- The paper presents a novel hybrid approach combining neural networks with explicit Markov models to parameterize transition matrices based on observable features.

- It demonstrates that volatility-state conditioning improves both predictive accuracy and Markovian consistency compared to return-state models in equity market analysis.

- The explicit transition matrices enable classical operator diagnostics, offering greater inspectability and actionable insights for risk assessment.

Inspectable Neural Markov Models for Non-Stationary Time Series: A Technical Analysis

Hybrid Markov-Neural Framework for Sparse, Non-Stationary Regimes

This paper addresses the limitations of both conventional Markov models and neural architectures in non-stationary time series modeling, proposing a hybrid approach wherein a neural network parameterizes explicit Markov transition matrices conditioned on observable features. The innovation lies in encoding the Markov state on a discretized observable variable and using a neural network to learn the map from current context to the manifold of n×n stochastic matrices, thereby mitigating the collapse of frequency-based estimators at high discretization due to data sparsity.

The framework is validated in the context of equity markets, examining ten major US bank stocks over decades of data encompassing multiple market regimes. It offers a direct comparative assessment of how the choice of Markov state variable—return or realized volatility—influences both predictive quality and the internal consistency of the resulting Markov process.

State Space Design and Neural Matrix Parameterization

A critical methodological contribution is the flexible definition of Markov state space through high-resolution quantile binning, typically with N=35, $45$, or $55$ bins. The state variable Xt is instantiated either by discretized log returns or by realized volatility computed over diverse rolling windows, with the framework designed to efficiently handle the resulting N2 transition possibilities.

Rather than relying on empirical count estimators, a multi-layer perceptron (MLP) directly outputs the transition probability distribution for each starting state and feature context. This enables robust estimation in ultra-sparse regimes while preserving mathematical inspectability.

The explicit matrices produced are fully compatible with classical operator diagnostics (row entropy, Dobrushin coefficient, Chapman-Kolmogorov consistency), allowing for a degree of inference transparency unavailable in black-box sequence models.

Empirical Findings: Volatility-State Versus Return-State Conditioning

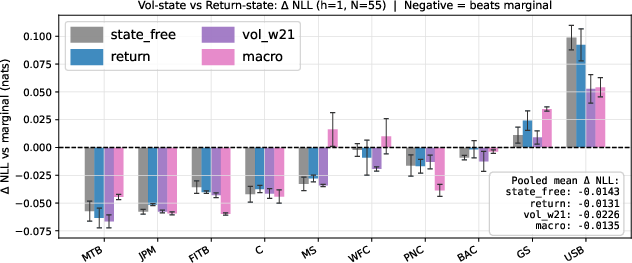

Across assets, volatility-state models (esp. with a 21-day window) consistently outperform return-state models and feature-only baselines by testing negative log-likelihood (NLL), with a pooled ΔNLL of −0.0226 (Figure 1). This advantage is most pronounced on short prediction horizons and holds for 9 out of 10 assets (Figure 2).

Figure 1: Per-asset ΔNLL versus the marginal baseline. Negative values indicate improved predictive accuracy; the volatility-state model achieves the strongest pooled performance.

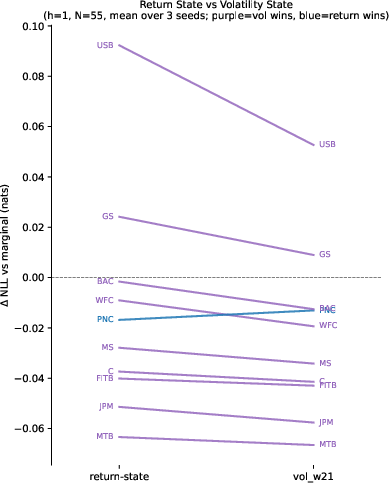

Figure 2: Paired ΔNLL comparison per asset, showing that volatility-state conditioning outperforms return-state conditioning in the majority of cases.

Notably, as the forecast horizon extends, the edge of volatility-state conditioning narrows, supporting the interpretation that realized volatility effectively encodes persistent regime information at short timescales, but that this advantage degrades when unobserved future regime changes occur within the prediction window.

Structural Self-Consistency and Markovianity

A central claim is that volatility-state conditioning produces a Markov structure that more closely aligns with the mathematical first-order Markov assumption, as measured by Chapman-Kolmogorov (CK) consistency. The CK discrepancy (mean KL divergence between direct and composed multi-step transitions) is reduced by N=350 for the volatility-state model versus the return-state model, with improvements in 8 of 10 assets—an outcome not paralleled by differences in the Dobrushin coefficient, which remains comparable across models.

