Ukraine, and Mid-East/Tariffs, emerging markets are the principal transmitters.

Figure 7: Advanced- versus emerging-market in-degree (receiver) and out-degree (transmitter) per sub-period, elucidating the shifting core-periphery structure of contagion.

Implications and Prospects

This framework delivers a comprehensive, identification-disciplined template for the channel attribution problem in contagion diagnosis. The explicit disclosure of identification status and the reporting of posterior distribution across candidate dominant mechanisms in fragile windows create a higher evidentiary standard for informing policy. Notably, policy intervention—the deployment of macroprudential tools, capital controls, or trade insurance—should key off identification-robust episodes, and portfolio risk management should address mechanism ambiguity in fragile regimes.

Practically, the analytical apparatus can be extended to integrate mixed-frequency instrument sets, high-frequency narrative monetary shock indices, and LLM-extracted sentiment composites. Further, the construction offers a generalizable architecture for future work in systemic risk, international spillover analysis, and regime-specific mechanism estimation.

Conclusion

This study provides a two-stage, identification-transparent protocol for joint detection and channel decomposition of cross-border financial contagion using daily G20 equity markets over two decades. It achieves methodological novelty by combining quantile- and scale-resolved nonparametric detection with mutually disciplining, multi-method causal attribution and explicit robustness and status disclosure. The paper’s results redefine the evidentiary baseline for claims about transmission mechanisms in international crises, constraining the set of plausible dominant mechanisms with granular empirical evidence and rigorous identification diagnostics. This design sets a new expectation for future empirical contagion studies: that channel attribution must be methodologically layered, status-disclosed, and robust to model and instrument choice (2604.26546).