- The paper introduces a two-stage Diffusion-Copula model that decouples marginal and dependence estimation for superior tail-risk calibration.

- It employs Mixture Density Networks for heavy-tailed marginal modeling and Classification-Diffusion Copulas to capture asymmetric inter-asset dependencies.

- Empirical analyses on cryptocurrency markets demonstrate enhanced prediction of joint tail events and systemic risk compared to traditional diffusion models.

Probabilistic Multivariate Time Series Forecasting with Diffusion Copulas

Motivation and Background

Estimation of joint risk in high-dimensional financial time series—particularly capturing both marginal asset volatility and asymmetric dependence structures among assets under extreme conditions—remains a critical but unresolved problem in quantitative finance. Traditional copula-based approaches, while flexible in separating marginal and dependence modeling, often fail in the tails due to rigid parametric families and implicit independence assumptions that break down during systemic events. Recent deep diffusion models have succeeded in generative modeling of complex multivariate distributions; however, end-to-end diffusion approaches suffer from "normality bias," sacrificing marginal calibration for joint coherence and underestimating tail risk.

This work introduces a hierarchical modeling paradigm—Diffusion-Copula—which addresses the above failings by explicitly decoupling the learning of marginal distributions from dependence structure learning. Marginals are handled by Mixture Density Networks (MDNs) optimized for heavy tails, while inter-asset dependence is parameterized as a Classification-Diffusion Copula (CDC). This two-stage approach directly targets systemic tail risk and is empirically validated on turbulent cryptocurrency markets.

Methodological Framework

Marginal Modeling with Mixture Density Networks

The framework first independently estimates the conditional distribution of each time series asset with an MDN. Each MDN predicts a convex combination of Normal, Laplace, and Student-t components, with parameters (mean, scale, degrees of freedom) driven by an LSTM network applied to a 14-lag Markovian window with engineered volatility and path features. This configuration allows for precise, asset-wise calibration of volatility clusters, skewness, multimodality, and, critically, heavy-tailed risk.

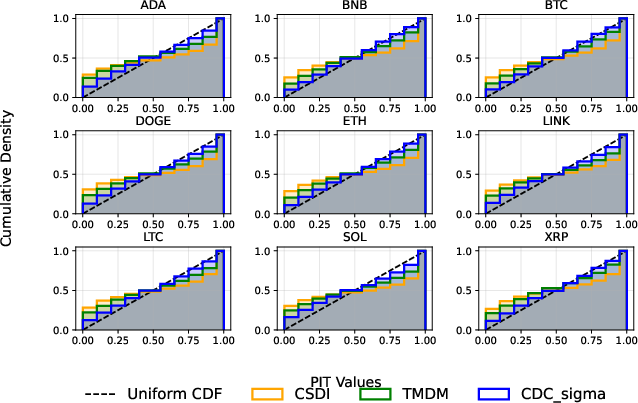

Figure 1: Marginal calibration curves show the CDC model closely matches the ideal (diagonal), indicating robust marginal fit especially in the tails.

Dependence Modeling with Classification-Diffusion Copulas

Marginal CDFs are used to transform returns to the uniform copula scale via the PIT; dependence modeling is then performed with a CDC. Each copula sample is mapped to Gaussian latent space, and a forward Ornstein-Uhlenbeck (OU) process is used to destroy dependence. A neural network classifier is trained to distinguish time steps along the diffusion process, and the copula density is defined as a density ratio derived from classifier outputs. The CDC parametrization is highly flexible: it does not assume any fixed parametric structure, enabling it to recover nonlinear and asymmetric joint tail dependencies observed in empirical market data.

Joint Sampling and Generation

Forecasting a joint trajectory involves: (1) sampling dependence structure from the CDC using Langevin dynamics in Gaussian space, (2) applying the inverse Gaussian CDF to recover copula samples, and (3) inverting the MDN marginals to obtain asset returns.

Empirical Evaluation

Benchmarking is conducted against two leading score-based diffusion baselines: Conditional Score-based Diffusion Model (CSDI) and Transformer-Modulated Diffusion Model (TMDM). Multiple diagnostics are considered, including marginal PIT/QQ diagnostics, dependence structure error in the tails, and "Black Swan" event detection.

