- The paper demonstrates that quantum models, specifically QLSTM and QRC, can outperform classical architectures in multivariate financial forecasting.

- It applies advanced quantum circuits with amplitude encoding and variational gates to capture complex, cross-series dependencies.

- Empirical results reveal lower RMSE in multivariate settings, highlighting the potential of quantum recurrence as an expressive feature extractor.

Quantum LSTM and Quantum Reservoir Computing for Financial Time Series: Comparative Analysis and Empirical Evidence

Introduction

This paper presents a systematic, parameter-matched benchmark of quantum and classical sequence models—specifically Quantum Long Short-Term Memory (QLSTM) and Quantum Reservoir Computing (QRC) versus classical LSTM and Reservoir Computing (RC)—on real and synthetic financial time series (2605.02656). The study addresses challenges intrinsic to financial series, including non-stationarity, heavy tails, and cross-asset dependencies, by leveraging both quantum and classical recurrent neural architectures. The core contribution is a rigorous, data-driven comparison of quantum and classical models, emphasizing lagged input structures, amplitude encoding, and hybrid quantum-classical pipelines, covering both univariate and multivariate prediction regimes.

Data Construction and Preprocessing

The analysis utilizes monthly revenue series for 20 products, each with approximately 8 years of history. Due to the brevity of each series, synthetic extensions are generated using product-wise Gaussian Process (GP) models with additive kernels (trend, periodic, rational quadratic, Matérn) and two-state Hidden Markov Models (HMMs) on the residuals to capture level shifts. Data is split into training and testing partitions (60 and 36 months, respectively) and subjected to log transformation and standardization to improve model regularity and numerical conditioning.

Forecasting tasks are formalized via supervised lag embeddings: for univariate settings, feature vectors are constructed from successive lags; for the multivariate regime, lagged vectors from multiple correlated series are concatenated, enriching the input space and enabling models to leverage cross-series dependencies.

Quantum and Classical Model Architectures

Quantum LSTM

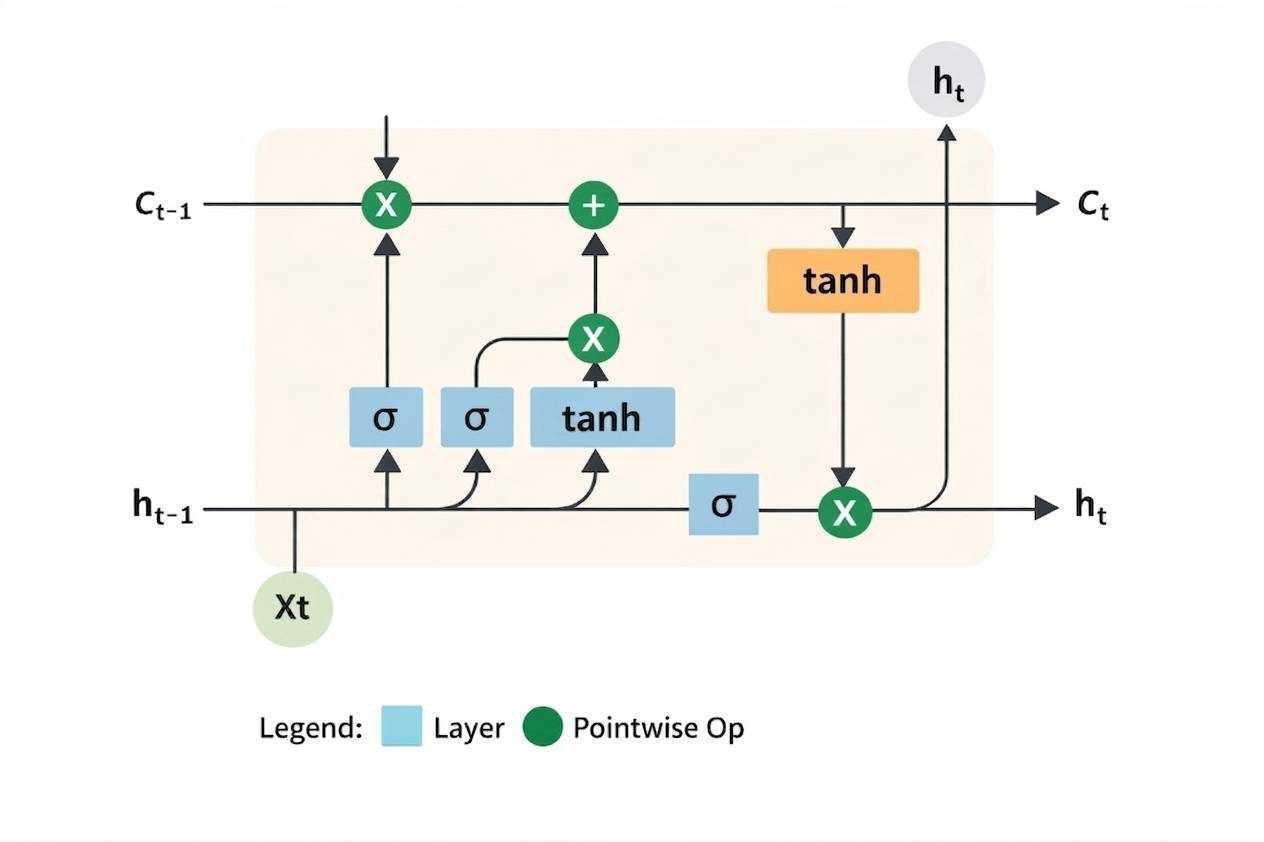

QLSTM emulates core LSTM gating (input, forget, candidate, output) using parameterized quantum circuits (VQCs) to process amplitude-encoded lag vectors. The circuit design (Figure 1) integrates amplitude encoding (using Q-Alchemy's state-preparation circuits), variational layers (parameterized by RX, RY, RZ gates and CNOT entanglement), and classical optimizers for gradient-based training.

Figure 1: Comparison between classical LSTM and QLSTM with VQCs.

Layer-wise, the QLSTM replaces each LSTM affine-gated unit with a quantum circuit, followed by non-linear activations akin to their classical counterparts. Classical and quantum cell states and hidden states evolve identically, enabling direct comparison at equivalent parameter budgets.

