- The paper proposes a continuous, share-based attribution model that replaces traditional authorship order with normalized contribution shares for authors, reviewers, and replicators.

- It utilizes graph-theoretic structures—Shares, References, and Capital Graphs—to analyze academic capital and accurately measure impact.

- The system introduces market-driven metrics to incentivize quality control, enabling real-time, field-adjusted reputation and performance attribution.

Liberata: A Graph-Theoretic, Share-Based System for Academic Scientometrics

Motivation and Critique of Current Scientometric Paradigms

The paper "Liberata -- Graph Scientometrics for a Share Based System of Academic Publishing" (2605.02128) systematically deconstructs the inadequacy of legacy scientometric indicators—such as author order, citation counts, and the h-index—for a scholarly ecosystem characterized by scale, high collaboration rates, and misaligned incentives. The authors assert that current metrics, based on discrete authorship orderings and unnormalized citations, fail to capture the continuous and heterogeneous nature of research contributions. This foundational critique motivates the development of a system wherein authorship credit and impact signals are both continuous, cross-role, and incentive-compatible.

Liberata: System Construction

Shares-Based Contribution Attribution

Liberata posits an explicit replacement of authorship order and traditional fractional counting schemes with a continuous distribution of shares for each manuscript. All contributors—authors, peer reviewers, and replicators—are allocated shares satisfying normalization (sum to unity) and positivity. This modular inclusion of peer review and replication into ownership of academic capital directly integrates credit for quality control into the impact metric. Unlike proxy schemes based on author order or inferred weights from co-citation analysis, Liberata enforces explicit quantification and fungibility of contribution shares at manuscript submission.

Weighted Citations and Correction Factors

Liberata critiques the basic unweighted citation paradigm on three main grounds: indifference to context (citations may be critical or supportive), lack of normalization across fields and reference-list lengths, and credit inflation via reference list expansion. The baseline metric is a reference-count-normalized edge weight: each citing manuscript prints a unit of academic capital, distributed across its references. Optional corrections include (i) normalization by field publication rate and (ii) citation discounting by author cosine similarity, suppressing self-citation and coalition effects.

Academic Capital and Marketplace Design

A central metric, academic capital, is defined as the sum over all shares (across manuscripts and roles), each multiplied by the appropriately weighted and possibly corrected citation count. This functional allows fine-grained queries—from individuals to institutions, fields, and time bins—extending traditional h-index-style metrics to arbitrary population units and resolving issues with double- or triple-counting prevalent in contemporary practice.

The market-driven innovation lies in deploying contribution shares as currency for acquiring peer review and replication. The system’s appeal for actors is incentive-compatible: authors surrender shares in exchange for improved quality signals (potentially yielding higher expected academic capital), while reviewers/replicators are rewarded proportionally with long-term impact-based returns.

Core Graph Representations

Shares Graph

The Shares Graph GS is a bipartite network (contributors and manuscripts), with three distinct contributor-role node types (author, reviewer, replicator) and directed, continuous-weight edges representing share allocations. The quadripartite block structure of the adjacency matrix supports block-wise algebraic operations, spectral analysis, and random-walk-based measures. Notably, GS encodes the true topology and granular concentration of contribution networks, with built-in ability to resolve community structure, collusion, or anomalous credit assignments via eigenspectrum analysis and spanning trees enumeration.

References Graph

The References Graph GW is a temporally consistent, directed, weighted network over manuscripts, with edges representing normalized citation flows. The weighted adjacency is upper triangular (non-circular, time-respecting), allowing for stochastic and Gram-matrix operations used in bibliometric coupling, co-citation analysis, and neighborhood enrichment procedures. The normalization fixes the “credit printing” capacity of each manuscript to unity, modulated by corrections as desired.

Capital Graph

Composing the shares and references graphs, the Capital Graph GA encodes the actual assignment of academic capital to all contributor-manuscript pairs. All graph-theoretic diagnostics—from degree centrality to spectral clustering—naturally lift from contribution shares to realized value, enabling performance and concentration analysis over arbitrary collections.

Portfolio and System-Level Metrics

Generalization of Attribution Objects

By computing aggregate academic capital across arbitrary (M,C) subsets (manuscripts and contributors), attribution can be made at the level of individuals, labs, institutions, geographies, disciplines, or time slices. The system’s compatibility with a hierarchy of domain/department/discipline/direction tags (OpenAlex-style taxonomy) enables fine-grained classification and cross-sectional analysis.

Advanced Portfolio Statistics

The system defines and operationalizes advanced metrics analogous to the financial domain: returns, volatility, Sharpe-type ratios, concentration (HHI, Gini, entropy), diversification, and efficiency (per time or per funding dollar unit). Risk premium and risk-adjusted performance are naturally derived by benchmarking against expected field-level returns. The attribution of quality control impact (by peer reviewers and replicators) is quantifiable through the change in capital growth rates pre- and post-intervention, normalized by discipline-level temporal dynamics.

