- The paper introduces a spectral Markov approach that decouples core identification from full TTC allocation, achieving asymptotic optimality.

- It leverages randomized SVD to compute the leading eigenvector, resulting in a 22.8x speedup and over 99% core identification accuracy in large, sparse markets.

- The methodology ensures Pareto efficiency, individual rationality, and strategy-proofness, making it suitable for real-world applications like school choice and housing assignments.

Fast Core Identification in One-Sided Matching Markets

Problem Motivation and Complexity Separation

The paper "Fast Core Identification" (2604.25954) addresses the computational bottleneck in identifying stable allocations (core) in one-sided matching markets, especially under the Top Trading Cycles (TTC) mechanism. Traditional TTC algorithms, including applications in school choice, housing, and kidney exchange, exhibit O(nlogn) computational complexity. This limits scalability for large markets requiring real-time responsiveness. The paper establishes a formal complexity separation: identifying which agents receive a core allocation (the Core Identification Problem, CIP) is strictly easier than computing the full TTC allocation.

Spectral Markov Approach and Algorithmic Innovation

The proposed method leverages spectral analysis of a preference-derived Markov transition matrix:

- Agent preferences are mapped into a Markov matrix U, with normalized transition probabilities reflecting ordinal rankings.

- The leading eigenvector π is computed via randomized SVD, exploiting fast matrix multiplication and parallel hardware, with theoretical complexity O(Ln) (for top-L preferences) and practical O(n) in large, sparse settings.

- Core membership is determined by the maximum coefficients in π. Agents with highest steady-state probabilities are guaranteed to receive core allocations.

This marks a strict improvement over prior methods, matching the information-theoretic lower bound and achieving asymptotic optimality. The algorithm preserves TTC properties: Pareto efficiency, individual rationality, and strategy-proofness.

Figure 1: The TTC cycles for a numerical example, illustrating core agent selection via Markov eigenvector sorting.

Robustness, Properties, and Model Analysis

Steady-state Markov properties (Theorems 1–4) underpin the methodology, with proofs referencing the Perron-Frobenius Theorem and spectral graph theory. Strong connectivity ensures the existence and uniqueness of the stationary distribution, aligning core agent identification with network centrality (PageRank-like interpretation).

