- The paper develops a semi-parametric MS-SSM framework using spline and RKHS functions to capture nonlinear regime transitions.

- It employs a generalized EM algorithm that integrates forward-backward inference with penalized logistic regression for efficient nonparametric estimation.

- Empirical results on synthetic and financial data show improved regime detection, forecasting accuracy, and earlier risk identification.

Semi-Parametric State-Space Modeling for Nonlinear Regime Transitions

Time series exhibiting latent regime switching are classically modeled using Markov-switching state-space models (MS-SSMs), where the regime transition process is often parameterized through logistic or probit links on linear combinations of covariates. Such parametric forms induce a rigid structure, failing to capture the nonlinearity and complex covariate interactions that empirically drive regime transitions, particularly in financial domains where threshold and interaction-driven phenomena are prevalent.

This paper introduces a semi-parametric framework for MS-SSMs by modeling the transition probabilities as flexible functions drawn from either a spline basis or a reproducing kernel Hilbert space (RKHS). For a latent state st∈{0,1} and covariate vector xt−1∈Rp, the transition probabilities take the form: pjk,t=σ(fj(xt−1))

where σ(⋅) denotes the logistic function and fj∈H, with H being a nonparametric function space (RKHS or spline). This formulation directly generalizes parametric approaches, enabling the model to express threshold behaviors, nonlinear interactions, and complex transition surfaces without explicit manual specification.

Estimation: Generalized EM Algorithm

The paper develops a generalized EM algorithm for joint estimation of both emission and transition model components. The E-step follows the classical forward–backward algorithm to obtain the smoothed state and transition occupation probabilities. The M-step updates regime-specific VAR emission parameters by weighted least squares and, crucially, updates the nonparametric transition functions via penalized logistic regression. This is operationalized using IRLS for both splines and RKHS representations. Smoothing parameters are chosen by GCV or REML.

Identifiability and consistency under the semi-parametric specification are established, building on generic HMM identification theory. In the RKHS setting, consistency rates for the transition function estimator match known nonparametric regression rates, with variance-bias tradeoff explicitly favoring semi-parametric modeling when the true transition dynamics are nonlinear.

Empirical Results: Synthetic and Financial Applications

Extensive simulation experiments were designed to directly challenge the modeling flexibility by generating data with genuinely nonlinear and interaction-rich transition probabilities unrepresentable by any linear form. Across 100 replications, both spline and RKHS-based semi-parametric models substantially outperformed standard logit/probit MS-SSMs in terms of out-of-sample log-likelihood, regime classification accuracy, and accuracy of transition onset timing.

Empirical application to a high-dimensional multivariate financial time series—comprising equity and commodity flows, VIX, and sentiment—demonstrated the benefits of the approach. The semi-parametric model, when evaluated against expert-annotated regime labels, delivered improved test log-likelihood (8–10% relative gains) and higher regime assignment accuracy. Notably, the method detected regime transitions earlier and more precisely, reflecting superior sensitivity to nonlinear, joint-tail risk mechanisms.

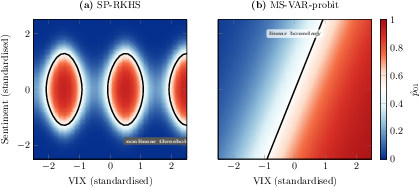

As revealed by transition surface visualizations for the risk-on-to-risk-off switching probability (see below), the semi-parametric model uncovers a pronounced threshold effect: transitions become probable only when both implied volatility and negative sentiment are simultaneously extreme—a joint-tail region that parametric models systematically underestimate.

Figure 1: Estimated risk-off transition probabilities as a function of VIX and investor sentiment. Only the semi-parametric model recovers the joint-tail threshold behavior.

Theoretical Implications and Methodological Extensions

The semi-parametric MS-SSM bridges classical statistical regime-switching models with modern nonparametric estimation, preserving full probabilistic state-space interpretation and the statistical efficiency of the forward–backward inference. Modularity is emphasized: the nonparametric estimator in the M-step can be replaced with more complex machinery (e.g., deep kernel methods or additive models), making the framework extensible to high-dimensional covariate spaces via structural regularization.

Identifiability is protected under mild separation and regularity assumptions, and convergence guarantees are maintained for the generalized EM implementation. Model selection for the number of regimes remains nontrivial in semi-parametric settings due to the ambiguity of degrees of freedom, suggesting a need for refined model complexity penalties.

Computationally, the dominant cost arises from the nonparametric logistic regression step; efficient low-rank approximations (e.g., Nyström methods) make the approach practical up to moderate time series lengths.

Practical Implications and Future Directions

Practically, this method enhances the ability to identify impending regime shifts in domains where transition determinants are nonlinear and complex, offering earlier warnings and more precise characterization—crucial for financial risk management, macroeconomic monitoring, and other applications with latent structural shifts. Its modular design enables rapid incorporation of emerging regression technologies and structural modeling assumptions.

Theoretically, this approach strengthens the connection between probabilistic time series modeling and flexible function approximation, opening possibilities for systematic study of latent dynamical processes governed by unknown nonlinearities. For high-dimensional regimes or covariates, additive generalizations and sparsity-inducing penalties offer promising directions, as do deep-hybrid transition functions within the EM framework.

Conclusion

This work advances MS-SSMs by endowing regime transition modeling with a nonparametric and highly flexible structure, estimated efficiently and with formal theoretical underpinnings. Empirical results confirm that such flexibility is both necessary and effective for accurate regime discovery and transition forecasting in complex, real-world time series, particularly where interaction and threshold effects dominate. The framework anticipates further methodological innovation by providing a principled template for nonparametric or deep transition modeling within the probabilistic state-space paradigm.