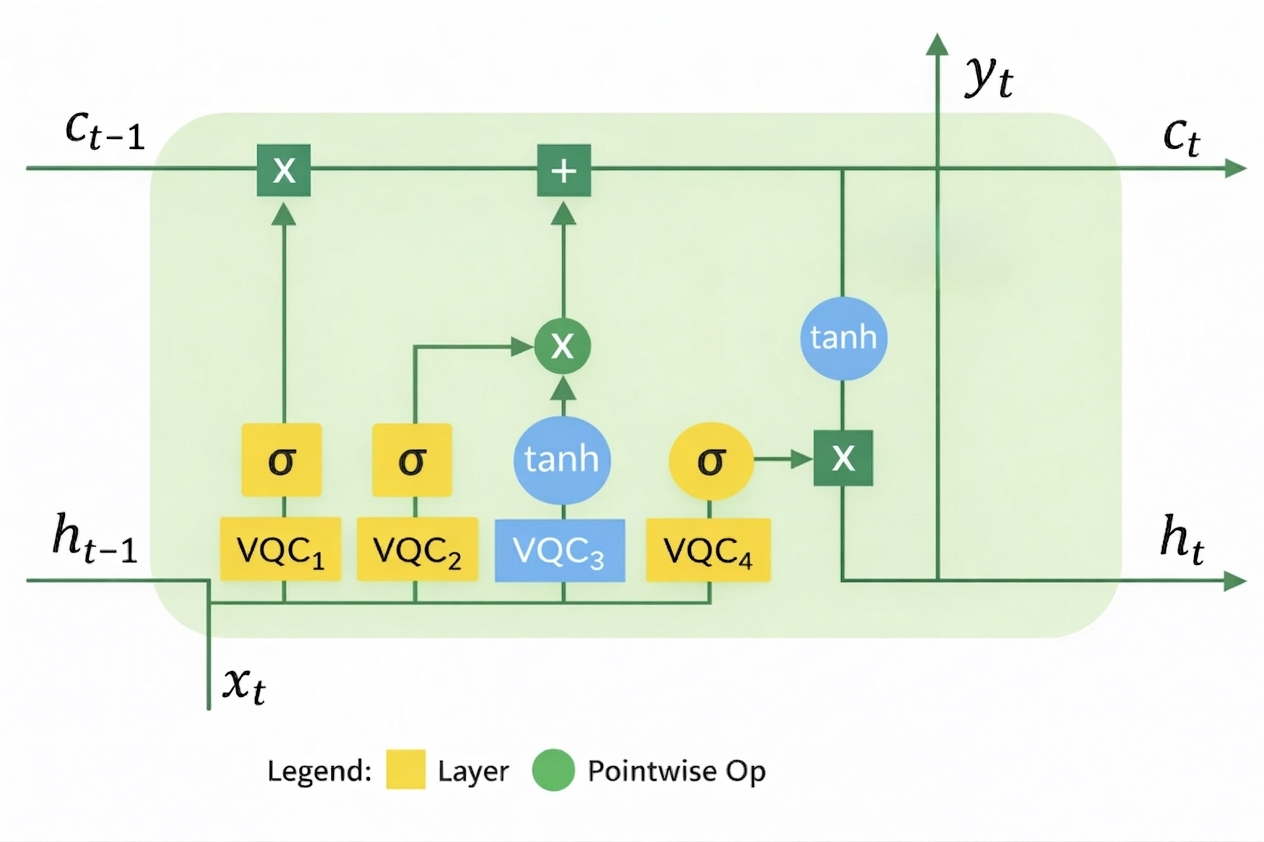

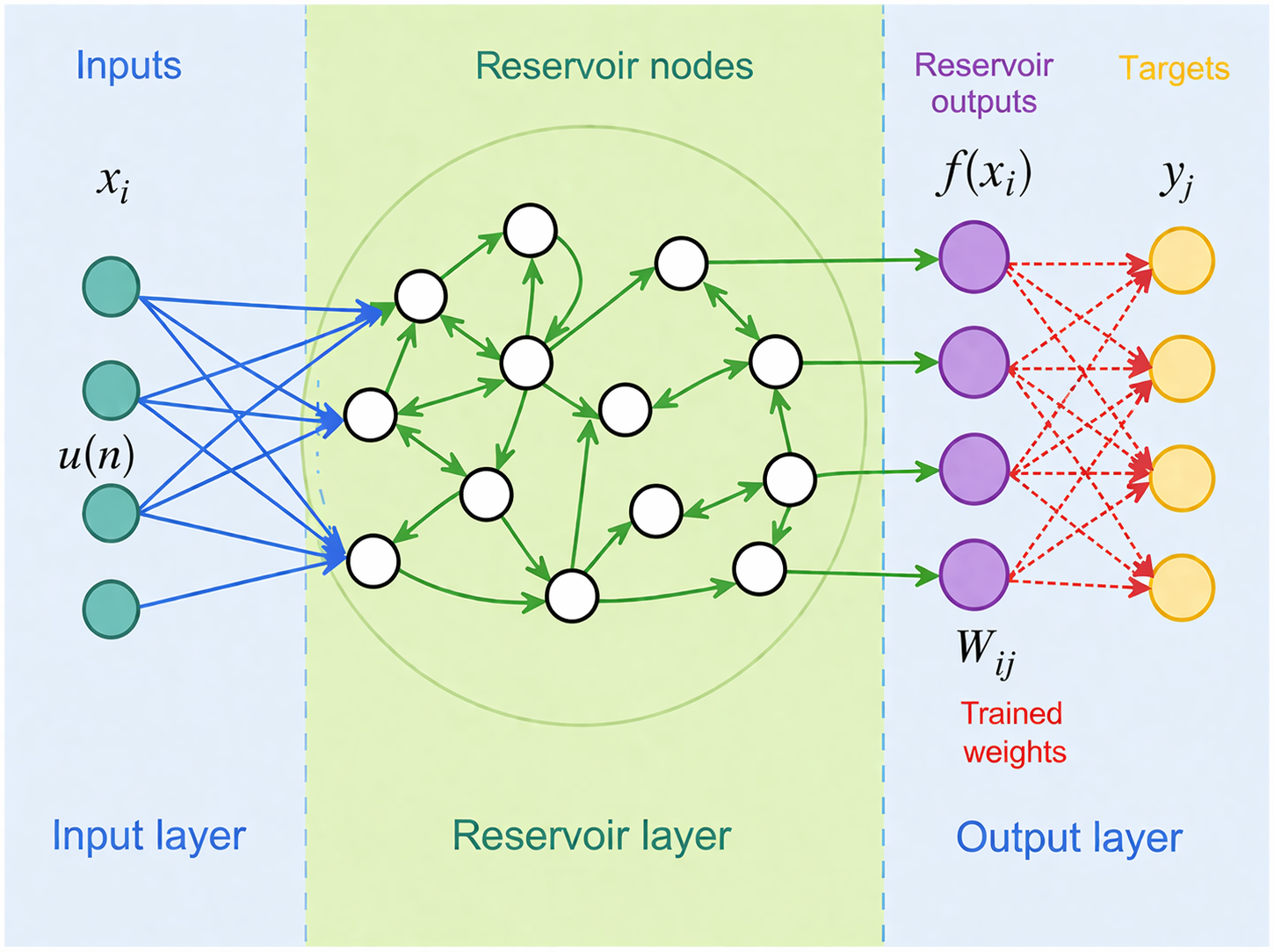

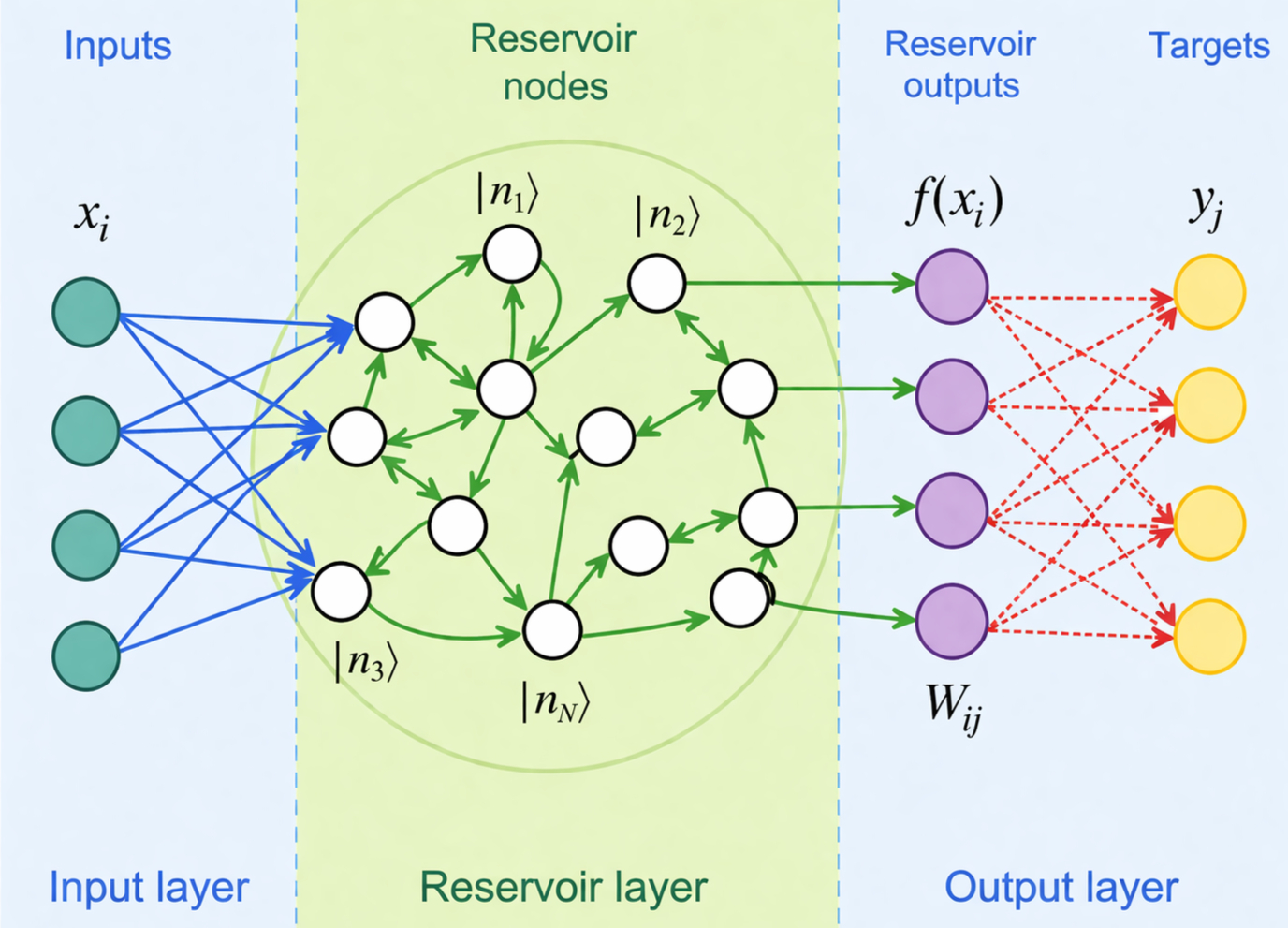

Quantum Reservoir Computing

QRC leverages fixed, random quantum circuits as reservoirs (Figure 2). Inputs—after normalization and (for multivariate data) random projection—are amplitude encoded into n-qubit states. Quantum circuits (parameterized by random rotations and ring CNOT interactions) evolve these states, and each qubit is measured along X, Y, and Z axes, concatenating outcomes as high-dimensional feature vectors for a classical readout.

