- The paper introduces a high-dimensional copula framework that separates dependence dynamics into principal spectral components using regularized score-driven updates.

- It demonstrates via simulations and empirical tests that non-linear spectral shrinkage effectively debiases eigenvalue estimates, improving out-of-sample performance.

- The approach enhances interpretability and systemic risk assessment by capturing both market-wide and sector-specific dependence without restrictive clustering.

Spectral Dynamics and Regularization in High-Dimensional Copula Modeling

Introduction

This paper introduces a high-dimensional copula framework that unifies spectral dynamics and non-linear regularization for modeling time-varying, asymmetric, tail-dependent dependence structures in large dimensions (2601.13281). The approach targets challenges inherent in multivariate financial data: pronounced time-variation, asymmetry, tail-dependence of returns, and the explosive parameterization and biased estimation endemic to high-dimensional covariance and copula matrices. Unlike competing methods reliant on cluster allocations or restrictive factor structures, this model leverages the spectral decomposition of the dependence matrix, applies regularized score-driven dynamics to the dominant eigenvalues, and shrinks the biased, small-sample spectrum to achieve parsimony, computational tractability, and robust out-of-sample performance.

Spectral Copula Parameterization and Dynamics

The core innovation is the separation of dependence dynamics into principal spectral components. The copula dependence matrix is constructed as

Rt=diag(WΛtW′)−1/2WΛtW′diag(WΛtW′)−1/2,

where W is orthogonal, and Λt is a diagonal matrix with strictly positive, time-varying eigenvalues. Score-driven dynamics are imposed on a parsimoniously selected subset of these eigenvalues,

ηt+1=ω+Bηt+Ast,

where st is the scaled score of the copula log-likelihood with respect to log-eigenvalues, yielding analytic and tractable updates. This framework extends prior score-driven GARCH models, crucially applying the dynamics within the copula (dependence) rather than the marginal time series. Model selection procedures (BIC-driven) identify the minimal number of dynamic eigenvalues required to explain dependence dynamics.

Non-linear Spectral Shrinkage

Large d induces substantial bias in the sample eigenvalues, deteriorating the estimated spectrum, in particular for non-dominant directions. To resolve this, the unconditional spectrum is regularized using non-linear quadratic shrinkage as developed in [Ledoit & Wolf, 2022]. This mapping produces debiased spectral intercepts,

λ~i=fQS(λ^i),

which improves both in-sample and out-of-sample likelihood, especially for smaller eigenvalues, as further demonstrated empirically and in simulation. The model thus combines regularization for static components with explicitly dynamic modeling for dominant directions.

Simulation Evidence

Two simulation experiments evaluate the method against clustered factor copulas and direct sample-based maximum likelihood.

1. Copula Structure Robustness: When the data generating process (dgp) is consistent with a group-based factor structure, cluster copulas show optimal out-of-sample log-likelihood. However, as the true correlation matrix deviates from strict block structure—reflecting heterogeneous group and cross-group effects—the spectral copula with regularization clearly dominates in out-of-sample performance. The regularized approach robustly captures both dominant and residual dependence, while clustering approaches exhibit rigidities and suboptimal fit under model misspecification.

2. Parameter and Path Recovery: Regularized maximum likelihood achieves unbiased estimation of large and small eigenvalues, while sample-based estimation greatly underestimates small eigenvalues. Model selection reliably identifies the true number of dynamic components, and pathwise estimation reliably tracks latent spectral volatility dynamics. Excess parameterization is not penalized in out-of-sample likelihood, but BIC appropriately selects parsimonious, well-calibrated models.

Empirical Results: Large-Scale Financial Dependence

The methodology is empirically validated on a panel of 100 European equities spanning 10 industries and countries over a decade. Standard AR-GARCH filtering is applied for marginal pre-processing. Empirical ACFs of spectral projections (as opposed to ordinary returns or copula PITs) show clear volatility clustering in the leading components, motivating the spectral dynamic copula approach.

Key empirical results:

- Allowing dynamics in the top two eigenvalues yields substantial in- and out-of-sample log-likelihood gains. Additional dynamic eigenvalues confer negligible benefit.

- Regularized spectral copulas with score-driven dynamics outperform both sample-based spectral copulas and cluster-based factor copulas.

- The introduction of tail dependence (Student's t and skewed t copulas) produces marked increases in fit, but skewness effects are less material relative to Gaussian versus t shifts.

- Out-of-sample log-likelihood increases by over 1000 when regularization is applied—dominated by corrections at the low end of the spectrum.