Marginal Tail Calibration

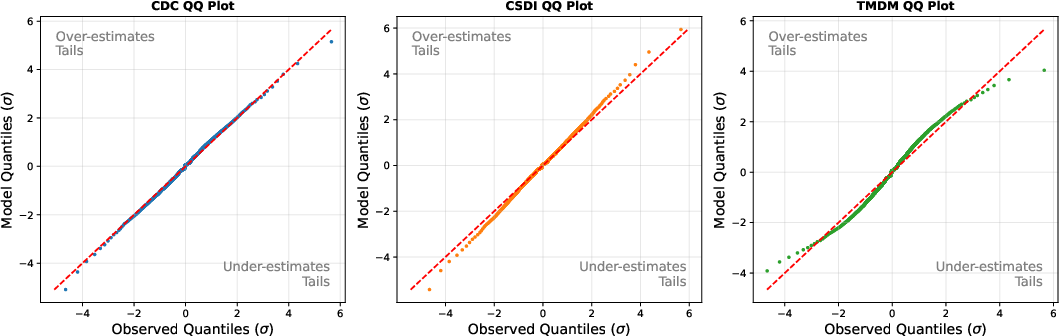

The CDC-based model demonstrates sharp calibration on marginal PIT (Figure 1) and QQ axes (Figure 2), accurately matching empirical quantiles even in extreme regions. Joint models (CSDI, TMDM) systematically underestimate tail probability, leading to mischaracterization of rare events.

Figure 2: QQ diagnostics indicate the CDC model aligns closely with the empirical quantiles, while CSDI/TMDM show “S-shaped” deviations and tail underestimation.