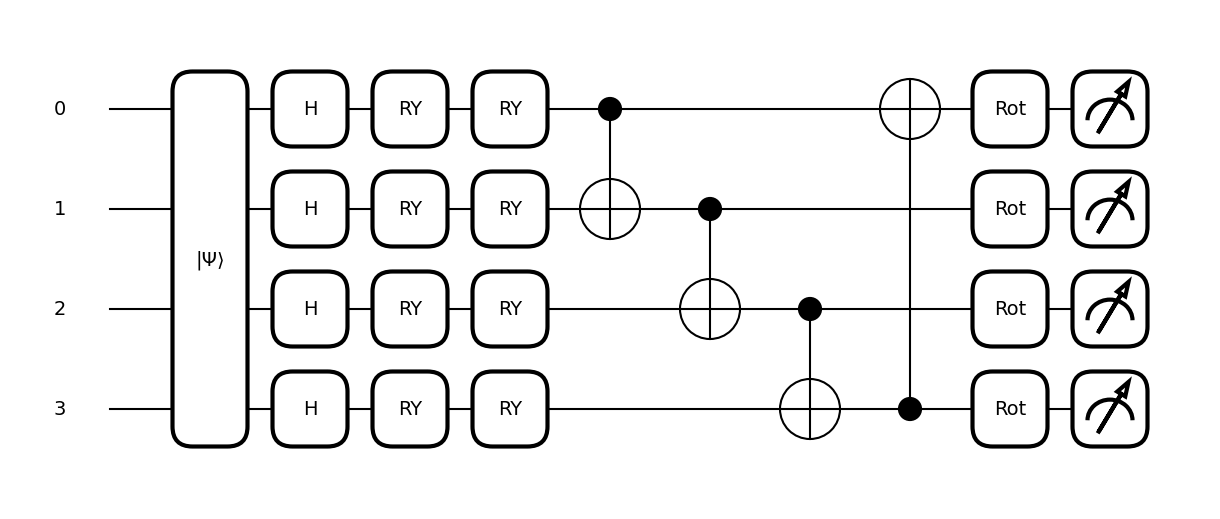

Figure 3: Variational quantum classifier (a) Layer structure, (b) Full classifier schematic as used within quantum models.

Figure 2: Comparison between classical RC and QRC architectures, demonstrating the pipeline and corresponding layers.

Only the readout layer is trained, akin to classical RC. The method preserves the non-adaptive, high-dimensional nonlinear transformation property fundamental to RC but exploits quantum state evolution for potentially superior expressivity.

Classical Baselines

- LSTM: Standard LSTM with identical lag embedding and network size as the QLSTM baseline; trained via backpropagation-through-time.

- Reservoir Computing: Randomized dynamical systems with linear or neural readouts, parameter-matched to QRC.

Experimental Setup

Models are implemented with PyTorch, scikit-learn, PennyLane, and Q-Alchemy. All quantum models employ amplitude encoding for n qubits (selecting n according to input dimensionality and hardware constraints). The data is split 80-20 for training and testing to measure both in-sample and generalization performance.