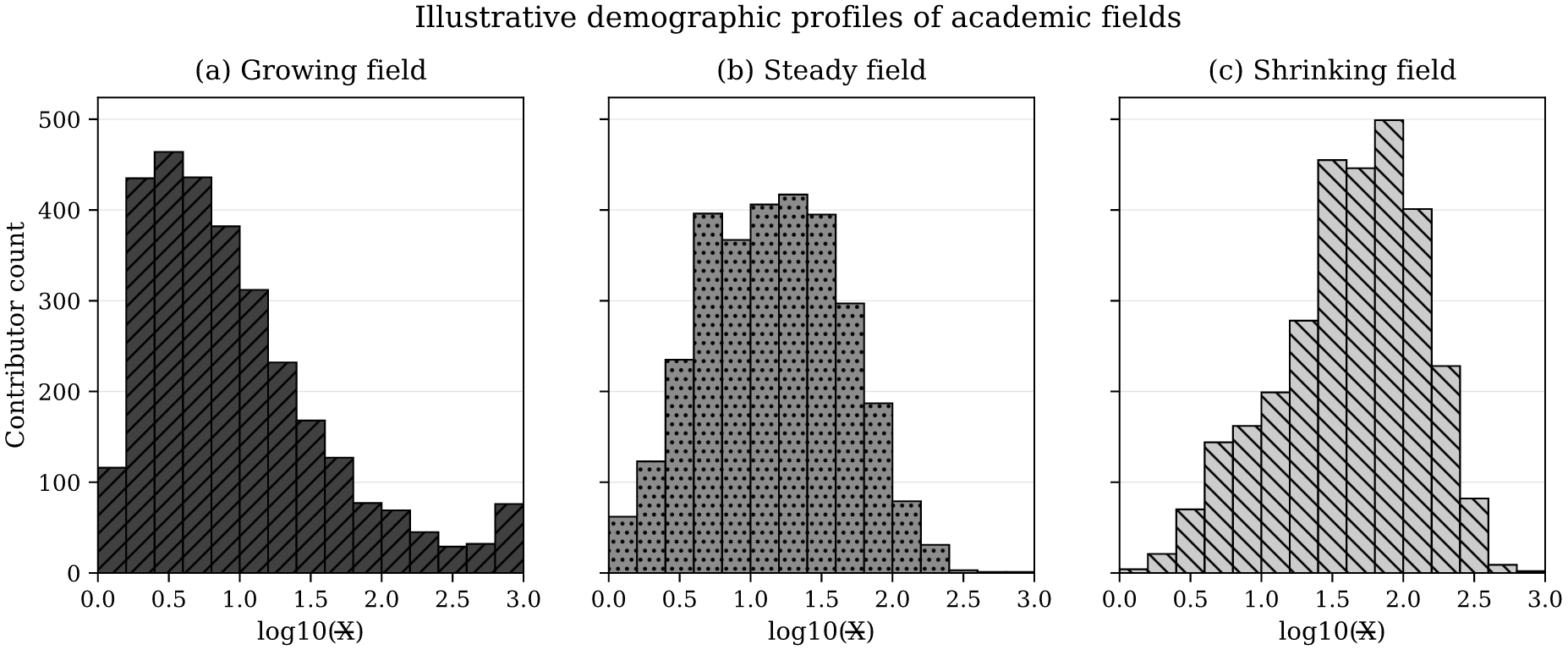

Population Distributions and Field Demography

Analysis of author share and academic capital distributions within portfolios yields field- and period-specific demographic “pyramids,” highlighting patterns of seniority, growth, and concentration.

Figure 1: Illustrative demographic profiles of academic fields.

Market Metrics and Health Diagnostics

Liberata operationalizes fair market prices for reviews and replications, field-specific risk premiums, and transactional volume, facilitating longitudinal studies of system efficiency, cost, and equity. Relative price shrinkage (e.g., of peer review in units of share) and volatility serve as meta-level health signals: e.g., decreasing price signifies systemic efficiency in quality control, higher volatility may indicate instability or unresolved areas of trust.

The system supports global efficiency metrics (capital per dollar, per GDP, per time) and inequality measures (Gini, HHI) at the regional level, enabling policy-relevant analysis of how funding structure and research concentration impact scientific output and diffusion.

Exploit Detection and Modular Corrections

Liberata is designed with modularity at the correctional level; multiple reference graph modifications can be composed (time modulation, impact dampening, richer normalization), yielding a “suite” of academic capital variants. The approach is robust against exploits such as self-citation, citation cartels, and field-skewed inflation. Systemic checks (Laplacian eigenvalues, degree distributions, author similarity discounting) allow for real-time or ex-post detection of anomalous patterns and credit laundering.

Implications and Outlook

The proposed architecture formalizes an extensible, share-based, incentive-compatible framework for scientometrics grounded in graph theory and market mechanisms. The formalization is parameter-rich, modular, and admits substantive comparison to and generalization of existing methods (fractional counting, PageRank, field normalization, author order heuristics). By integrating review and replication as credit-holding roles rather than externalities, the system aligns incentives for both quality generation and control.

The theoretical implications extend to improved measurement fidelity for science-of-science studies: concentration, interdisciplinarity, collaboration, and portfolio diversification become quantifiable at any desired resolution, with modular corrections to address field effects or exploitable incentives. Market signals emerge naturally from platform activity, enabling field-level benchmarking and risk discovery.

From a practical perspective, adoption would enable real-time, field-adjusted reputation and performance attribution among individuals, labs, and countries; empower portfolio management at the institutional level; and counteract inflationary or political practices by arming funders, journals, and policymakers with robust, cross-field comparable metrics.

Conclusion

Liberata advances a comprehensive, graph-based, share-driven framework that subsumes and corrects for legacy academic metrics, integrates quality control as a first-class credit-receiving operation, and deploys modular market and system health measures. It is positioned as a reference implementation and analytical foundation for platform-centric, incentive-compatible academic publishing. The implications for future AI-driven, data-informed research funding and policy, as well as the detection of emerging fields and exploitation, are substantial.