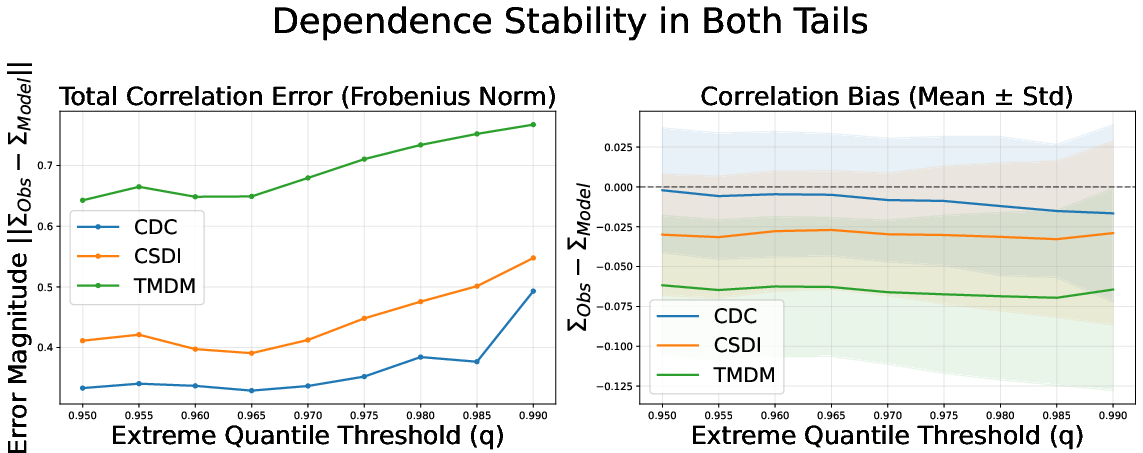

Dependence and Systemic Risk

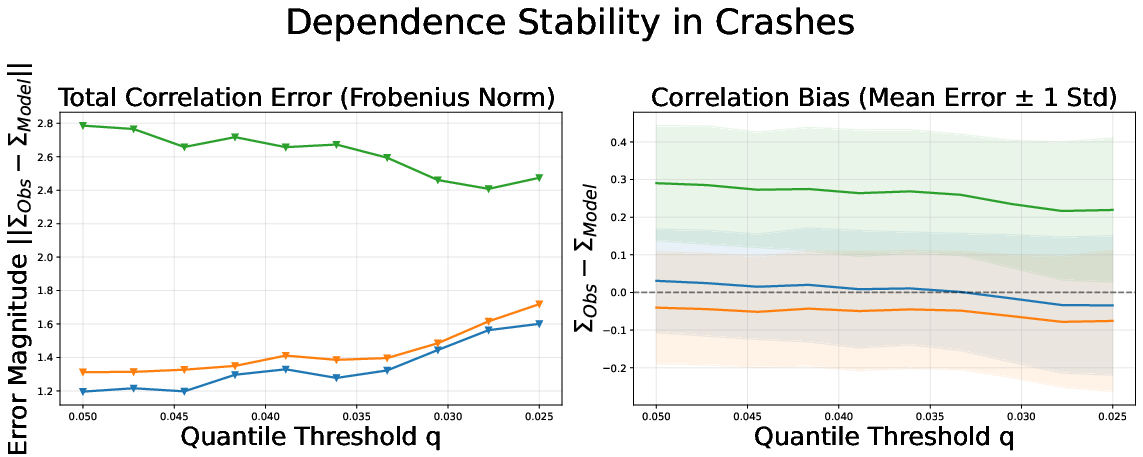

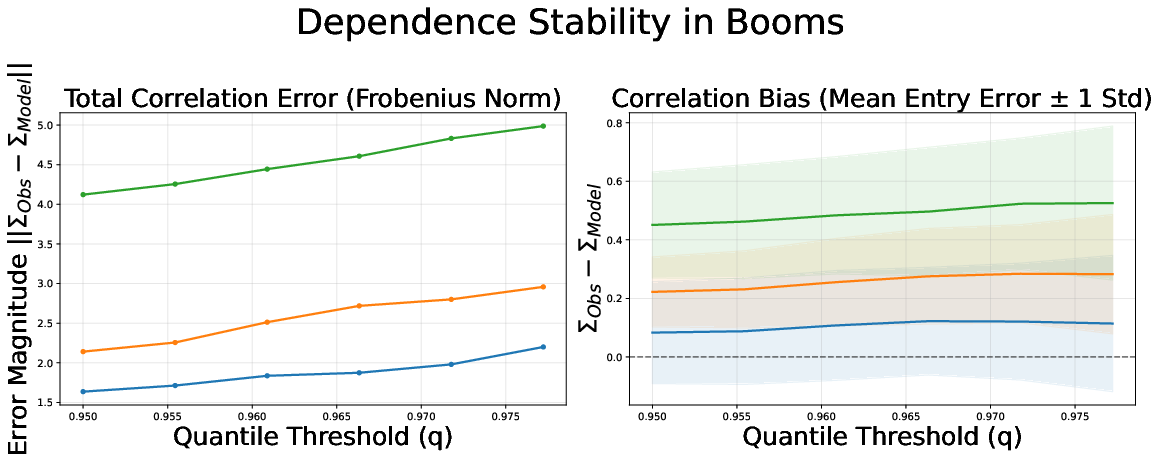

Evaluation of estimated correlation structure at increasing levels of joint tail events reveals that CDC preserves accurate correlation as quantile thresholds become more extreme, while CSDI overestimates and TMDM fails to capture co-movement during distress (Figure 3).

Figure 3: Correlation matrix errors show stability for CDC as the threshold deepens; joint diffusion models deviate, highlighting unreliable tail dependence.

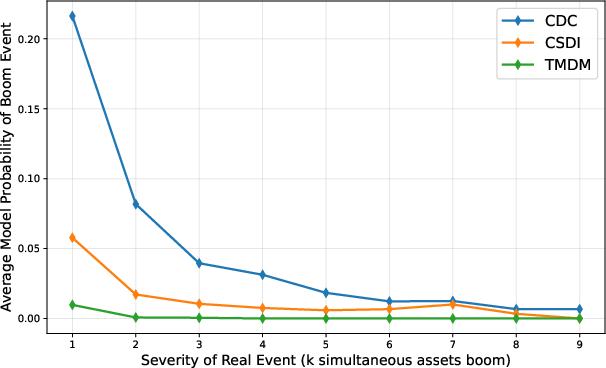

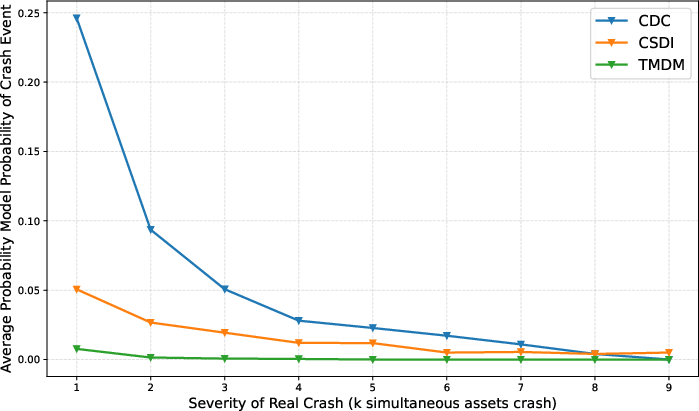

Probability of Simultaneous Extremes

When assessing the probability assigned to observing simultaneous extremes involving increasing numbers of assets, baseline models rapidly assign negligible probability, classifying observed systemic events as "statistically impossible" (Figure 4). The CDC model, in contrast, maintains non-trivial mass across the range, reflecting an ability to anticipate contagion phenomena consistent with financial crises.