Empirical Results

Loss Dynamics and Predictive Accuracy

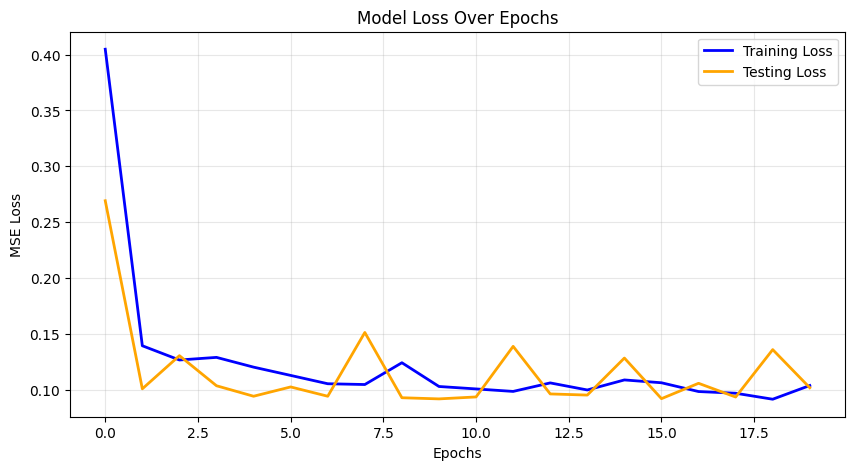

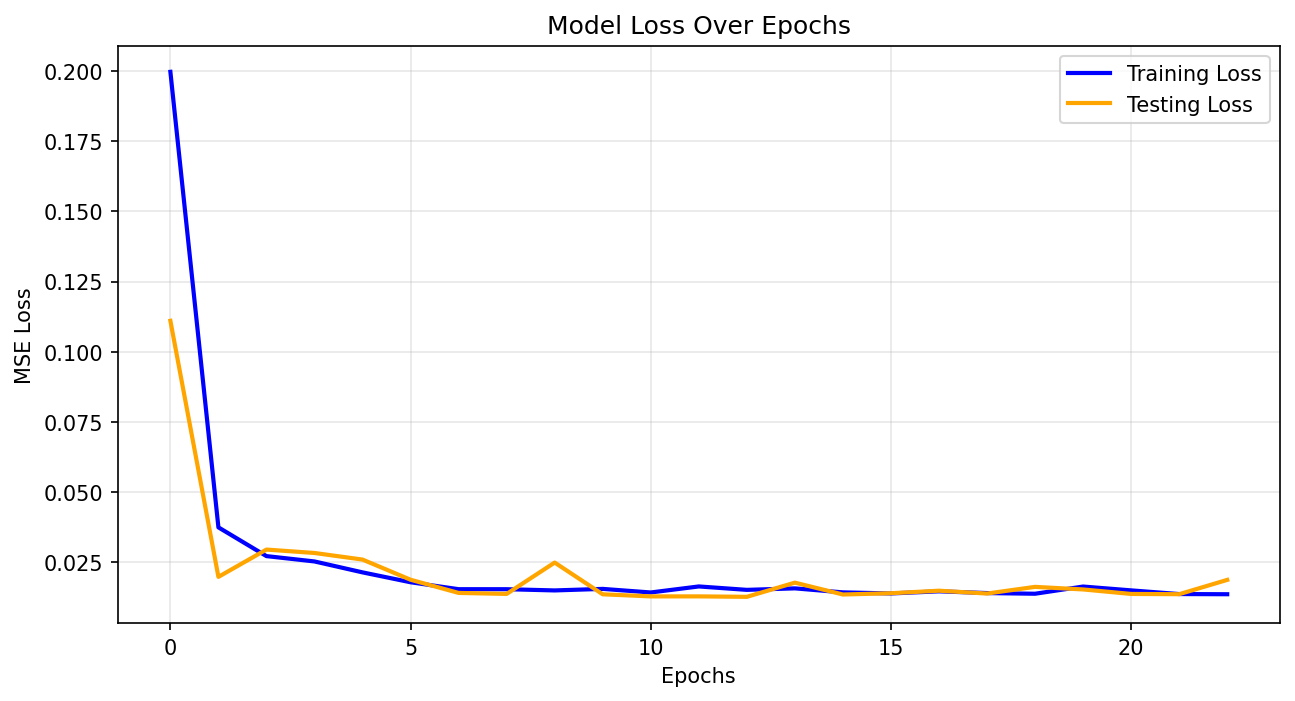

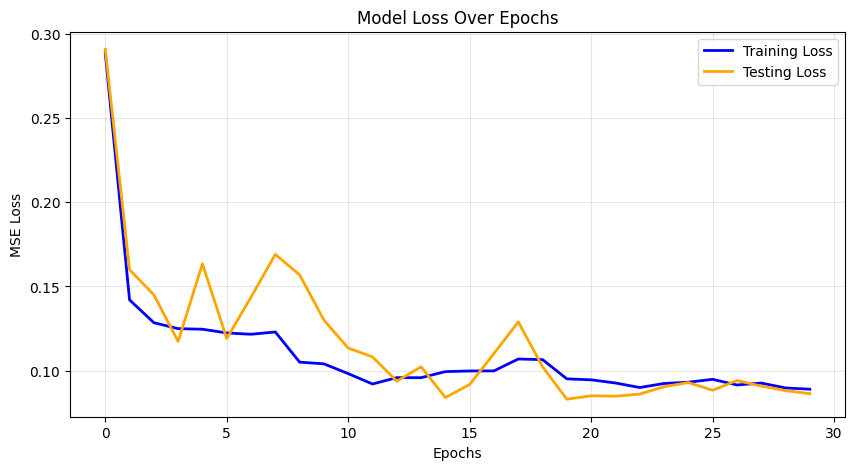

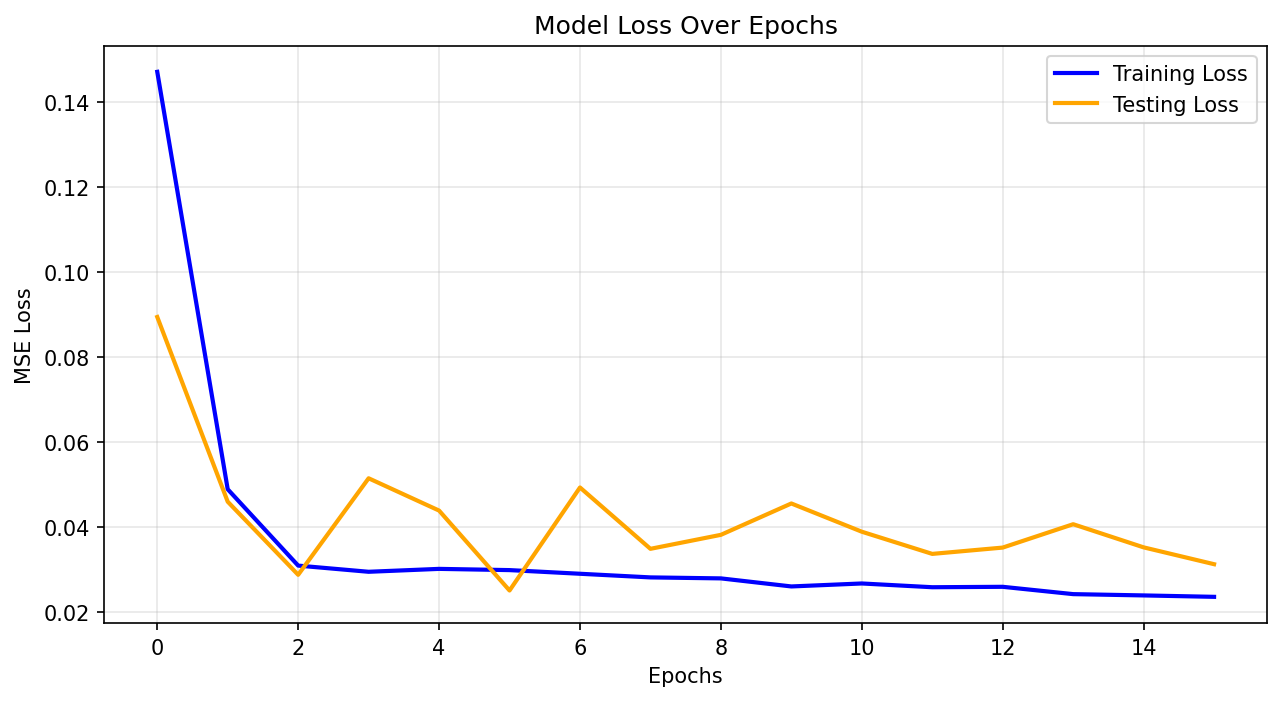

In univariate regimes, QLSTM and LSTM yield nearly indistinguishable training and test losses, both converging without underfitting or overfitting. QLSTM achieves marginally lower RMSE than LSTM, but the improvement is limited (Figure 4).

Figure 4: Loss comparison of LSTM and QLSTM models for univariate and multivariate settings.

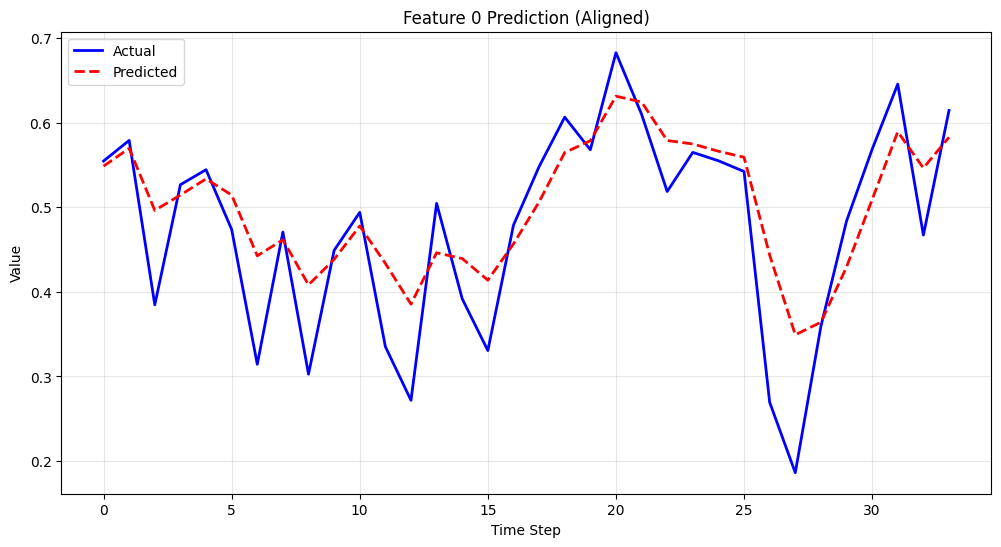

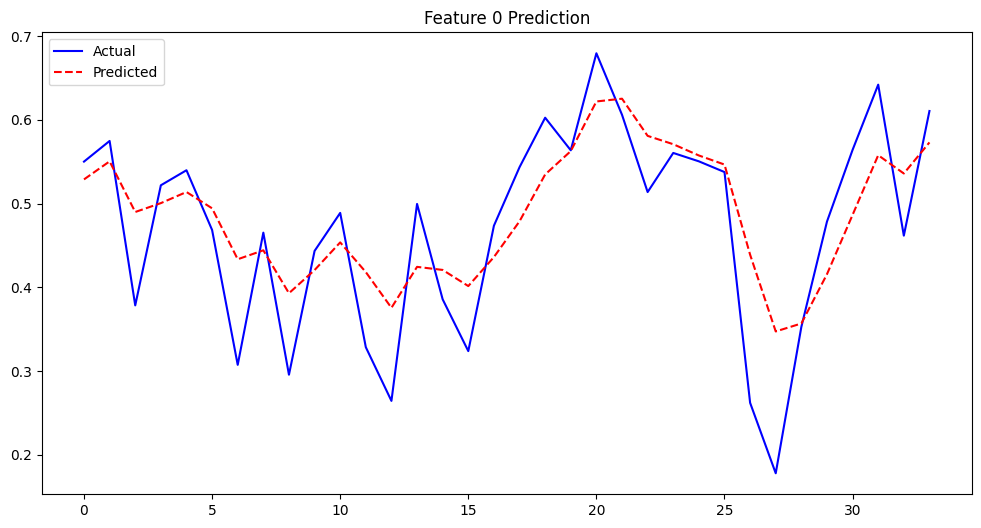

Predicted trajectories almost overlap, with QLSTM producing marginally smoother, phase-aligned predictions (Figure 5), indicating a negligible representational boost from quantum recurrence for single-channel series.