This reduction in CK error quantitatively supports the thesis that realized volatility, due to its clustering and persistence, forms a more faithful summary statistic for regime-dependent dynamics than nearly uncorrelated returns.

Inspectability: Structural Diagnostics and Regime Interpretation

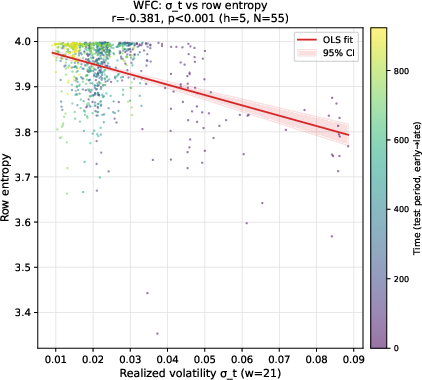

The explicit transition matrices enable novel geometric and statistical analyses indicative of market-wide regime behavior. Operator row entropy, a measure of predictive uncertainty conditioned on current state, exhibits a universally significant negative correlation with realized volatility (mean N=351, peaking at N=352), demonstrating that high-volatility periods homogenize transition matrices (Figure 3). Rows become less differentiated and concentrated, indicating that regime stress reduces the conditional informativeness of the current state.

Figure 3: Realized volatility (N=353) versus operator row entropy (N=354) for WFC, demonstrating that high volatility compresses and homogenizes predictive distributions.

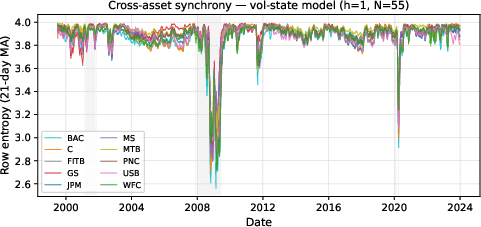

Cross-sectional analysis of row entropy time series across all assets reveals strong synchrony, particularly during systemic episodes such as recession periods, confirming the model's sensitivity to aggregate regime transitions and its ability to capture shared systemic risk exposures (Figure 4).

Figure 4: 21-day moving average of row entropy across all ten assets, showing coherent entropy dips during known systemic stress periods.

Theoretical and Practical Implications

The findings reinforce that the selection of Markov state variable is a substantive inductive bias with measurable impact on both predictive and structural fidelity. Conditioning on volatility moves the system closer to a truly Markovian process by embodying persistent regime information in the explicit state, rather than leaving that burden to be absorbed as non-Markovian effects in the operator itself.

From an operator-theoretic perspective, the inspectable nature of the learned matrices supports a suite of classical analyses, such as contraction rates and entropy dynamics, which are neither computable nor even conceptually defined for black-box sequence models or purely recurrent neural architectures. Thus, outputting an explicit stochastic matrix fundamentally broadens the class of testable scientific questions.

Pragmatically, the framework provides actionable diagnostics for model selection, risk assessment, and regime detection in portfolio management. By inspecting the explicit geometry of transition probability matrices, practitioners can identify periods of operator homogenization—interpreted as systemic stress or increased market coordination—and adjust risk models accordingly.

Limitations and Generalizability

While predictive lift over strong baselines is modest, this aligns with the weak predictability of daily returns in liquid equities. The observed structural enhancements and inspectability, not raw NLL gains, are the principal novelties. Moreover, generalization across asset classes and domains is theoretically straightforward where the state variable can be meaningfully discretized and exhibits serial dependence.

Limitations include the homogeneous asset pool (US bank equities), potential model sensitivity to state space discretization, and limited explanatory lift for certain idiosyncratic assets (e.g., USB at daily frequency).

Future Directions

Potential extensions encompass adaptive or learned Markov state representations, deployment in more heterogeneous multi-asset domains, and the integration of higher-order or latent state structures conditionally parameterized on explicit features. There is also clear scope for leveraging the inspectable operator approach in model-based RL and other settings requiring rigorous sequential uncertainty quantification with operator-level transparency.

Conclusion

This work demonstrates that neural parameterization of feature-conditioned Markov transition matrices allows for highly inspectable, structurally coherent modeling of non-stationary time series in sparse-data, high-resolution regimes. The explicit choice of state variable is revealed as a critical inductive bias, with realized volatility shown to more effectively Markovianize equity returns than the return itself. The approach produces competitive predictive performance, exposes internal model consistency via classical Markov diagnostics, and offers unique transparency into the evolution of systemic risk and uncertainty.

These attributes are broadly applicable to discrete-state, non-stationary time-series domains where interpretability and mathematical consistency of learned operators are essential.