Figure 4: The CDC model alone avoids vanishing probability for high-order joint extremes, matching empirical systemic event frequencies.

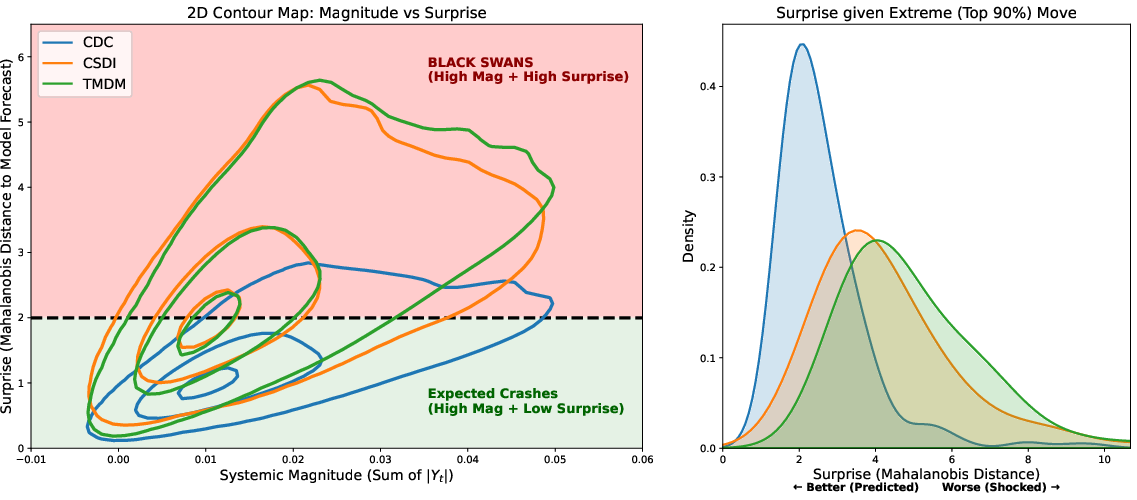

Black Swan Versus Expected Crash Separation

A two-dimensional analysis (event magnitude versus model surprise) illustrates that the CDC is unique in forecasting high-magnitude joint moves as expected, low-surprise events (Figure 5). Baselines produce high Mahalanobis distances for these events, misclassifying them as Black Swans—showing their inability to model realistic joint market stress scenarios.

Figure 5: The CDC's probability contours differ sharply from joint diffusions, which lie in the “Black Swan” zone for high-magnitude events, while CDC classifies these as ordinary tail risk.

Implications and Future Directions

This work demonstrates that generative diffusion-based modeling benefits from explicit architectural separation of marginal and dependence learning when applied to multivariate time series. The CDC approach achieves simultaneous superior marginal calibration and precise modeling of correlation spikes during market crashes—capabilities not present in current end-to-end diffusion models. Such decomposable frameworks naturally extend to stress testing, risk aggregation, and robust Expected Shortfall estimation in high-dimensional markets. Furthermore, the two-stage paradigm may be enhanced by adopting more flexible, model-free marginals (e.g., flow-based models) and investigating alternative dependence architectures tailored to high-dimensional, multi-modal tail dependence.

From a theoretical standpoint, this approach supports further development of hierarchical, modular generative models that mirror the stochastic structure of real-world multivariate systems. Practically, these advances enable robust synthetic scenario generation and portfolio construction strategies that account for cross-asset contagion, a central concern in risk engineering and regulatory practice.

Conclusion

By decoupling marginal and dependence modeling, the CDC framework marks a robust advance in probabilistic multivariate time series forecasting. Results indicate that it provides calibrated tail-risk forecasting and consistent joint event modeling, overcoming the limitations of prior diffusion- and copula-based methods. The approach is particularly relevant for dynamic, high-volatility markets where tail contamination and joint extremes dominate risk considerations. Further research into nonparametric marginals and scalable dependence flows presents an open path towards universal, interpretable generative risk models for next-generation financial analytics.