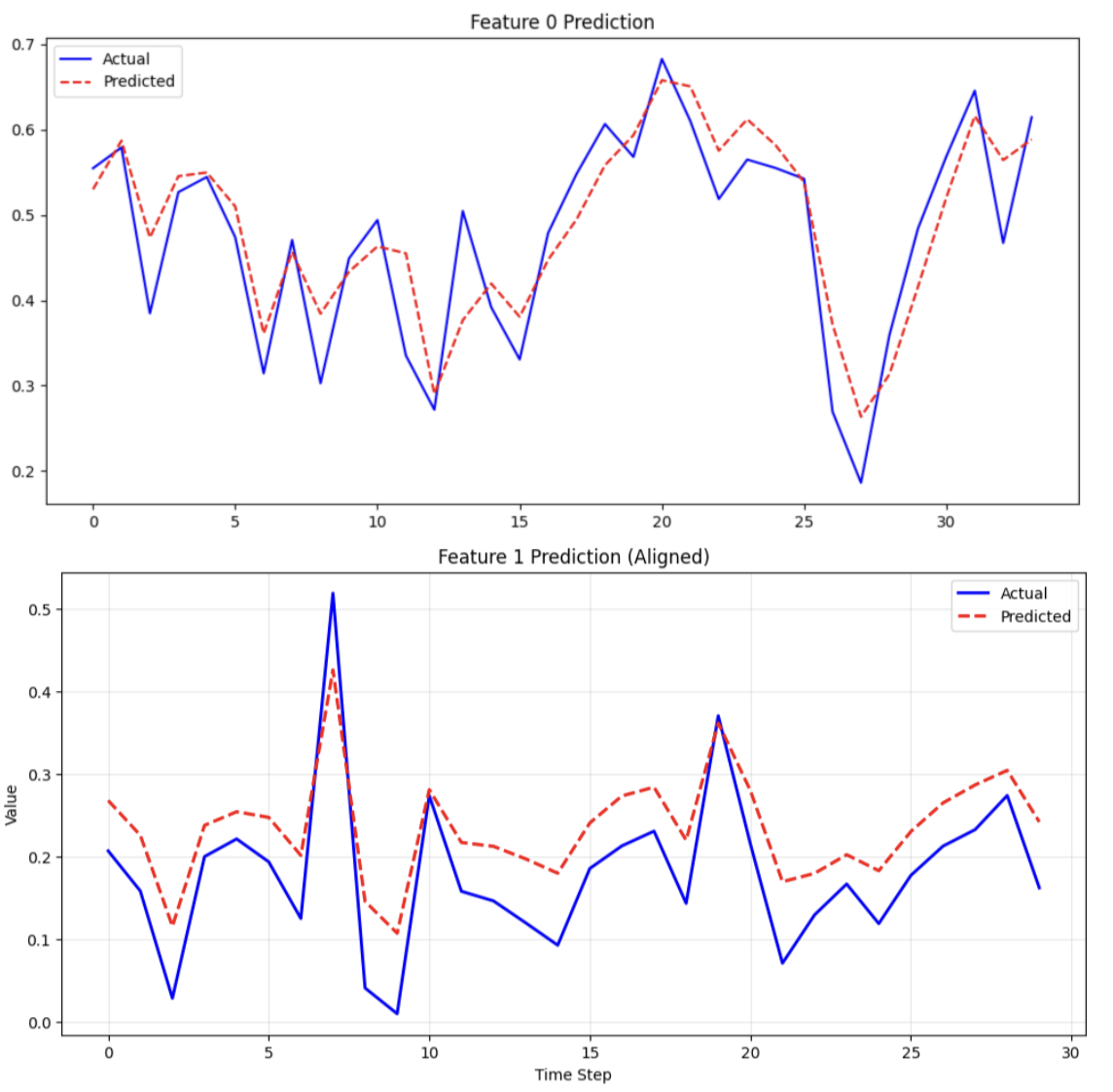

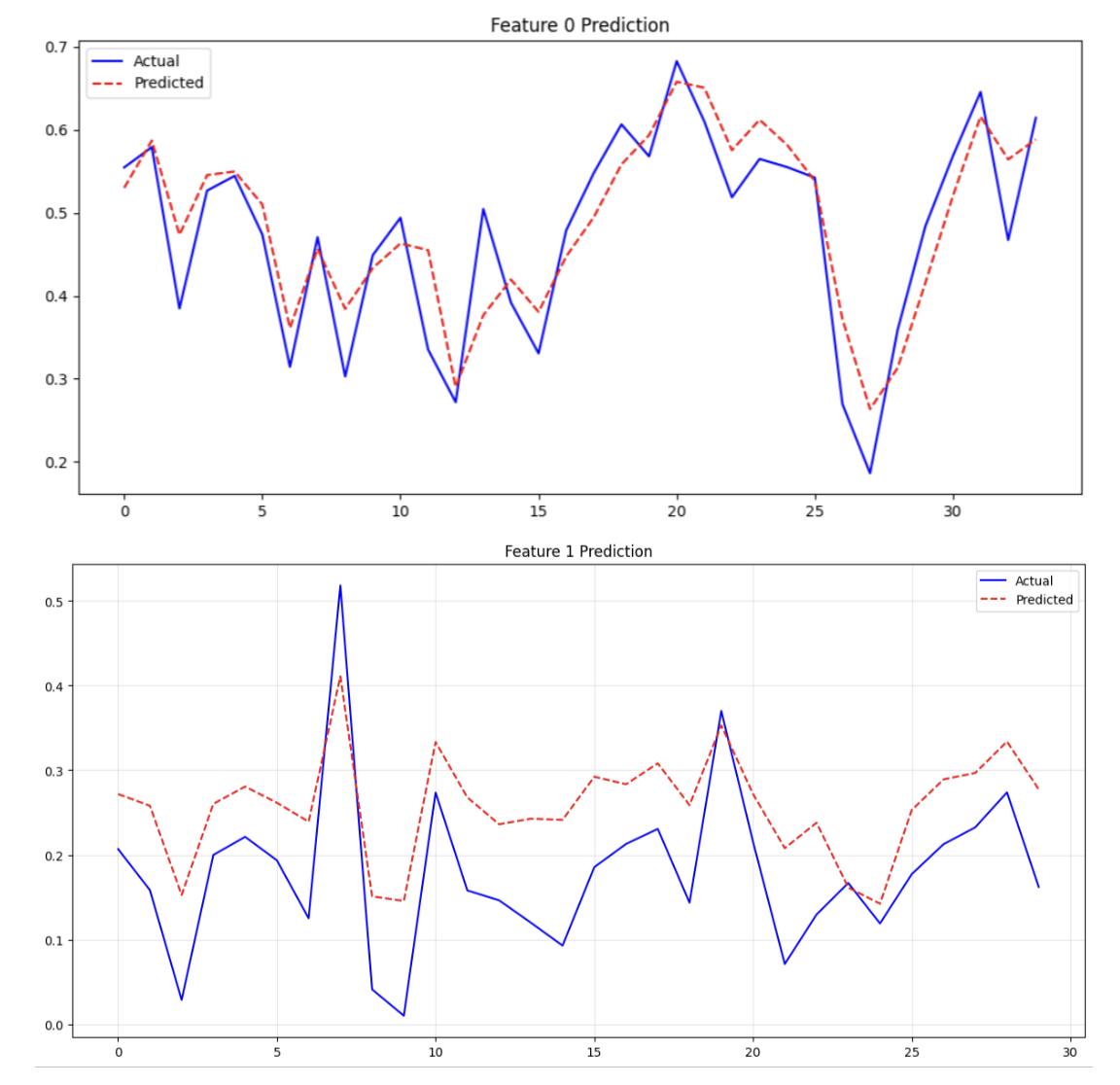

Figure 5: Prediction comparison of LSTM and QLSTM models for univariate and multivariate settings.

The situation shifts in the multivariate regime. When predicting multiple correlated series, QLSTM substantially lowers RMSE compared to LSTM in both training and test sets, signaling improved out-of-sample forecasting. Loss curves reveal QLSTM’s ability to reach lower, more stable error plateaus (Figure 4). The advantage centers on enhanced modeling of lagged cross-channel correlations and complex dependence structures, which classical LSTMs capture less efficiently under parameter constraints.