Interpretation of Spectral Components

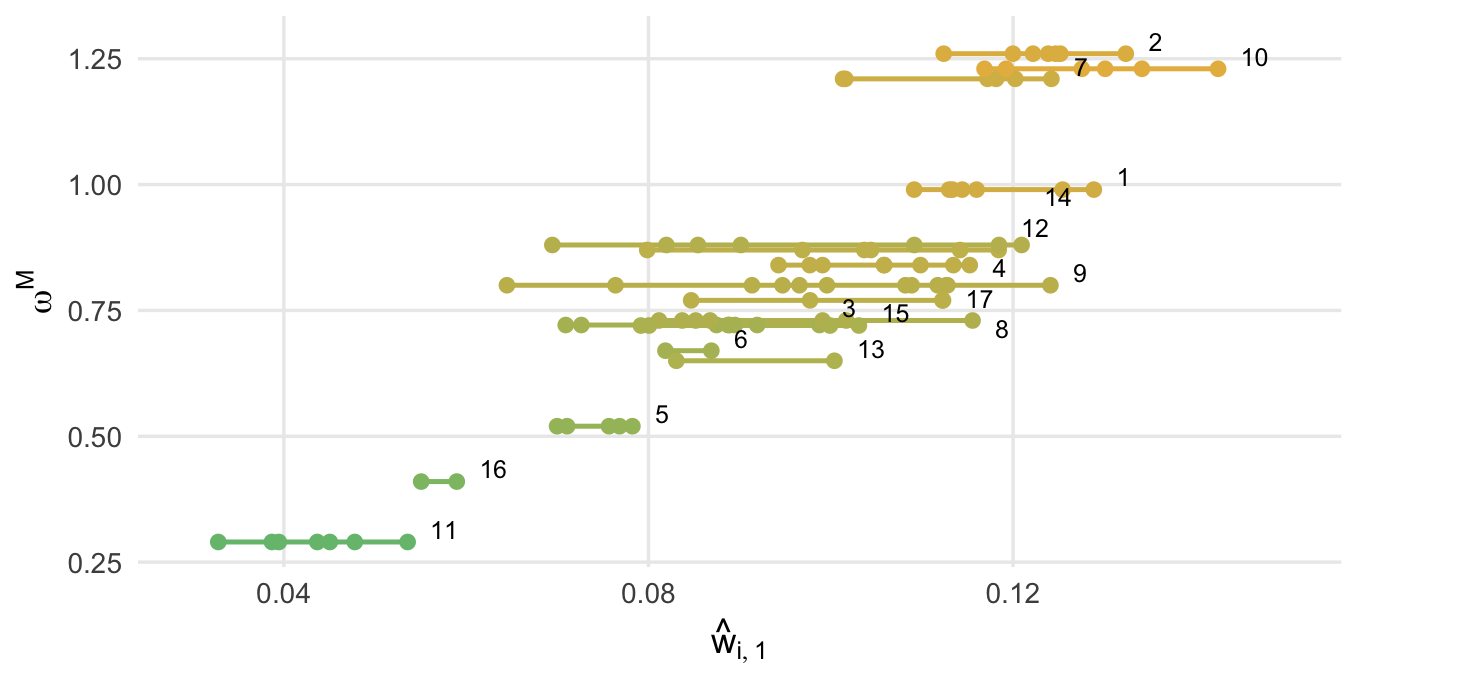

The first estimated eigenvector is nearly uniform across all assets, representing parallel (market-wide) comovement; its associated eigenvalue strongly increases in crisis episodes (flash crash, Brexit, COVID-19), indicating jumps in systemic risk and sharp contractions in diversification potential.

Figure 2: ωM versus first spectral eigenvector w^i,1—visualizing the alignment between cluster-based market factors and spectral copula loadings.