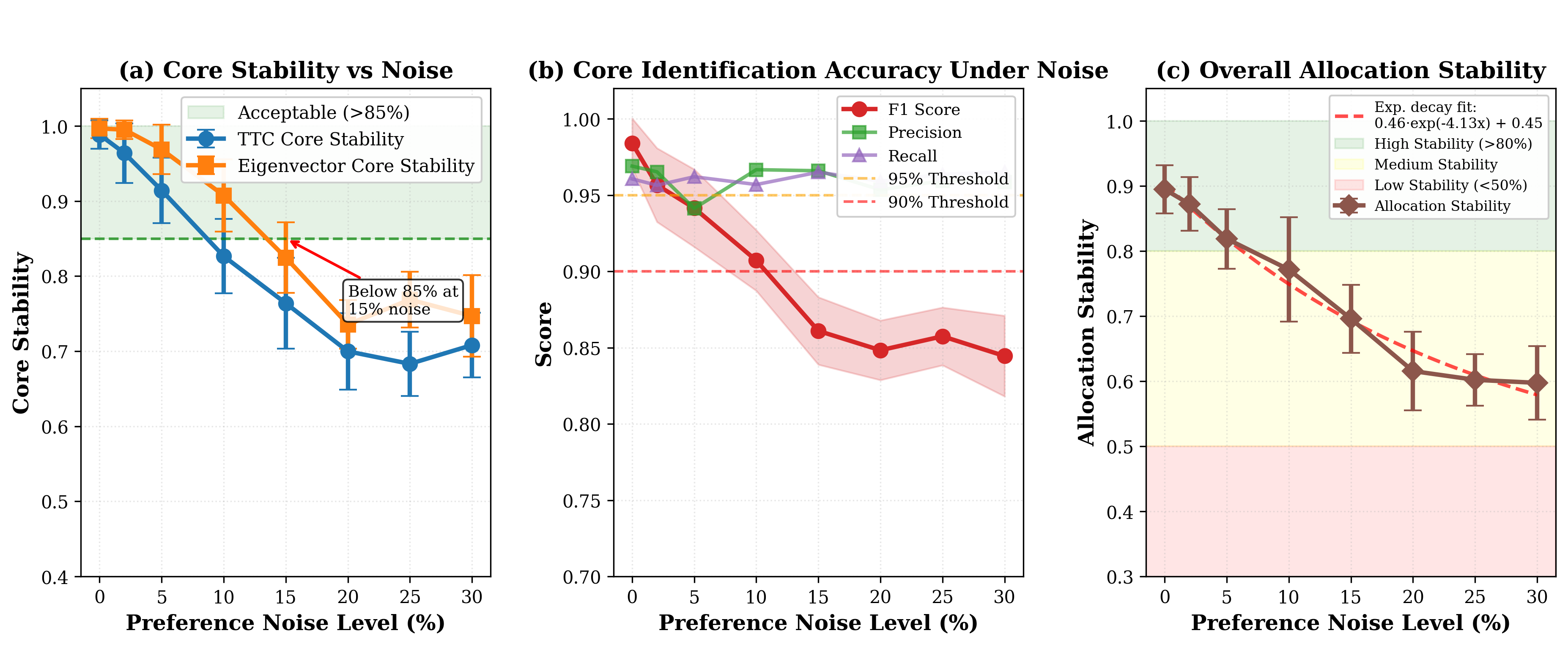

The eigenvector-based process demonstrates robustness to preference noise and misreporting—small perturbations in reported preferences do not materially affect the steady-state probabilities or core membership for sufficiently large n. This is formally justified via spectral perturbation arguments.