Reservoir Model Comparisons

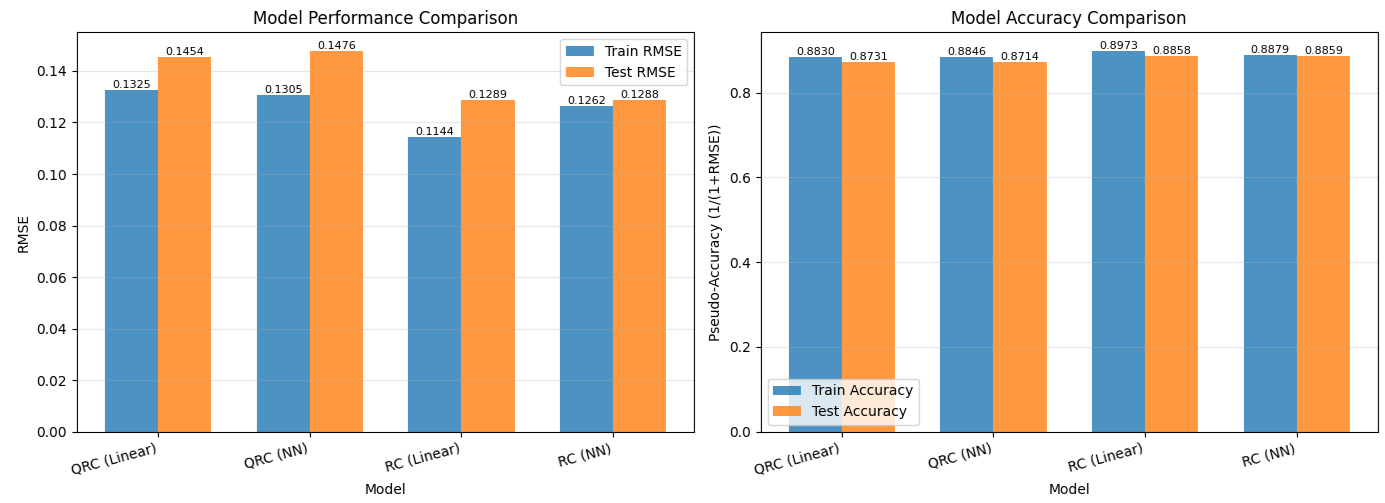

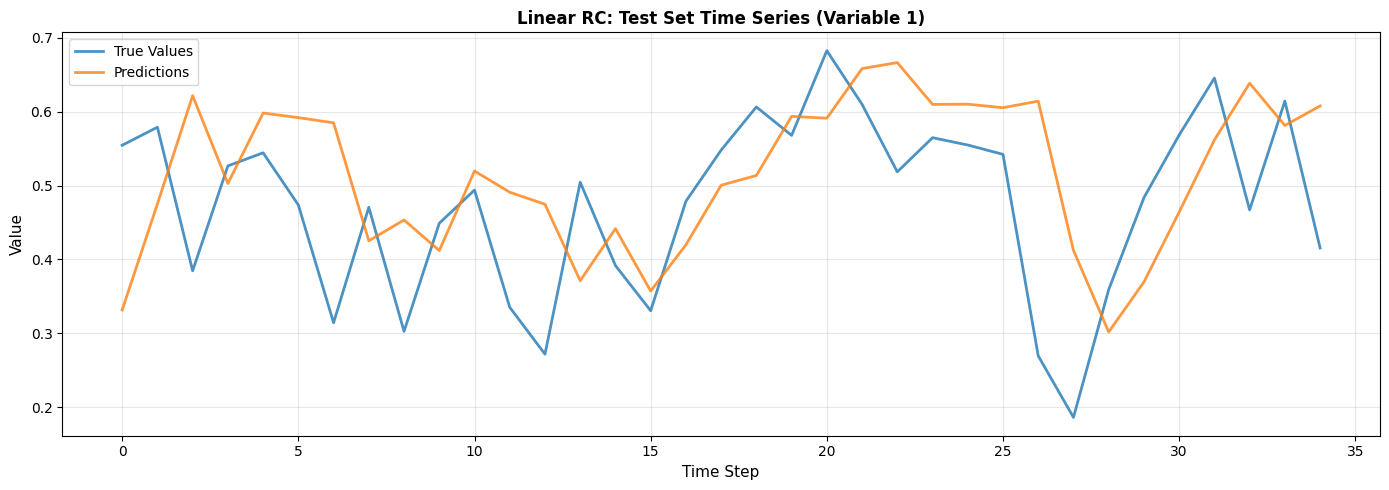

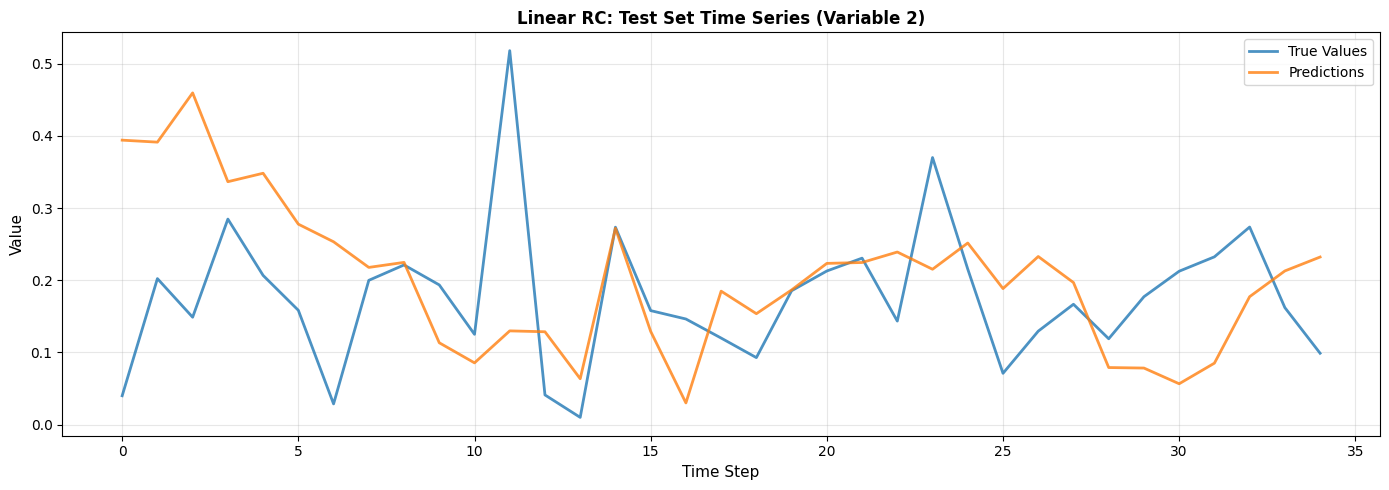

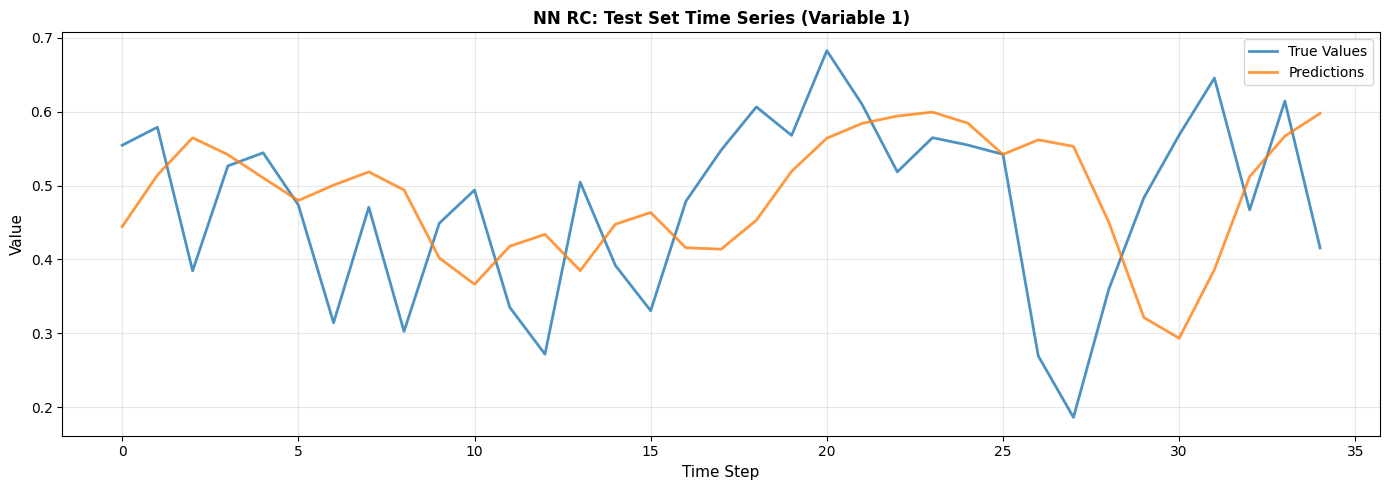

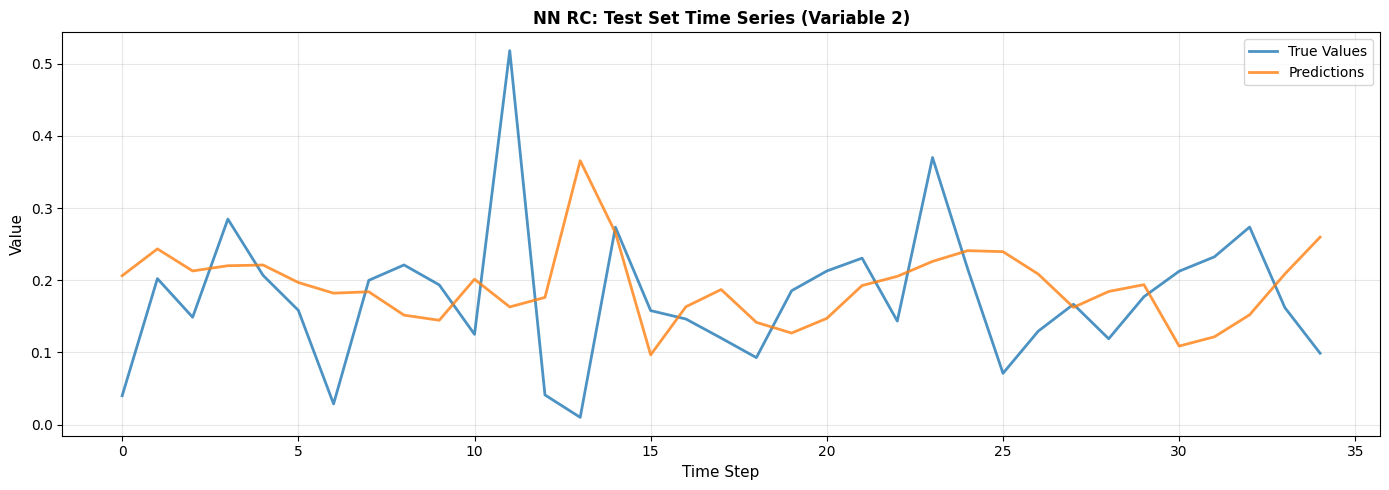

In univariate settings, QRC produces slightly higher RMSE than classical RC, with both providing accurate, robust feature mappings (Figure 6). The difference is statistically insignificant, affirming the sufficiency of classical RC for scalar financial trajectories.