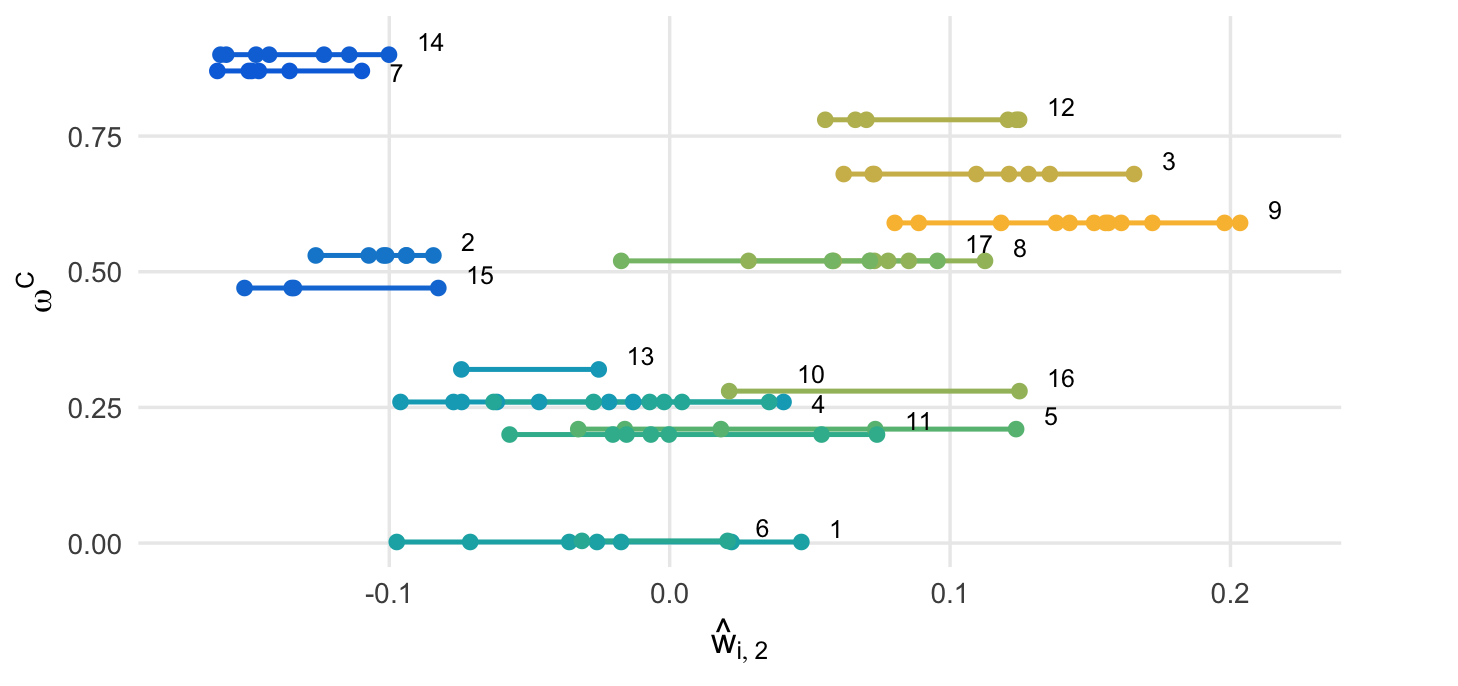

Heatmaps for the second eigenvector reveal sectoral and national structure, with signs and magnitudes correlating closely with clusters identified by the factor copula model. However, the spectral approach does not impose block-diagonality, thus capturing non-trivial cross-cluster dependencies absent from factor models.

Figure 4: Heatmap of estimated eigenvector weights w^, illustrating the sectoral and national organization of dependence structure.

Analysis of the effect of shrinkage demonstrates that the bulk of likelihood improvement derives from correcting severely downward-biased small sample eigenvalues—such corrections are inaccessible to unregularized approaches.

Practical and Theoretical Implications

This work brings several advances:

- It provides a scalable and flexible framework for high-dimensional, dynamic copula modeling adaptable to heterogeneously structured financial panels.

- The inclusion of regularized spectral shrinkage resolves longstanding high-dimensional bias issues without sacrificing rich dynamic structure in the dominant comovement directions.

- By avoiding group clustering and restrictive factor loading constraints, the approach achieves greater out-of-sample stability under model misspecification and in highly heterogeneous data settings.

- The interpretability of spectral dynamics facilitates systemic risk assessment and stress testing, as market events manifest directly in the dynamics of the leading eigenvalue.

The approach is readily extensible. Potential directions include further dimension reduction, alternative shrinkage functions, application to non-financial domains, and the integration with alternative marginal filtering regimes. For practitioners involved in portfolio construction, systemic risk monitoring, or regulatory stress testing, the regularized spectral copula methodology offers both enhanced performance and diagnostic interpretability.

Conclusion

Spectral dynamics and non-linear regularization in copula models represent a robust, computationally efficient solution to modeling high-dimensional dependence with time-varying, heavy-tailed, and asymmetric features. The model attains strong empirical and simulation-based accuracy and interpretability, outperforming cluster-based alternatives especially in heterogeneous and non-block-structured dependence scenarios. Regularization is critical at the low spectrum, while dynamic modeling of the leading eigenvalues enables accurate systemic risk and comovement monitoring. This framework sets a new standard for high-dimensional dependence modeling in finance and allied fields.