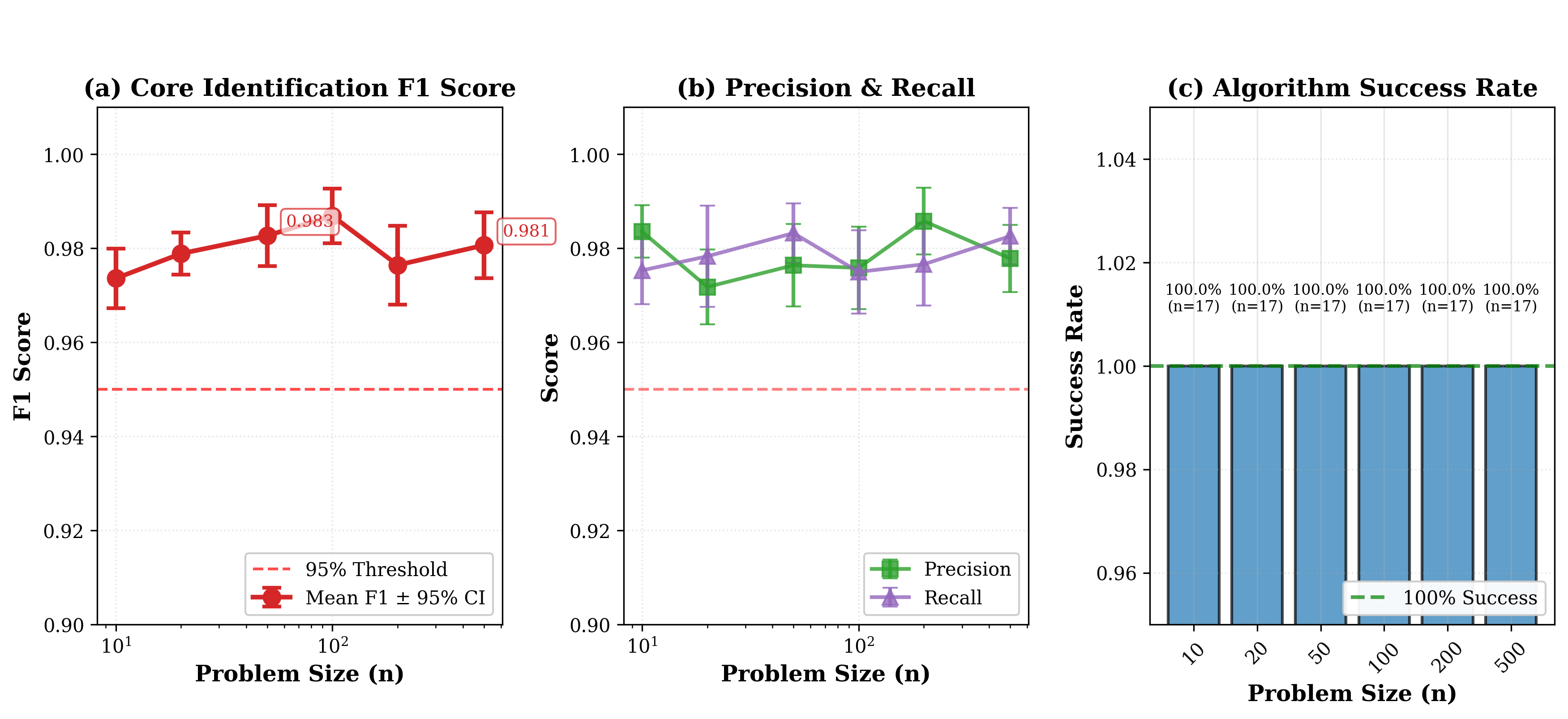

Figure 2: Precision and recall of core identification as a function of n, evidencing near-perfect accuracy for moderate and large markets.

Figure 3: Robustness of the core identification method against random preference noise.

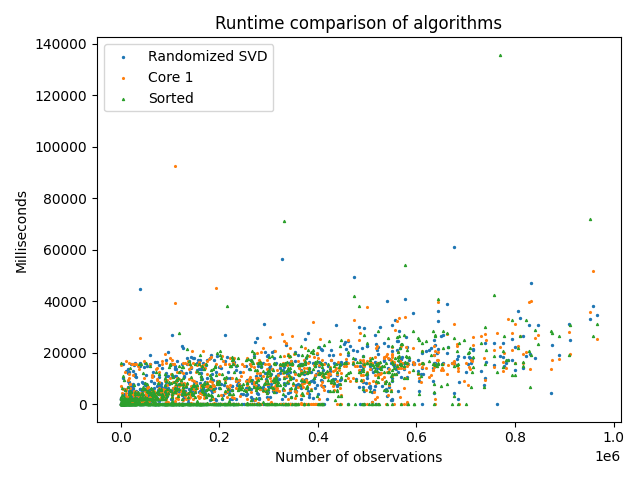

Experimental Results and Speedup

Extensive computational experiments benchmark the proposed approach. Results indicate:

- Core identification accuracy exceeding 99% for n≥100.

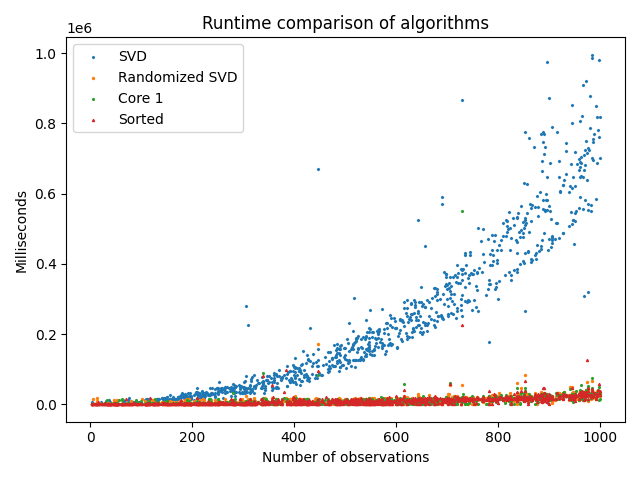

- Empirical speedup grows rapidly with U0; for U1, the spectral method is 22.8x faster than standard TTC allocation computation.

- No significant time difference between randomized SVD, U2 extraction, and sorting operations, confirming theoretical predictions.

Figure 4: Wall-clock runtime comparison of traditional SVD versus randomized SVD, evidencing dramatic temporal gains for large matrices.

Figure 5: Visualization of the first eigenvector via randomized SVD with maximum and sorting steps, confirming rapid identification of core agents.

Theoretical and Practical Implications

This work contributes a novel complexity separation for algorithmic matching markets. Practically, it enables high-frequency, scalable core identification for applications such as real-time school choice, housing assignment, and digital asset exchanges. Theoretical implications include:

- Established linkage between spectral stationary measures and matching allocation stability.

- Robustness guarantees support adaptability in noisy and incomplete preference environments.

- The framework can be extended to continuous preference models, dynamic reallocation, and non-square agent-object scenarios via matrix padding.

Conclusion

"Fast Core Identification" provides a rigorously justified, spectrally-driven algorithm for stable core identification in matching markets, with optimal complexity and robust performance properties. The method is widely applicable in modern economic allocation problems, offering both practical speed and theoretical clarity. Spectral approaches are poised to become a central toolkit for large-scale, exact, and approximate matching mechanism design.