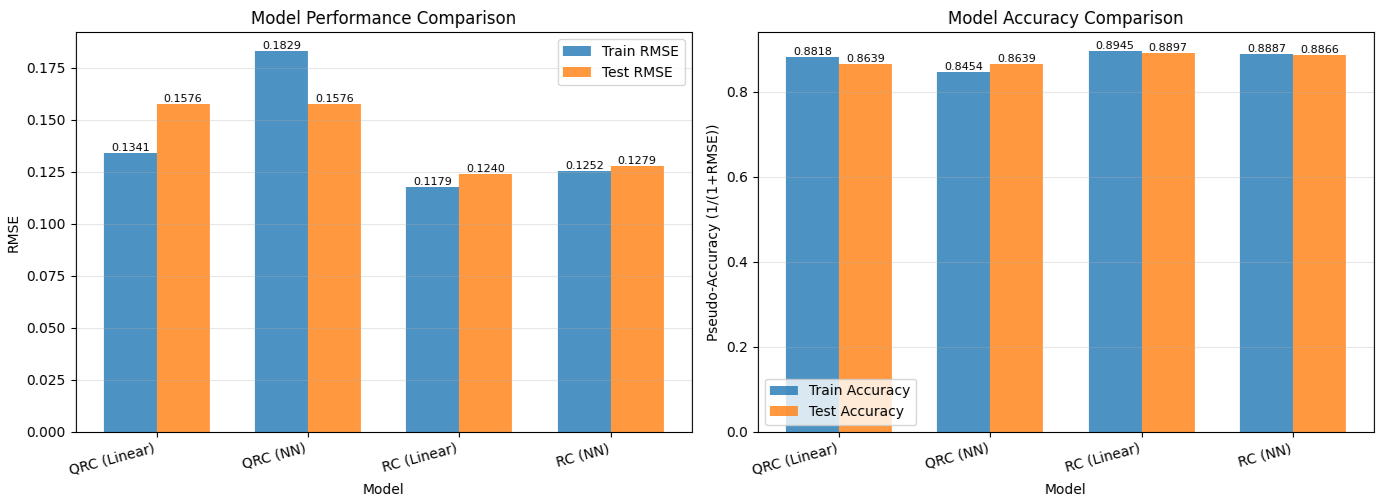

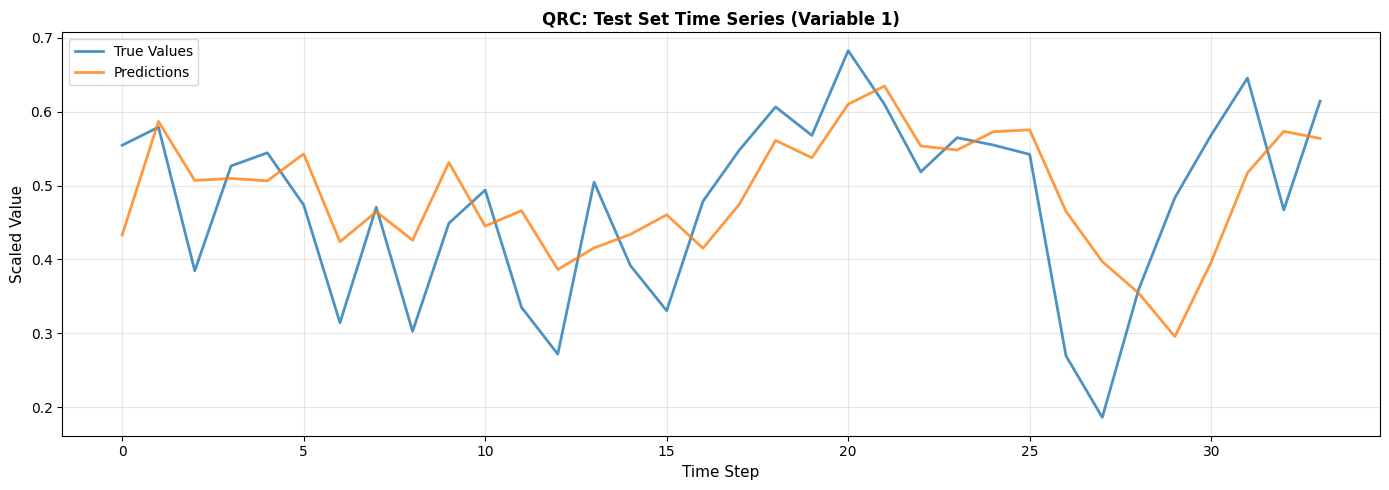

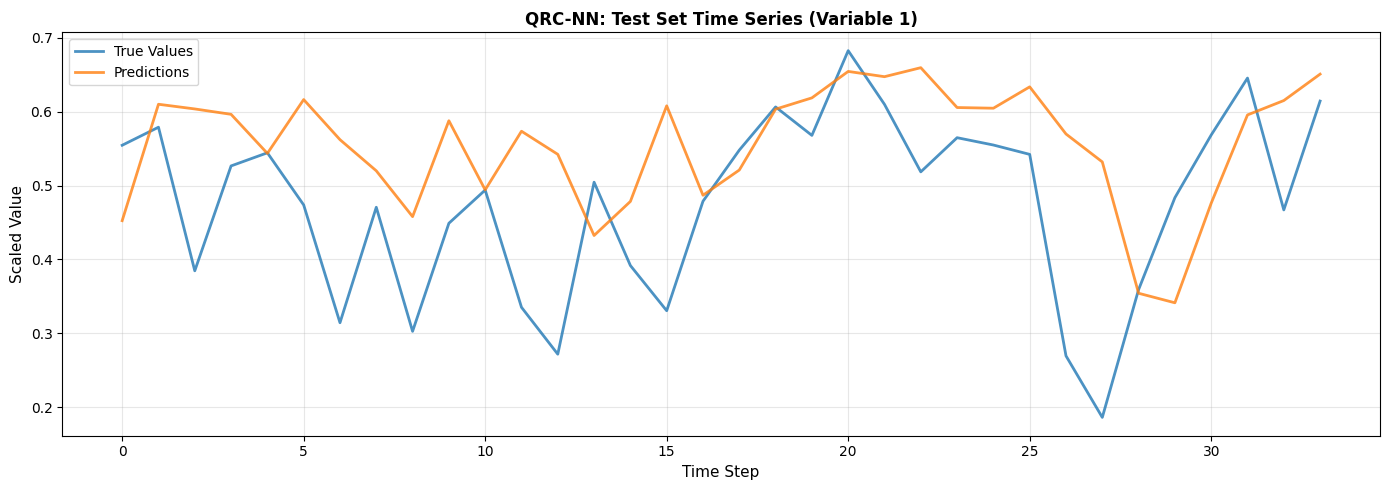

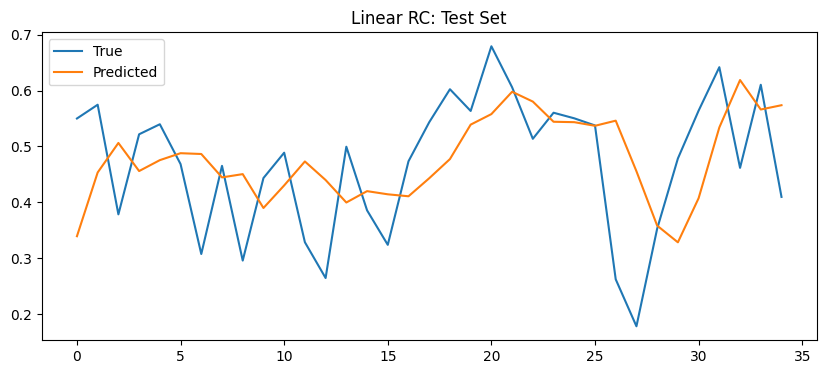

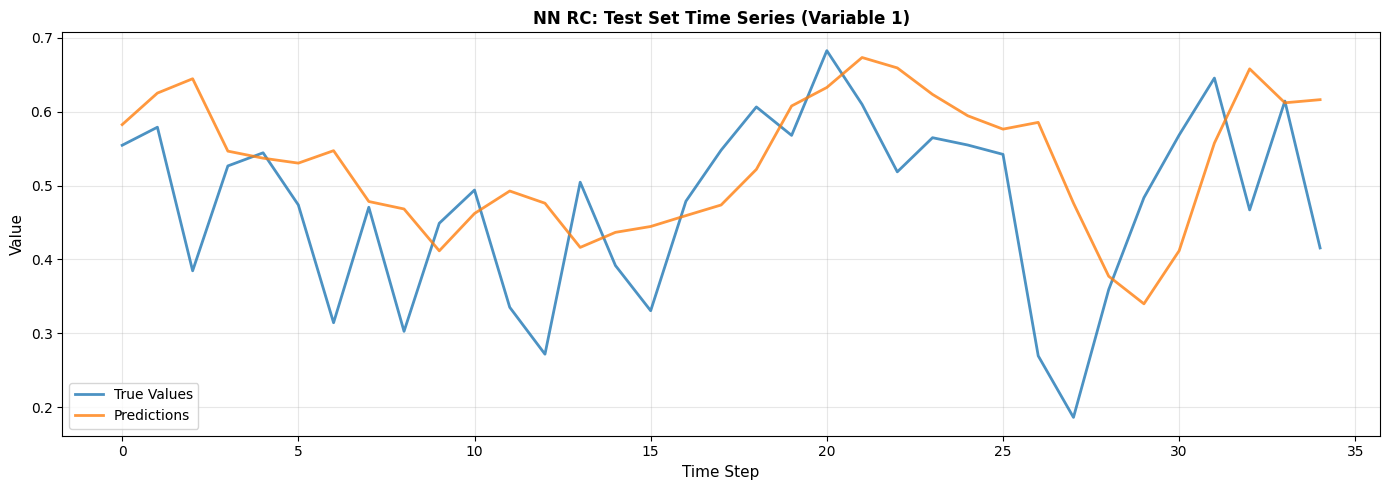

Figure 6: Comparison of QRC and RC variant tasks for both univariate and multivariate forecasting.

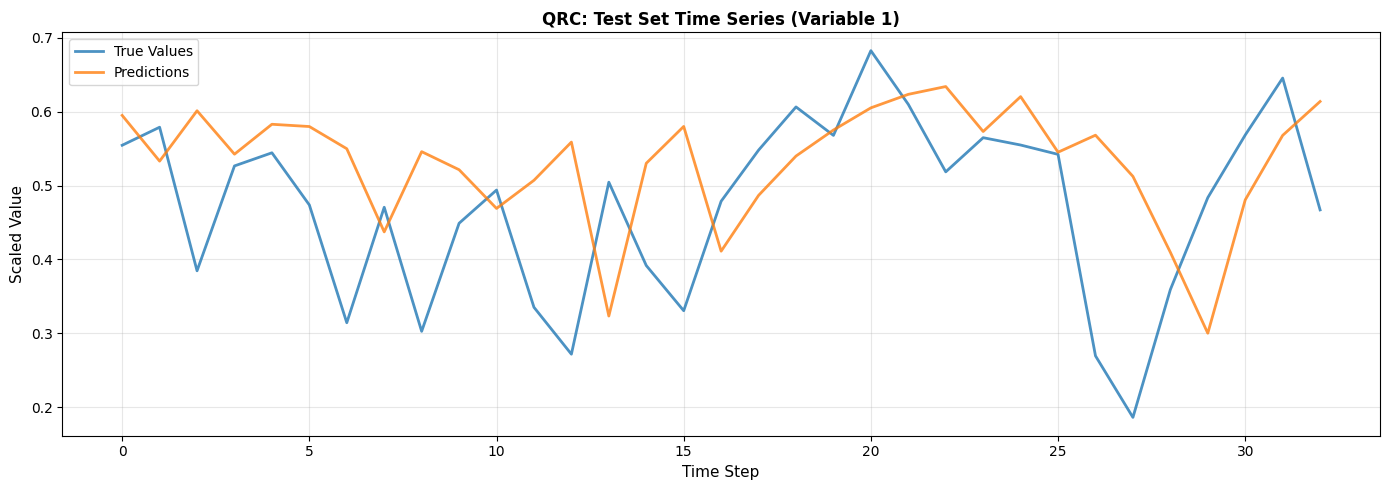

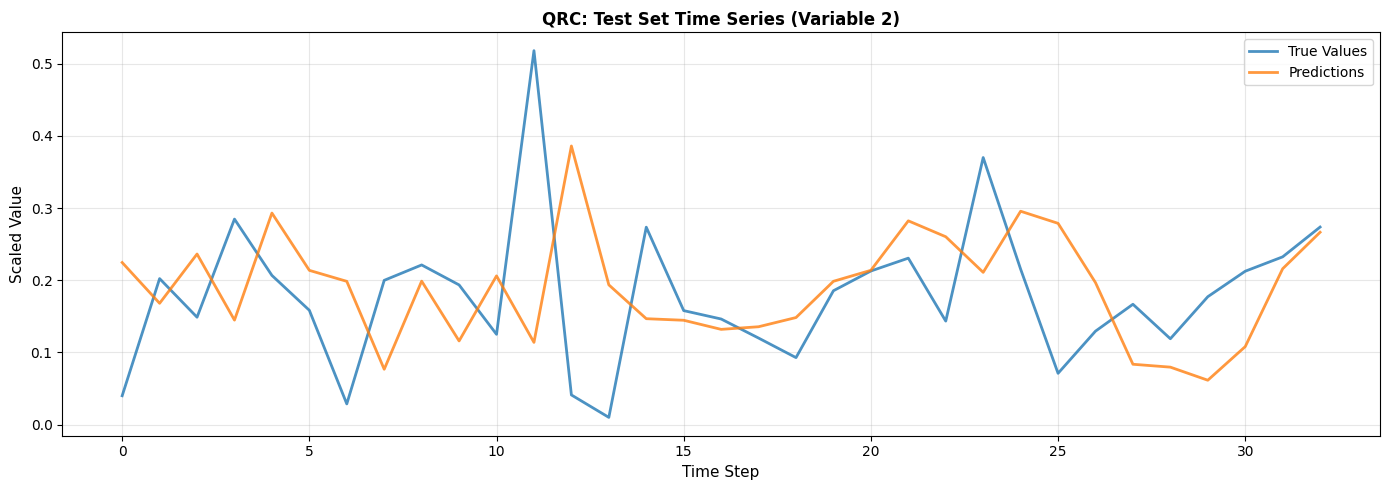

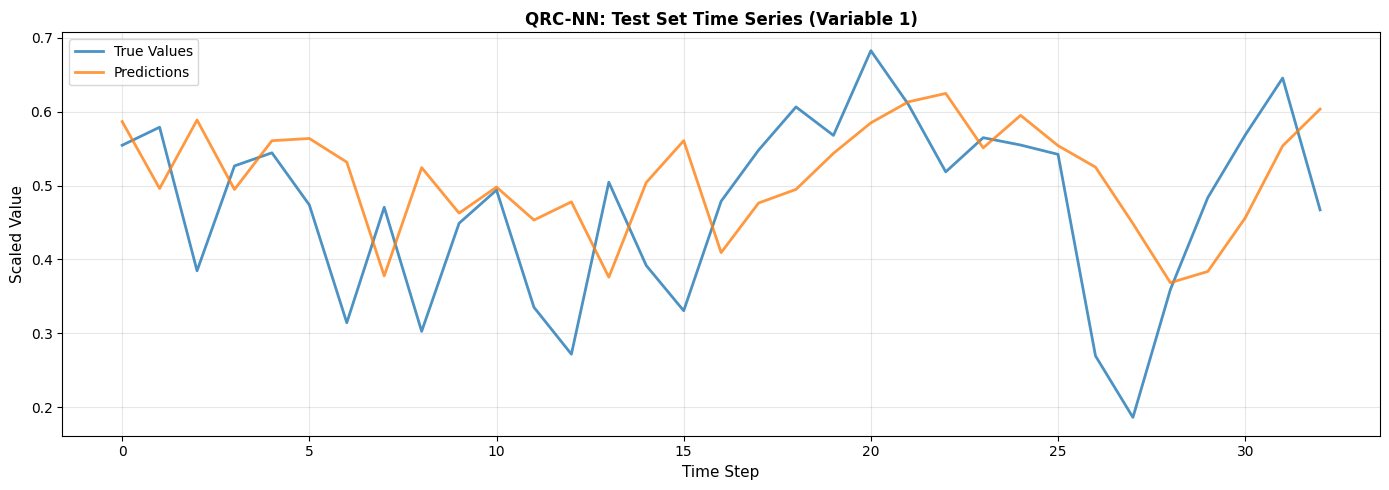

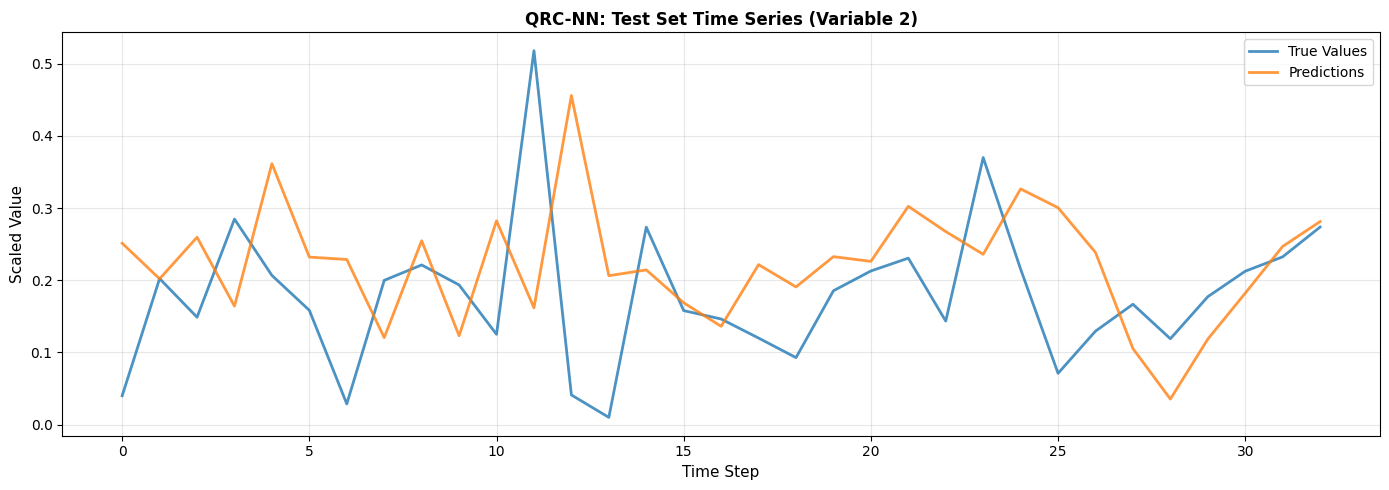

With multivariate lags, QRC consistently outperforms RC—across both linear and neural-network readouts—yielding lower RMSE and higher pseudo-accuracy (Figure 7, Figure 8). The QRC-coded reservoir better preserves both the amplitude and inter-channel temporal structure, capturing lagged cross-series dependencies otherwise under-explored by classical RC.

Figure 7: QRC and RC comparison on univariate data, demonstrating similar effectiveness in single-channel forecasting.

Figure 8: QRC and RC comparison on multivariate data, highlighting QRC’s improved capture of inter-series dependencies.

These results are replicated across real and synthetic series, with QRC demonstrating particular fitness for high-dimensional, cross-correlated financial time series scenarios.

Theoretical and Practical Implications

The study’s principal claim is that under matched resource and data constraints, quantum models—when properly encoded and optimized—can match or modestly outperform classical architectures in multivariate financial forecasting. This advantage emerges chiefly when the modeled system exhibits high cross-series correlation and complex, nonlinear dependency structure.

These findings provide a nuanced perspective on claims of quantum advantage for supervised sequence modeling in finance. The results suggest that quantum recurrent models have the greatest potential not as universal performance boosters, but rather as highly expressive, learnable feature maps in high-dimensional, strongly correlated input regimes. They also underscore the continued importance of effective quantum data encoding (amplitude encoding, random projections), classical-quantum co-optimization, and careful model capacity matching in empirical evaluations.

Future Directions

The work identifies opportunities for advancing quantum sequence learning:

- Scaling up QLSTM and QRC to larger quantum devices to further probe high-dimensional state space advantages

- Exploring alternative data-encoding (basis, angle, or Hamiltonian-based embeddings)

- Experimenting with non-standard variational ansätze for recurrent quantum gates and reservoir evolution

- Developing hardware-aware training protocols to mitigate device noise and gate errors

- Investigating hybrid quantum-classical ensembles and model selection algorithms for adaptive financial forecasting

Conclusion

This comparative analysis demonstrates that QLSTM and QRC architectures, when subjected to consistent resource and parameter controls, provide comparable or modestly improved performance over classical LSTM and RC for financial time series forecasting, with the quantum advantage primarily manifesting in multivariate, strongly correlated data settings. The results underline that quantum recurrent models offer their clearest utility as expressive, trainable feature extractors for complex, high-dimensional sequence prediction tasks, aligning theoretical predictions with practical empirical outcomes.

(2605.02656)